PeopleImages/iStock via Getty Images

PeopleImages/iStock via Getty Images

It has been a very disappointing year so far for DarioHealth (NASDAQ:DRIO). We covered the stock in June and were quite optimistic back then.

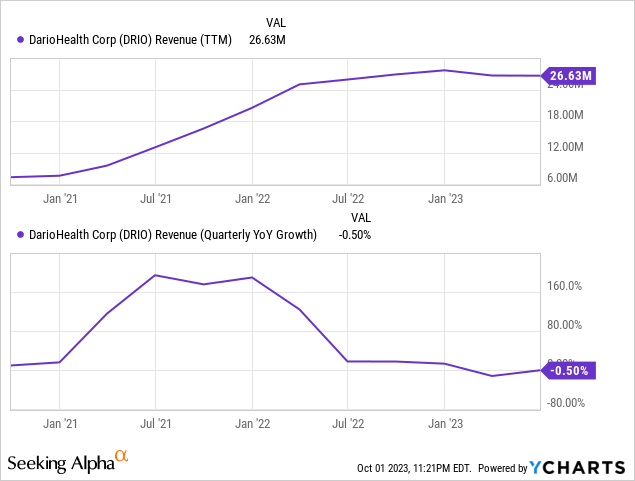

However, in the meantime, Q2 results came in that show that revenue growth has stalled (even if the most important part, ARR from their B2B segment keeps on growing) as a result of customer delays and the pace of new customer wins has declined.

While obviously disappointing, we're not in despair just yet as we think that there are reasons to assume that H2/23 and especially FY24 should be much better.

So we're not giving up on the company just yet apart from renewed revenue growth, gross margin will expand and OpEx is on a mildly declining path so considerable operating leverage and improving company financials are in store.

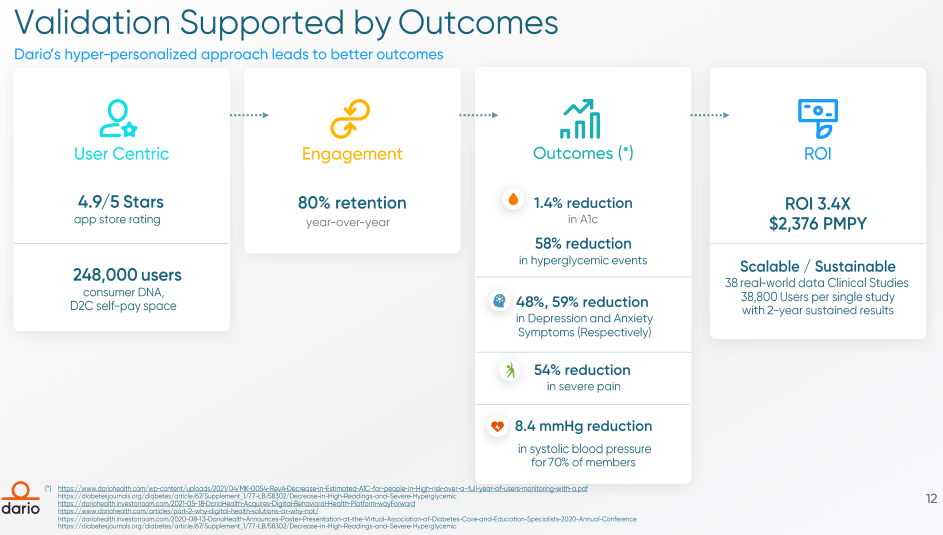

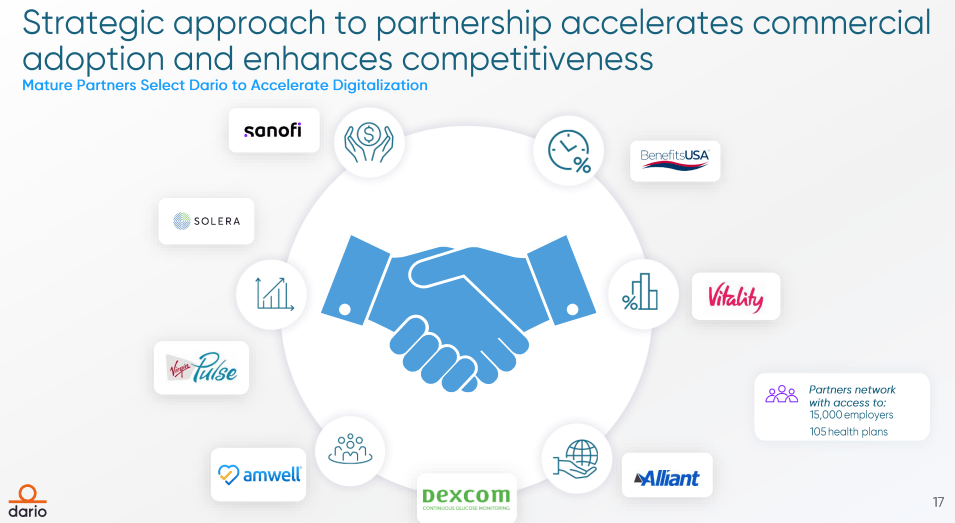

The company is also very well placed with numerous important partners giving it access to a host of potential additional customers and its multi-condition platform is a competitive advantage that has been clinically proven out.

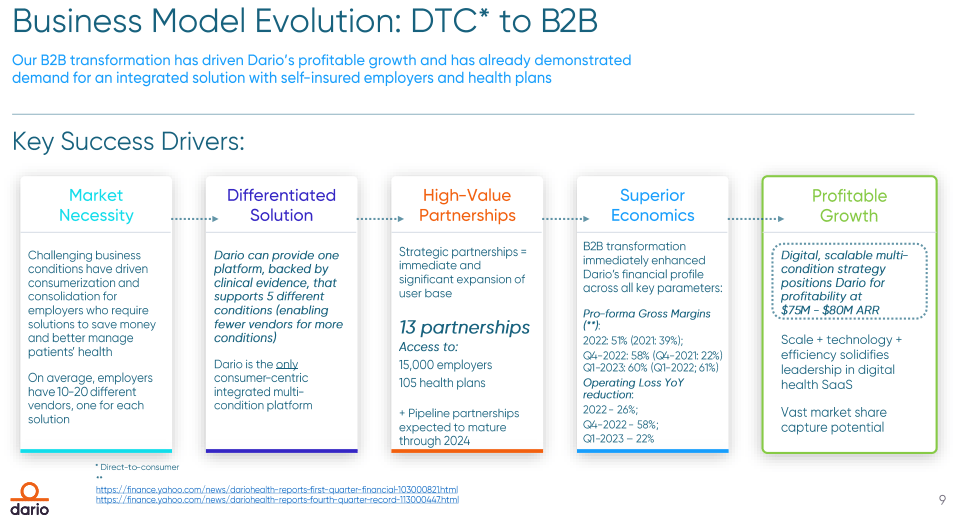

The company's digital health platform started as a B2C platform, which explains the customer-friendly nature, which is a bit of an advantage. The company made a successful shift to B2B where there is less competition and much higher margins can be obtained.

Apart from its customer-friendly platform, another competitive advantage is providing for multiple conditions, enabling a holistic patient view and producing better economics. It offers clinically validated solutions and grows mainly through partnerships.

Customers are health plans and self-insured employers, producing recurring revenues (ARR) on top of milestone payments from partners. They still have their B2C platform which they're not actively marketing hence revenues are flat.

DRIO IR presentation

DRIO IR presentation

DRIO IR presentation

The companies signed a $30M cooperation contract for three areas, data, promotion of Dario's platform with Sanofi's customers, and development of new solutions. This contract was enhanced just two weeks ago, accelerating funds to speed up their program.

Sanofi executed independent studies (here and here) show clinical benefits, and reduced cost (Q2/23CC, our emphasis):

This additional cost data showed that Dario's user’s costs were reduced by approximately $5,000 more per year than a match group that did not use Dario [ph] given that the full suite solution costs less than $1,100 a year

There was a milestone payment delay due to internal reorganization but this will come in Q3. The first customer, MEDI, was launched in Q2/23.

In July/23 launched a regional Blues plan as a customer, the first one through Solera partnership with Diet as an expansion of the contract.

Some 90M people have access to the Aetna platform on which DRIO is integrated. The company delivered its behavioral health platform in Q2/23 and received the milestone payment.

However, Aetna will not start to enroll members before Q1/24 but the population will be 30M rather than the 10M expected initially as it will be sold into more populations. There are other opportunities with Aetna materializing in H2/23.

Amwell is integrating Dario's cardiometabolic solution into its platform for its customers. They expect customers from Amwell in Q4/23 or Q1/24. From the Q2CC (our emphasis):

We remain especially excited about our AML relationship where we are the only cardiometabolic solution integrated into their platform. With an installed base of approximately 2,000 customers, including 55 health plans, we believe this represents an extremely large opportunity. Their health plan customers include several Blues plans, including the largest Blues plan in the country.

DRIO IR presentation

Growth has stalled which is the reason for the retreat in the stock price:

The B2C business isn't shrinking anymore at 37% of revenue

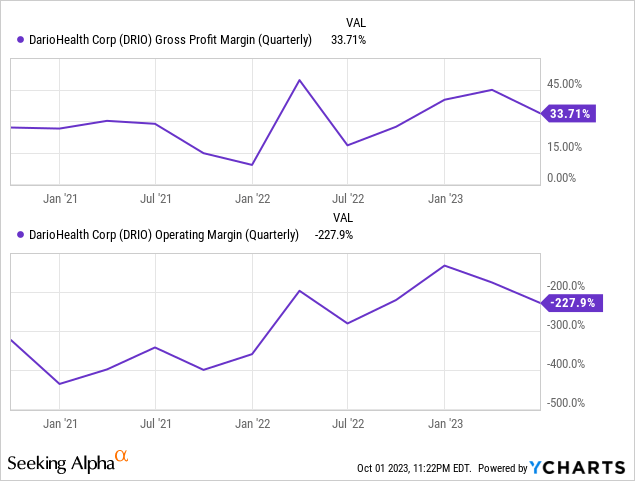

GAAP margins are still pretty ugly:

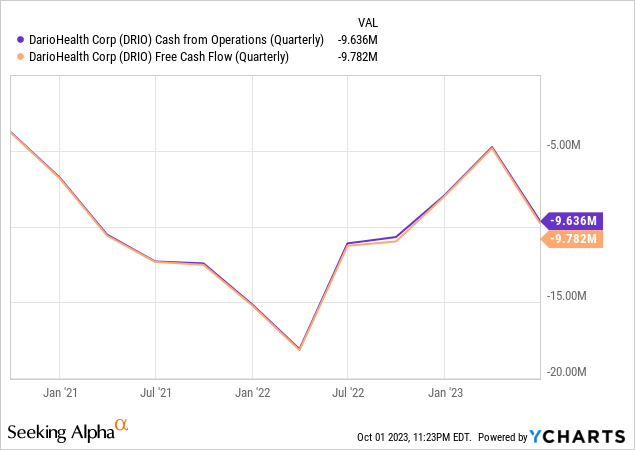

Cash flow has improved considerably until this quarter:

But whether that's enough to avoid additional financing needs remains very much to be seen as management argues that they will be cash flow positive at $80M, which is still far away.

Management expects B2B revenue growth in H2 albeit slower as a result of the Aetna outroll delay. B2C revenue will roughly be constant. There are some near-time drivers that were launched recently:

From the Q2CC (our emphasis):

We remain in the normal annual sales cycle for self-insured employers, the majority of which are on a January to December benefit cycle with most employer contracts signed in the late third and fourth quarters. Based on our current pipeline, we anticipate announcing a larger number of contracts towards the end of this year and realizing significant growth in our B2B2C ARR revenue starting in 2024 from new customers

So we arrive at 39.42M shares out at $2.7 per share gives a market cap of $126.1 and an EV of $103.1. With an estimated $24.7M in revenues this year (rising to $38.9M next year) this results in a still considerable 4.17x EV/S valuation (or 2.64x FY24 EV/S).

Needless to say, the company isn't profitable and won't be next year so earnings-based valuation is senseless at the moment. We're not terribly impressed with these preferred shares, from the PR:

The Preferred Stock provides for holders of Preferred Stock, upon conversion, to receive a 5% dividend payable in common stock each quarter for the first four quarters, followed by a 10% stock dividend in the fifth quarter, for an aggregate stock dividend of up to 30%.

While Q2 results were disappointing, we think that better times are ahead and the shares have already recovered most of the post-Q2 selloff. The company still has multiple things going for it like:

So we think the shares are still a buy here, however, we're not blind and acknowledge that a number of risks exist:

The upshot is that 2023 so far has been a disappointing year but we're not counting the company out as revenue growth is set to re-emerge in H2 and especially next year.

Given the coming revenue growth, gross margin expansion and mildly declining OpEx, cash outlays should gradually decrease and company financials improve. Still a Buy.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.