phive2015

phive2015

ETF assets under management have compounded at a 15% compound annual growth rate in 2010. According to Oliver Wyman, this is 3x faster than the growth of traditional mutual funds. At first ETFs were mostly associated with passive investment strategies. That's no longer necessarily the case, and there is an increasing amount of active strategies that are available through ETFs and ETNs. Lately, I'm fascinated by the leveraged and volatility-related products that are coming to the market. Some good, some bad. It is especially interesting to me what market impact they are potentially having or could have in the future (on further growth).

To understand this better, it helps to understand the products. I've found a number of surprising products recently, like leveraged ETFs on volatile single stocks like Coinbase Global, Inc. (COIN) and Tesla, Inc. (TSLA). Today, I came across an ETN, called the MAX S&P 500 4X Leveraged ETN (NYSEARCA:XXXX), that is leveraging the S&P 500 (SP500) by, you guessed it, 4x.

This can be a useful product for some investors, but it is important to understand some of its specific characteristics because a buy & hold strategy will be highly likely to lead to disappointing returns.

In addition, exchange-traded notes, or ETNs, are also senior unsecured debt obligations and introduce a secondary risk in terms of the issuer's creditworthiness. This ETN is given out by Bank of Montreal (BMO).

The credit risk doesn't seem to be very high given that 4.8% perpetuals trade above 96 cents on the dollar.

BMO perpetual price (Boerse Frankfurt)

It is something to keep in mind when we're entering a financial crisis. Getting access to leverage could suddenly look a lot less appealing.

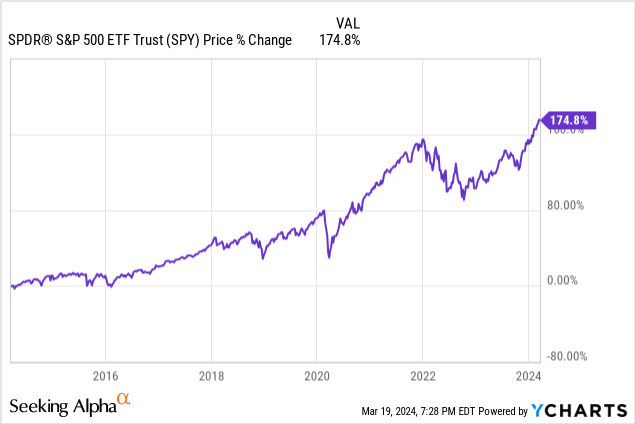

Investors are likely attracted to this ETF because the prospect of 4x exposure to one of the best-performing indexes over the last decade is enticing. The S&P 500 has been an unstoppable force.

I can definitely see the appeal.

The fund charges a daily fee that's like charging ~0.95% on an annualized basis.

That's quite high for what's essentially a passive investment on steroids. However, the fund is able to get its leverage. I expected this rate to be relatively attractive making up for the fee level. However, according to the prospectus, the fund is borrowing at the Fed's Bank Loan Prime Rate. To this, they add a financing spread of 2%. That's currently 8.5% + 2% = 10.5%.

There are other challenges to holding an ETF like this. Looking at the website and the materials provided, I have to give props to the Bank of Montreal. I have not come across a leveraged ETF product that spells out the important risks (especially path dependency) so clearly and prominently. The materials straight-up warn investors that buying & holding this product is not how this product should be utilized.

A key problem with these ETFs is that they up leverage after a positive day (to maintain 4x exposure) and decrease leverage at the end of a negative day (to maintain 4x exposure). Interest costs also play a part but the effect of this "volatility tax" can be very significant. Or as the issuer puts it in the prospectus:

It is possible that you will suffer significant losses in the 4x ETNs even if the long-term performance of the Index is positive (before taking into account the negative effect of the Daily Investor Fee and the Daily Financing Charge, and the Redemption Fee Amount, if applicable).

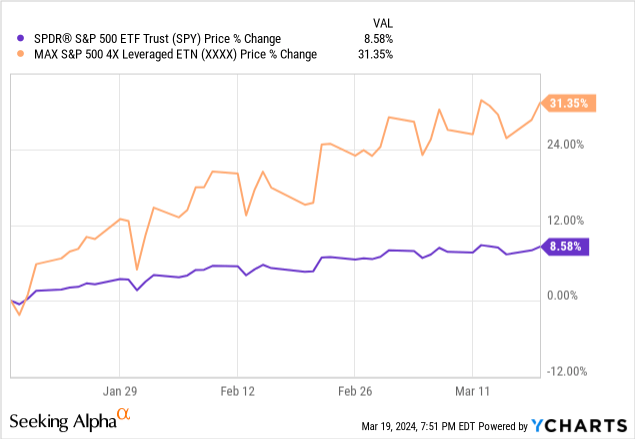

Things have been very calm with very little volatility since inception of the fund. I think it is not unfair to call these ideal circumstances.

Yet the fund didn't 4x the S&P 500. It falls ~2.5% short of that within a timeframe of 4 months. And I couldn't have drawn up a S&P 500 graph that is more conducive to a leveraged ETF like this.

What really hurts returns are choppy markets. One day up, one day down. Especially, if the moves are fairly large. This is easy to see with extreme examples.

Let's say the S&P 500 falls 12.5%. The ETN is 4x leveraged so it would fall 50%. Then the next day the S&P 500 rebounds 14.3% (that would get it back to the same level as the day before. However, the leveraged ETF would only bounce back to 78% of its prior level. In a flat market a buy & hold investor would have lost 22%.

The effect is very strong in our extreme example and that's also why high volatility is very detrimental. A downwards direction is obviously not conducive to a leveraged long investment but a flat trajectory or an upwards trajectory with lots of 2% up days and 2% down days will also be a very challenging environment.

The issuer is actually very blunt about the importance of this effect (emphasis mine):

As a result of this decay effect, it is extremely likely that the value of the notes will decline to near zero (absent reverse splits) by the Maturity Date, and likely significantly sooner. Accordingly, the notes are not suitable for intermediate- or long-term investment, as any intermediate or long-term investment is very likely to sustain significant losses, even if the Index increases over the relevant time period. Although the decay effect is more likely to manifest itself the longer the notes are held, the decay effect can have a significant impact on the performance of the notes, even over a period as short as two days

Another problem these types of products sometimes have is that they follow the index but do not pass on the dividends on the underlying. In this case, the ETN doesn't pass the dividends on either. However, it has picked an S&P 500 variant index that adds the paid dividends by the constituents to the level of the index.

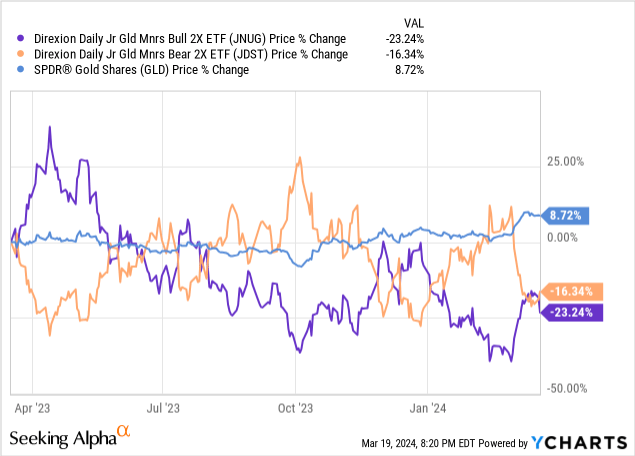

How bad this tends to turn out is evident if you look at leveraged volatile ETFs. Favorites of mine are the leveraged Direxion Daily Junior Gold Miners Index Bull 2X Shares ETF (JNUG) and the Direxion Daily Gold Miners Index Bear 2X Shares ETF (DUST). You would think these are inverse products. Over one day they actually produce inverse results. Over the past year, both ETFs are down 15%+ while gold is actually up 8%:

If this is such a dangerous product, then why does it exist? Well, it is possible to do well with an ETN like this. It works best for short-term traders who have an idea of how the S&P total return index will behave over the next few days. A number of up days in a row without down days in between leads to very strong performance. The ETF will leverage up further each day and you don't suffer the volatility drain that occurs when investing over a period with up and down days.

In sum, bull markets draw investors to leverage. It depends on traders and investors ability to generate returns and expectations whether that's right for them or not. I'm not sure getting leverage through a product like this is the most efficient way. It looks quite expensive.

However, the issuer, Bank of Montreal, is very transparent and puts the disadvantages of these products front and center in its communications. Leveraging the S&P 500 by four times may seem appealing, especially given its historical performance, but as illustrated above, the reality of achieving quadruple the index's return is far from straightforward. I'd stay away from this product unless I was a short-term index trader knowing exactly what I was doing. Even then, I imagine I'd prefer to trade futures. For anyone but a short-term to medium-term speculator, this seems like a clear sell to me.