VioletaStoimenova

VioletaStoimenova

DXC Technology (NYSE:DXC) has suffered from declining revenue from its infrastructure segment and delayed client engagement activity, although these delays are being felt across the consulting industry in the wake of the pandemic's end.

I previously wrote about DXC in December 2023 with a Hold outlook on 'lumpy' bookings amid a soft discretionary project environment.

Leadership is seeking to manage a transition of greater focus on its GBS segment while trying to retain and retrain talent to take advantage of the future potential of AI and other business transformation consulting opportunities.

I remain Neutral [Hold] on DXC in the near term during a down period in client spending.

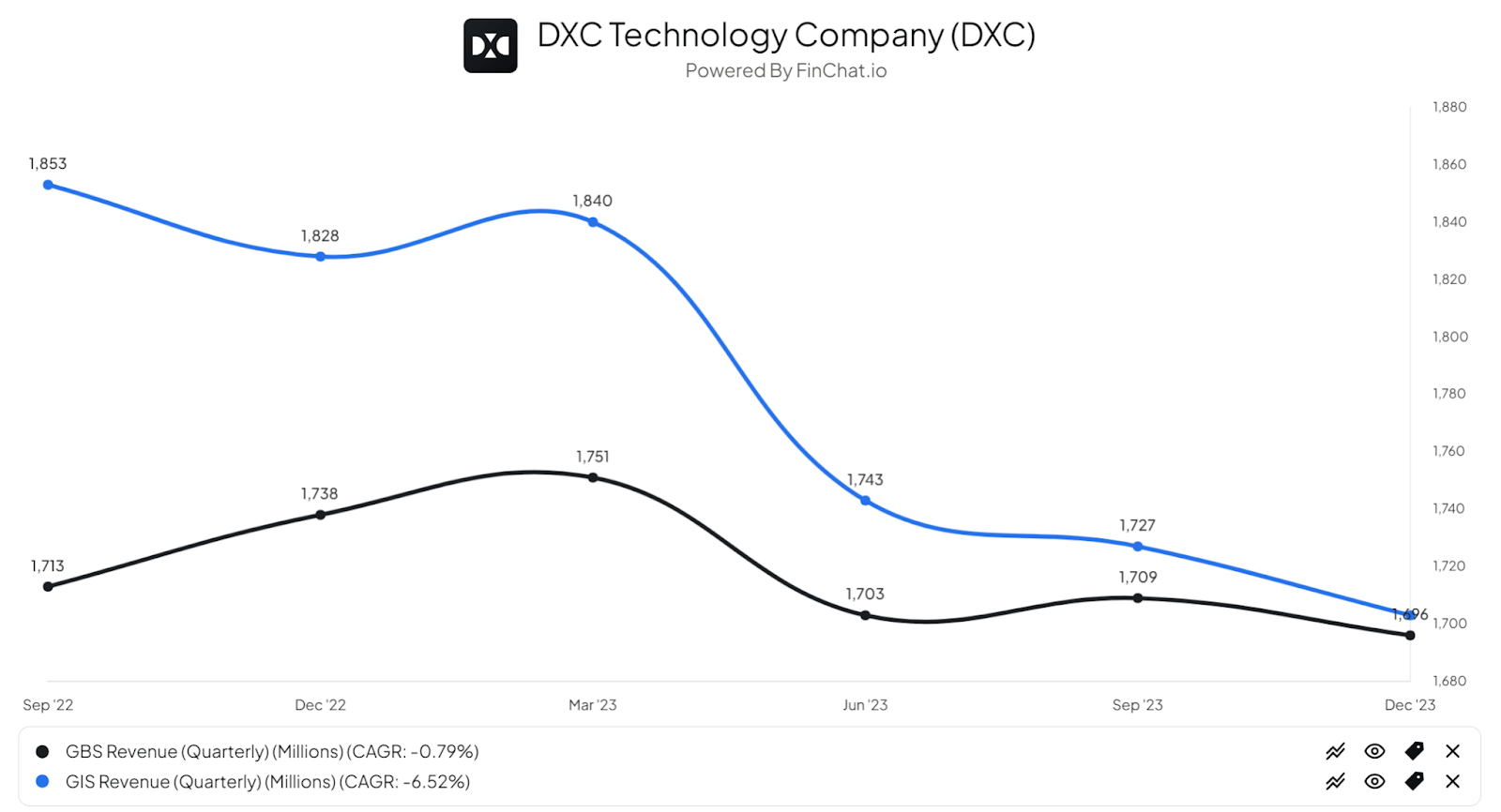

DXC generates revenue from two business segments, its GBS (Global Business Services) and GIS (Global Infrastructure Services).

Management has been transitioning its focus to the GBS segment as the GIS segment is a more challenged area for the firm to outperform.

By focusing on the GBS segment, the company is reducing its capital expenditure profile while improving its margin results over time as it sells underutilized assets.

As a result, DXC has produced declining revenue for the GIS segment (Blue line) as shown in the chart below:

FinChat.io

GBS revenue(Black line) has produced a slight decline on a CAGR basis in the past six quarters with most of that decline between Q1 and Q2 of 2023.

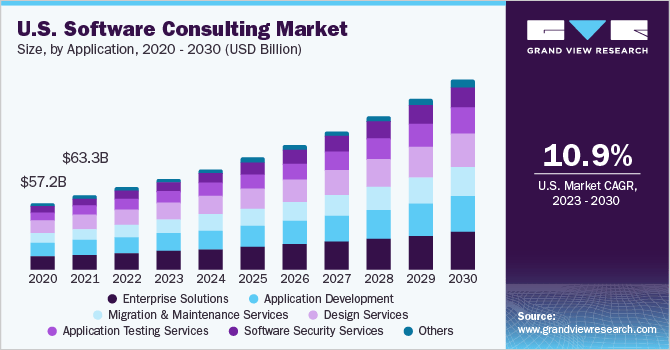

The overall market for software consulting services (part of the company's service offering suite) according to 2023 market research report by Grand View Research was forecasted to reach $681 billion by 2030.

If achieved, this would produce a compound annual growth rate of 12.1% through 2030.

The primary reasons for this forecasted growth are the ongoing movement of IT operations from legacy, on-premises modes to the cloud and the need for businesses to compete for customers through their IPO operations while producing efficiency gains and growing profits.

The chart here illustrates estimated growth trajectory from 2020 to 2030 of the U.S. software consulting market by application type:

Grand View Research

The company is also active in other in other regions, including Europe, Asia and Latin America.

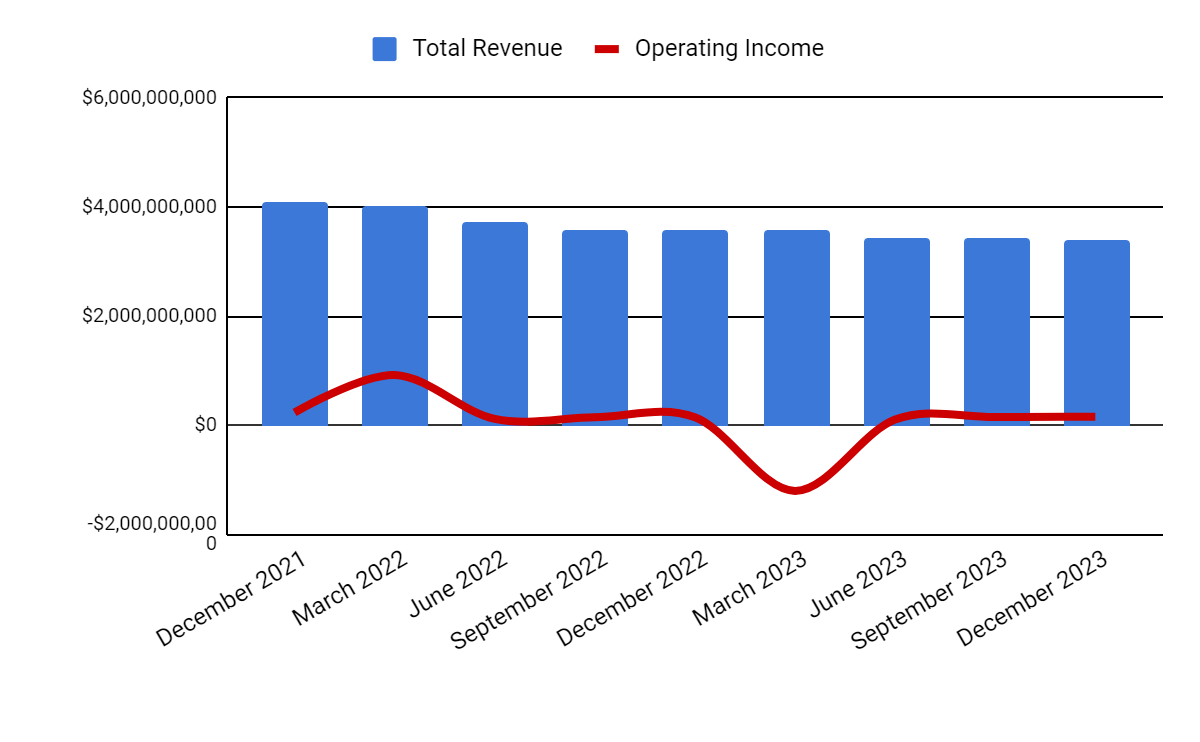

Total revenue by quarter (columns) has continued to decline primarily due to reduced GIS (Infrastructure) segment activity; Operating income by quarter (line) has increased 5.4% year-over-year due to slightly improved gross profit margin.

Seeking Alpha

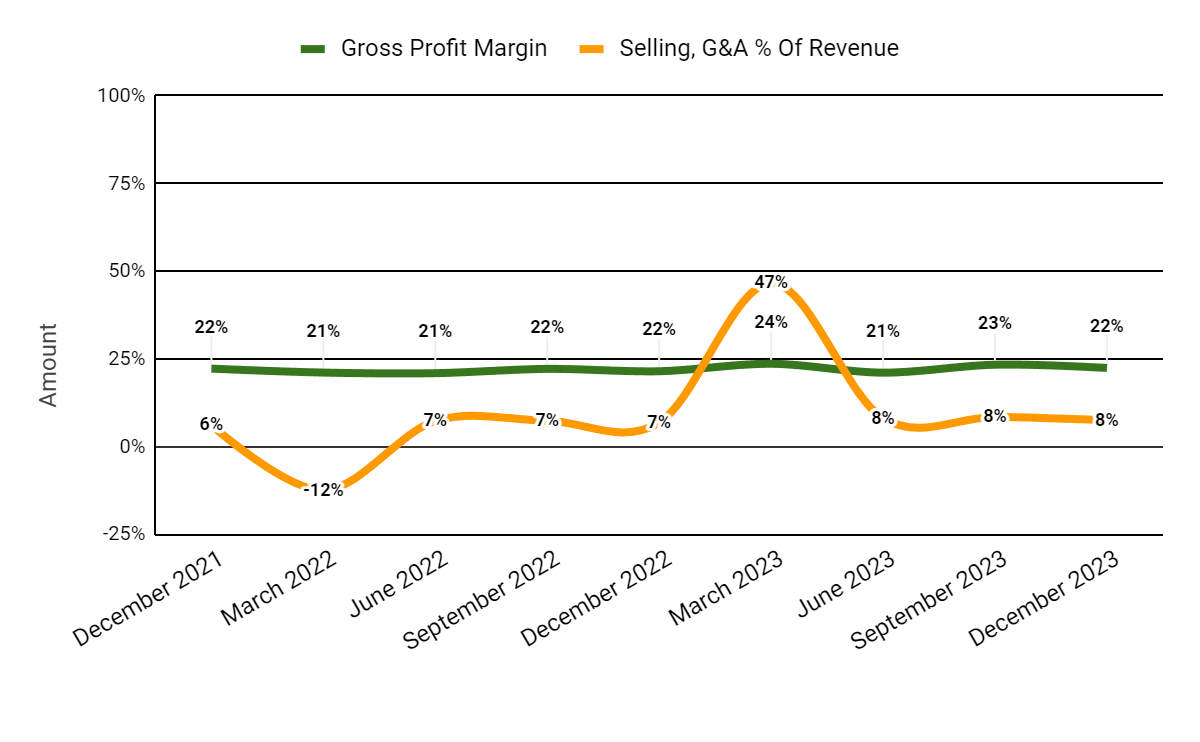

Gross profit margin by quarter (green line) has been slightly higher despite lower GIS segment activity and due to ongoing cost reductions; Selling and G&A expenses as a percentage of total revenue by quarter (orange line) have remained elevated at 8% compared to 7% during 2022.

Seeking Alpha

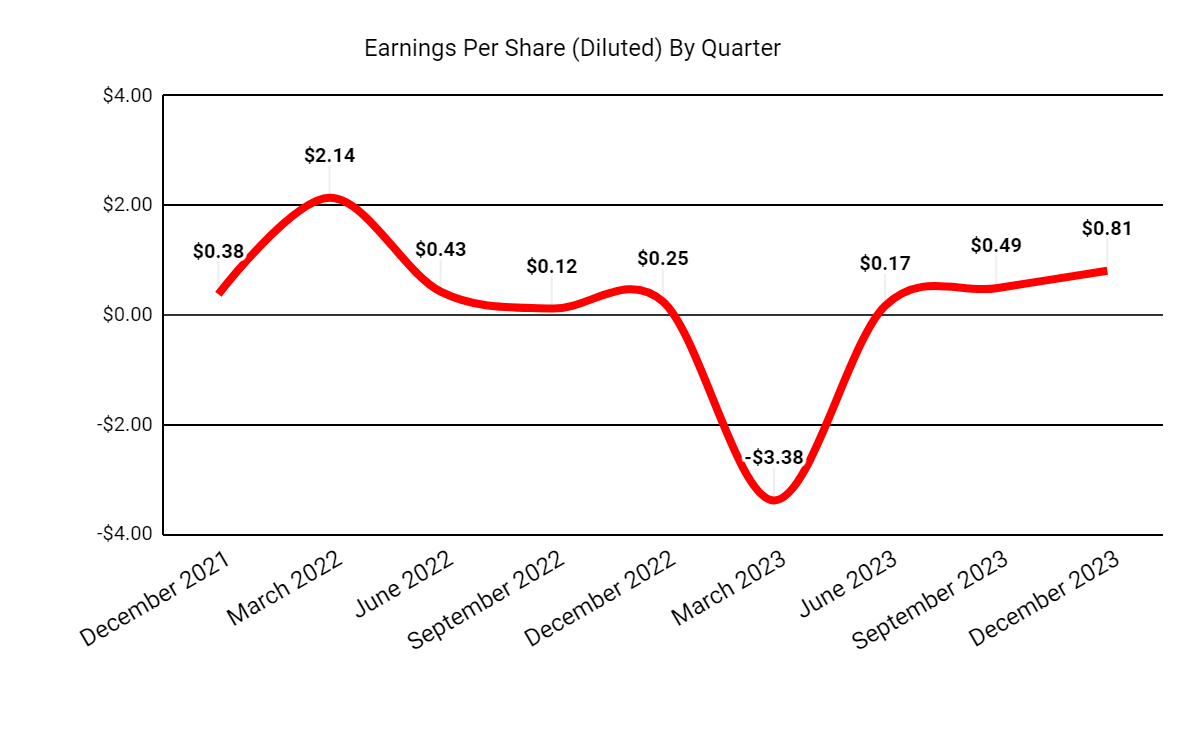

Earnings per share (Diluted) have improved in recent quarters in part due to continued share repurchases.

Seeking Alpha

(All data in the above charts is GAAP.)

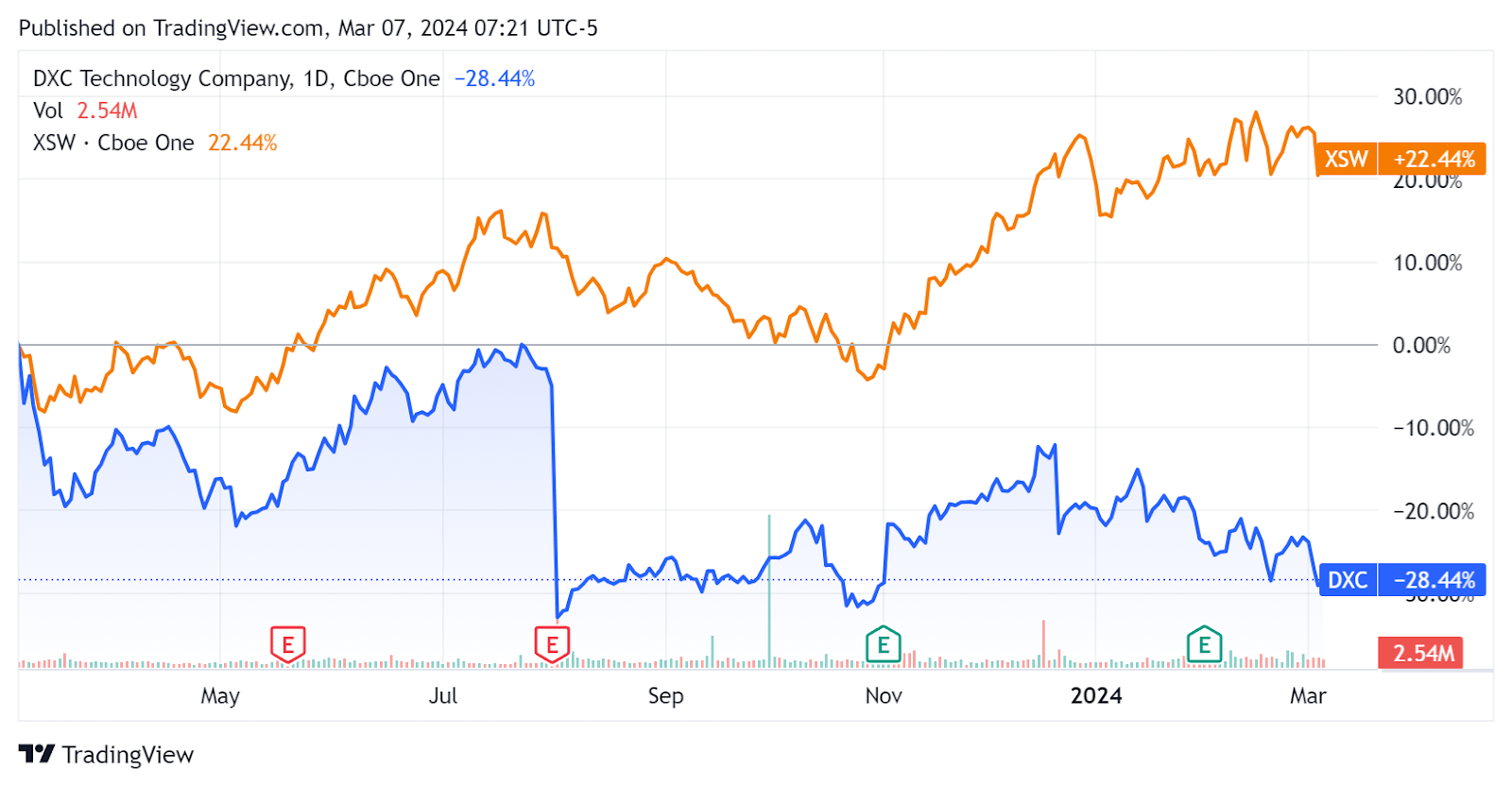

Compared to the 12-month SPDR S&P Software & Services ETF's (XSW) gain of 22.4%, DXC's stock price has fallen by 28.4%, as the chart shows here:

Seeking Alpha

Below is a major metrics table I've prepared from the company's most recent figures and performance:

Metric | Amount |

EV/Sales ("FWD") | 0.6 |

EV/EBITDA ("FWD") | 3.8 |

Price/Sales ("TTM") | 0.3 |

Revenue Growth ("YoY") | -6.6% |

Net Income Margin | -3.4% |

EBITDA Margin | 3.4% |

Market Capitalization | $3,690,000,000 |

Enterprise Value | $7,640,000,000 |

Operating Cash Flow | $1,500,000,000 |

Earnings Per Share (Fully Diluted) | -$1.91 |

2024 FWD EPS Estimate | $3.02 |

Rev. Growth Estimate ("FWD") | -4.3% |

Free Cash Flow/Share ("TTM") | $5.26 |

Seeking Alpha Quant Score | Hold - 2.60 |

(Source: Seeking Alpha)

Consulting companies have been having a difficult time after the waning of the pandemic.

With the sharp rise in interest rates, many stocks have been hard hit, causing managements to focus more on profitability and reducing discretionary spending.

Digital transformation projects have been put on the chopping block, unless they are focused on quick cost-takeout initiatives that can reduce expenses in the short term.

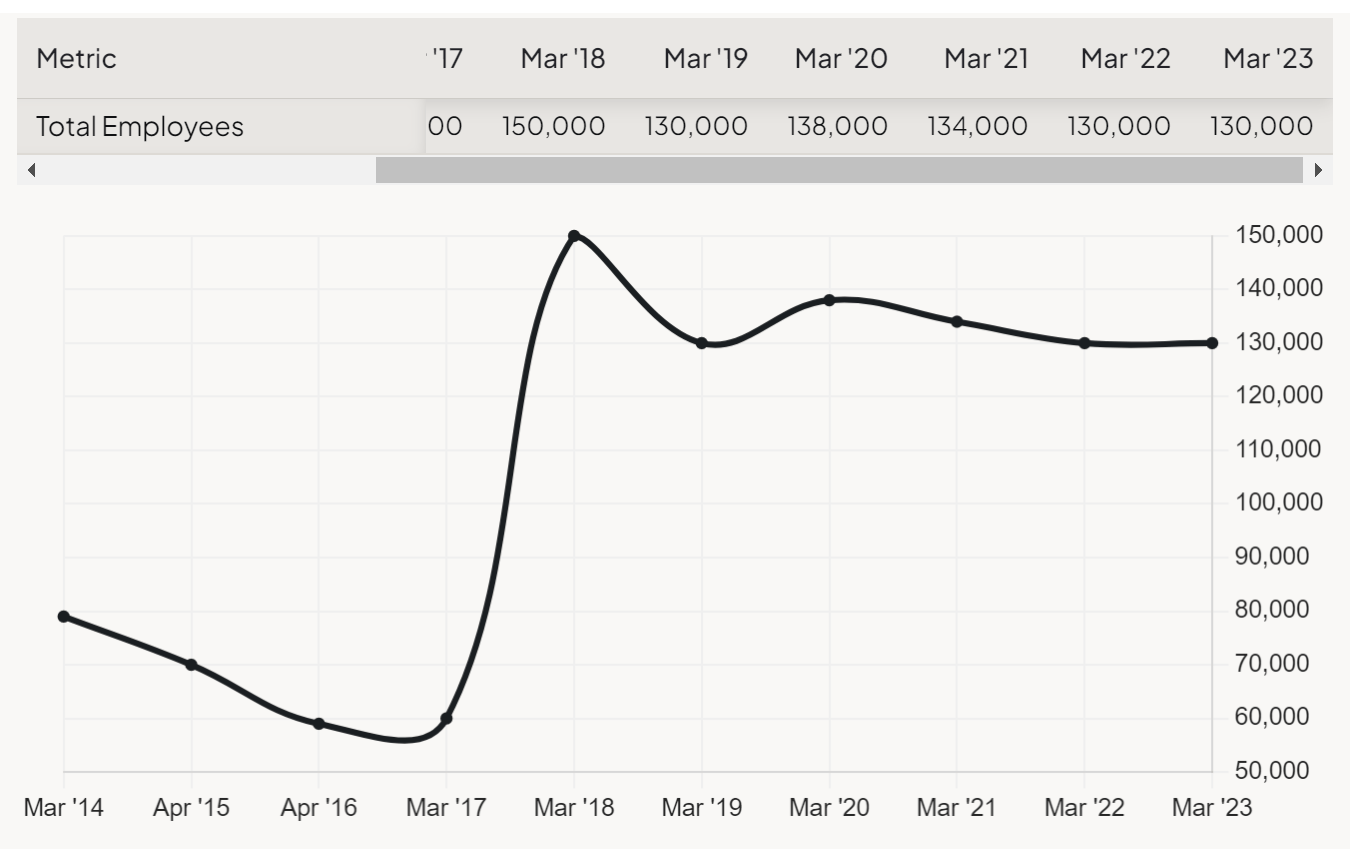

That has left companies like DXC with high headcount and challenged employee utilization rates.

The firm's headcount grew sharply before the pandemic, but has fallen slightly each year during and since, plateauing in 2023 at 130,000, shown here in this chart:

FinChat.io

The firm continues to repurchase its shares and expects to achieve $1 billion in fiscal 2024 through a combination of free cash flow and asset sales, so that figure may not continue if asset sales drop.

Looking ahead, management reduced its forward revenue guidance to negative 4.4% at the midpoint of the range.

If achieved, this 4.4% decline for fiscal 2024 would produce slightly improved revenue decline from a drop of 11.3% during fiscal 2023.

This is cold comfort as the company is still experiencing client delays on discretionary, 'transformation' projects despite improved bookings so far in the second half of DXC's fiscal year.

Debt levels have remained stable at around $4.5 billion, but interest expense has risen, hurting otherwise stable earnings results.

Management has a similar problem to many other consulting companies, that of managing declining revenue while seeking to retain talent and scale in a hoped-for recovery in client spending.

While AI engagements have shown promise for many consultancies, so far they have produced only 'pilot' programs and haven't really ramped up as a meaningful revenue source.

As a result, some of the more forward-looking consulting firms have spent this time training their workforces on the latest AI capabilities and seeking to develop some practice expertise to be able to offer their clients.

The AI field is currently nascent and fast-moving, with new capabilities being offered by AI technology providers on an almost monthly basis.

So, the potential for consulting companies to help clients manage their transition to greater use of these powerful tools is significant, but will require patience from investors during this period of soft client demand.

As a result, I remain Neutral [Hold] on DXC for the near term and look to signs of stronger client demand perhaps in the second half of 2024.