Smith Collection/Gado/Archive Photos via Getty Images

Smith Collection/Gado/Archive Photos via Getty Images

Ecolab (NYSE:ECL) is a high-quality business selling water, hygiene, and infection prevention solutions. The company is resilient because 95% of its sales are recurring, and cleaning products are non-discretionary. Additionally, Ecolab dominates the fragmented markets in which it operates because it benefits from economies of scale. Ecolab can secure exclusive contracts with businesses because it can outbid smaller competitors. Ecolab also has an excellent track record of capital allocation - Ecolab has consistently repurchased stock, paid dividends to shareholders, and made smart acquisitions. Unfortunately, Ecolab’s 30%+ runup since October last year has left the stock too expensive.

Ecolab’s Q4 earnings were good, but most information was in line with expectations or inconsequential. However, management gave investors some visibility into what 2024 will look like. Management expects 2%+ pricing growth in 2024 and expressed increased confidence in their 20% operating income margin target.

Analysts questioned the 20% operating income margin target during the call, so management tried to defend it with several points. For example, management noted that Ecolab’s institutional segment continues to recover from COVID (390 bps increase in operating margin YoY). Ecolab’s company-wide gross margin is also below pre-COVID levels. Additionally, management noted that delivered product costs are still up 35% since 2019, so some easing can be expected in 1H 2024.

Analysts project 5-6% revenue growth (retrieved from CapIQ) over the next five years. I don’t expect revenue growth to surprise to the downside because management is expecting 2%+ pricing growth, acquisitions should add a few percentage points of revenue growth per year, and R&D spending remains at just below 200 million dollars per year (which should add a few percentage points to revenue growth). (Reinvestment/Sales) can be multiplied by Sales/(Invested Capital) to get a fundamental growth rate (I am only considering R&D as reinvestment in the calculation below). If anything, I think revenue growth will beat estimates if Ecolab pulls off a large acquisition.

S&P Capital IQ

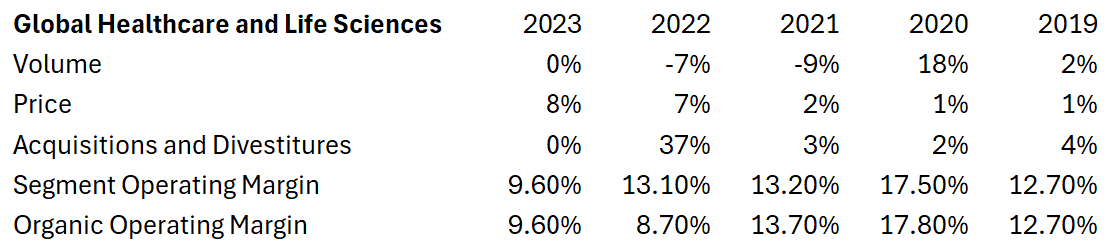

Ecolab’s healthcare business, which should be driving revenue growth for Ecolab, is currently struggling. Christophe Beck, CEO of Ecolab, made the following statement in Ecolab’s Q3 conference call:

So, I’ve not been happy with the performance of Healthcare for many years.

Ecolab Investor Relations

Ecolab’s healthcare and life sciences business has grown primarily through acquisitions and price increases, whereas volume has remained roughly flat (assuming COVID didn’t happen). Given the underwhelming performance of the healthcare and life sciences business, it’s slightly concerning to see growth from acquisitions rather than more significant efforts from management to improve the existing business.

Ecolab appears to be a mature business operating in mature markets, given that volume growth is 1-2% annually in its core business. Unfortunately, Ecolab cannot look to international markets for growth because international markets are far less profitable than domestic markets (import costs, smaller scale, reliance on distributors and agents). Also, management noted that two-thirds of Ecolab’s new business is from cross-selling in Ecolab’s Q3 conference call, indicating that Ecolab is acquiring very few new customers. Additionally, Christopher Beck said, “I don’t think our team is going to get much bigger,” suggesting that Ecolab’s growth prospects are relatively limited.

Ecolab Investor Relations

Ecolab Investor Relations

Pricing has been the critical driver of revenue growth for Ecolab. Ecolab has increased prices aggressively thanks to its new value-based pricing strategy. However, prices cannot increase forever because competition exists in Ecolab’s markets. Given management’s guide for 2%+ pricing in 2024, it seems like price growth is slowing down. Slower price growth should be expected, given how much prices have increased. Of course, investors should also consider that price increases will take away from volume increases.

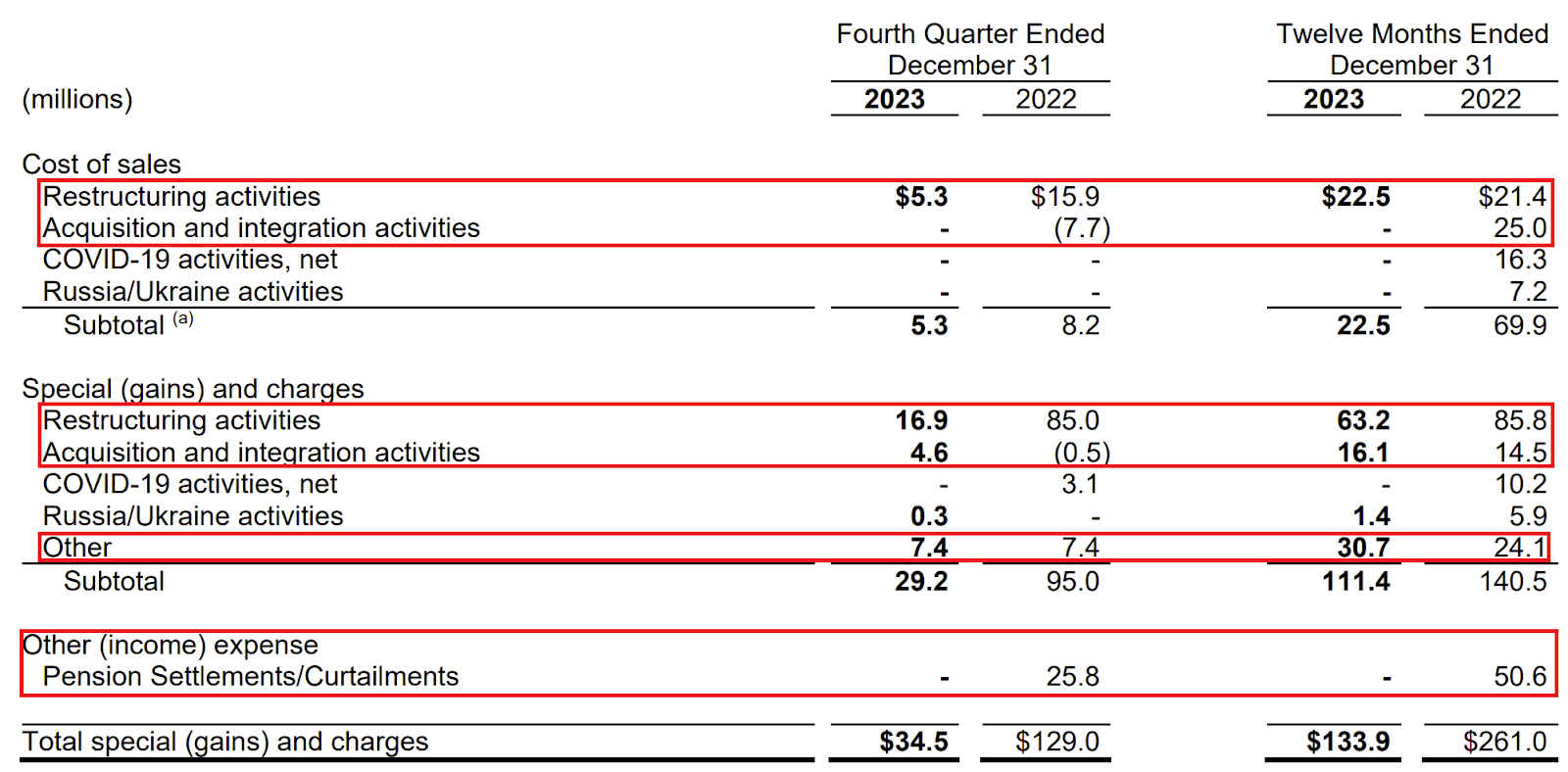

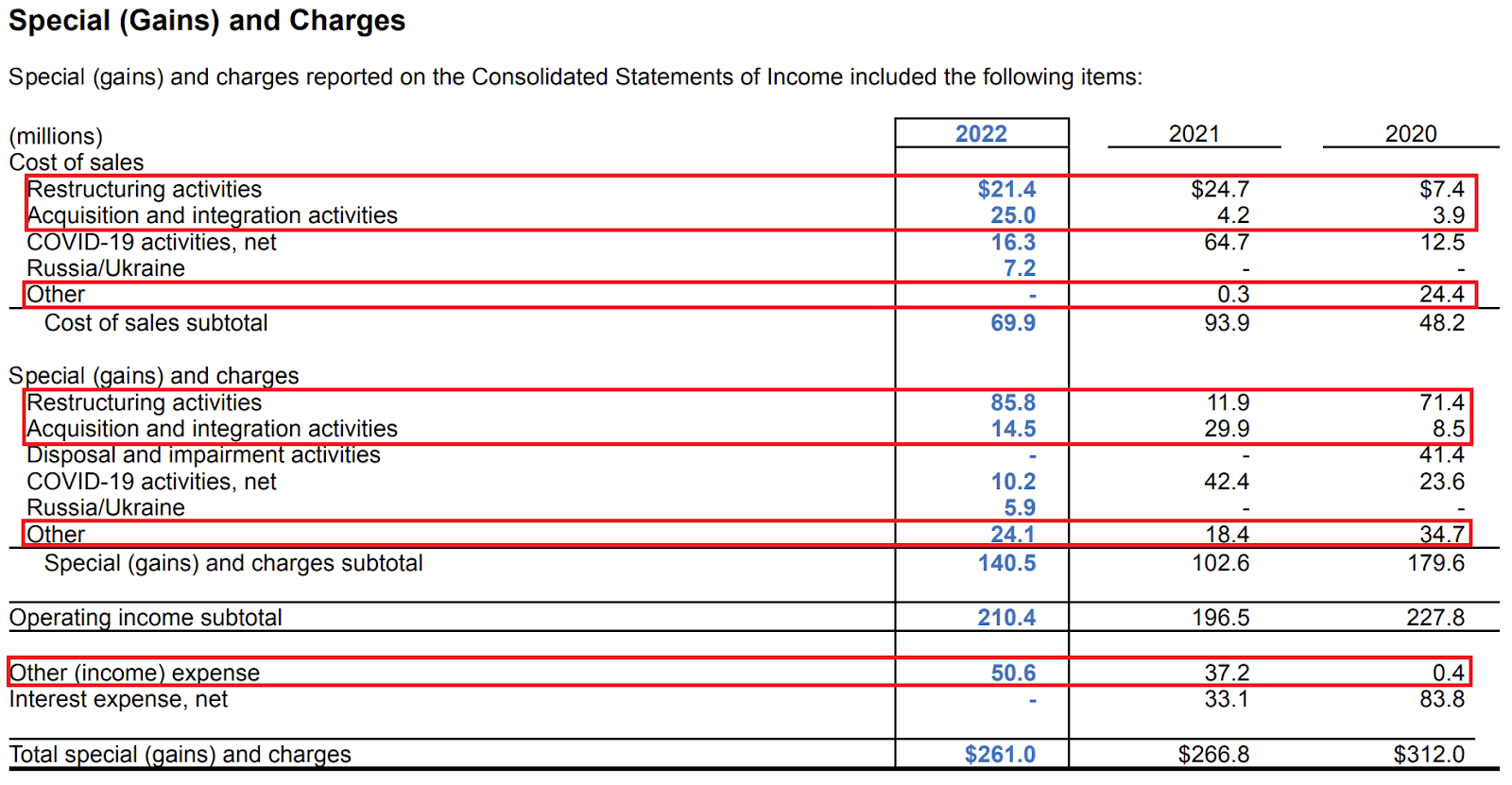

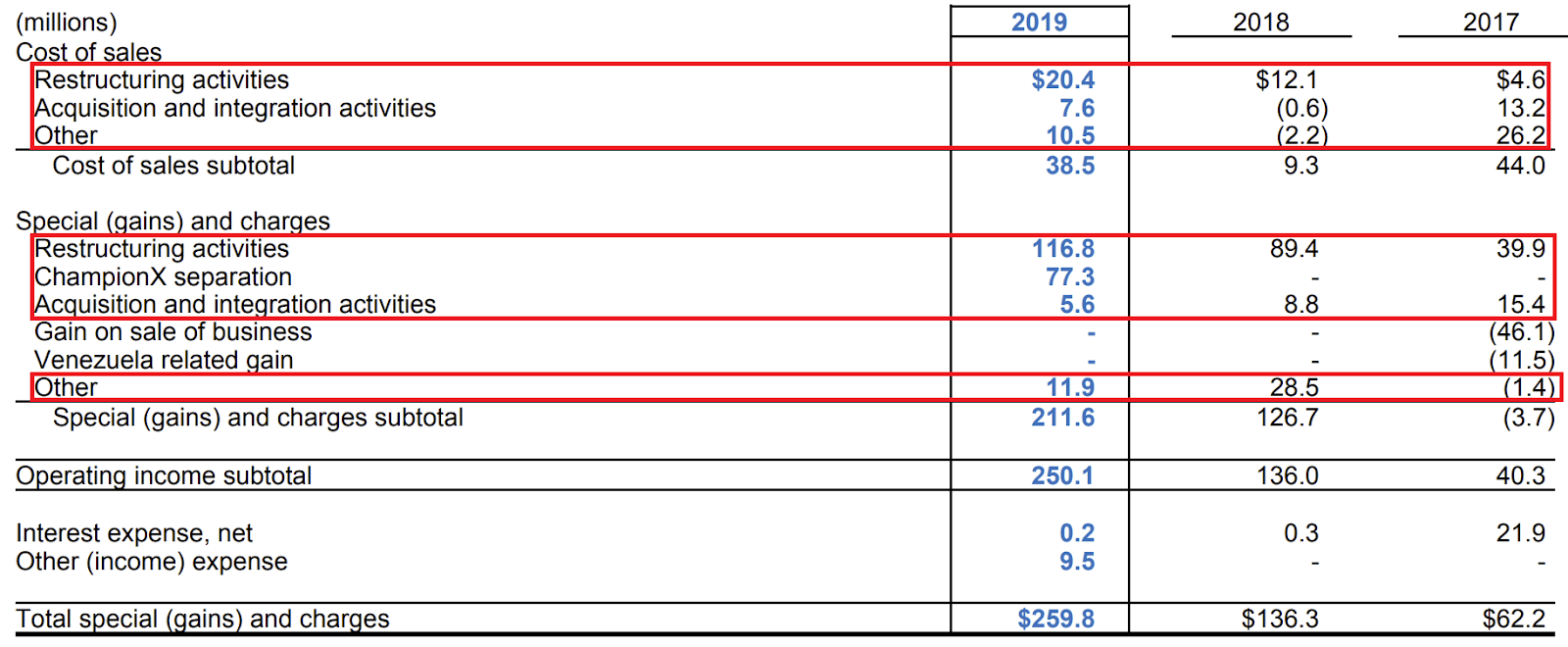

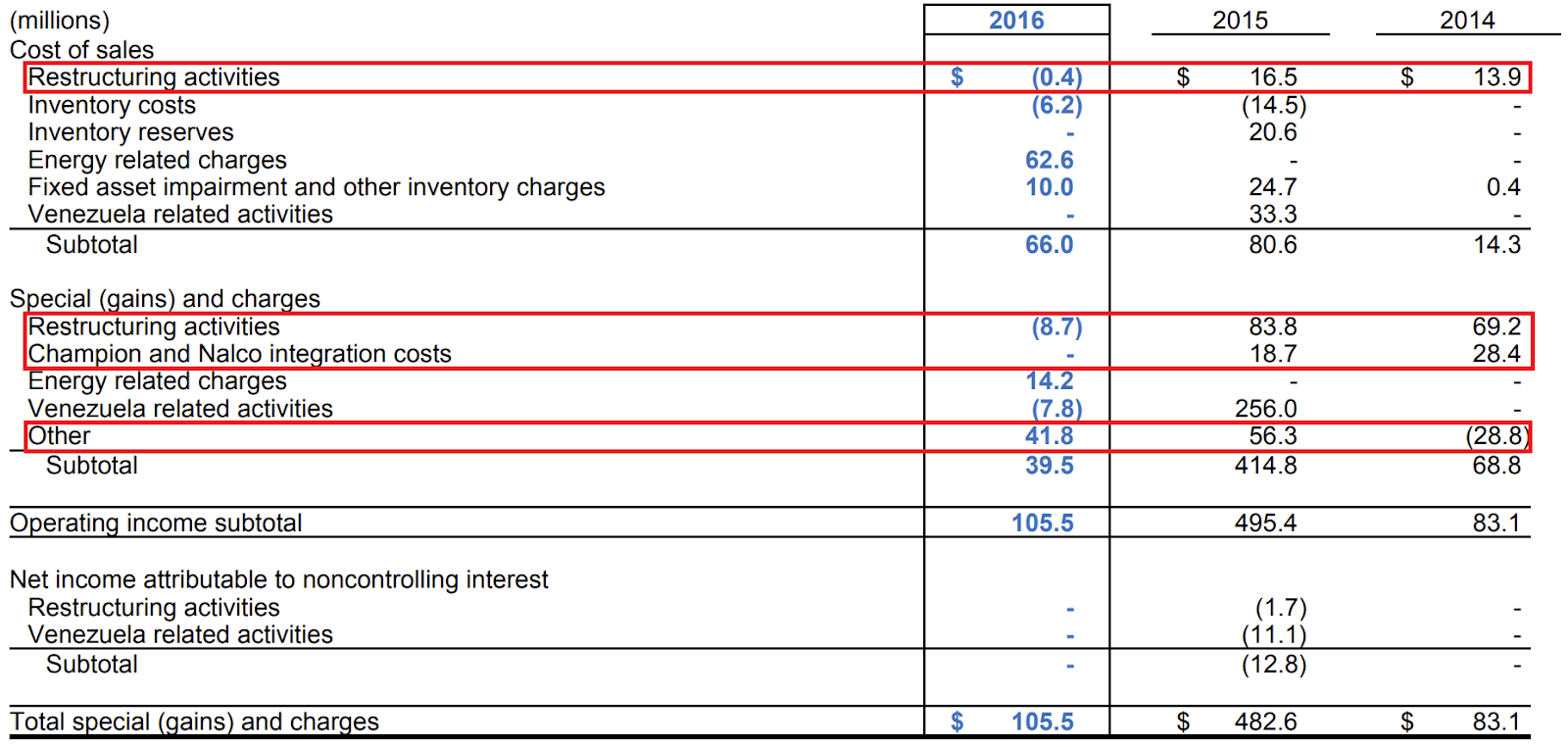

Management has repeatedly talked about reaching 20% operating margins, but management’s non-GAAP operating income numbers add back numerous “special” charges. The most notable add-backs are restructuring activities, acquisitions/integration activities, and other expenses. Despite being classified as “special charges,” these items appear yearly, resulting in $100-$300 million in annual add-backs (2023 operating income was ~$2.1 billion). In my opinion, management shouldn't add back any of these charges to operating income:

The majority of other expenses are legal fees, which show up yearly.

Ecolab Earnings Release

Ecolab 10-K

Ecolab 10-K

Ecolab 10-K

Ecolab Investor Relations

A substantial amount of Ecolab’s earnings growth has come from declining taxes. If anything, taxes should stay constant or increase in the future because Ecolab’s tax rate is below the worldwide average corporate tax rate (~25%), and the OECD recently got >140 countries to agree on a 15% global corporate minimum tax rate.

Author's Calculations

Author's Calculations

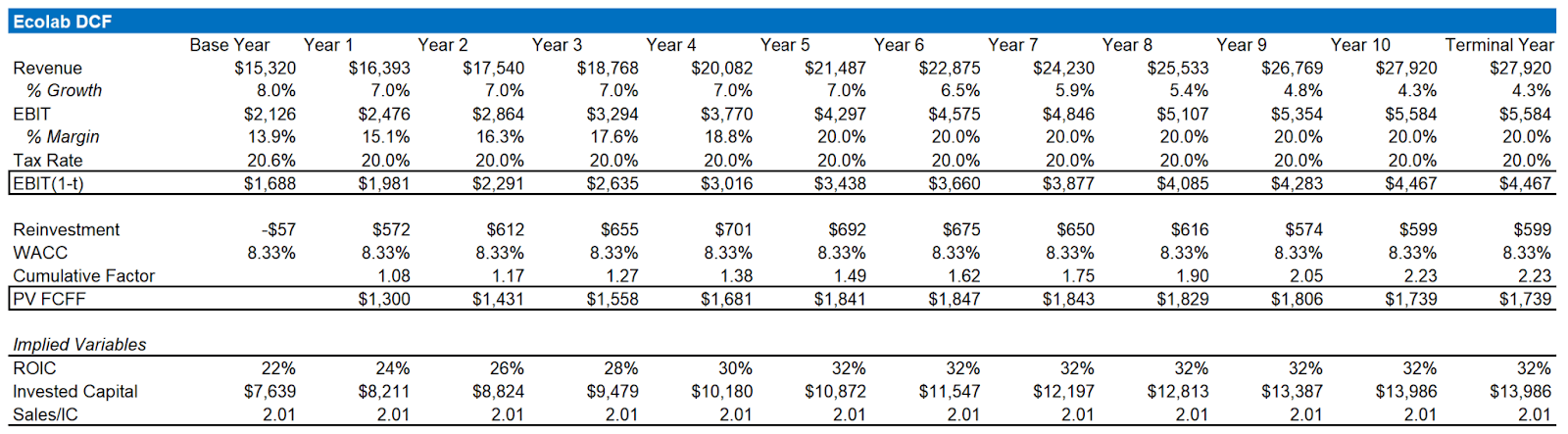

Revenue Growth: I assume 3% growth from pricing, 2% growth from volume, and 2% growth from acquisitions for years 1-5. Then, I assume Ecolab’s growth rate moves linearly towards the growth rate of the economy (4.3%, which is the 10-year rate).

Operating Margin: I assume that Ecolab’s operating margin will move linearly toward 20% over five years. I believe this assumption is optimistic because management is adding back expenses to non-GAAP operating income.

Tax Rate: I assume Ecolab’s tax rate stays at 20% (close to current levels). This assumption is likely optimistic because Ecolab’s tax rate is below the global average corporate tax rate.

Reinvestment: I calculate reinvestment using Ecolab’s Sales/(Invested Capital) ratio. Reinvestment is (Increase in Sales the Following Year)/(Sales/(Invested Capital) ratio).

Terminal Growth Rate: The risk-free rate (10-year rate), which is a proxy for the growth rate of the economy

Terminal ROIC: I use the ROIC from year 10. This assumption is likely optimistic because competition usually reduces excess returns over time.

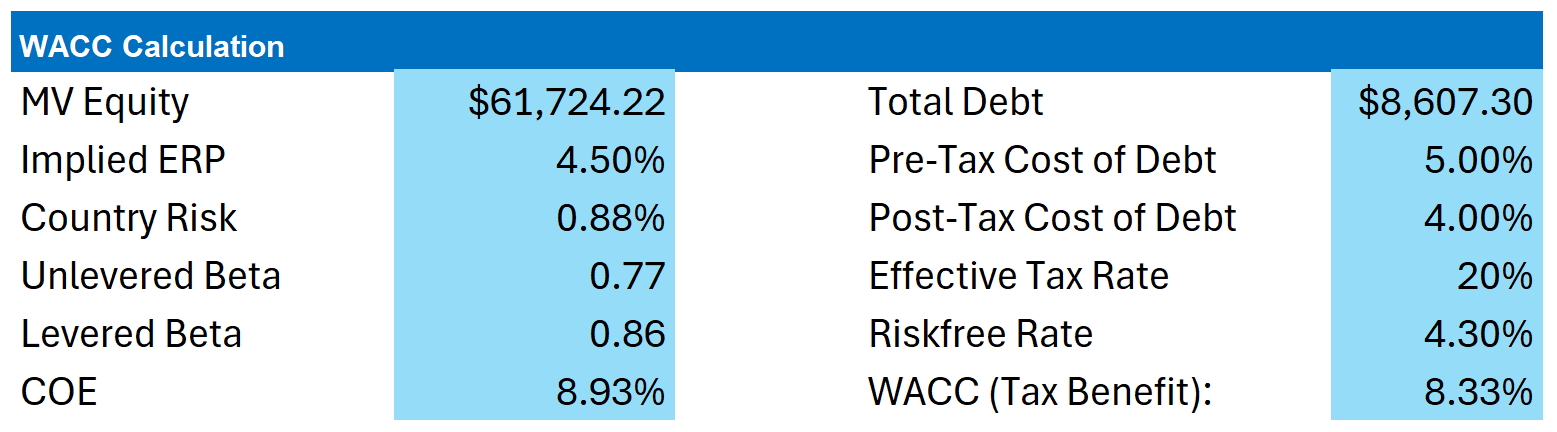

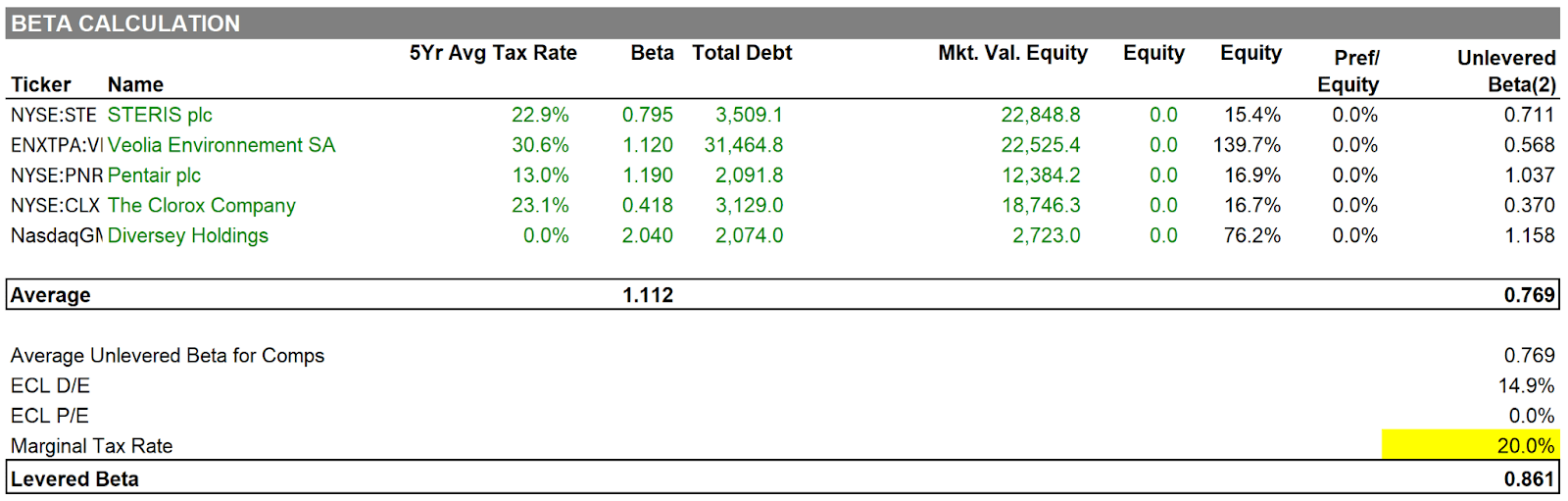

WACC: Beta is a bottom-up beta, pre-tax cost of debt is the YTM on Ecolab’s bonds, country risk premium was calculated using data from Aswath Damodaran’s website, implied equity risk premium was taken from Aswath Damodaran’s website

S&P Capital IQ

S&P Capital IQ

S&P Capital IQ

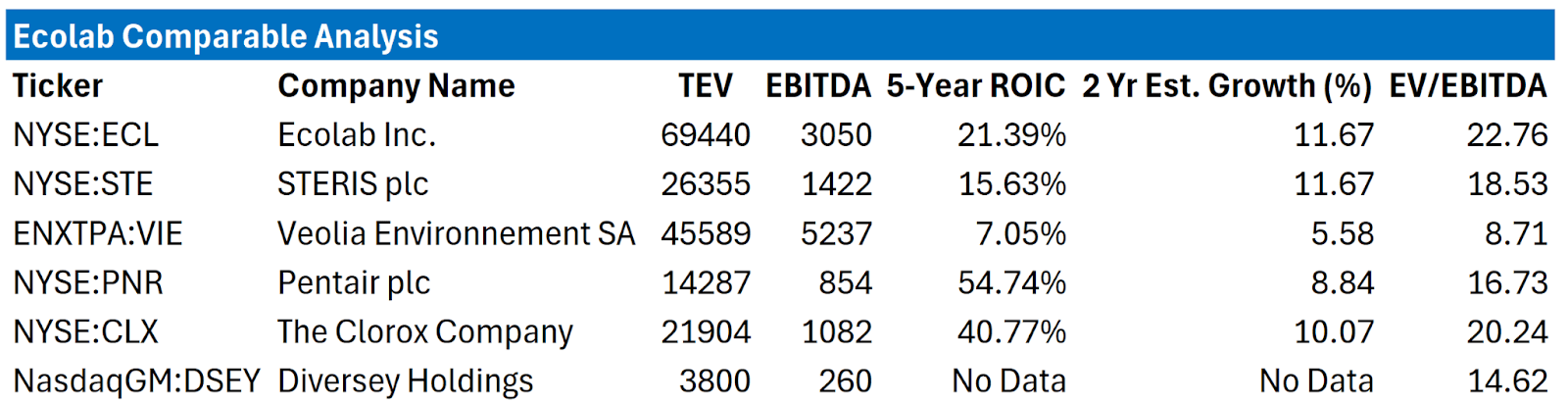

Ecolab looks expensive on a relative basis because it trades at a higher multiple relative to its peers. Yet, its ROIC and 2-year estimated EBITDA growth (analyst estimates) are in line with peers. My view is that Ecolab could be interesting at <18x EBITDA.

Although Ecolab is an excellent business that arguably deserves a place in a buy-and-hold portfolio, I believe it’s unlikely to outperform the market over the next five years. Investors seem to be pricing in management’s 20% operating margins and aggressive growth estimates (given that I’m getting to ~$180/share in my DCF). I believe Ecolab will likely fall short of investors’ expectations, so investors shouldn’t consider buying the stock until a correction occurs. I’ll be on the sidelines until Ecolab falls below $150/share.