Jeremy Poland

Jeremy Poland

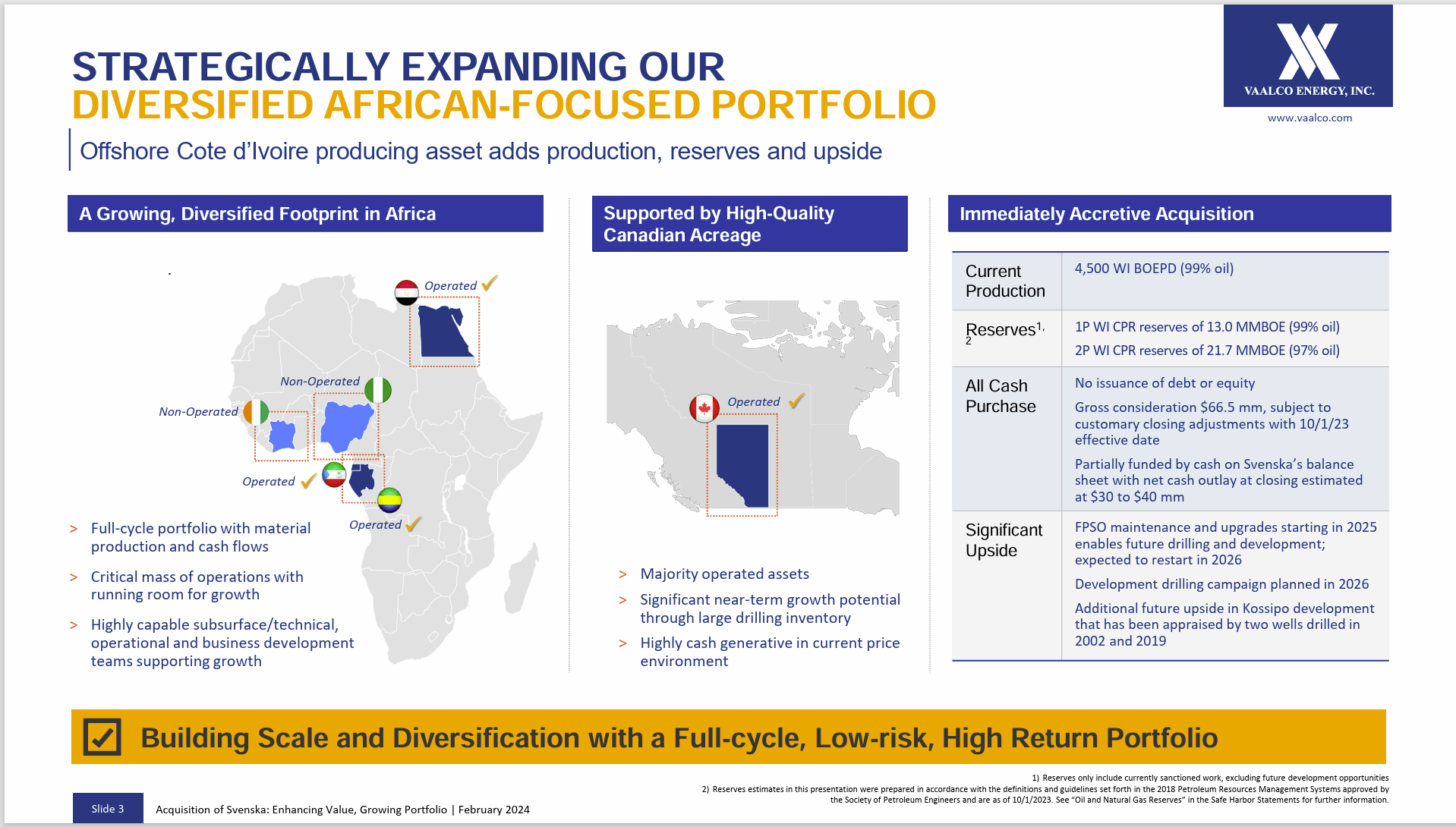

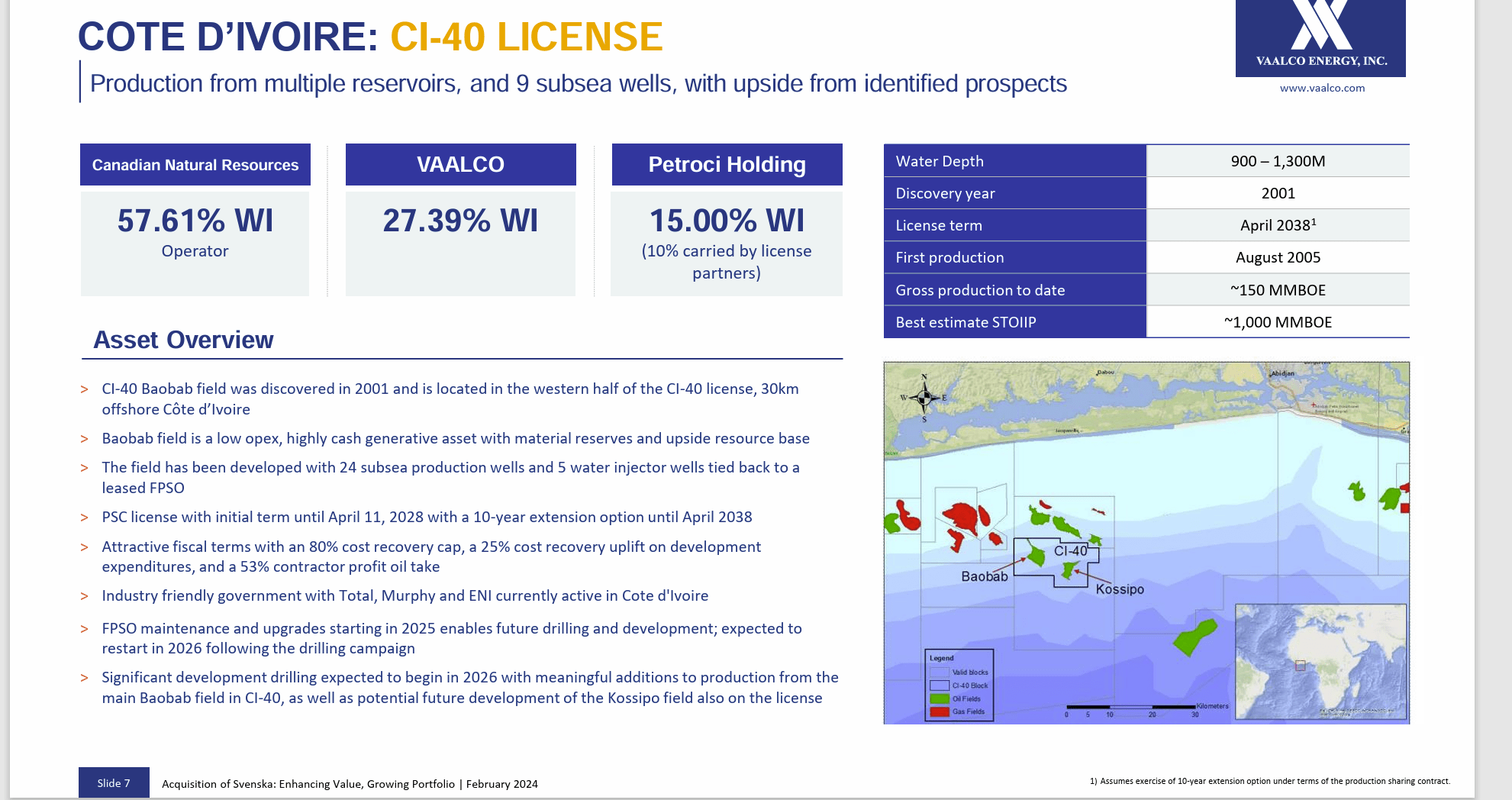

Vaalco Energy (NYSE:EGY) recently announced a new deal to obtain Svenska Petroleum Exploration AB for cash. The immediate benefit of this acquisition is ongoing net production of 4500 BOED off the coast of Cote d'Ivoire. This represents a roughly 27% interest. That production is operated by Canadian Natural Resources (CNQ) a well-established producer. There is also an interest in an Exxon Mobil (XOM) discovery in Nigeria that is not expected to be developed at this time.

Like the deals in the past, management will use part of its substantial cash balance to fund the deal. Management also realizes that the production will go offline in 2025 and come back online in 2026.

One of the interesting things about this deal is management has its own projects elsewhere that could potentially make up for that offline production during the fiscal year. It was not too long ago that this company only had one source of income. As the diversification efforts continue, the production reported to shareholders should gradually smooth out over time as each production area becomes less significant due to diversification. This would allow for a higher market valuation in the future as a larger company attracts more interest.

There is a concentration of business in Western Africa. Even though the latest acquisition is seen as being in a more stable part of the continent. That is not exactly a high bar for some areas of the continent to get past.

Vaalco Energy Map Of Basins In Company Project Portfolio (Vaalco Energy Acquisition Corporate Presentation February 2024)

A lot of the areas where the company has a presence in Western Africa need the money that oil production provides. Since management generally remains offshore for much of the company business, much of the instability in the area does not affect operations. So far, it does not appear to have affected the business at all. But it is a risk factor for investors to consider.

The extra risk in Western Africa is offset by a presence in Canada and Egypt. Both of these are considered far more supportive in the industry with both stability and effective governments.

The one thing about the business in the company's areas is that much of Africa has a good return for those that know how to navigate the continent. But that navigation ability is a specialty in and of itself.

Offsetting some of the business risk is a very strong balance sheet with no reported debt and a decent cash balance. Given where the company operates as an upstream company, that is unlikely to change anytime soon.

Management usually, similar to the current acquisition, will work with established companies when it does not manage the operation itself. The presence of a larger operator often adds credibility in risky areas.

Management, as shown on the map above, is also diversifying so that a disappointment with any one project will have a materially lower effect as the diversification program proceeds.

Management has so far been very good at finding countries that honor contracts no matter the political system and assumed instability. That luck can run out at any time. Hence, many of these proposals come with fairly low prices so that the buyer earns back the purchase money relatively quickly.

The governments themselves are not necessarily hostile to the oil and gas business, it is the instability that permeates the region that increases the risk of doing business.

Note that Vaalco is a relatively small player in the offshore industry. Yet the offshore industry is known for large projects that require a lot of cash to get started. Vaalco needs (and has) a strong (and comprehensive) risk reduction program.

Vaalco made sure of quite a few certainties in the current acquisition and that has really been the case throughout its history. These offshore wells and the accompanying equipment are relatively expensive. Any success has a relatively long lead time. Therefore, any mitigation of failure is essential for a smaller company.

The company this time purchased existing production and already knows the costs of the FPSO downtime. Furthermore, the upside in 2026 is relatively well established with work done in the past.

More to the point, management does not do high risk exploration. This often takes years to show any results and is very cash draining. Management instead sticks to well-known fields that major integrated companies often have no interest in.

For this reason, Vaalco tends to want to develop discoveries that are too small for the bigger players in the industry. But these same discoveries are profitable for a smaller company like this one. Many times, there are other wells drilled in the area or other work done so that the risk of a dry well is much lower than normal.

But staying out of the way of the bigger players limits competition and therefore keeps overall costs lower.

Management released the production figures and some other qualitative items on the fourth quarter before this acquisition was announced. The company has several relatively large projects underway. Any updates on offshore wells to be drilled often has an outsized effect on future expectations and stock prices (as do dry well announcements).

Basically, this company is debt free with a decent cash balance that allows it to take advantage of deals like this one. Companies with a lot of cash rarely get into serious trouble. The company's Fourth Quarter earnings release is scheduled for March 13, but quarterly reports are not feared (or worried about) quite as much because of the strong finances.

This company is really more about when the next platform is coming online (and are their cost overruns or unexpected delays). A new offshore well is expensive but can add thousands of barrels a day to production if successful. Those kinds of things command market attention. The quarterly report is more about making sure there are no material surprises. This stock very much trades on forward prospects.

One of the more reassuring things about this is that there are several large players with an interest in producing in this area.

Vaalco Energy Acquisition Details (Vaalco Energy Acquisition Presentation February 2024)

Any acquisition that is made for all cash will be accretive on a per share of production basis to company shareholders. This management, to its credit, regularly maintains a healthy cash balance in case an opportunity like this one makes an appears. Therefore, no shareholder dilution was necessary.

The balance sheet remains strong even if the amount of cash is reduced. But more importantly, prices in these smaller projects are often cheaper (due to less competition) than is the case for larger projects. The other consideration for the nice price is that the area itself does have some political instability that raises the risk of doing business in that part of Africa.

This particular country, Cote d'Ivoire, appears to be somewhat more stable than a few of its neighbors. But that could easily change.

Enough of these offshore projects will smooth the growth curve of the company as it gets larger. It also makes the overall risk of the business lower because each project becomes less significant to overall results. However, management's ability to navigate this part of the African continent is crucial to the success of the business.

Profit margins and return on equity is high. The offshore business is often unaffected by what happens onshore. Therefore, the business is often well supported because it brings more than a few otherwise cash starved countries some badly needed foreign currency.

For those that do not mind the risk of doing business in this part of Africa, this company would be a speculative strong buy. Management does reduce a lot of inherent risks. But it is still a risky place to do business. Nonetheless, the company has been successful in the past. As long as that success continues, there could be a sizable appreciation potential for shareholders of this company well into the future.