Delmaine Donson/E+ via Getty Images

Delmaine Donson/E+ via Getty Images

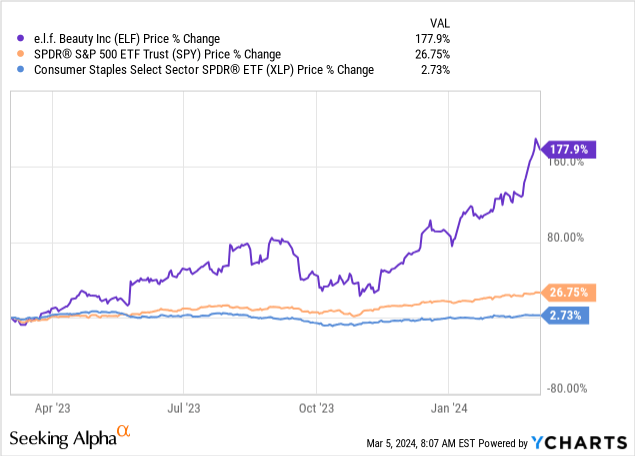

e.l.f. Beauty, Inc. (NYSE:ELF), together with its subsidiaries, provides cosmetic and skin care products under the e.l.f. Cosmetics, e.l.f. Skin, Well People, and Keys Soulcare brand names worldwide. The firm's stock has had an exceptional price performance over the past 12-month period, rising by as much as 178%, far outperforming both the broader market and the consumer staples sector.

The aim of our writing today is to determine whether the current share price, after the extraordinary gains, is justified based on the company's fundamentals or not. When talking about fundamentals, our focus will be on growth metrics, profitability metrics, and most importantly on valuation metrics.

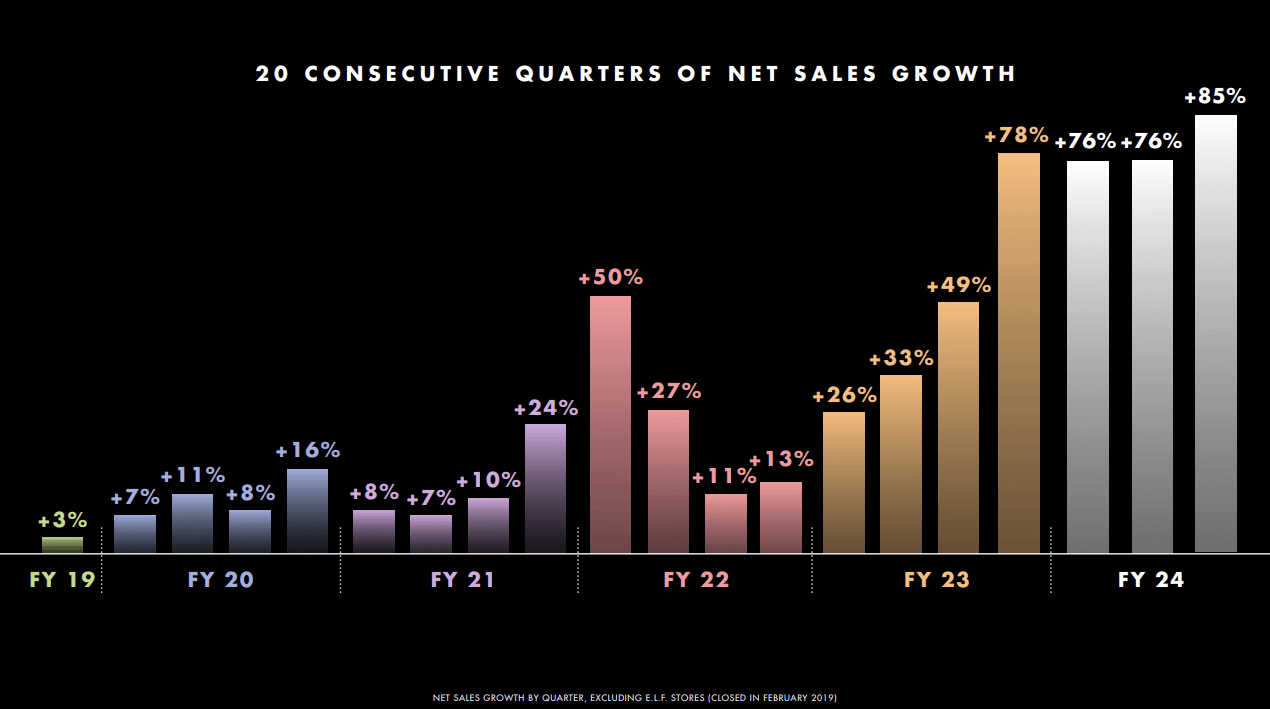

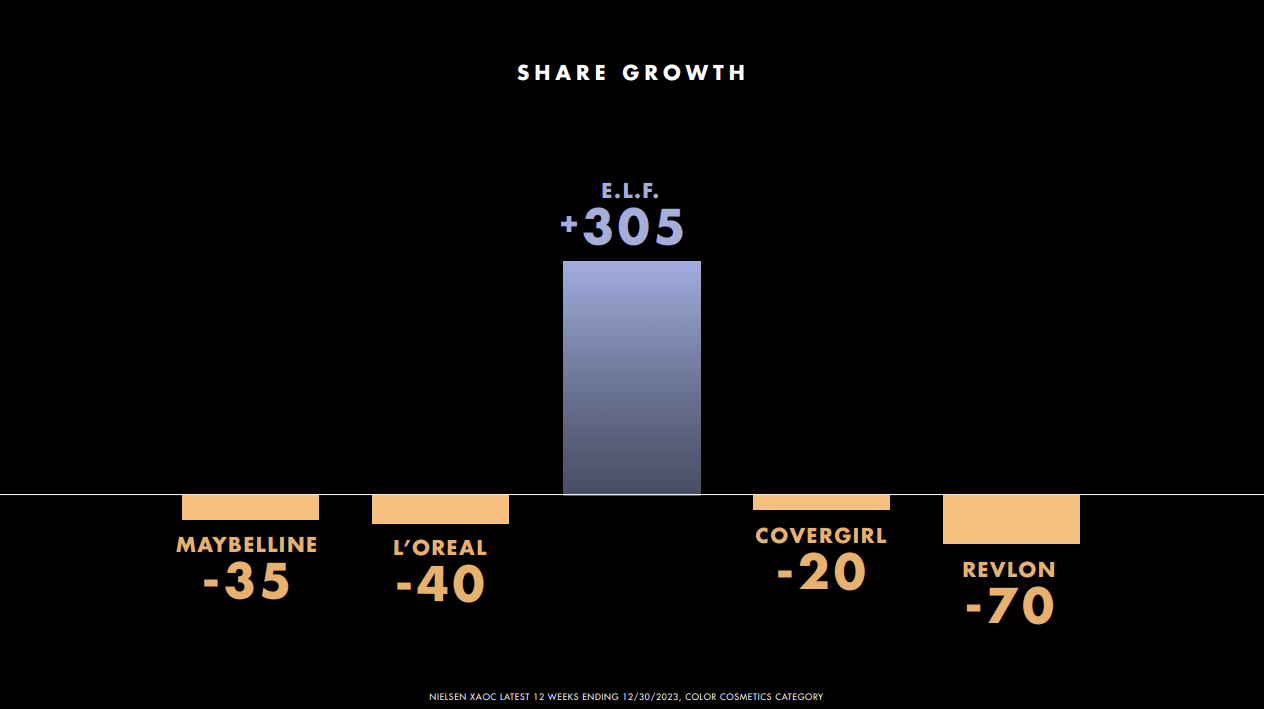

Over the past years, ELF has been growing at an outstanding rate. Management presented on the last earnings call a slide, showing what sales growth rate the company has managed to achieve in the recent past. With this growth, the firm has also managed to gain 305 basis points of market share.

Growth (ELF) Market share (ELF)

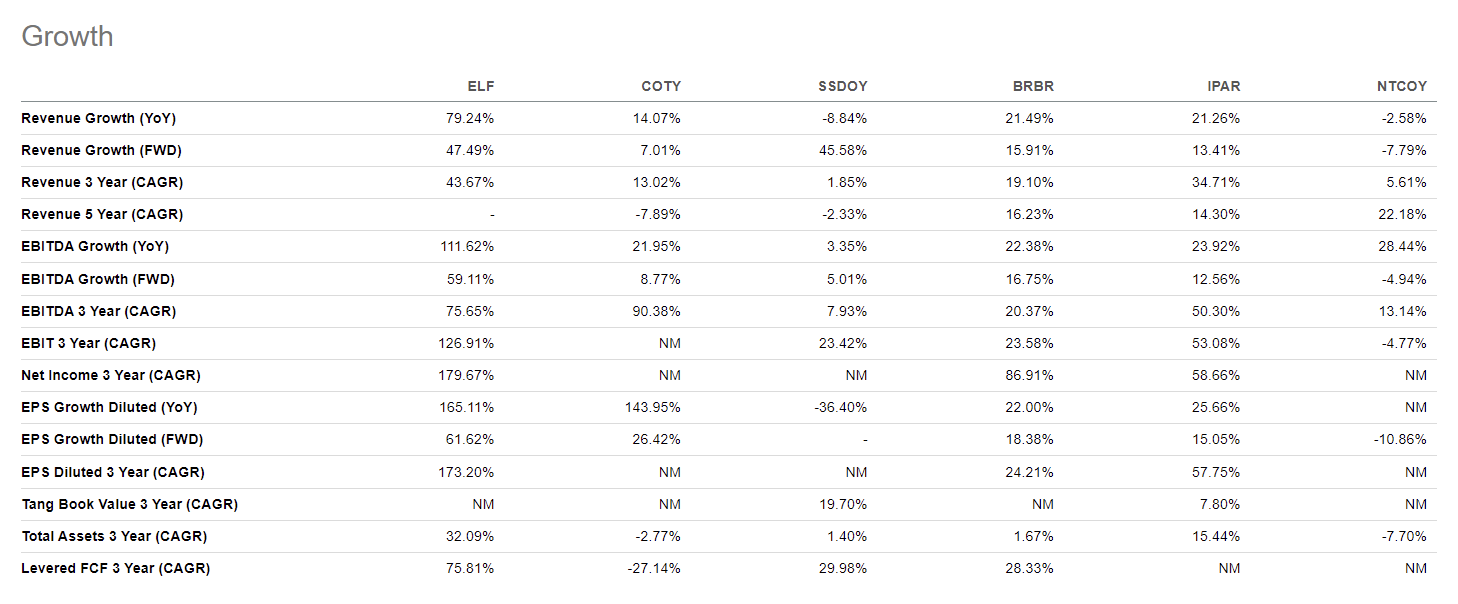

If we compare these growth rates with those of ELF's industry peers, we can see that ELF's growth far outpaces that of its closest peers/competitors across all of the listed metrics.

Comparison (Seeking Alpha)

In the past quarter, the impressive sales growth has been driven by the healthy demand both through retailer and e-commerce channels. But other tailwinds, like the favorable foreign exchange impacts, improved transportation costs, cost savings, and mix have contributed to also reaching a meaningful improvement in the bottom-line results.

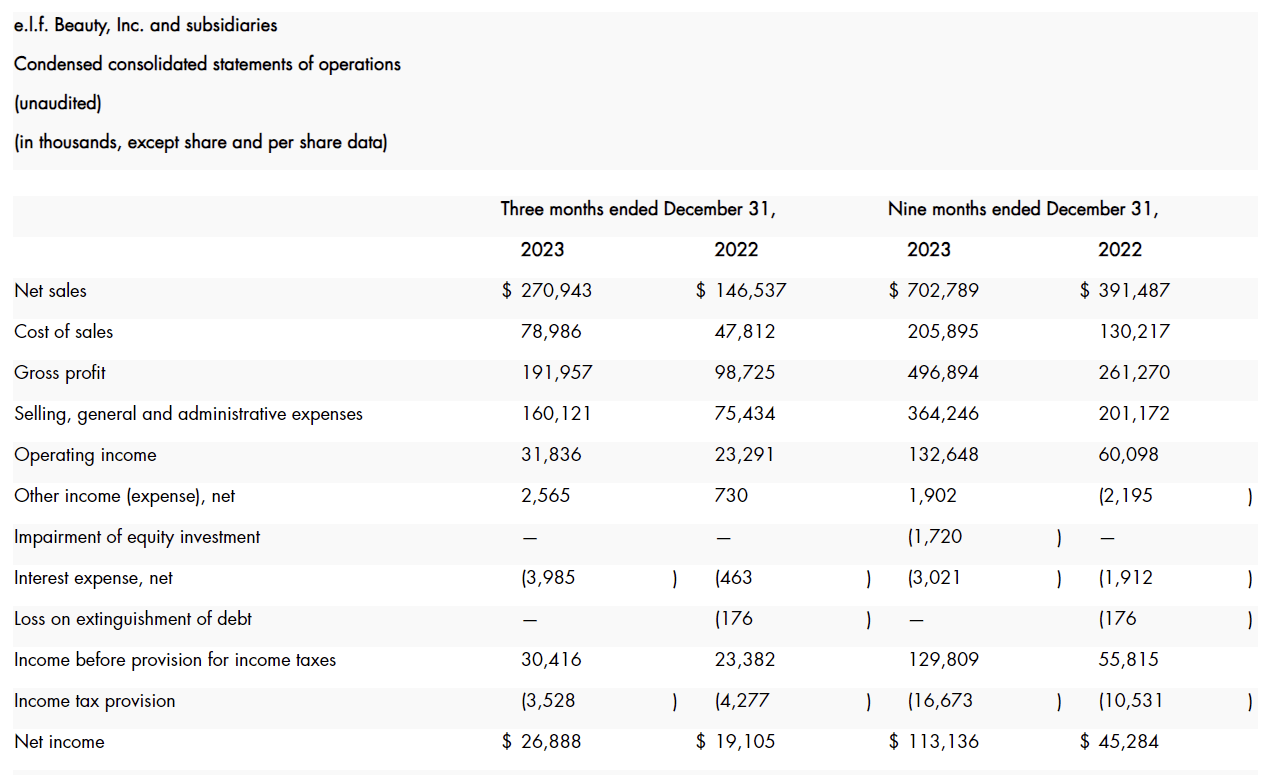

Income statement (ELF)

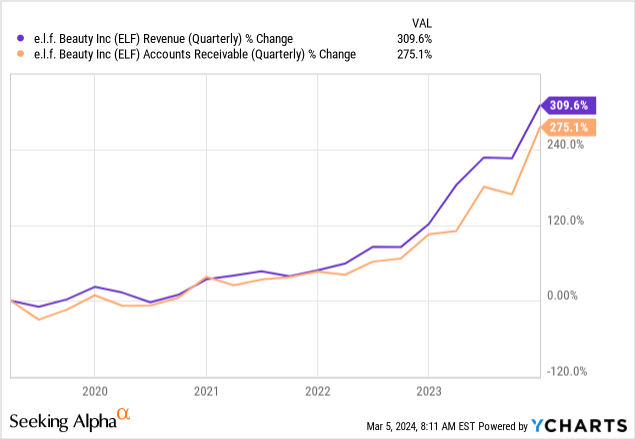

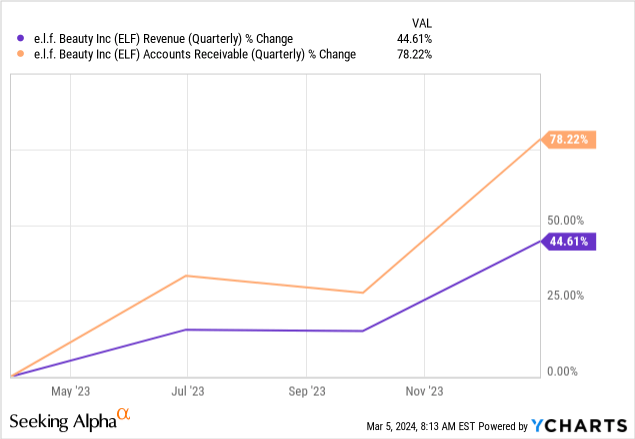

The following chart shows how the revenue and accounts receivable have developed over the past years. Normally, we would like to see these two metrics growing at the same rate, or revenue outpacing accounts receivable. If accounts receivable grow at a faster rate than sales, it could be a warning sign that the firm is selling more on credit to pull forward demand from future periods, or has changed its revenue recognition policies in order to create the appearance of growth.

If we are focusing on a 5-year time horizon, the two line items appear to have been moving closely together. However, when we zoom in to the last year only, we can see that accounts receivable have been growing at a faster rate. This is definitely a development that one should keep an eye on, as it may lead to slowing sales in the coming quarters.

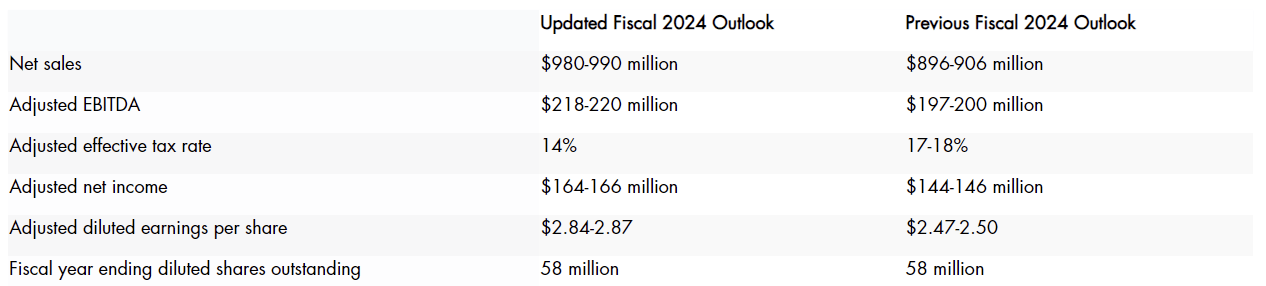

Looking forward, despite this divergence, we can be relatively optimistic. Management has boosted its fiscal 2024 outlook significantly, forecasting now higher net sales, higher adjusted EBITDA, lower adjusted effective tax rate, and eventually a higher adjusted net income.

Outlook (ELF)

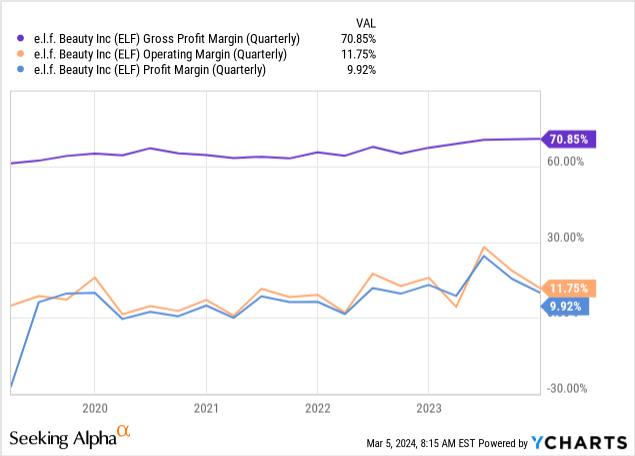

When assessing the profitability of a firm, normally we look at three metrics, namely the gross profit margin, the operating margin, and the net profit margin. The following graph depicts how ELF's margins have been developing over the past 5 years. It is clear that despite the challenging macroeconomic environment in the past years, including poor consumer sentiment, elevated inflation levels, and higher commodity prices, ELF has not only managed to keep its margins relatively but also expand them.

Also, during the last quarterly earnings call, it was pointed out that gross profit margin expanded by as much as 350 basis points, reaching 71%, mainly driven by favorable foreign exchange impacts, improved transportation costs, cost savings and mix. On the other hand, SG&A expenses have increased and slightly offset the previously mentioned tailwinds.

Selling, general and administrative ("SG&A") expenses increased $84.7 million to $160.1 million, or 59% of net sales. Adjusted SG&A increased $79.1 million to $147.3 million, or 54% of net sales. The increase in SG&A dollars was primarily due to an increase in marketing and digital spend, compensation and benefits, operations costs, retail fixturing and visual merchandising costs, depreciation and amortization and professional fees.

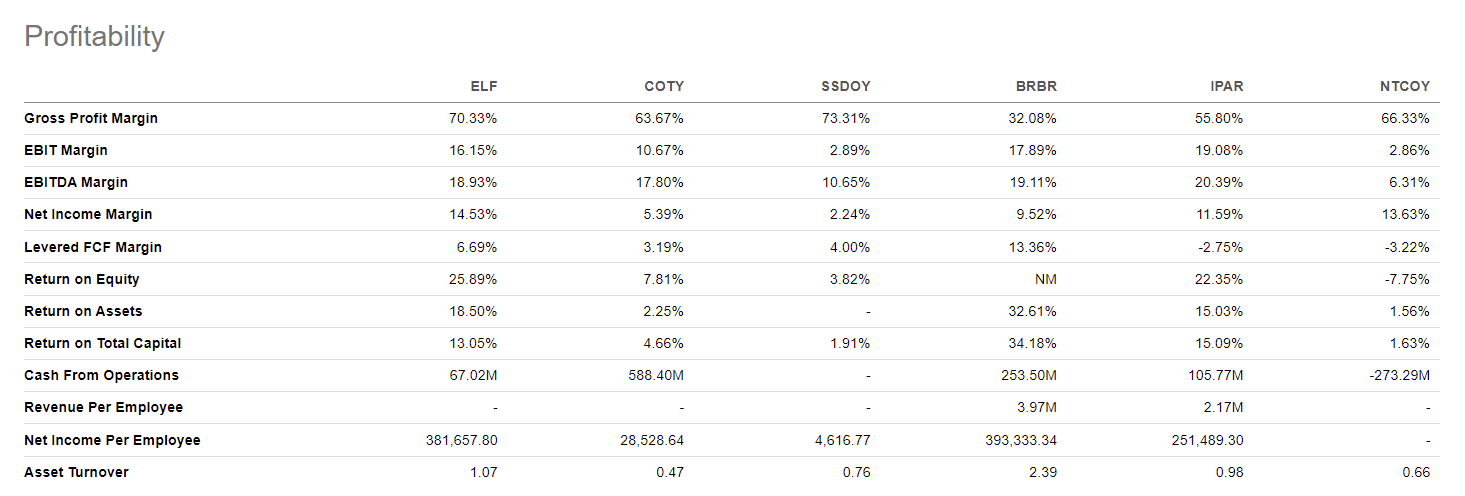

Now, once again, to put these figures into perspective, the following table compares ELF's profitability metrics with those of its peers and competitors. It is clearly visible that ELF is way ahead of the rest of the group.

Comparison (Seeking Alpha)

Just as with the growth metrics, the profitability metrics also indicate ELF's superiority compared to its peers. The above table also shows an efficiency measure, namely the asset turnover, which shows how efficiently the firm is using its assets to generate sales. In the above peer group, ELF appears to be one of the most efficient firms as well.

While ELF's business looks exciting from both a growth and profitability perspective, we have to understand, how much one should actually pay for this. In the next section, we will be discussing the firm's valuation, using a set of traditional price multiples.

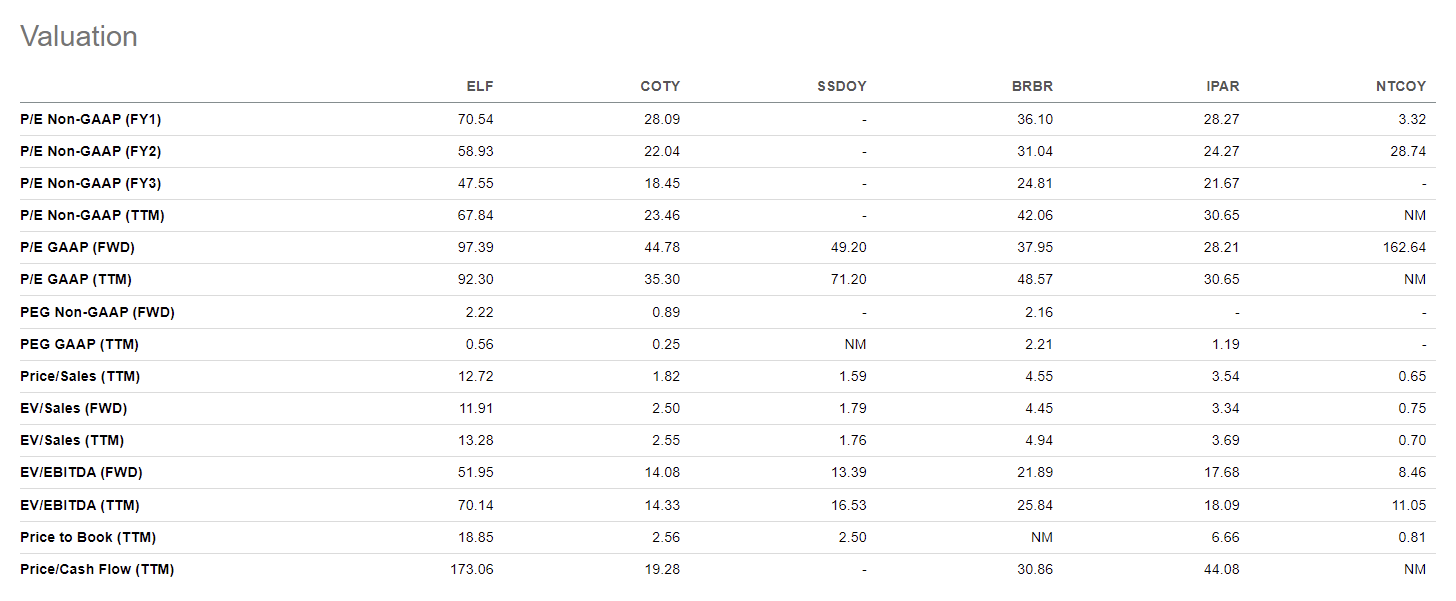

While the business appears to have a high-quality business model and strong fundamentals, its valuation seems too high for us. The following table compares a set of traditional price multiples with those of ELF's peers and competitors.

Comparison (Seeking Alpha)

ELF appears to be trading at a significant premium compared to this group. When we compare the current values with the firm's own 5Y averages, ELF also seems to be quite overvalued. For this reason, we believe that it is worth being cautious at these price levels. Due to the significant run-up in the previous year, we do not think that there is significant upside potential left. Although we expect the growth to continue, and we also expect the macroeconomic environment to improve towards the end of the year, we still cannot justify a "buy" rating at the current price multiples.

ELF has managed to beat both top- and bottom-line estimates in the previous quarter, further fuelling the already exceptional stock price performance seen in 2023.

The company appears to be an interesting and attractive investment option based on its fundamentals. The firm has one of the best growth metrics in the personal care products industry, as well as it has one of the best set of profitability metrics.

On the other hand, ELF's stock appears to be trading at a significant premium. The price multiples are not only indicating an overvaluation compared to the consumer staples sector median but also compared to the firm's own 5YR averages.

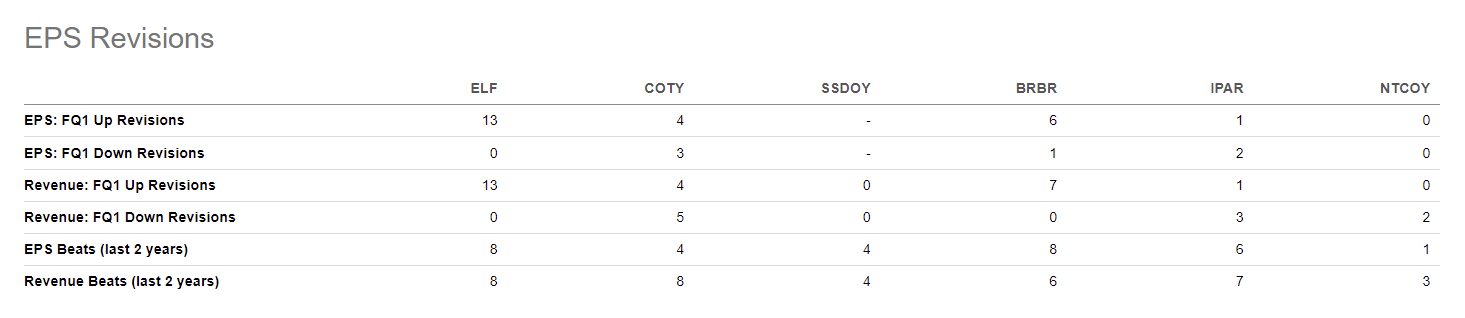

Also, important to point out that analysts have been being positive on the stock, with most analysts revising their earnings estimates upwards lately. This comes to us as no surprise due to the boosted guidance, and the firm's history of consistently beating analyst estimates.

EPS revisions (Seeking Alpha)

All in all, we believe that ELF's stock is an attractive one to hold, but not an attractive one to start buying now. We would like to see the stock price pull back before we could assign this firm a clear "Buy" rating.