Galeanu Mihai

Editor's note: Seeking Alpha is proud to welcome Future Tech Investing as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Galeanu Mihai

With this article, I want to discuss EHang's (NASDAQ:EH) latest communication, share my opinion of the prospects to its business, and address its valuation. To give you the key message: if you are fine with the regulatory and political uncertainty that comes with investments in Chinese start-ups, EHang is a great growth bet for the long run. The technology has reached certification, tailwinds in the domestic market are strong, and international expansion seems to be within reach. I rate EHang a Strong Buy at current levels with the potential to multiply in the coming years. Having said that, volatility in this stock has often been insane and positions should be kept at a reasonable size.

October 13th marked a leap in EHang's development. The company announced that it had been granted type certification for its flagship passenger drone, the EH 216-S, and is now the first drone manufacturer in the world to have achieved this milestone. Investors have been awaiting this moment for years and at first, after almost a week of trading halt, EHang's stock price was up about 85% pre-marked, from an already elevated level of $17, before coming down substantially. I can only speculate that investors were hoping for a clearer breakthrough regarding future perspectives and share price. EHang however did not communicate too much on how things would proceed from this point and in the following days, the share price lost further ground to break below the pre-announcement level and bottomed in the low $13s after yet another report from short seller Hindenburg Research. With the Q3 earnings presentation, the company finally showed some more direction and its share price managed to climb again.

EHang 6-month share price development (Seeking Alpha)

I have been an investor in EHang since January 2020 and held my stake through the peaks and bottoms (yet with some profit taking and buying back again and more later). What has always characterized the company in this time, is that it does not communicate too well and this is what happened again after the announcement of type certification (TC). After almost a week of trading halt and announcing the transformational news, the management seemed to expect that this would suffice and did not provide a lot of guidance into what this entails for its business and what the next steps are that it plans to take. The subsequent events (short report and share price development) might have been educational though, as they did better with the Q3 earnings call. Management issued a revenue guidance for the first time and provided some insights into how they plan to approach commercial development. Of course, communication could have been a lot more concrete and many questions remain, but the commentary already gives a much clearer picture. The information and citations provided in the following are taken from the company's Q3 earnings presentation and the management's commentary. So let's dive in!

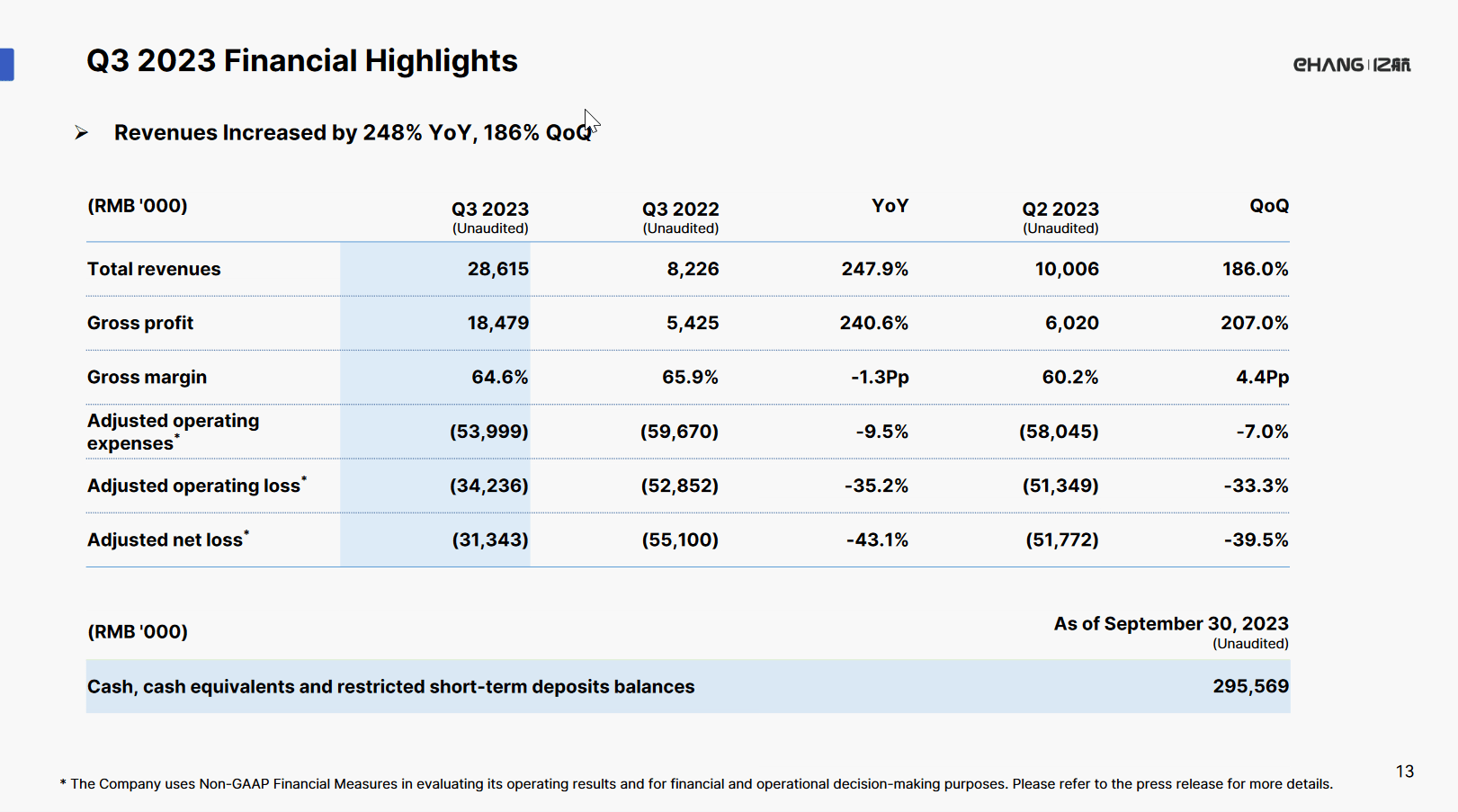

Upon completing TC in Q3, EHang delivered 13 units of the EH 216-S, which represents a clear improvement from the 5 units delivered in the previous quarter. This constituted the basis for a revenue increase of 248% YoY and 186% QoQ to RMB28.6 million and the company expects to almost double this number again to RMB56 million for the coming quarter. Additionally, gross margin slightly increased QoQ to 64.6%, up from 60.2%, and roughly stable from Q3 last year. According to the CFO, the reason for this is that with TC in the bag, average sales prices increased slightly and are expected to increase even further as more drones are being delivered according to the TC specifications.

With this revenue increase at a stable cost basis, EHang managed to reduce its operating loss by 35%. By doubling this base and assuming again stable costs and gross margins, the company could already get close to breakeven in Q4 2023. Of course, costs might rise due to the ramp-up of production, yet a part of operating costs in the previous quarters should also have been incurred by the works towards type certification and thus counteract a strong increase. The company guides to achieve positive cash flow "in the later part of 2024" (Chia-Hung Yang, CFO).

Q3 2023 Financial Highlights (The company's Q3 earnings presentation)

Next to these financial results, EHang achieved several operating and financing objectives. On the financing side, it carried out a private placement from several strategic investors to gain $23 million, which equals about RMB163 million and enables the company to substantially extend its runway at the projected cash burn. I could even imagine that the current balance sheet suffices to last until the projected point of positive cash flow, if no large additional investments are taken. On the cash-negative side, the company announced a strategic investment into Shenzhen Inx Technology Co., Ltd., a solid-state lithium metal battery technology company in China to cooperate on the research, development, and production of solid-state batteries for its eVTOLs. However, the size of this investment was not disclosed.

Further operating advances include the award of a permit to perform trial operations for unmanned aircraft cloud systems which among other features includes EHang's airspace and UAV management for remote drone operation. After the quarter-end, the company also announced the opening of an Urban Air Mobility Center for Unmanned eVTOLs at Lleida-Alguaire International Airport in Spain. The project is the first of its kind in Europe and is set to demonstrate the effective integration of eVTOL operation with airport infrastructure, air traffic management systems, operational procedures, and other information technologies.

More generally, EHang's management reiterated in the call that it plans to follow a hybrid business model of (1) achieving one-off revenue from selling drones to corporate customers and (2) operating routes themselves and generate continuous service payments from people who take a flight. With the award of TC, the company experiences a strong rise in customer interest, product demand and secured new deals with interested municipalities. The Chinese government also seems to push this development by releasing a "green aviation manufacturing industry development outline 2023 to 2035" in order to foster eVTOL operations by 2025. Furthermore, local governments issued supplemental support policies with some of them already partnering with EHang, like in Q3 Bao'an district government of Shenzhen and Hefei municipal government. By 2025, the Bao'an district plans to build over 100 vertiports and launch more than 50 UAV routes. The Hefei government agreed to provide financing of $100 million including facilitating purchase orders and financing support. Management commented in the earnings call:

"With the EHang 216-S receiving CTC, we've seen a significant increase in business collaborations and product purchase demand from customers around the globe, especially from China. For instance, Shenzhen Boling intends to purchase 100 units of EHang 216-S, and we have delivered the initial 5 units for operational preparations. Moreover, in accordance with our strategic partnership, the Hefei municipal government is set to facilitate orders for at least 100 units of EHang 216 Series products. As of now, the total sales pipeline for the EHang-216 Series in China have more than 245 units, which will be delivered in phases as per customers' requirements." (Xin Fang, COO).

Regarding the dependability of such preliminary sales contracts in the pipeline, the CFO added:

"For our preorder and order of intent, we charge a small non-refundable deposits, which varies by customers to confirm their commitment to purchase. And for the purchase order, right now, we will collect about 30% for down payment. And then for the remaining 60% to 70% before delivered." (Chia-Hung Yang, CFO)

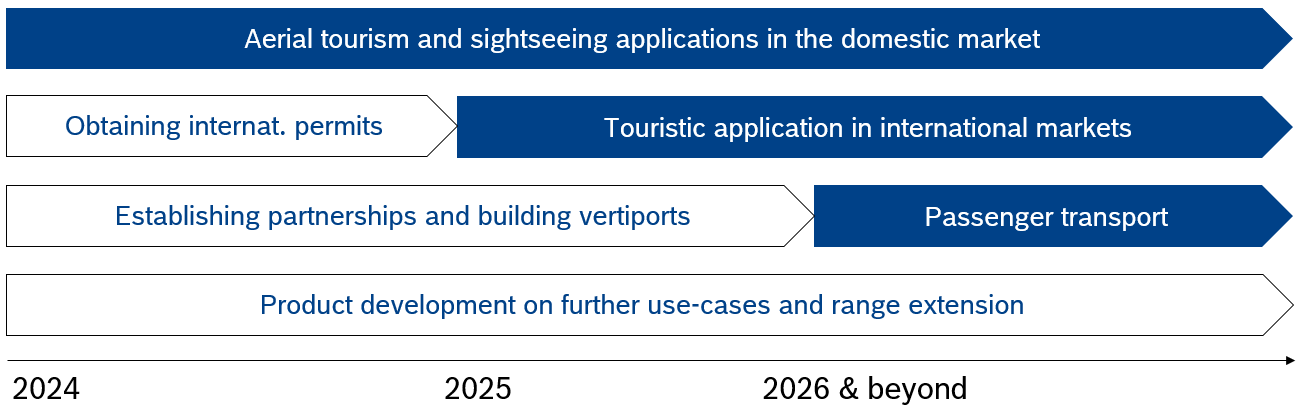

In the question-and-answer session, the management went into more detail and talked quite clearly about its plans for the coming years. First, EH 216-S are expected to be sold mostly for domestic sightseeing applications in 2024 - with China possessing over 6,000 spots of interest. The CFO added to this: "Even if we use like a 10% penetration rate in each site to use 5 units, that will be like over 3,000 216 demand from domestic scenic spot in the next several years." (Chia-Hung Yang, CFO). For this, customers usually initially purchase a few units for training and trial operations and then proceed with more volume. Sales could thus be expected to ramp more significantly in the coming quarters.

From early 2025, the company expects to be able to initiate deliveries into international markets, with an additional sales pipeline of 210 units (of which over 90% are EH 216-S) from other Asian markets and strong customer demand coming from e.g., Indonesia, Malaysia, and Japan. Management expects the achievable average sales price for international markets to be higher compared to the Chinese domestic market. Up until now, it was mostly unclear if each of these markets would again necessitate a lengthy and costly certification process. According to the management, this will probably not be the case as the company expects that the Chinese certification can be realized with reduced effort so that recognition/validation could be achieved in less than 12 months. They commented on this a few times:

"Internationally, following by obtaining a TC from the CAAC, we are proactively engaging in efforts to secure a bilateral recognition and certification from various civil aviation authorities through communication and collaborations with our local customers and partners. This will position us well for the next phase of delivering international orders and expanding our business abroad." (Xin Fang, COO). "As we all know, in the past few years, the CAAC has reached a lot of bilateral regulation agreement with other aviation authorities in other countries. We're promoting the communication between the CAAC and with other civil aviation authorities. For example, recently, the Brazil Civil Aviation Authority came to China. So first, we will prioritize the -- to work on the regions that we have orders in the local market. We believe we will make efforts to promote the VTC procedure, which means the verification of the type certificates in the local countries. And we will provide support to that work. Before we obtain the VTC, we can deliver some products to the local market and do some trainings for the local clients. We will extend our market expansions at a proper pace to the international market. We believe that soon, we will see our global exposures. So the VTC is an administrative work. So it's not as complicated as the type certificate." (Huazhi Hu, CEO)

After these touristic purposes, EHang anticipates use cases beyond tourism by approaching the market for passenger transport. First preparations for this are already underway, particularly in Bao'an, with the build-up of vertiports for transportation purposes. I suspect construction of this infrastructure is also the reason why this use case will take up additional time and might require structured long-term partnerships with upfront commitment of capital being rather high. Reaching agreements with multiple cities individually will thus take some time. Yet, EHang might be able to create a certain level of market power in this area from being the first mover (similar to Tesla being the first mover with supercharger locations/infrastructure). In my view, this market can become huge - particularly if the Chinese government aims to use its leading role in this industry to show the word how far it has come by establishing this futuristic form of public transport. I could also imagine use cases like luxury hotels in wealthy Arabian countries offering quick and convenient airport pick-up via drones and many other applications that first address the luxury segment.

Outline of managements development plan (The author)

In addition to these use cases for EH 216-S, next steps also include the market introduction and sale of EH 216-L and EH 216-F which respectively represent a logistics and firefighting solution of the EH 216-S. The 216-F has been described in previous earnings call as a solution for firefighting in high-rise building (of which Chinese megacities have quite a few), where the drone carries a "gun" and a water tank to open windows and extinguish fires that traditional firefighting cannot reach (there are some product videos on the internet that I recommend watching). EHang has already successfully completed tests with the Chinese firefighting equipment quality supervision testing center in 2021.

Regarding the 216-L, the company announced a strategic partnership with the Chinese branch of DHL (DHL is the world's largest logistics provider in terms of employees) in 2019 to develop the technology for fully automated and intelligent urban drone delivery solution - however communication on this has been scarce in the last few quarters and I am not aware of any developments (Hindenburg argues that the cooperation has been abandoned). Still, there are a few product videos from EHang and I can imagine that some effort has been spent on this behind the scenes.

Moreover, in the later course of the Q&A, the management was asked about its plans for product development and improvements in its battery technology which the CEO answered in the following way:

"The EHang 216-S is designed for the short-distance air transportation with the industry. So according to our test, our product is capable to do the air taxi services within the city. In order to achieve the longer flight time, we will continue to optimize our power system and the battery system. Yes. As you know that there are many companies in China who have invested in the solid-state lithium batteries. For example, the (inaudible). And recently, we have also invested in a domestic solid-state lithium battery company. So we are making efforts to achieve the goal that to tackle the flight performance in the future. Our goal is to achieve a longer flight range, but meanwhile, we will ensure safety. We are doing the type certification with the EHang 216, the VT-30 development pace is much slower. But now we are after the type certification of EHang 216, we are also developing and working on the long-range model, which is the VT-30, a lift and cruise model for the intercity, longer range air mobility. The EHang 216-L have obtained the operation -- trial operation certificate for the cargo transportation previously. So after, there is certification standards for this kind of aircraft, we will supply for type certification for the EHang 216-L. Before we obtain the type certificate of the EHang 216-L, we can still expand our business based on the trial operation permit that we have obtained. As the EHang 216-L and -S share the same flight platform, so we can leverage the experience from the type certification for the passenger model. So we can expect to take short of time on the EHang 216-L type certification than that of the passenger one." (Huazhi Hu, CEO)

The eVTOL sector is one of the next big growth sectors for the coming years and decades and is expected to reach a market size of $34.92 billion in 2030 (numbers in different studies vary largely). Growth perspectives thereafter are just as impressive with Morgen Stanley believing that the market could be worth $1.5 trillion by 2040. Correspondingly, more than 300 companies currently work on eVTOL's worldwide, yet, not all designs and ambitions are comparable to EHang and by far not all of them will get to the point of commercial operation. Also, many, including the popular names Archer (ACHR), Joby (JOBY), or Lilium (LILM), aim to provide longer-distance flights between cities for around 5-7 passengers and only compete with EHang as soon as it introduces its VT-30 into the market.

For the moment, none of the companies in this field generate material revenue, but the sector is about to ramp up in the coming years and some competitors aim to reach certification in the near future. German Volocopter seems to be the closest competitor, working towards a first commercial use-case at the Olympic Games in Paris in summer 2024 for its 2-seater air taxi. However, Volocopter's VoloCity is not certified yet and will only be equipped with autonomous flight at a later point. It will therefore require a pilot for the foreseeable future, meaning that it will only be able to carry one passenger. Being almost two times heavier, carrying only one passenger and requiring a costly pilot, it is hard to imagine how VoloCity could be economically competitive to EH 216-S. I also don't think that Volocopter will be active in the same geographical markets as EHang for the coming years.

In my opinion, competition will not be a big issue for EHang in the near to medium-term future. The attractiveness of the market and EHang's ambitions to expand to for instance Europe are however indicators that this situation will change and the company is going to be faced with more competitive pressure in the long run. Particularly markets like logistics and inter-city passenger flights will experience competition much quicker and more intensely.

Due to the early stage nature of the eVTOL market, many unknowns and assumptions are involved in evaluating a company like EHang. To still make my rough estimates more robust, I will approach the issue from two different angles and compare the results. To do this, I (1) give a relative estimate vis-a-vis the values of competitors and (2) derive a stand-alone valuation from expected future revenues.

Regarding the first point, not too many relevant competitors in the eVTOL space are listed on the stock exchange (all Nasdaq). I include the stocks below as the only companies currently listed with a market cap above $500 million and added Volocopter's latest valuation from a capital raise in March 2022 due to its nice comparability.

| Company | Archer | EHang | Joby | Lilium | Volocopter |

| Type | long-distance | air taxi | long-distance | long-distance | air taxi |

| Market Value | 1.880 | 0.974 | 4.429 | 0.695 | 1.87 |

Except for Lilium, EHang is valued by far the cheapest among these companies (as of December 7th) even though it is the only one having obtained a certification for its drones and exhibits ramping revenues (for Lilium there are serious doubts if its concept will be able to fly, as fellow SA author Steven Tobin explains). Some of this deficit is of course due to it being a Chinese firm and the doubts raised by short sellers. Still, taking its more mature state and its proximity to positive cash flows into account, EHang appears to be undervalued in a relative perspective.

Another approach I want to take is to give a rough approximation to EHang's value by deriving estimates for future revenues. For this, I take exemplary market shares out of the above eVTOL market size for 2030 and assign revenue multiples. In my view, a market share between 3% and 10% is not unrealistic and at the low end conservative - particularly as I expect that China will push the technology and EHang quite strongly. The scenarios of 5% and 7% seem to be the most realistic, while 10% global market share represents a more optimistic projection. Also, I believe sales multiples of 3, 5, and 7 are not aggressive keeping in mind the expected high growth rates between 2030 and 2040 and even considering a multiple discount for Chinese growth stocks. The results depicted represent a market capitalization for 2030 in billion Dollars.

| Market share | 3% | 5% | 7% | 10% |

| P/S ratio of 3 | 3.143 | 5.238 | 7.333 | 10.476 |

| P/S ratio of 5 | 5.238 | 8.730 | 12.222 | 17.460 |

| P/S ratio of 7 | 7.333 | 12.222 | 17.111 | 24.444 |

To get some perspective on the size of these numbers: being asked about a per unit sales price, EHang's CFO answered that they usually sell at RMB2.16 billion, which corresponds to $300,000. He also estimated that there are about 6,000 scenic spots in China that could be serviced by aerial tourism, which would yield a market opportunity for only this application and only in the Chinese market of $1.8 billion. Including transportation use cases and expanding to international markets, the ballpark above therefore seems to be within EHang's reach.

Of course building a business in an entirely new technology market entails that many things could go wrong. The most obvious hurdles that EHang still has to overcome are obtaining flight permits, managing cash, and generating sufficient orders. After achieving TC, I believe that obtaining further permits for actual operation should work out smoothly as all safety and technology concerns have already been addressed. Additionally, EHang's CFO mentioned in the Q3 earnings call that he believes working capital is sufficient and showed that the current quarterly operational cash burn rate of RMB10 million is well below the cash reserve of RMB295 million, with only 4-5 quarters to go to achieve positive cash flow. Hindenburg research criticized the low cash balance in their short report while at the same time criticizing the low cash burn. To me these arguments seem contradictory as it is the low cash burn allowing EHang to comfortably get by with less capital requirements than competitors. Regarding orders, with the described size of the market opportunity, I believe it is a matter of EHang's sales team to translate a sufficient share of this into sales.

More serious risks are in my opinion on the regulatory side, in the influence of competition, or lie particularly in the aftereffects of possible accidents. In the past few years, China has often shown that changes to underlying regulation can be implemented suddenly and distort the entire business model of even domestic companies (online education, fintech, etc.). Even as policy has promised to reduce such activities, similar dynamics might capture the eVTOL sector. Also, unfavorable regulation in other countries could slow down or halt EHang's international expansion. Further on, once more and more competitors reach certification, EHang's products might become technologically inferior leading to a decrease in demand.

Lastly, the most substantial risk to me lies in the loss of confidence the company would be faced with when a serious accident occurs. Up until now, EHang's success rate is stunning with more than 40,000 trial flights (Q3 earnings presentation p.5) and no accidents, but with commercial adoption and many flights in less controlled environments, the probability of incidents rises. It is difficult to predict how regulators and customers would react to this and what the aftereffects for the company would be.

With the award of TC, EHang has made tremendous progress on its way to becoming the world's first passenger drone company entering the initial phases of commercial operations. If EHang were to be a trusted Silicon Valley company, it would probably be valued as an early Tesla on steroids. Yet, being subject to all the restrictions and limitations that come with being a Chinese firm and its trouble at communicating effectively, its business prospects often remain clouded and make it more difficult to ascertain a solid evaluation. Understanding that this is not a common Nasdaq stock and that it must be approached differently is key to recognizing the risk and volatility that come with such an investment. There is a reason for the high short quota and the frequency of short attacks which is something to keep closely in mind when deciding on position size.

Having said that, past short reports were widely unsubstantiated and I believe the short sellers will be proven wrong as well. In my opinion, EHang does not communicate poorly to hide bad news or fraud. It often struggles to sufficiently keep investors updated on positive developments too and will, with ramping business, also surprise to the upside. Looking at the commentary in this earnings call, one can see that there is a lot more happening behind the scenes regarding the technology (the past quarters were all about 216-S with little progress sharing on the other products) and business development than meets the eye at first. EHang is also historically very capital efficient and I expect that with money coming in from ramping 216-S sales, efforts on the other products will progress much quicker once the introduction of its flagship product is achieved.

By entering new product classes and expanding use cases as well as geographic markets on its passenger drone, the addressable market for the company is huge. This fact is even more relevant when considering that there is only limited competition for the foreseeable future and that EHang already has ties with many Asian countries and the EU (EHang exhibits a lot at European fairs, is the only eVTOL startup participating in the EU's AMU-LED program, and conducted trial flights in Austria, Spain, and the Netherlands). Moreover, China has a strong interest in developing future technologies to generate leading technology companies so that strong political tailwinds in the domestic market are very probable.

The plans laid out in the earnings call make me feel very positive about EHang's future. Although there are yet many unknowns in deriving a target price, I am confident that the share price has a lot of upside potential when comparing the estimated future market and EHang's leading and comparatively mature position with the current market cap of almost $1 billion. The numbers I have shown suggest that its market cap could multiply until 2030, if EHang manages to capture a sufficient market share. I therefore rate the company a Strong Buy at current levels and recommend a small to medium position for risk-aware investors with a long investment horizon. Due to the volatility involved, I suggest to cost-average into the position and hold on for a couple of years. This investment has been a roller coaster ride for me and even after experiencing quite a few low points, I'm confident that the company will deliver. This is a leading player in one of the most exciting sectors for the next decade who is about to ramp up ahead of competition in a market out of reach for most of its competitors.