Maskot

Maskot

8x8 (NASDAQ:EGHT) is a cloud-based communications company that provides integrated voice, video, chat, and contact center solutions. Founded in 2002, the company has grown to become a leading provider of unified communications (UCaaS), Communications Platform as a Service (CPaaS), and contact center as a service (CCaaS) solutions for businesses of all sizes.

EGHT has had a bumpy ride. While it soared to an all-time high of $37 in 2021, it currently sits at $2.5, down -63% all time and -87% over five years. The stock is also down over -29% since my latest coverage last year, confirming my neutral call despite the projected upside based on my target price model.

I maintain my neutral rating for the stock. Though my 1-year target price of $2.87 presents a projected 12% upside, I believe the lack of growth visibility in 2024 presents a major concern for me.

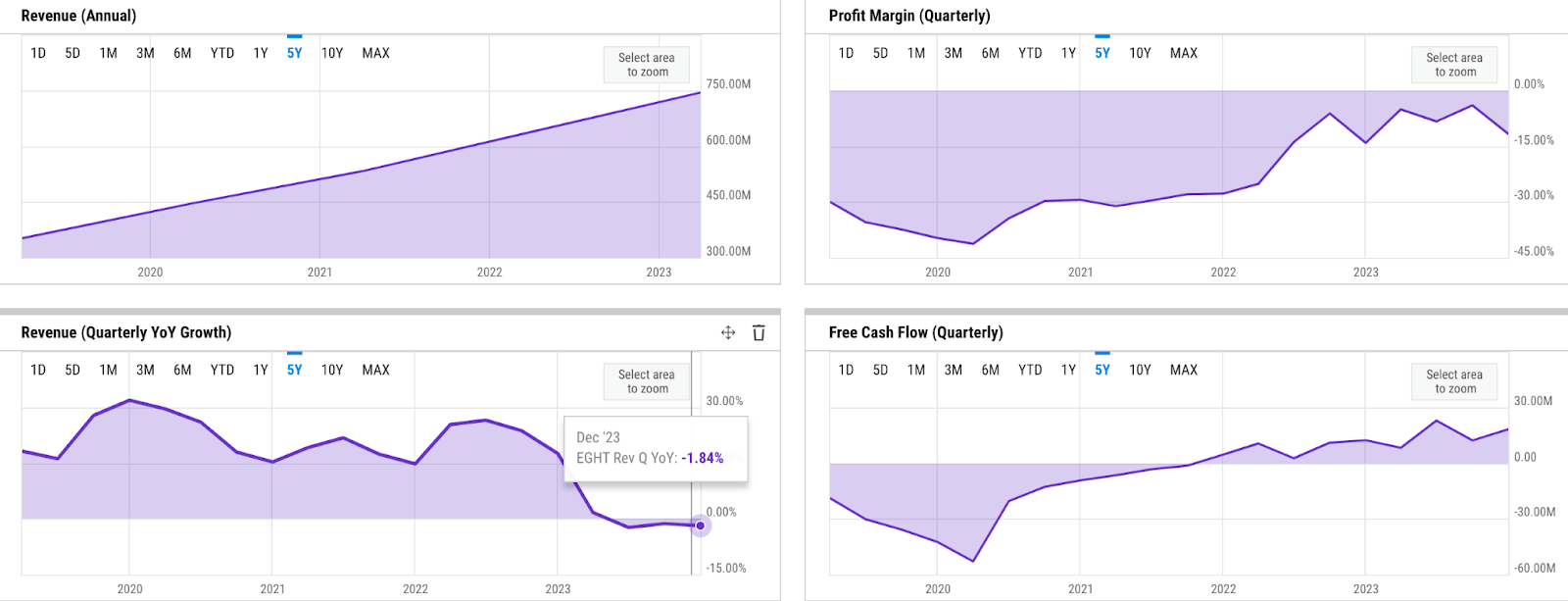

key metrics (YCharts)

EGHT's fundamentals have a mixed outlook. It has never been profitable over the past five years, but the net loss margin has significantly narrowed. EGHT saw a -40% quarterly net loss margin at some point in 2020, a stark contrast to -11% in the most recent quarter, Q3 2023.

In the meantime, revenue growth has been consistently declining for most of 2023, making EGHT potentially finish FY 2023 with a negative growth rate. A positive thing here would be a consistent FCF expansion pattern upon breakeven sometime in 2022. In Q3, EGHT generated over $18 million of FCF, already about 50% YoY growth, and over 4x where it was in Q3 2021.

key metrics (YCharts)

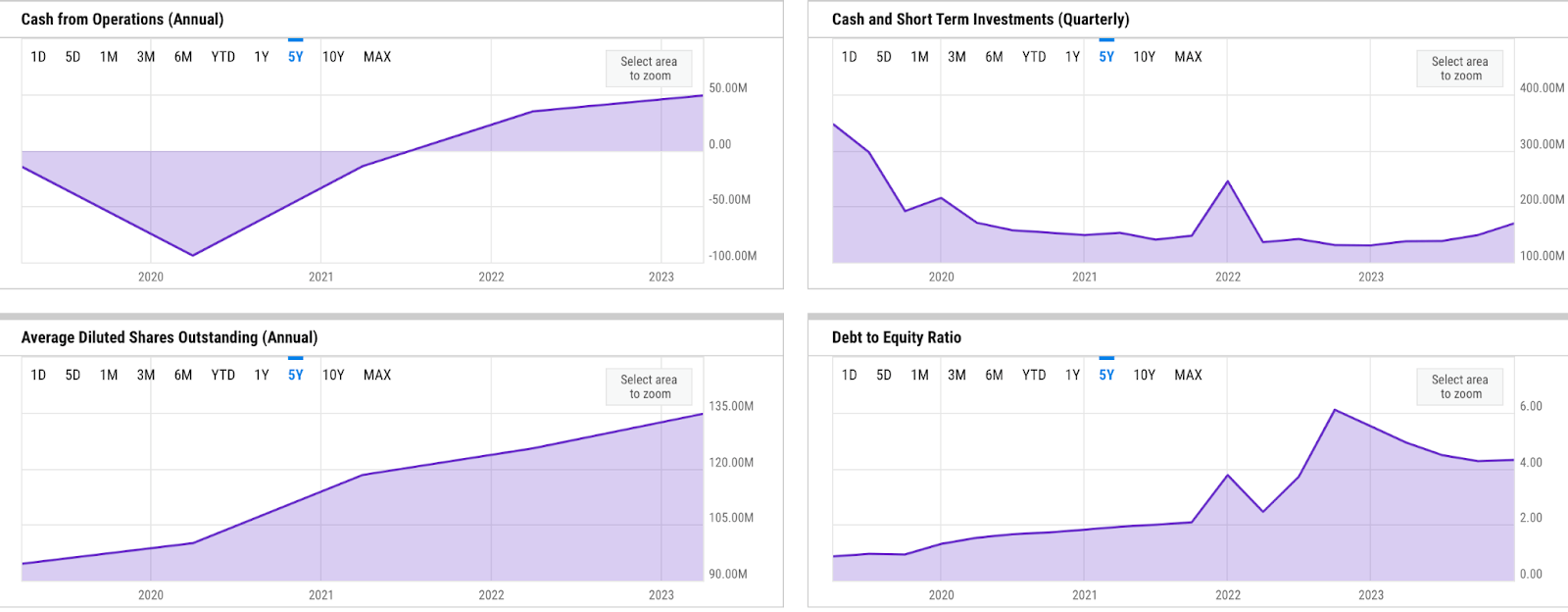

The biggest driver of FCF has been EGHT's expanding operating cash flow / OCF. After reaching breakeven point and generating over $34 million of OCF in 2022, EGHT continued to see an expansion to $48 million in 2023.

The balance sheet outlook has been moderate. Liquidity has seen expansion from $130 million in 2022 to over $169 million in December 2023. The strength in FCF as of late has also reduced dependencies on cash flows from financing. However, stock offerings made to boost liquidity since 2021 have resulted in a considerable share dilution. It is important to note that EGHT's share price has been trending down since 2021, making dilution more pronounced as offerings were taking place.

Meanwhile, the history of sizable net losses since 2016 has widened the accumulated deficit significantly, effectively increasing the debt-to-equity / DE ratio to above 4x as of late - a relatively undesirable level in my view. This was exacerbated by doubling long-term debt levels since 2019.

Several key factors could act as catalysts for the stock price. However, I believe their near-term effects could be minimal at the time being.

Firstly, the positive uptake experienced by CPaaS offerings could signal growth bottoming out and reaccelerating in 2024, in my opinion. The challenging macro situation today could support this idea. Due to the uncertain macro outlook, I would expect many businesses to prioritize the more efficient ways to grow sales. This trend aligns well with EGHT's CPaaS value proposition:

We also continue to expand our outbound customer engagement capabilities available through our CPaaS solutions, enabling customers to build more effective, customized outbound campaigns. With just a few new products at general availability, we are already seeing 60% year-over-year growth in revenue from our new products, with quarter-on-quarter acceleration driven by workforce optimization, our intelligent customer assistant, digital and voice, payments compliance solutions, all wrapped in add-on subscription-based services.

Source: Q3 earnings call.

Beyond CPaaS growth, EGHT is also focusing on improving its financial fundamentals. In my view, successful execution of these initiatives could provide some boost to market confidence.

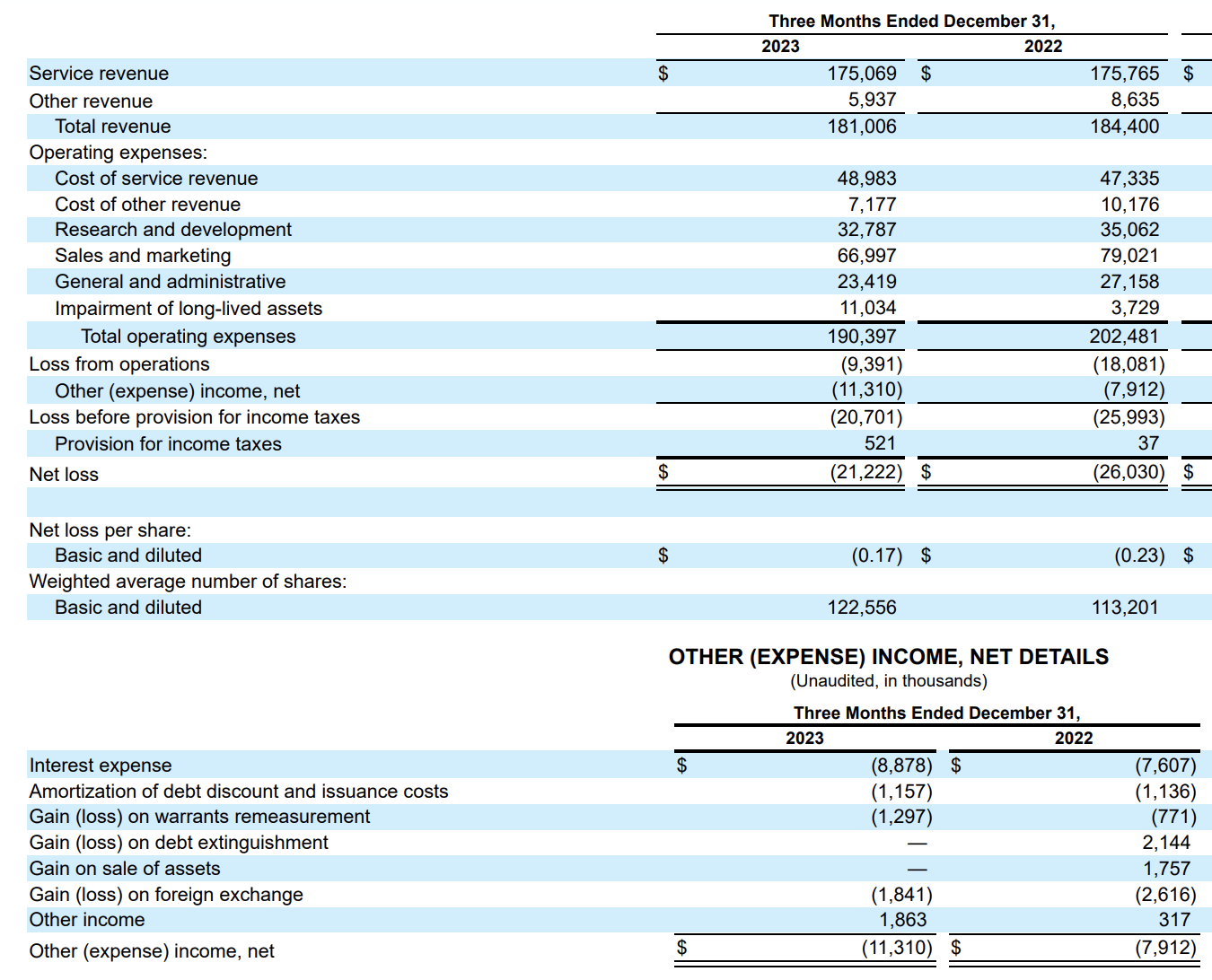

income statement (10Q)

Among several considerations, a meaningful one that seems sensible would be potential debt refinancing. The debt level has doubled since 2019, and in December 2023 still sat around $400 million despite recent repayment. As discussed briefly during the Q3 earnings call, EGHT has indeed seen improved profitability and cash flow generation in recent times, which has demonstrated potential for refinancing at better terms. Refinancing could help narrow net loss further. In December 2023, over 40% of EGHT's net loss of -$21 million was driven by interest expense.

Consequently, these activities should strengthen the financial position and free up resources for further growth initiatives. In conjunction with the mitigation of more pronounced share dilution by shifting towards cash compensation for employees, I believe they hold the potential to drive up share prices.

Last but not least, EGHT is also still well-positioned to benefit from the booming AI trend. Expanding existing AI integration unlocks exciting potential, such as advanced AI chatbots, seamless human-agent transitions, or CPaaS solutions powered by AI-driven customer insights:

Customers like Walsall Housing Group in the U.K. and Teradata are implementing 8x8 solutions to take advantage of our seamless integration with teams, our global presence, and our unified UCaaS and CCaaS capabilities, including AI-driven digital self-service.

Source: Q3 earnings call.

Risk remains high. In particular, I consider the lack of product adoption as a key risk factor. While the reported 60% growth in new products is promising, it's still too early to predict a clear trend reversal that will positively impact the stock price, in my opinion.

On the other hand, EGHT's decision to integrate AI into its platform also holds potential. However, navigating this exciting space comes with risks that investors should carefully consider.

One key challenge is the intense competition. While EGHT embraces AI, established players and agile startups are doing the same. As such, simply riding the AI wave won't suffice, in my opinion. In the CPaaS space alone, we see players like Twilio (TWLO), Infobip, or Sinch competing for market share. To truly capitalize, I believe EGHT needs to clearly differentiate its offerings, showcasing the unique value proposition its AI features bring to the table.

The timing mismatch between EGHT's AI's go-to-market and broader AI penetration in the contact center industry also creates a potential risk. EGHT's main revenue model relies heavily on platform usage and seat-based fees, which pose a long-term threat if AI disrupts traditional usage patterns. This is where things get tricky. As AI becomes more mainstream and competitors offer superior solutions, EGHT could see declining market share if its own offerings don't keep pace.

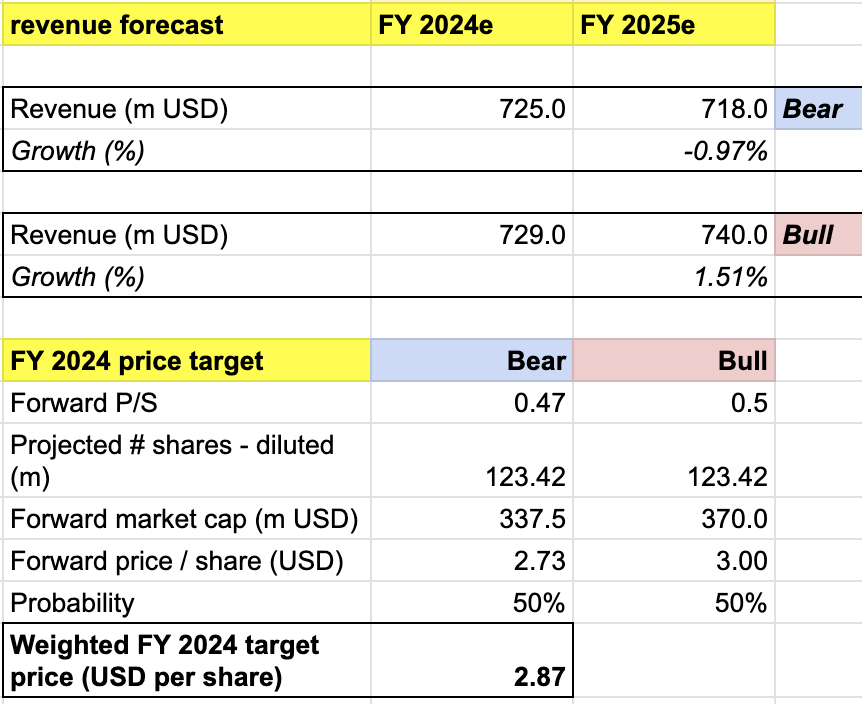

My target price for EGHT is driven by the following assumptions for the bull vs bear scenarios of the FY 2024 projection:

Bull scenario (50% probability) assumptions - EGHT to achieve FY 2024 revenue of $729 million, at the high end of the market's estimate. EGHT to also achieve $740 million of revenue in FY 2025, missing the high-end estimate. Given the potential margin expansion and revenue growth reacceleration, I expect P/S multiple to expand slightly to 0.5x.

Bear scenario (50% probability) assumptions - EGHT to deliver FY 2024 revenue of $725 million, missing the low-end analyst's estimate. In FY 2025, revenue growth deteriorates further, leaving EGHT with a revenue of $718 million, a -0.97% YoY decline. In this scenario, I would expect EGHT to face increased competition and go-to market challenges. I assign EGHT a 0.47x forward P/S, where it is trading today, implying a correction to $2.7.

price target (own analysis)

Consolidating all the information above into my model, I arrived at a FY 2024 weighted target price of $2.87 per share, suggesting a 12% upside from the current price level of $2.5.

I maintain my neutral rating on the stock. At $2.5, the share price seems to be at a depressed level and may present a speculative opportunity for some investors. However, the uncertainty around EGHT's growth prospects remains a key concern for me. I would advise interested investors to monitor EGHT's performance for early signs of sales momentum in 2024 before dipping in.

Despite its established presence in cloud communications, 8x8 faces a crossroads. Opportunities, like CPaaS focus and AI integration, are promising, but challenges persist. The stock's volatile history and uncertain 2024 outlook warrant caution. While my target price suggests potential upside, I maintain a neutral rating pending progress on strategic initiatives and clearer growth visibility.