aluxum

aluxum

I believe there is a good investment opportunity being created in emerging markets. Considering the Fed's monetary policy outlook and the direction of the world economy, I look with great interest at developing market equities.

More specifically, in my opinion, the real driver of growth in these emerging countries could be found in the Internet services.

We must first, however, also answer another question: Which emerging country? As you well know, the answer is not easy, especially in 2024. Would you include China in emerging markets? In my opinion, China must remain in these lists for a series of motivations that will be discussed later in this article.

For these reasons, I follow EMQQ The Emerging Markets Internet & Ecommerce ETF (NYSEARCA:EMQQ), with great interest. In my opinion, this ETF is extremely relevant as it is generating alpha.

According to the World Bank's estimates, the possibility of a soft landing for the Federal Reserve is increasing. The prospect is for a softer policy as early as 2024, and although, at this moment, markets seem to be betting on a postponement of the first cuts, a lightening in the monetary policy remains a probable event. The dollar could weaken itself, especially given the bullish hypertension it has experienced in recent years, and capital could shift to economies with better growth rates, such as emerging countries. Given the convenience of the Chinese stock market, it could become tempting for investors to diversify towards this sector as well, which seems to have almost been abandoned by investors, perhaps forgetting that it is the world's second-largest economy in terms of size and with growth rates worthy of an emerging economy, despite all the problems involved.

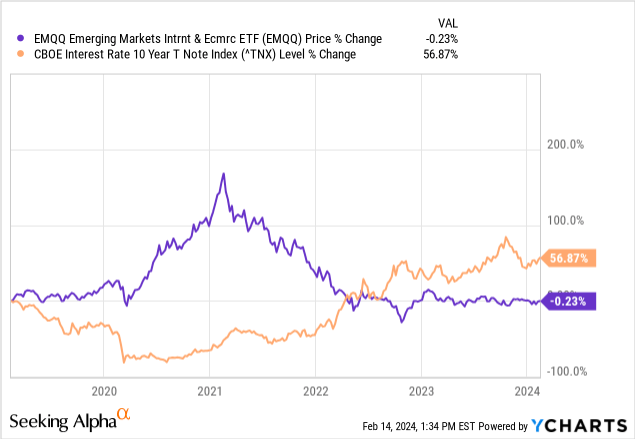

Source: YCharts: The Graph displays an inverse relationship between the two variables. The DXY tends to exhibit an opposite trend in comparison to the EMQQ, yet aligns with the movement of interest rates.

You might be thinking, "Okay, I get it, but why specifically an ETF focused on the Internet and E-commerce?"

The Internet effort is the key to overcoming all the concerns that have intimidated investors in recent years.

As highlighted in the report "The future of digital transformation in emerging markets" of OECD, the digitalization of Emerging Countries and the adoption of digital technologies are improving the efficiency of small and medium-sized enterprises ((SMEs)), stimulating the productivity in these countries. India, for example, has implemented a national "tech stack" :a set of state-sponsored digital services that connect Indians with the digital universe, such as payment and tax systems, and bank accounts.

The rapid adoption of these platforms has forced the digitization of the country.

Recent innovations and the introduction of broadband systems could have an even greater impact on the size of the communication markets, IoT, and digital payments.

The EMQQ follows the EMQQ The Emerging Markets Internet & Ecommerce Index, designed by EMQQ Global LLC, providing a complete replication.

Created by Big Tree Capital LLC and co-managed by Penserra Capital Management, LLC, the ETF includes companies with significant exposure to the Internet and e-commerce sector, based on specific eligibility criteria.

It uses a modified weighting methodology based on floating market capitalization and is rebalanced semi-annually.

The ETF aims to provide direct exposure to the evolution of Internet and Ecommerce solutions in China and other Emerging Markets.

It has an AUM of $358.45M and an Expense Ratio of 0.86%. It has 43.84% exposure to Consumer Cyclical and 28.77% exposure to Communication.

The technology component is really minimal as it amounts to 4.83%.

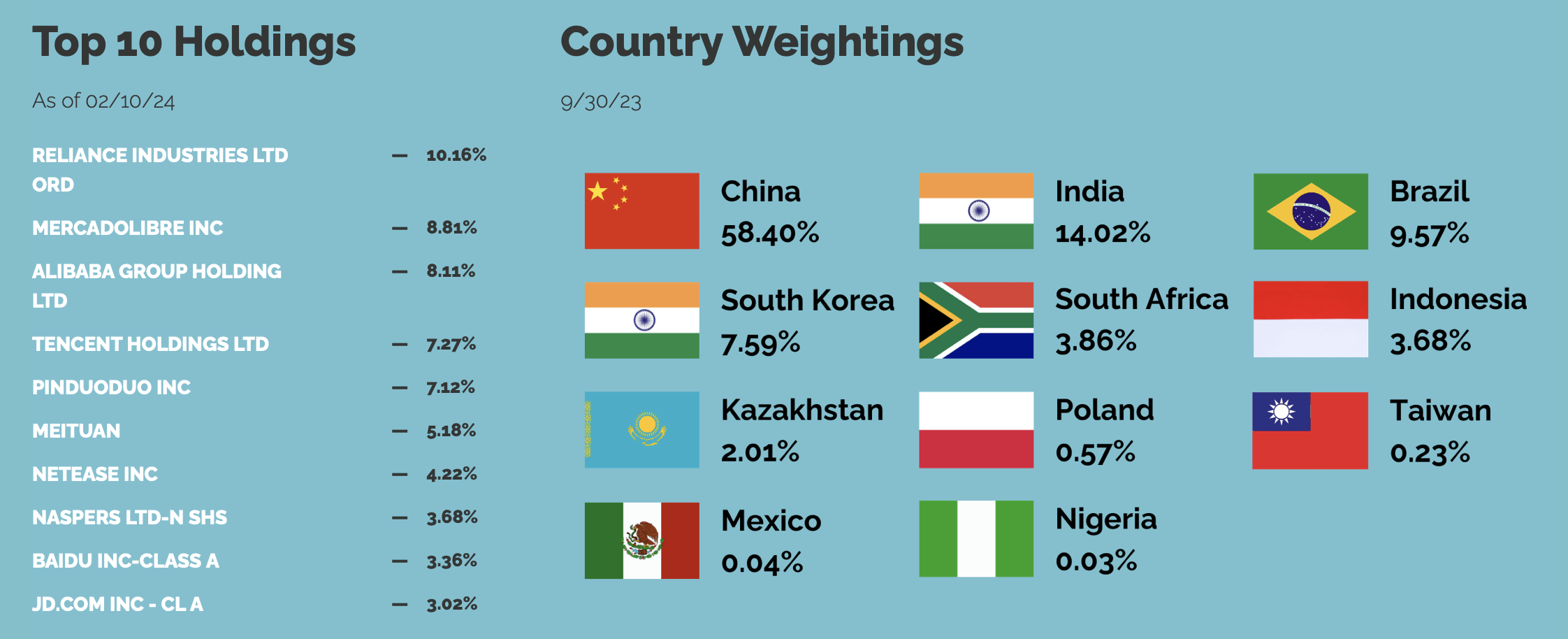

The top 10 holdings cover about 61% of the fund capitalization, as shown in this table.

Top 10 Holdings and Country Weightings of EMQQ ETF (emqqetf)

Geographically, it has 58.4% exposure to China, making it highly dependent on the performance of the Chinese stock market. The other two largest geographic areas are India and Brazil, accounting for 14.2% and 9.57%.

Regarding the Chinese companies included in the ETF, I reaffirm my positive outlook.

For this reason, I prefer to focus, in this context, on the other two most significant geographic areas of the ETF: India and Brazil.

In order to gain a comprehensive overview of all the Indian and Brazilian companies in which the ETF invests, I invite you to open this report and proceed directly to page 9.

The ETF's top 10 holdings, excluding the China geographic area, include Reliance Inc., MercadoLibre, Inc. (MELI), and Naspers Ltd.

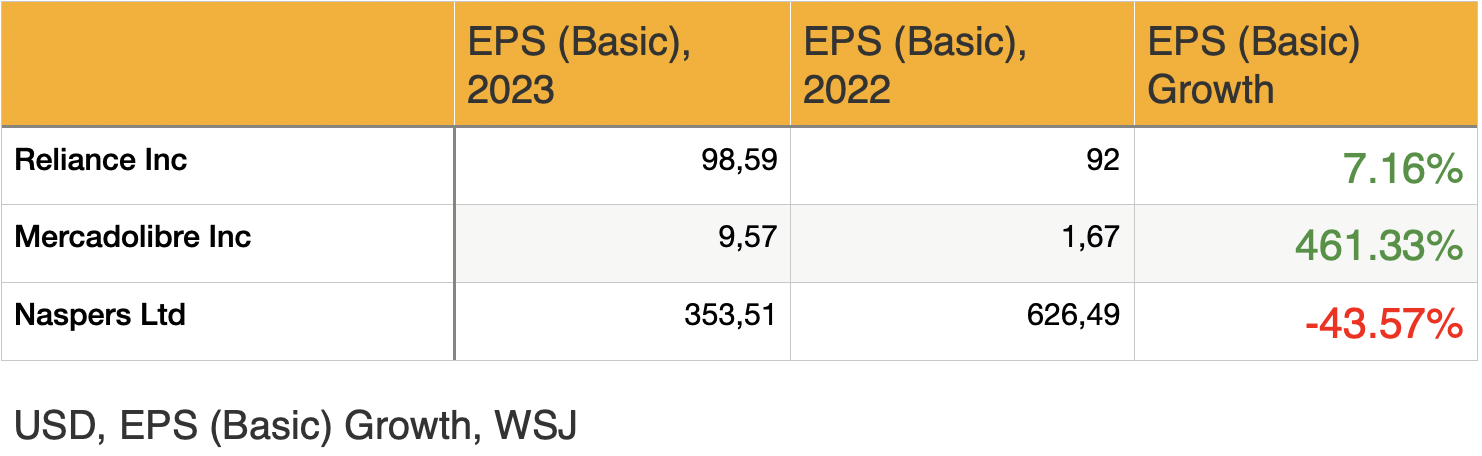

Comparison of EPS growth | Reliance Industries, Naspers, MercadoLibre. (Reprocessing of data from WSJ)

All the top 10 holdings have recorded strong earnings per share (EPS) growth over the last two years, except for Naspers Ltd., which has shown rather volatile performance. Although it experienced an EPS growth of 208.10% between 2021 and 2022, there was a contraction of 43.57% from 2022 to the past year.

Among the ETF's largest capitalizations, Naspers Ltd. raises the most concerns.

There are basically three critical points to think about: The first is the low-priced affordability: the benchmark's average P/E is 22.02, which is higher than its peer KraneShares CSI China Internet ETF (KWEB) of 19.55, which similarly has not been able to benefit from the price growth of the Indian and Brazilian stock markets, as it is 100% China-facing. As a comparison, the iShares MSCI Emerging Markets ETF (EEM) has a P/E of 11.14.

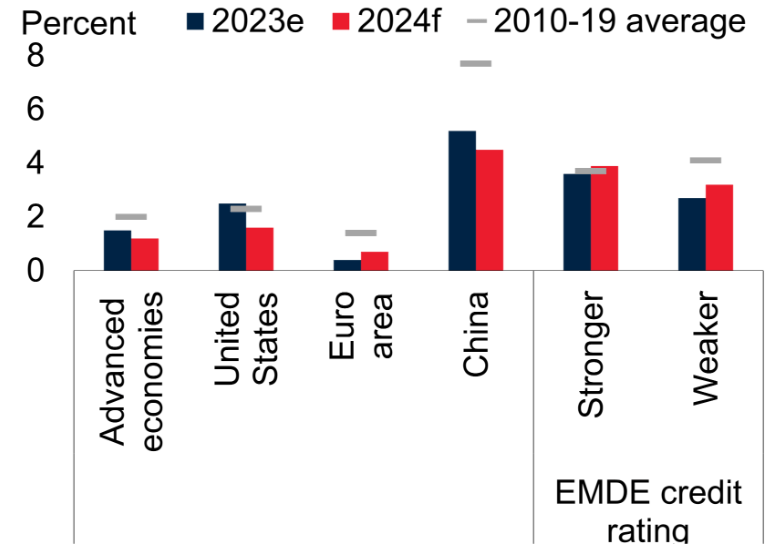

The second is the prevalence of Asian stocks: 75% of its holdings are concentrated in three East Asian countries; more than 50% in China. The latter's economic data showed a poor ability to meet analysts' expectations. Therefore, such pronounced exposure to the Chinese e-commerce and internet market is alarming. As can be seen from the chart, although emerging markets with stronger credit ratings are projected to maintain economic value, the same does not seem to apply in China (for now).

Growth, by economy and EMDE credit rating (Moody's Analytics; World Bank.)

However, there is an issue about the ETF expense Ratio: the expense Ratio is 0.86%, among the highest in its class. This could sink the net performance of one's investment in the long run.

The EMQQ ETF is in fact largely composed of Asian stocks, particularly Chinese ones. I personally do not see this as a feature to be seen in a negative sense. Rather, it is a response to a specific need: the digitization of developing economies. And willing or not, China plays a key role in this process, both from a social point of view, and from a technological point of view. Of course, if you are looking for an investment solution that won't expose you to China-related risks, this is not the right choice.

As far as the Expense Ratio is concerned, it is objectively above the peer average and amounts to 0.86%. When we move to these kinds of thematic ETFs, however, the Expense Ratio averages above 0.50%. For example, among its Peers is the KWEB, with an Expense Ratio of 0.69%.

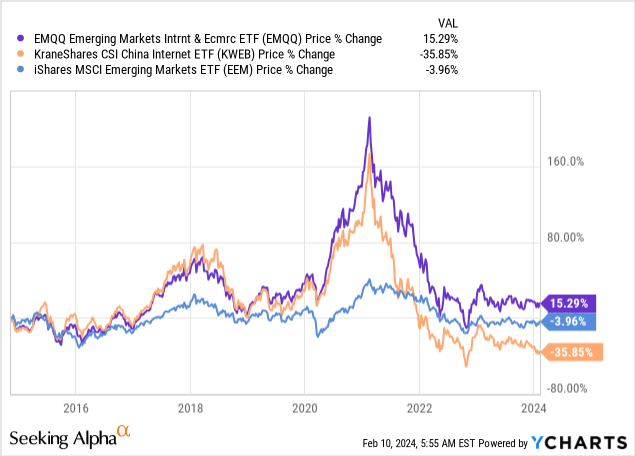

Finally, normalizing the returns in percentage terms of the EMQQ and comparing them with its peers, an important consideration comes to light.

EMQQ's returns in percentage terms in the last years have been higher in comparison to the ones of the peers.

The evidence arose after 2020 when digitalization became a "must" for the emerging countries as well. According to my point of view, this alpha expressed in terms of return could continue to play in the future.

Therefore, the Expense Ratio and high P/E have historically been partly justified and reduced by the ETF's returns.

To summarize, I will pay particular attention to the evolution of the financial statements of the companies composing the ETF EMQQ rather than the economic growth of emerging countries, as I strongly believe that digital tools will be the key to economic expansion.

The ETF in question represents a smart investment solution for those who are interested in China, but also in India and Brazil. As expensive it appears, the expense ratio is justified by the performance, which has been historically higher in the peers utilized in the last years.

Unequivocally, the convenience of P/F of the EMQQ has largely depended on the crush of Chinese stocks. Therefore, a potential recovery is strongly linked to the performance of the Asian colossus. However, in my opinion, this evidence must not be seen as a negative aspect, but rather one more reason to be bullish about the EMQQ trend.