nicoletaionescu

nicoletaionescu

Co-Authored by Treading Softly

When I was a kid, I used to love the idea that every morning would be Christmas morning. Wake up; all the magic is there. All the presents are there. The time with family where no one had to go to work was there.

For many of us, Christmas morning symbolizes a wonderful time in our childhood when we look forward to all the magic that comes with Christmas. Yet, part of the reason that Christmas morning is so special is that it does not happen every day. If every morning were Christmas morning, then Christmas morning would lose the specialness that surrounds it.

When it comes to the market, I often get asked if I ever get tired of talking about income investments. My skills in analysis and fundamental research would allow me to investigate and discuss a lot of different types of investing. I could use them to evaluate growth investments or momentum trading. Yet, whenever I start to look into those types of investments, I find that I see no magic there. Not that you can't make millions of dollars being a momentum trader or a growth investor - there's plenty of evidence of that. The joy and the excitement of investing do not lie within those aspects for me. Instead, I like to use my money to place into investments in areas that will reward me back with income, but also that I can place my confidence in. For me, that is investing in the U.S. economy and understanding the specialness that is there. Unlike so many other economies, the U.S. economy is a place that for many is like Christmas morning. The ability to start a company, watch that company grow, and develop - it is unique and special. You do see that occurring in other economies and countries, but here is something special about the U.S. economy's ability to support an entrepreneur in seeing wealth development.

Today, I want to take a few minutes and look at an investment that focuses on supporting the U.S. economy through its debt. This is not an investment that focuses on U.S. government debt. No, this is an investment that focuses on supporting businesses of all shapes and sizes that make up the U.S. economy.

Last month, we looked at this opportunity and determined that it was well worth holding to enjoy strong recurring income, but we were unsure if supplemental distributions would confine. Now that the score is in for 2023, let's update our outlook.

Let's dive in!

Eagle Point Credit Co LLC (NYSE:ECC), yielding 17.2%, went into 2023 with NAV of $9.07/share and paying a distribution of $0.14/month for a yield on NAV of 18.5% - something widely declared "impossible". Anyone who suggested buying it was accused of "yield-chasing" followed by endless charts about how much ECC lost over this or that period. They are "returning your own capital"!!! Only X% annualized returns since such and such date.

The score is in for 2023:

ECC NAV December 31, 2022: $9.07

ECC NAV December 31, 2023: $9.21

ECC distributions to shareholders in 2023: $1.86

Total return on NAV: 22%

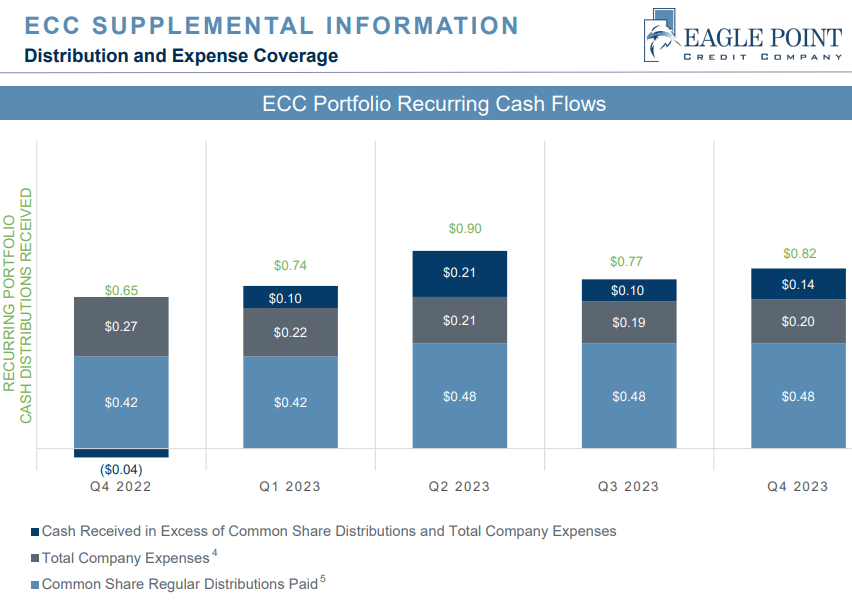

ECC raised its distribution in 2023. Even with a higher distribution, it was able to cover it with cash flow and had extra to spare. Source

ECC Q4 Investor Presentation

ECC announced that it is extending its $0.02/month supplemental distribution through the first half of 2024.

How is this possible? Because CLO equity has been trading at very low prices, even as it has outperformed fundamentally. At the end of the day, CLO equity investments are a "credit risk" investment. The main risk/reward of the investment is based on how many borrowers repay as agreed, compared to how many defaults are "priced in" when the position is bought.

The market has been extremely wrong. Before 2023, most were predicting that leveraged loan defaults would rise to the 2.5-3% range. As CEO Tom Majewski noted in the earnings call:

During the fourth quarter, we saw only four leveraged loan defaults and that's down from six in the prior quarter. As of yearend, the trailing 12 month default rates stood at 1.53%, remaining well below the long term historic average of 2.7%. While some research desks believe the default rate will rise modestly in 2024, nearly all were completely wrong in 2023. And we believe that typical loan borrower has far more tools in its toolkit to manage their balance sheet than the average researcher gives credit to. While defaults may actually increase in 2024, we don't expect a spike and believe many forecasters will again miss the mark.

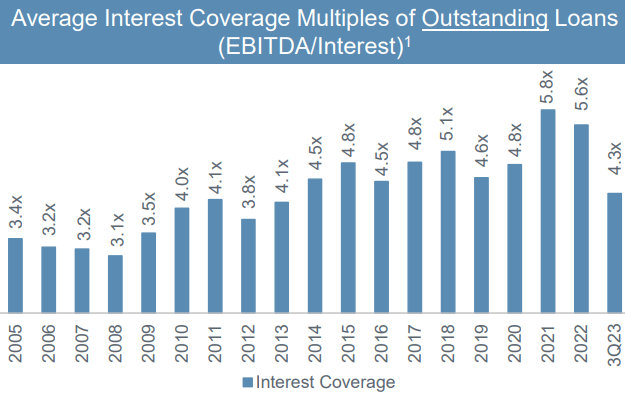

This is a topic I've been discussing for a few years. COVID-19 had a huge impact on a number of things in our economy. One of the big ones is that businesses are focused on improving their balance sheets. Faced with both the opportunity of historically low-interest rates and the uncertainty of how the pandemic might impact their businesses, everyone was forced to assess the strengths and weaknesses of their balance sheets.

As a result, balance sheets were excessively strong before the Fed started hiking. If we look at EBITDA/Interest coverage, we can see that it was well over 5x on average - which is just incredibly high. Naturally, when the Fed started increasing rates, that decreased coverage by increasing interest expense. Yet despite rising to the highest levels in 20+ years, coverage is still relatively strong.

ECC Q4 Investor Presentation

It fell a lot, but instead of falling to "Danger, Will Robinson, danger!" levels seen in the mid-2000s, it has declined to about the 2010-2019 average. Borrowers are feeling the squeeze relative to the days of plenty, but it's like being served a light meal the day after Thanksgiving. It's a lot less, but you aren't in danger of starving.

This puts CLO investments in a very attractive position because the prices of debt are lower thanks to the sheer force of the Fed's rapid hiking. Higher Treasury rates decrease the price of essentially all debt. Many loans are trading below par, which would typically happen during times of distress - when borrowers are defaulting and above-average losses are being absorbed. Yet borrowers are defaulting at a well-below-average pace. There is a mismatch between market perception and reality, and that is creating a great buying opportunity.

For 2024, we do expect that the pace of defaults might climb. And that could be a headwind to ECC's cash flow, though there is plenty of cushion to absorb it. On the other hand, on the liability side of CLO's balance sheets are the senior tranches and the spreads that the AAA tranches are trading at have been compressing as banks have been buying them up. With interest rates peaking, we are seeing a rotation back into the very safe but slightly higher-yielding alternatives to Treasuries, like agency MBS and AAA tranches of CLOs.

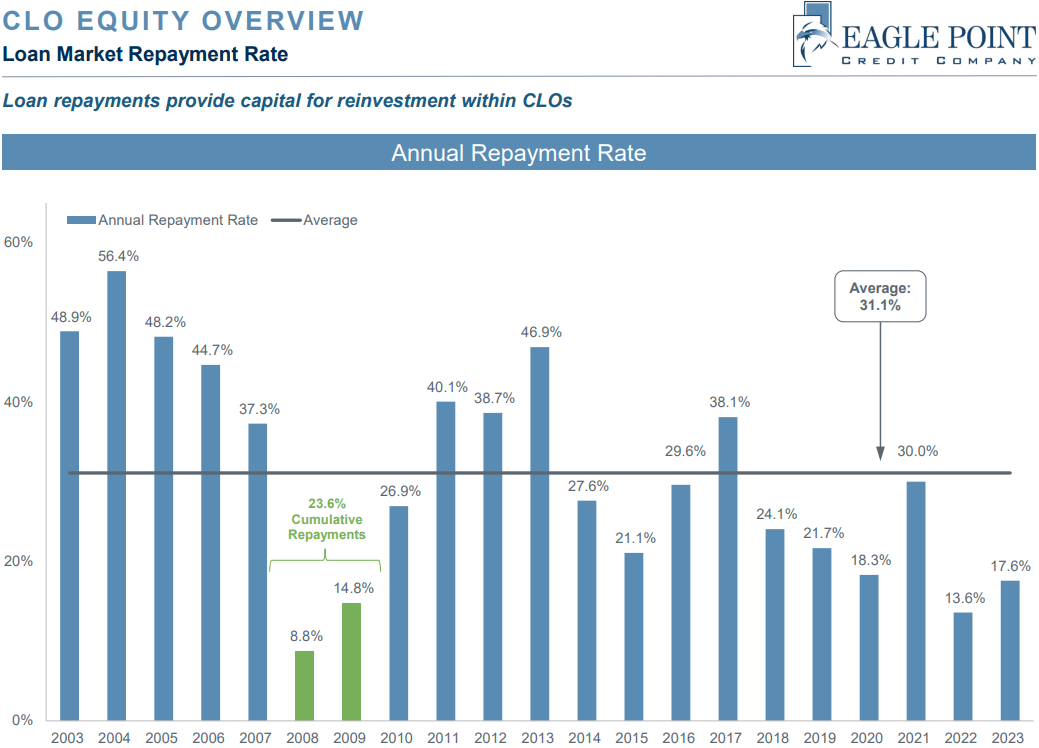

For the CLO equity positions that ECC owns, there are some opportunities to refinance the senior loan tranches, lowering the interest rate that the CLO pays and, therefore, increasing the amount that the equity profits. There are opportunities to "reset" where the entire debt structure (senior and junior) is refinanced and the CLO reinvestment period is extended. Also, there are opportunities for the CLOs to reinvest loans that are repaid at par into loans that are trading below par. This increases income and par value for the CLO equity. Prepayments picked up in Q4, as approximately 5% of loans were prepaid. In total, 17.6% of loans were repaid in 2023.

With interest rates stabilizing, more borrowers will be looking to refinance, and prepayment speeds, which have been low for so long, should pick up.

ECC Q4 Investor Presentation

With many loans still trading below par, this will be a source of increased par value and higher earnings for CLOs.

Overall, we expect that these tailwinds will outweigh any headwinds from rising default rates in 2024. ECC had a strong 2023, despite CLO equity prices staying low throughout the year and failing to rally. In 2024, CLO equity positions will see some headwinds from defaults, but we believe the various tailwinds will prove to be stronger.

Today we reviewed how 2023 went for ECC, and we saw that throughout the entire 12-month period its NAV has increased while still paying out a massive amount of income in 2023. 2023 was a good year for many debt investments, even though they remained at depressed pricing. Looking ahead, we expect 2024 to be as good as well.

The U.S. economy remains stubbornly strong as we look towards a recession coming in the future. High-interest rates continue to try to weigh down the U.S. economy, which seems to be powering through as we see inflation cooling. The goal of the Federal Reserve is to try to stabilize inflation and then stabilize the economy. An overheated economy is bad for many reasons. Likewise, an overly cooled economy is also bad for many reasons.

When it comes to your retirement, you should not have to worry about what the economy is doing, what commodity prices are doing, or what way the political winds are blowing today. What you should have to worry about is what you're going to do with your free time. Retirement is going to present you with a lot more free time than you had previously, and you will need to find things to fill up that time. Staying physically active and mentally stimulated is very important, but the last thing you need for your mental health is to fill up your time with anxiety and worries about what's going on with your portfolio every minute of every day. A professional income investor accepts that they cannot control the rest of the world, but that they can control how much income their portfolio produces and then use that income to enjoy hobbies or interests that are outside just the market itself. If you find yourself constantly fretting or worrying about what is going on in the world and things that are outside your control, it might be time to take a step back from your portfolio, reevaluate how you manage that portfolio, and see how you can free yourself from constant worry. The Income Method is a key that unlocks that and so much more.

That's the beauty of my Income Method. That's the beauty of income investing.