Joan Manel Moreno/iStock Editorial via Getty Images

Joan Manel Moreno/iStock Editorial via Getty Images

Euronet Worldwide (NASDAQ:EEFT) is a growing company that has now reached pre-pandemic income levels again. In case there are no major economic and travel disruptions, the company will continue to grow. However, this growth is already priced into the stock, and it is not a bargain anymore as it was last year in October.

On February 6, 2024, the company published its fourth quarter and full-year financial results for the year 2023. Therefore, it is a good time to check the performance and see whether the stock is suitable for the portfolio.

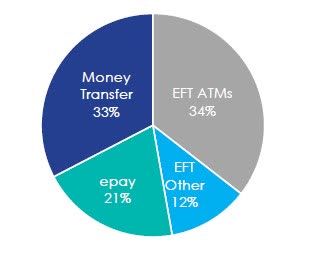

Euronet provides payment processing, especially for financial institutions, retailers, and individual consumers. Their revenue comes mainly from the ATM network, the POS (point-of-sale) terminal network, processing fees for the distribution of electronic content, and money transfer services.

The company operates in three segments:

Fourth Quarter and Full Year 2023 Results Presentation

Fourth Quarter and Full Year 2023 Results Presentation

Fourth Quarter and Full Year 2023 Results Presentation

There is nothing wrong from a business perspective. The company is growing in each segment, new contracts are being signed and new services launched.

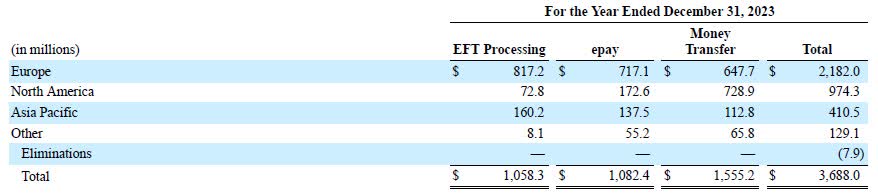

Euronet growth by segment (Table: Author; Data: Euronet 10-K report)

The EBITDA is also diversified across the segments, so if there is a problem in one segment, it should not have a devastating impact on the company.

Fourth Quarter and Full Year 2023 Results Presentation

Most of their revenue comes from Europe (59%), and in the case of ETF processing, more than 77% of revenue is from Europe, so they are heavily dependent on the economic situation and travel in Europe.

Euronet source of revenue by region (Euronet 10-K report)

However, during my research, I have discovered complaints from inhabitants of Europe about their value-added service for ATMs and POS terminals, which they call dynamic currency conversion ("DCC"). So, what is this service? I've provided a short explanation below (source: Euronet 10-K annual report for 2023):

The customer is offered a choice between completing the transaction in the local currency or in the customer's home currency via a DCC transaction. If a cardholder chooses to perform a DCC transaction, the acquirer or processor performs the foreign exchange conversion at the time that the funds are delivered at an ATM. Alternatively, the customer may have the transaction converted by the card issuing bank, in which the amount of local currency is communicated to the card issuing bank and the card issuing bank makes the conversion to the customer's home currency.

When a customer chooses DCC at an ATM, Euronet receives the entire foreign exchange margin. This margin increases the amount Euronet earns from the underlying ATMs and supports the deployment of additional ATMs in new locations.

What does it mean in practice for you as a client? Well, imagine you are on holiday and want to withdraw some cash in the local currency. You come to the ATM, put your card inside, type the amount you want in cash, and the ATM asks you whether you want to withdraw it "with conversion" or "without conversion." Do you know which answer is the correct one? If not, you may end up paying 15% or more for the withdrawal. Imagine you withdraw €100 from an ATM and have to pay €15 or more for this service. You probably will not be a happy customer.

You can even find many articles on this issue on the web with advice on what to do in case you have to pick up money from a Euronet ATM. I have found one good article (it is not in English, so I provided a short translation below).

Euronet is a non-banking company focused on financial transactions. It's not a bank. It charges its own fees. If you are currently on vacation and you are standing in front of a Euronet ATM, do not withdraw money from it. Withdraw from the ATM of a local bank or pay by card.

An ATM from Euronet Worldwide will offer conversion every time you use a foreign payment card. Avoid the conversion it offers if you can. ATMs offer a worse exchange rate and you will pay 10 to 35% more for a withdrawal.

We do not recommend accepting a transfer in another currency. If for some reason you have to use a Euronet ATM, select the "Reject conversion" option. This will force the ATM to use the official exchange rate for your currency.

There will always be some customers unsatisfied, and the complaint about their DCC service is the only complaint I could find. For me, it's not that serious for the future growth of the company. Well, somehow the company has to make money for the shareholders. Let us now check the business financials and see if there is no hidden issue.

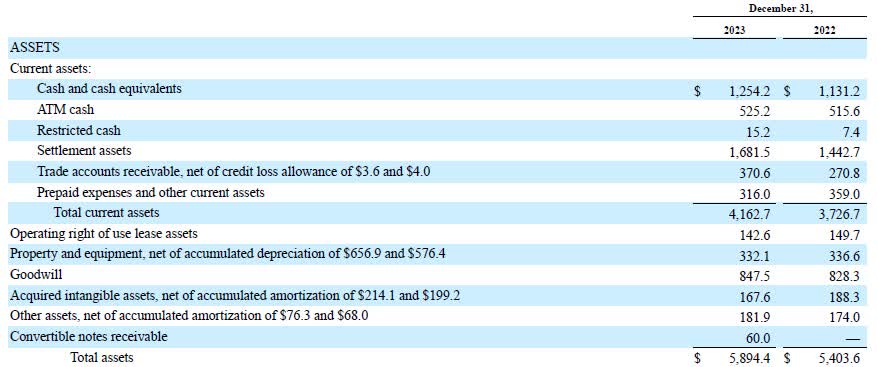

At the end of 2023, they had cash and cash equivalents of $1,254.2 million and ATMs of $525.2 million, so their total cash position was $1,779.2 million. However, they require a substantial portion of the cash as working capital to finance their operations.

Euronet 10-K report

There is also $847.5 million of goodwill, suggesting that the company is engaged in a significant number of acquisitions. Settlement assets represent only the time difference between currency outflow and currency income, and we don't have to burden ourselves with them.

Euronet 10-K report

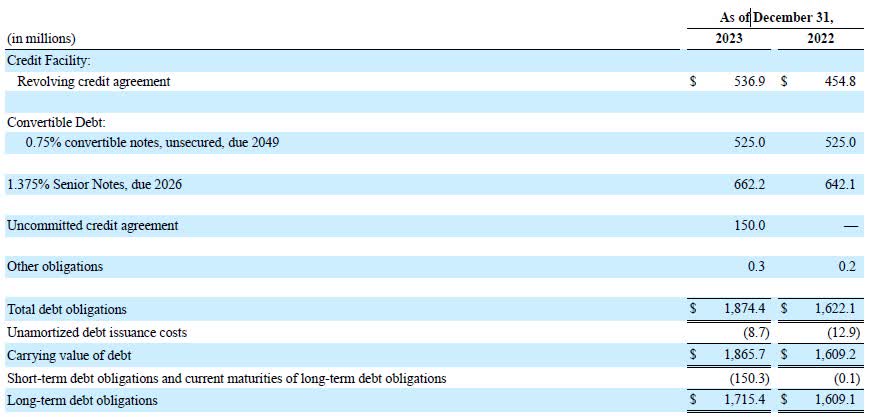

There is nothing extraordinary on the balance sheet that one should be worried about. The company has $1,874.4 million in debt, which is financed by a credit facility with an interest rate of 6.5% as of December 31, 2023, and an uncommitted credit agreement with an interest rate of 6.37%, which is used to provide vault cash for ATMs. Euronet also has convertible notes with a very low-interest rate of 0.75%, which are due in 2049 and can be converted to common stock at $188.73 per share. These terms are favorable for Euronet; however, there is a small catch. Convertible notes must be repurchased by the company on March 15, 2025, if their holders ask Euronet to do so. The repurchase price will be equal to the principal. Considering that the current 10-year Treasury rate is at 4.26% and the stock price is $80 lower than the conversion price, I would ask the company to purchase the notes back if these conditions persist in 2025. The senior notes due in 2026 will affect the company's debt profile only two years from now, so there is nothing to worry about for this year. But if they have to refinance the debt next year and the year after at current rates, their interest expenses will go up, which will hurt the net profit.

Dept obligations (Euronet 10-K report)

Operating and net income were significantly impacted during the pandemic in 2020 and 2021, and they have not reached 2019 levels since. This suggests that the company is dependent on economic activity and travel, primarily in Europe, which is not far from a recession. The good news is that they are back on their growth trajectory and anticipate further growth in 2024. The company expects its 2024 adjusted EPS to grow by 10% to 15%.

Seeking Alpha; Euronet 10-K report

Diluted EPS for the year 2023 was $5.50, giving a P/E ratio of 19.78, which is not low. Of course, the earnings look much better when you use adjusted earnings, which were $7.46 for 2023, but I do not like adjusted earnings.

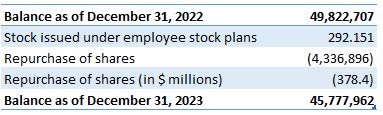

The company is also engaged in share buybacks, having spent $378.4 million to reduce the number of shares by 4 million. This represents a cost of $99.53 per share, and despite an 8% decline in the number of shares, the share price has remained almost the same, which tells me that there is some selling going on.

Number of Shares Outstanding (Table: Author; Data: Euronet 10-K report)

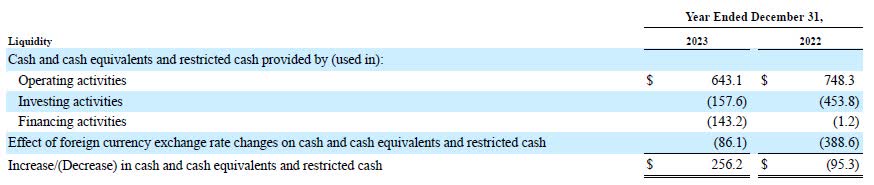

When we look at the cash movements, it looks good, but we have to look deeper to understand it better, as it is not that simple.

Euronet 10-K report

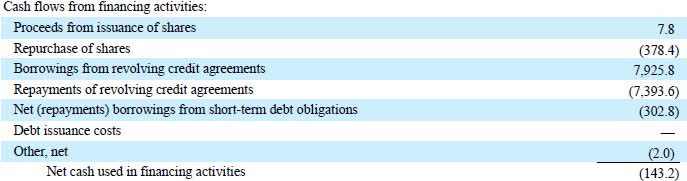

The difference in operating cash flow was caused mainly by the timing of the settlement processes with third parties and is not a big deal. Investment cash flow was lower as there were no material acquisitions in 2023, and they just used $94.4 million for purchases of property and equipment. The interesting move was in the financing cash flow, where their net borrowing was $229.4 million, as they needed the cash for share repurchases.

Euronet 10-K report

Now that we know how the company is making money and have an overview of their finances, let us value the company.

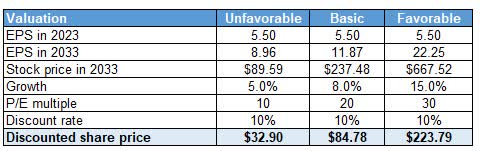

For the valuation, I will use my DCF model and EPS (not adjusted EPS), as they better reflect the value created for the shareholders due to the share buybacks that the company is doing.

When I look at the analyst estimate, they expect revenue to grow by 8%, so I will use it for EPS growth in my basic scenario.

Seeking Alpha

I have also checked the valuations of peers and sector median. The lowest valuation has Western Union (WU) P/E = 7 and the highest Shift4 Payments (FOUR) P/E = 45.

Seeking Alpha

I have prepared three scenarios:

Author

The current stock price is $108.80, and for me, the stock is more than fully priced. It is a good, growing business, but I am missing a margin of safety here.

There are risks connected with my thesis. The most relevant are:

Euronet is a good company that is still growing and providing competitive services to its customers worldwide. They will probably continue to grow in the coming years too, as I do not think that the current money system and cash will go away until the end of this decade. For me, this company is overpriced, as my base case price is more than $20 below the current stock price. The stock may be a buy again if the price is below $80, but for now, it is priced for an 8% discount rate with 8% yearly growth, and I am focusing on companies offering higher growth.

In the long term, I see risks connected with the future of money transfers and cash, as each government would like to eliminate cash, have an overview of all transactions, and collect more taxes. Will this happen? Maybe. When will this happen? I have no idea.