Scott Olson

Scott Olson

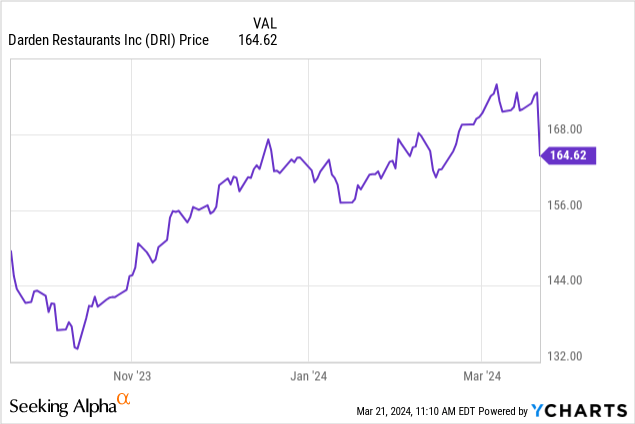

We previously discussed a successful public trade on Darden Restaurants, Inc. (NYSE:DRI). In our last coverage, we told you that the play was to close the trade and to consider leaving some profit in the name of a long-term investment, collecting the dividend, and any future gains with house money. We also felt the stock was about fairly valued at the time.

For the most part, DRI shares have moved sideways overall since then, although the shares caught a recent run up a few points heading into the fiscal Q3 earnings print. We believe watching the action in names we have traded or hold positions in is paramount. But we further believe looking into patterns and results, as well as forecasts, of major companies in key sectors can give us insight into the economy and the consumer.

Darden is a big player in the casual/light fine dining space. So, in this column, we check back in on the company and the stock and discuss the just-reported fiscal Q3 earnings.

Anyone who follows our public work or belongs to our investing group knows that in this space, comparable sales are the key metric we watch for restaurants. In the just reported fiscal Q3 2024, Darden saw growth in sales versus the prior year. The total top-line revenue figure was up 7.5% to $3 billion, which narrowly consensus estimates. What about the all-important comparable sales figure? Comparable sales for the entire company were up just 1.0%. This is positive, but relatively minimal growth. But it is growth nonetheless. Let's examine the comparable sales by each operating restaurant segment.

Here we get more color on what we were seeing. Once again, the best same-store sales increases were in the LongHorn Steakhouse banner, with comparable sales rising 2.3%. However, the same-store sales figure was down in every other segment, suggesting some pushback from a consumer that is getting stretched thin in this high rate, high rent, high credit card debt environment. Same-store sales for the Olive Garden banner were down 1.8%, we had thought we would see positive comps here. The fine dining part of the business saw a 2.3% decline. And other business was also down 2.6%.

While there were these declines, Rick Cardenas, Darden President & CEO stated in the earnings release:

Each one of our segments grew sales and profit in an operating environment that was tougher than we anticipated, and we continued to outperform industry same-restaurant sales and traffic.

While it is true that the comparable sales overall are ahead of the average competitor, seeing comparable sales down in nearly all segments does not exactly jive with the assertion that all segments grew sales. The reason overall sales were up was more operating stores overall.

However, segment profit was up decently year-over-year in most segments except Olive Garden which was roughly flat. Olive Garden saw a profit of $294.7 million vs. $293.0 million last year. The LongHorn Steakhouse banner had a segment profit of $136.6 million, rising from $121.2 million a year ago. Fine dining profit also rose to nearly $81.4 million, up from $51.3 million a year ago, while the other business banners saw a $5.9 million increase to $83.7 million year-over-year.

So overall, fiscal Q3 was "ok," but nothing to write home about. Looking at all revenue and operating expenses, Darden reported adjusted EPS of $2.62, surpassing estimates, and rose 12% from last year.

With this morning's dividend announcement of another $1.31 per share for the quarter, the stock now provides a 3.0% yield. We do expect dividend increases in the future. Darden is also repurchasing shares, with the company retiring $33 million worth of shares in the quarter.

Now, with shares about at levels where we last covered Darden Restaurants, Inc. stock, valuation is pretty fair in exchange for the growth here, in our opinion. The reason shares pulled back however was the guidance was narrowed.

As we look ahead, this Darden Restaurants, Inc. fiscal Q3 performance led to a slight narrowing in the outlook. Sales are seen at $11.4 billion, versus a consensus of $12 billion. Darden Restaurants, Inc. upped its guidance however on the low end of EPS from $8.75-$8.90, to $8.80-$8.90 in EPS on the back of strong first-half earnings. We continue to remain neutral/hold here.