Arvydas Lakacauskas/iStock via Getty Images

Arvydas Lakacauskas/iStock via Getty Images

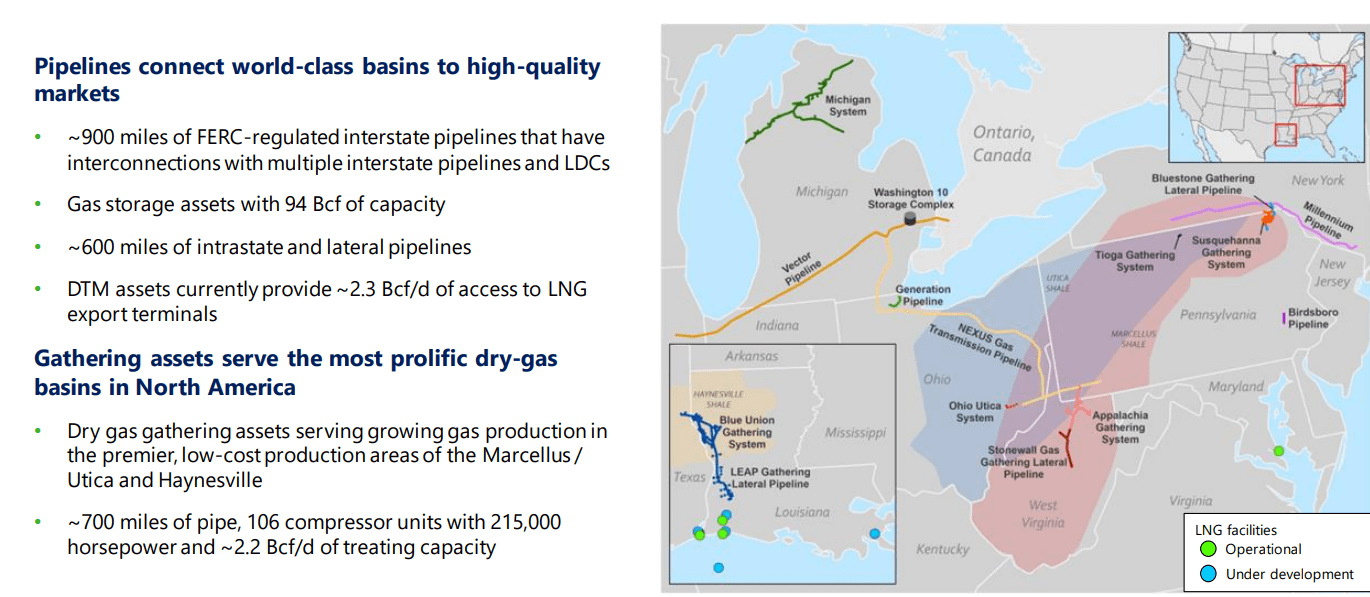

DT Midstream (NYSE:DTM) will publish its full-year results on Friday, February 16, before the open, but I didn’t want to wait for those results to check in on this midstream company. DT Midstream was spun off from DT Energy (DTE) and focuses on natural gas pipelines and storage assets.

DTM Investor Relations

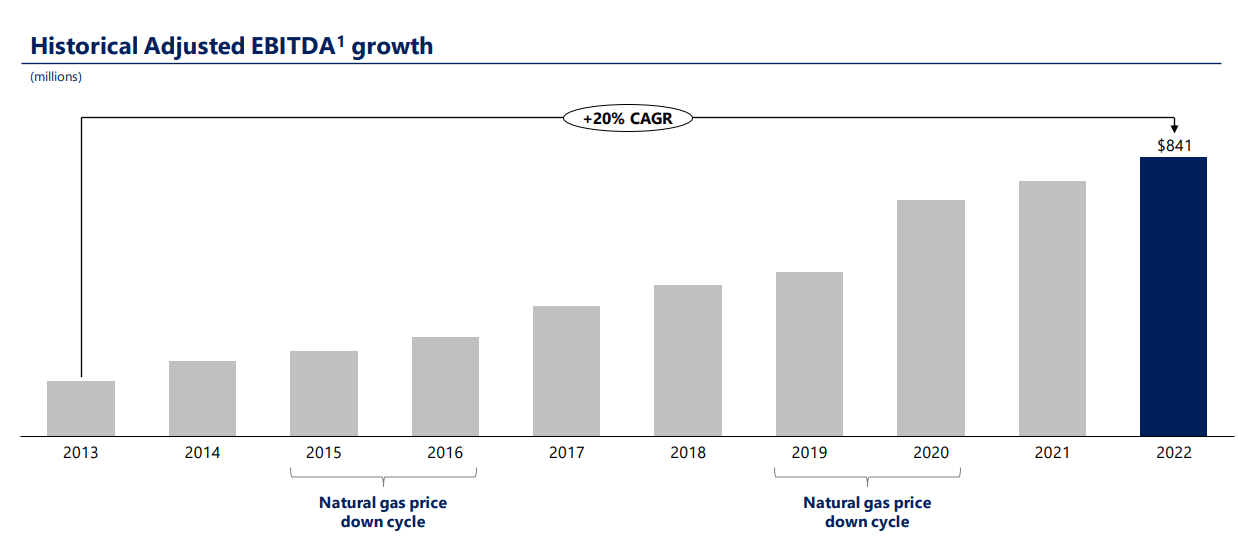

Although the natural gas price is definitely in a downcycle, DT Midstream doesn’t appear to be too worried, as it highlighted its historical EBITDA performance during downcycles. Indeed, the company continued to grow its EBITDA even during weaker times, and its initial guidance for 2024 suggests we can expect more growth, albeit at a much slower rate.

DTM Investor Relations

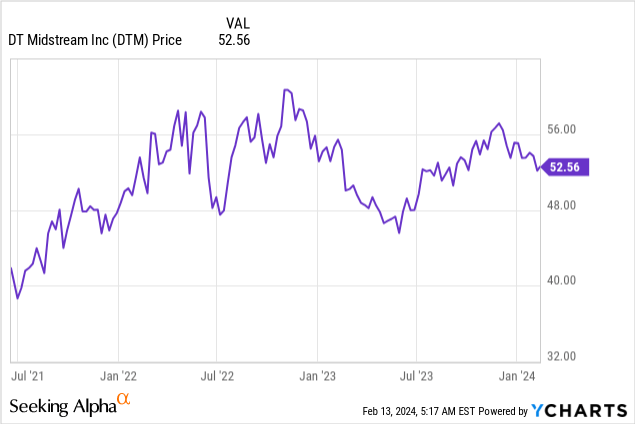

Although DT Midstream’s performance throughout 2023 was pretty strong, its share price came down by approximately 10% since its peak in the fourth quarter of last year.

There are likely two contributing factors to the relatively poor share price performance: although the company has been able to perform well during the past few natural gas crises, there’s no guarantee it will continue to limit the damage. And secondly, as interest rates on the financial markets aren’t going down fast enough, investors may be reducing their exposure to midstream companies.

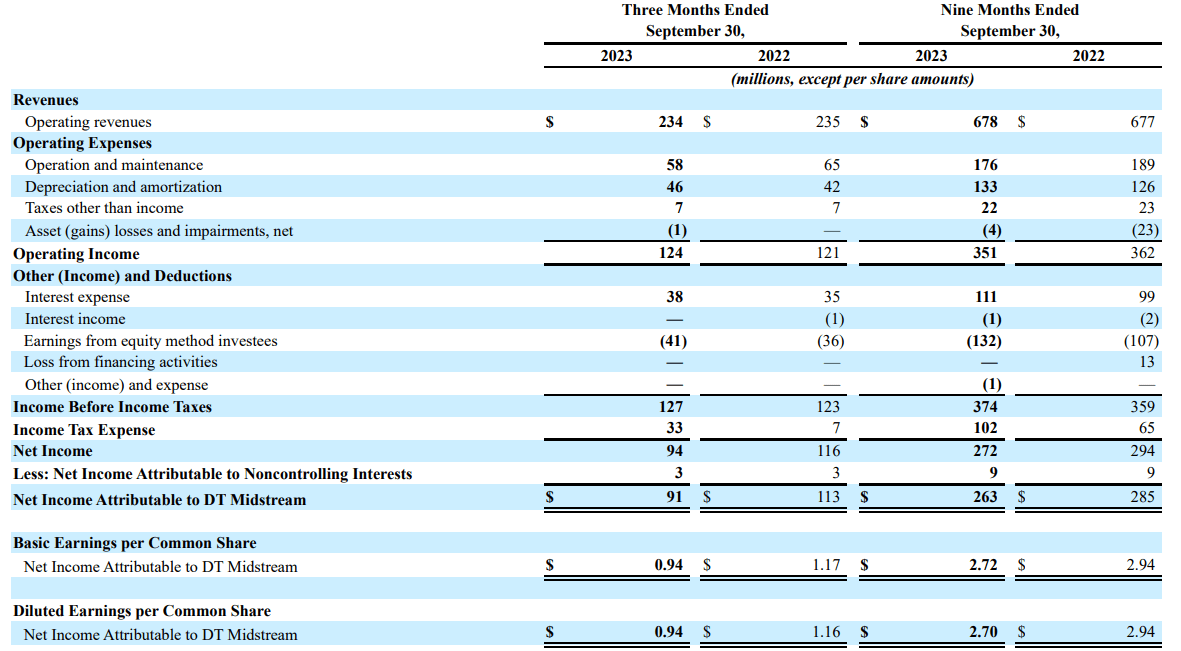

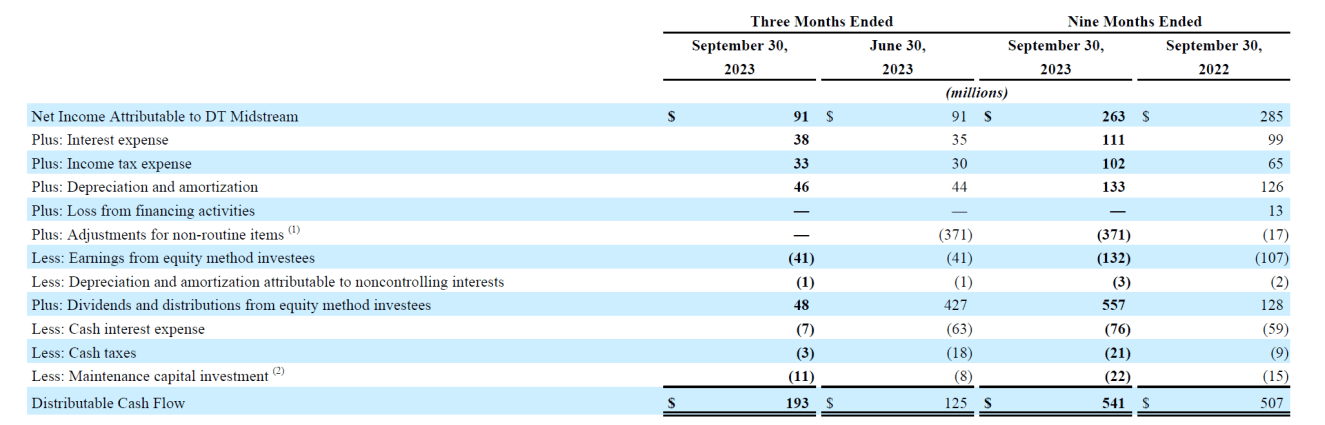

During the third quarter of 2023, DT Midstream reported a total revenue of $234M, resulting in an operating income of $124M after deducting the operating expenses and the $46M in depreciation and amortization expenses. The company also paid about $38M in interest expenses but also earned $41M from equity method investees, resulting in a pre-tax income of $127M and a net profit of $94M of which $91M was attributable to the common shareholders of DT Midstream.

DTM Investor Relations

As you can see above, that worked out to an EPS of $0.94, bringing the 9M 2023 EPS to $2.72. A very decent result, but you can’t look at reported earnings to figure out how attractive a midstream company is. The distributable cash flow is a more important metric as it takes into consideration the assets that are being depreciated are mainly a sunk cost and the maintenance capex is just a fraction of the depreciation and amortization expenses.

As you can see below, the distributable cash flow during the third quarter was actually $193M, mainly thanks to a very low cash tax payment.

DTM Investor Relations

Divided over the 97M shares outstanding, the Q3 DCF was $1.99 per share while the DCF in the first nine months of the year exceeded $5.50 per share.

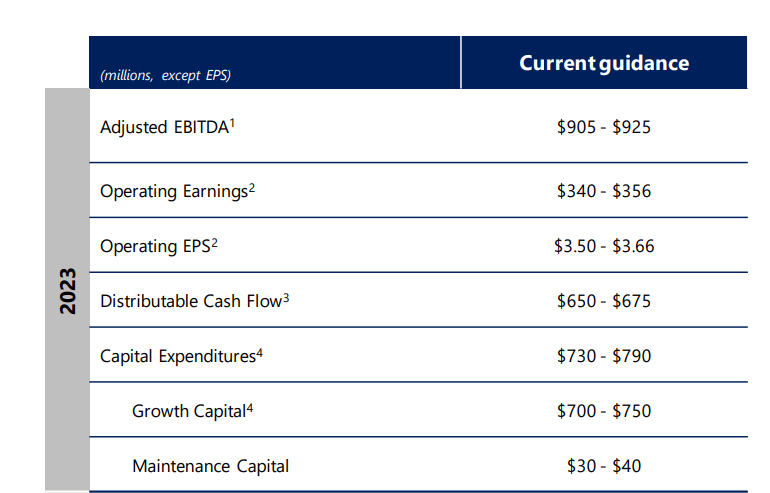

The company recently also confirmed its full-year outlook. As you can see below, it expects to generate $905-$925M in adjusted EBITDA which should result in a total distributable cash flow of $650-$675M. The lower end of that equation indicates a full-year DCFPS of approximately $6.70.

DTM Investor Relations

Meanwhile, the company continues to invest, as it has earmarked $700-$750M for growth investments. Some of those investments have now already been completed and will likely start to contribute to the global result in 2024.

DTM Investor Relations

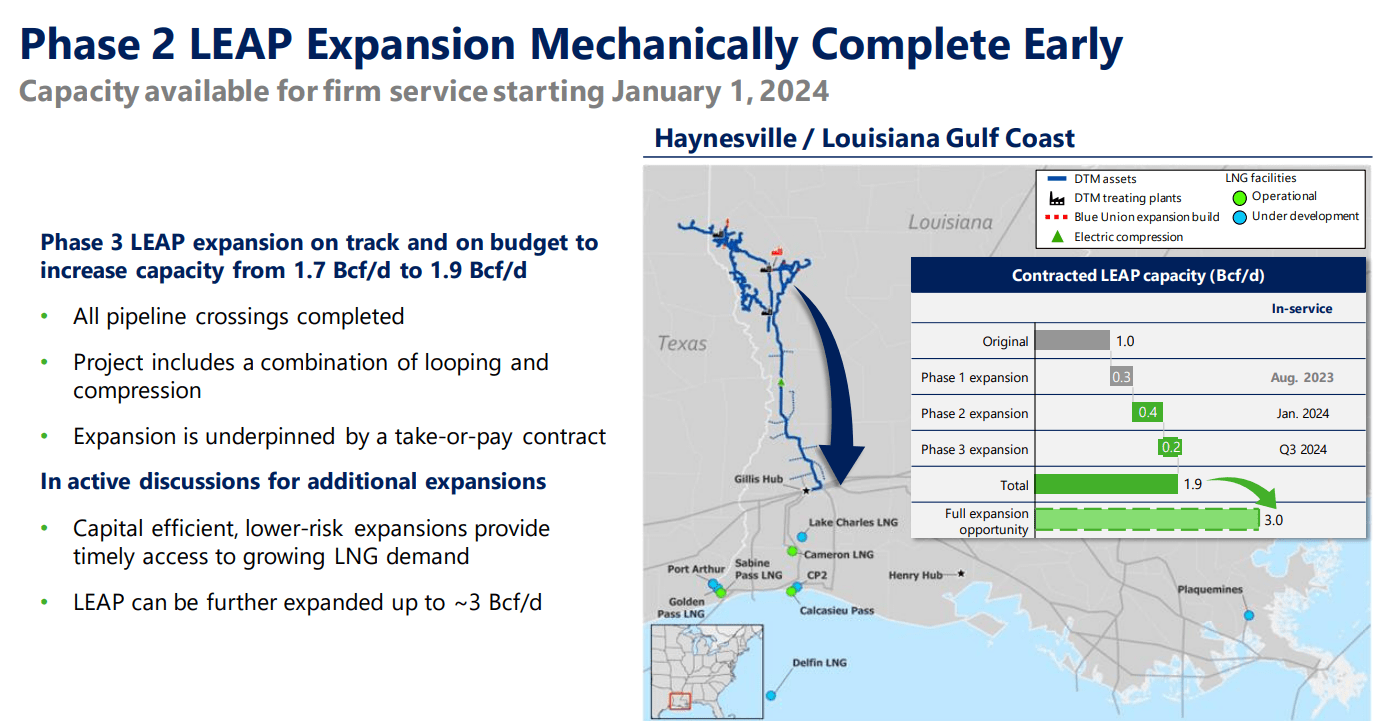

Now that the US has halted the permitting of all new LNG facilities, I doubt DTM will go ahead with all potential expansions, so it will be interesting to get some more color on that.

DT Midstream currently pays a quarterly dividend of $0.69 per share, representing a dividend yield of approximately 5.2%. This dividend will be very well covered, as it represents just 41% of the lower end of the 2023 DCF guidance.

While we will for sure get more details on the projections for 2024 when DTM reports its full-year results, the preliminary EBITDA guidance calls for an adjusted EBITDA of $920-$970M. If I would use the mid-point of that equation, $945M and deduct the sustaining capex (estimated at $40M) as well as the cash taxes (estimated at $35M, subject to revision based on the company’s official guidance) and assume a full-year interest expense of $180M, the DCF would come in at approximately $690M, or $7.11 per share.

That would be a good result, but I hope to see more details when the company reports its full-year financial results.

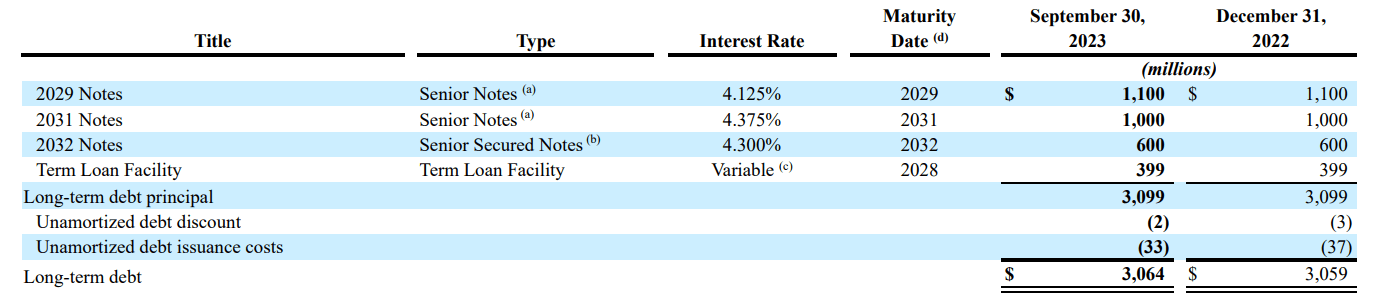

Fortunately DT Midstream has mainly used fixed rate notes for the debt component of its balance sheet. This means the interest expenses should be fairly predictable and it is only the term loan facility that has a variable interest rate.

DTM Investor Relations

The fixed rate component of the annual interest expenses will be $115M. And even if I’d assume an increase in variable debt to $750M by the end of this year and assuming an average cost of debt of 8% (the variable interest rate on the term loan is the 1-month SOFR + 211 base points, which would indicate a cost of debt of just under 7.5% based on the current situation), the total interest expenses would come in at around $60M (and likely gradually increasing throughout the year as DT requires more cash). I topped this up with the anticipated interest expenses on the short-term credit facility to end up with $180M in my DCF scenario above. It’s only when the notes mature in 2029, 2031 and 2032 we will see a substantial increase in interest expenses. Right now, the YTM on those three bonds hovers around 5.8-6% on the secondary markets. This would increase the interest rate bill by $45-$50M, but it will take almost 10 years to see the full impact of the debt refinancings, so I’m not too worried about that.

I currently have no position in DT Midstream, but I will likely initiate a small long position soon, and I would like to expand that position throughout this year. I may write some out of the money put options in an attempt to get my hands on more shares at a lower price. The dividend is attractive as well and considering the strong DCF result and the anticipated single digit DCF per share growth in 2024, I expect the company to deliver on its promise to ‘grow the dividend in line with cash flow’.

This means that if my assumptions for 2024 are correct, we can likely expect an increase in the quarterly dividend to $0.73/share for a full-year dividend of $2.92 for a yield of 5.5%, while keeping the payout ratio virtually unchanged.