luismmolina

luismmolina

While recently looking at Ecopetrol (EC), I came across Parex Resources (OTCPK:PARXF), which has a similar investment case, excluding government ties. Parex is Colombia’s largest independent oil & gas company and has a great track record of rewarding its shareholders. Its share price currently hovers at the pre-pandemic level, while outstanding diluted shares have decreased 35% from 2018 levels. At the same time production is up 22%, and they've paid out $240M in dividends of their current $1.6B market cap.

Due to concerns surrounding Colombian president Gustavo Petro, the stock took significant hits. Additionally, a stronger Colombian peso, workovers, and the temporarily closure of an oil field caused Parex to slightly underperform its overly optimistic 2023 guidance. Given Parex's wonderful valuation at 1.96x EV/EBITDA and clean balance sheet, I consider it a Strong Buy. That is, if you can bear the inherent risks, such as geopolitical uncertainties, and the cyclicality of the oil sector.

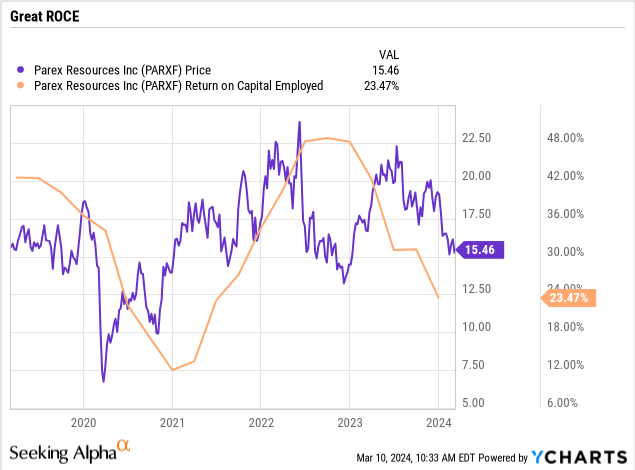

Parex Resources is an independent oil and gas exploration and production company, with 100% of its operations in Colombia. Parex is a stellar business with great capital allocation at a 23.5% ROCE and top EBITDA margins at 68% with Brent around $82/bbl in 2023. This was achieved despite disruptions amounting to ~5% of revenues across the year. They have a clean balance sheet with minimal debt, drawn from their credit facility to manage capital requirements at different times during 2024.

Note the drop in the middle of 2022 because of the Colombian elections.

Parex is planning for an annual production growth of at least 5% per year. This goal rises from their belief in the positive risk-reward of exploring new reserves in Colombia, an emerging market with plenty of unexplored regions. They plan to invest $375-450M of yearly capital expenditures over the next three years to reach this goal.

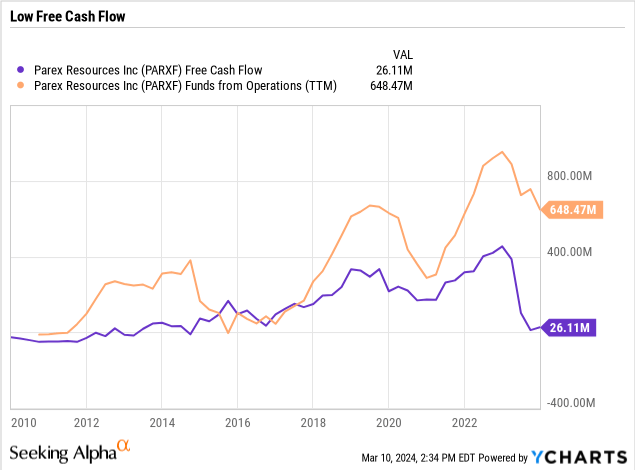

The stagnation around 2020 can be explained due to the covid crisis, which they took quite well, considering they kept their free cash flow positive during the entire period.

Historical Production Levels (Parex)

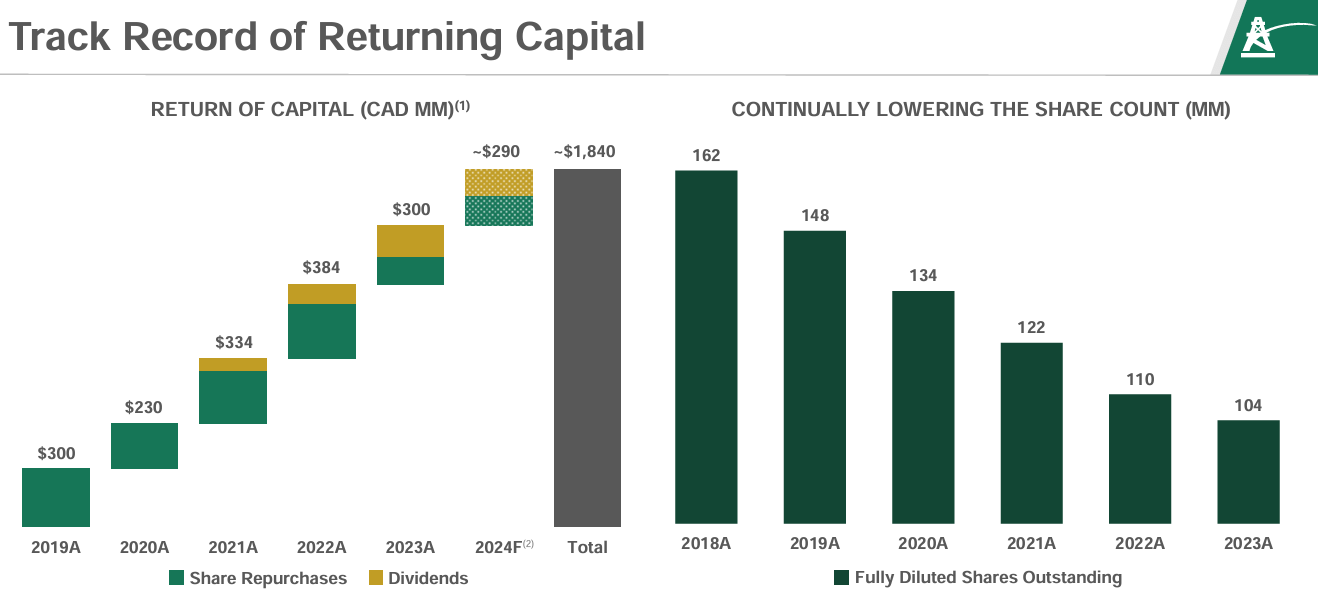

Being a high cash flow business, Parex has the ability to constantly reinvest for growth. They aim to reinvest ~2/3 of FFO (Free Funds from Operations), while the rest is returned to shareholders. They set a base dividend at $1.5 CAD per share annually (7.15% yield), but in the case of higher oil prices they will also buy back shares with the additional cash. Based on the low point of their 2024 guidance that would mean ~$200M returned to shareholders. However with lower share prices, more could get distributed through share repurchases.

Historically, Parex has been repurchasing around 7% of the shares outstanding per year. Considering Parex believes that the Common Shares have been trading in a price range which does not adequately reflect their value in relation to the Company's current operations and its growth prospects (Barron's), more buybacks are due in the future.

Returning Capital History (Parex)

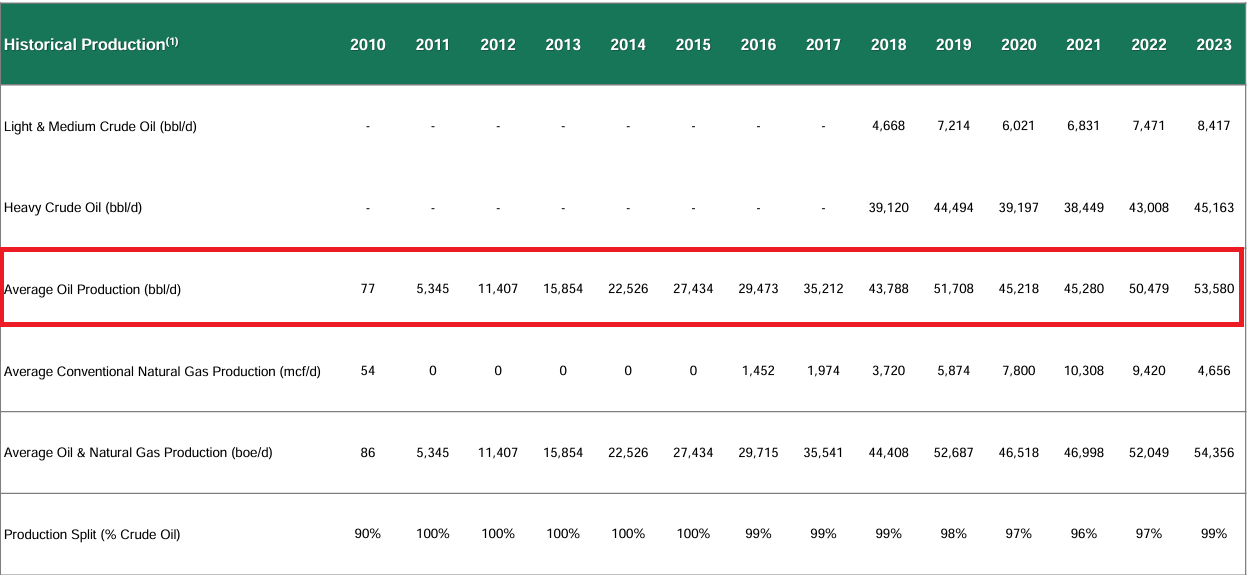

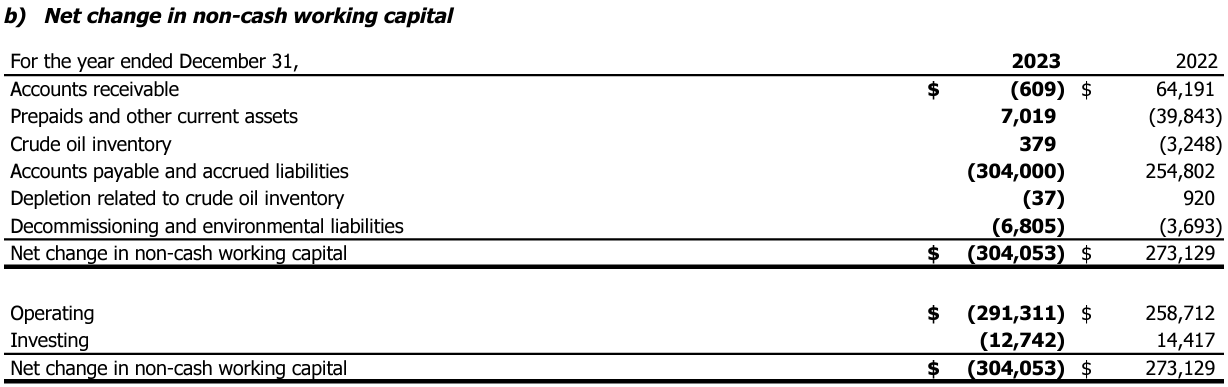

Despite their record production of 54,356 boe/d in 2023, they still only reached $184M cash flow (Parex). This has a few reasons:

Large Tax Payments in 2023 (Parex Annual Report) Net Change in Working Capital (Parex Annual Report)

3. They took on debt for the first time in history, which shouldn't be alarming. According to their earnings call:

The sale of a large export cargo in the fourth quarter and the timing difference between collecting cash on that cargo versus closing the quarter resulted in a $90 million draw on our credit facility that has been partially repaid.

However, FFO tells a less worrying story, in line with the decreasing oil prices. This almost record FFO was reached in a period with disruptions by protestors: Parex closes Colombian oil field due to protests, threats.

The shut-ins affected Parex’s Q1 2024 results. The lost net production of Capachos was approximately 5,000 boe/d for a few months. Parex has announced that it has resumed full operations at its Capachos and Arauca Blocks in the Northern Llanos. Historically, around every two years there's been a shut-in, making it recurring risk for Parex.

Colombia's electricity is generated by hydroelectric sources for 73.3% (Statista), making energy prices susceptible to large droughts. Operational costs peaked in 2023 because of the high electricity prices, partially caused by the El Niño phenomenon. This phenomenon causes warmer water to spread further, and stay closer to the surface, resulting in dry weather conditions (BBC News). Prices have seemingly stabilized and in the 2023 earnings call:

Power is still at a slightly elevated level but is not hitting the peaks that we saw last year.

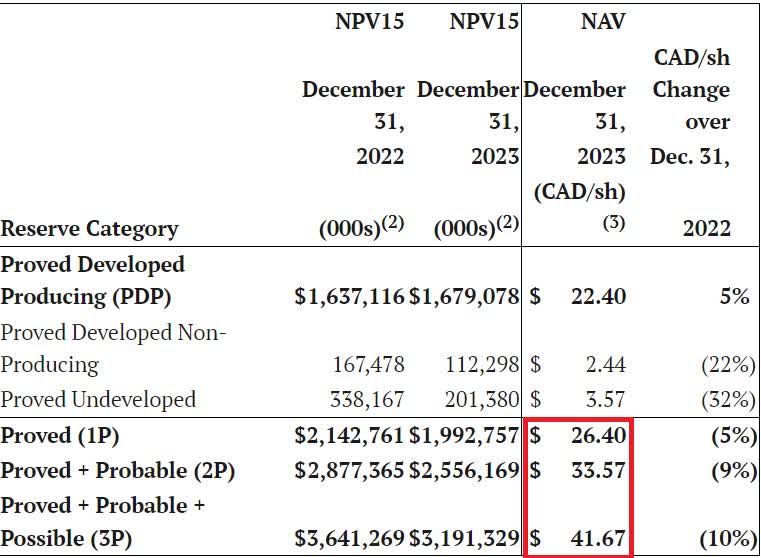

In 2023, Parex was able to replace ~100% of its PDP reserves. Here's an independent valuation by GLJ of their reserves. There's three valuations for three different reserve totals, all explained here according to Wikipedia:

The NAV is in CAD$ for the Canadian ticker (TSX:PXT:CA).Note that they used a 15% discount rate!

Reserves Net Present Value After Tax Summary – GLJ Brent Forecast (The Globe And Mail)

Their reserve volumes for 1P is at 112,500 Mboe and for 2P is at 168,500 which are down 14% and 16%, respectively, compared to 2022 (The Globe And Mail). However, I don't deem this worrying, as Parex's production reached record amounts in 4Q2023. Simultaneously, they have 5.4 million net acres position, which gives abundant opportunities to choose from.

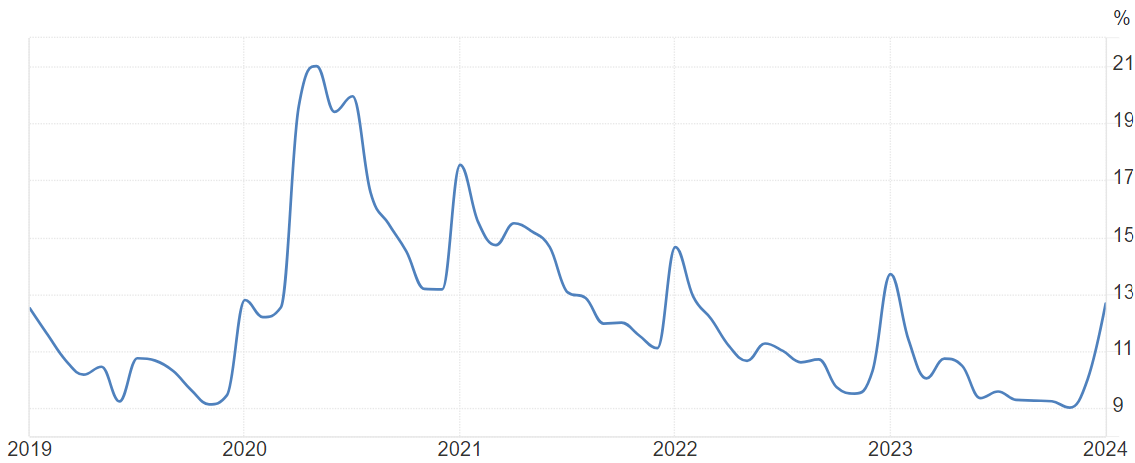

Colombia had a tough recovery after the pandemic with unemployment rates slowly recovering from its 21% pandemic high. I believe the markets fears of Gustavo Petro's big reforms should slowly fade away now, as his proposals are clear by now with all information made available. And as he's falling out of favor it's important to note that each president only gets one term in Colombia.

Colombian Unemployment Rate (Trading Economics)

Now what's left is we only need to assess how likely it is Gustavo Petro will take over the company must he centralize power, but let's first look at the reforms already in place. He introduced two major changes for the oil sector, lasting 4 years, the length of Petro's presidency.

The new law states that oil companies will be taxed an additional 5% when international prices are between $67.3 and $75 per barrel. That then becomes an additional 10% when prices are between $75 and $82.2 per barrel and then 15% if they climb any higher.

As I recently looked at Ecopetrol, they claimed the tax reforms didn't affect them that much. Additionally, Parex has entered a contract with Ecopetrol, through which they get to leverage their expertise in the Colombian foothills. From an investment perspective Parex has the advantage that it's just an E&P company, which doesn't have any additional responsibilities like Ecopetrol.

For 2024, Parex is currently assuming a 10% income surtax based on current commodity prices. Here's how different Brent prices would affect their FFO netback.

Tax Reform Effects (Parex)

What I’m proposing is not jumping into a void, as some denialist voices say,” he says. “Rather, it’s a change in the way forward. A way forward which, from my point of view, can be much more powerful, and prosperous, than the path that we would be leaving behind. (Gustavo Petro, on Time.)

As is usual in politics, presidential candidates' views get exaggerated as journalists selling fear reach the largest audiences. Instead of a destruction of all oil projects, Petro promotes gradual diversification to alternative sources of energy and agricultural growth to steer its economy away from relying on exhaustible resources. For perspective, in 2022, 26.7% of Colombia's exports consisted of crude petroleum.

These gradual reforms make more sense than the 'Marxist' label he often receives, as almost all oil dependent nations are trying to move away. Petro plans to partially replace this lost income by tourism, with his new branding campaign: “Colombia, the country of beauty” (Discurso). On July 20, 2023 Petro gave a speech before congress where he mentioned that he sees tourism as a more sustainable economy to develop and he hopes it will help replace dependency on oil (El Pais).

This indicates a strong headwind for oil as Colombia's own president is against its own core sector. But as we've seen in other countries like Saudi Arabia, this transition doesn't happen overnight. Besides, Parex's high ESG rating puts them more in favor of the government. They've been generously donating 1-2% of their capital yearly to give back to local communities (Parex).

Petro made the electoral promise in a public notary in Bogota, where he signed a document that said that “nothing or nobody will be expropriated” if he becomes president. -AP news

Gustavo Petro's relationship with the army is quite tense, as a former member of the guerrilla M19 group, that opposed the army. He has been actively exposing corruption and now has proposed significant reforms for the security forces. The military's reputation has been suffering from several corruption and human rights scandals in the past. This is highly relevant for the investment thesis as it highlights Petro's lack of power to overtake Colombia and its core sectors by force.

He's dealing with more core problems to Colombia, trying to resolve the long-lasting conflicts as he promised. Across Colombia, kidnappings have increased more than 80 per cent under Petro, extortion is up 27 per cent and the murder rate has barely fallen (Financial Times). Nearly 60 percent of Colombians think Petro’s Total Peace agenda is moving in the wrong direction. Now, Petro government officials and opposition leaders are calling on the president to change course (Council on Foreign Relations).

The military and police were already pretty terrified of a Petro government and now with Iván Velásquez as defence minister they’re likely to be even more so. -Jeremy McDermott, on AP news

This brings us to our next point, Petro isn't very liked in congress either, as many members in power were still elected during previous periods under right-wing leaders, opposed to Gustavo Petro. Adding to the oppositions' leverage, Petro's son is under investigation for alleged money laundering and illicit enrichment (Reuters). This again indicates Petro's lack of control over the country as he has to deal with strong opposition (NPR).

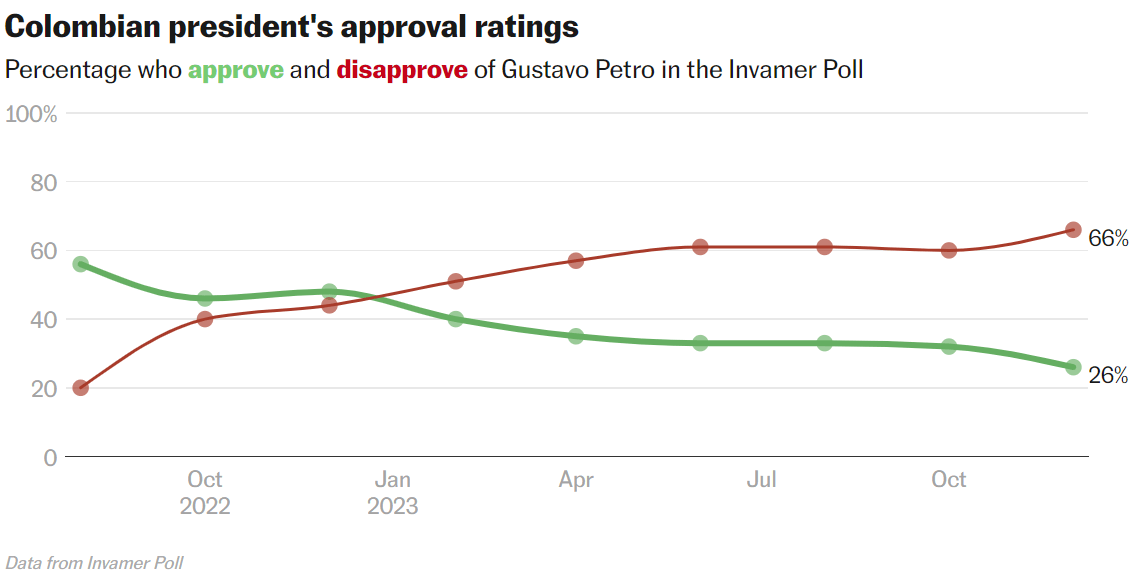

Gustavo Petro won the run-off with a slight 51% and by now his approval rating has dropped to 26% (El Pais), as it harder to turn the troubled country around than he promised. This also makes it more likely the next election will once again be won by a central/right-win politician in favor of oil, yet the investment thesis doesn't solely depend on this.

He’s moved on to a phase of his presidency where he’ll likely focus more on symbolic gestures and on issues he can control unilaterally, instead of big legislative reforms. -Will Freeman, on AP news

Gustavo Petro Approval Rating. (El Pais)

I won't restate my entire oil thesis, but here are what I believe to be some driving factors which will push oil higher in the long run.

Oil Demand in India by Sector. (OPEC)

With oil at relatively normal prices, EBITDA totaled $813M at a 1.98x EV/EBITDA ratio. This should make it immediately clear the stock is trading at an incredibly low valuation. Looking at the reserves, discounted at 15%, we get a 2P valuation of $24.89 USD per share. Add the working capital surplus of $79 million, which adds another $0.75 value for the American shares. This leaves 65% of upwards potential at $25.64 USD, excluding the 5% growth.

Parex expects to reach a cumulative Free cash flow of approximately $850 million over the next three years. As mentioned earlier, the current free cash flow isn't a good metric to show the sheer value in the stock. With the large capital expenditures projected forward, free cash flow is bound to be lower than its potential. For the 2024 plan at $75/bbl Brent is expected to generate ~$215MM of free cash flow, while FFO is projected to $625M. With a 2.38 P/FFO in 2023, even without additional output the stock pays itself back in less than 3 years.

2024 Guidance (Parex)

The investment thesis for Parex doesn't need oil to increase, as guidance projections are made for Brent crude at $75/bbl. The oil sector is always bound to deal with some headwinds like regulations, social unrest, workover, and increasing operational costs. I believe that temporary geopolitical uncertainties make for a great entry point in the stock and that the cheap valuation accounts for a great margin of safety for operating in such a volatile environment. However, one should always be aware of the significant risks of owning such a stock.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.