Aleksandr Golubev/iStock via Getty Images

Aleksandr Golubev/iStock via Getty Images

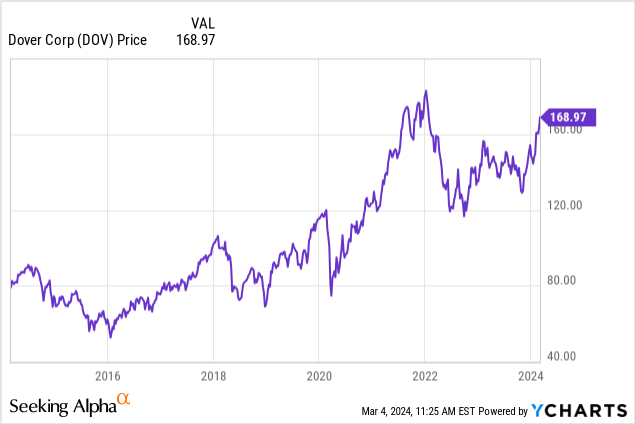

Dover Corp (NYSE:DOV) hit a new annual high Monday. Not only are investors being irrational when valuing DOV, they are irrational in valuing much of the equity market. Most of the DOV metrics indicate the stock is not a buy at the latest price - the dividend yield is only 1.2%, the forward P/E is 18.7x, and it has a negative tangible book value. In addition, the CFO continues to sell stock.

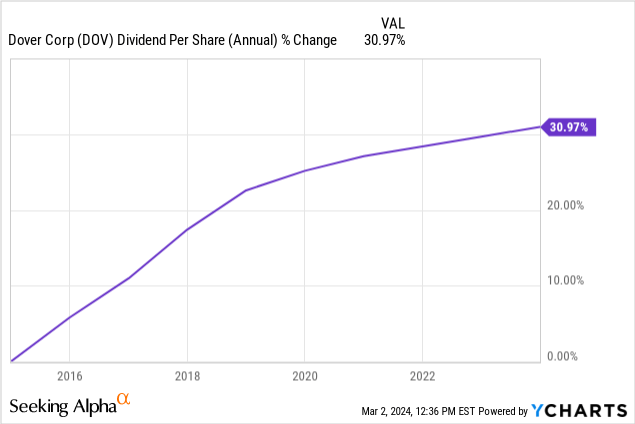

I want to start with Dover's dividends. They increased their dividends for 69 consecutive years. While that seems very impressive, it is not, in my opinion, a rational reason to buy/hold a stock if the stock is otherwise fully valued. The current $0.51 quarterly dividend results in a dividend yield of only 1.2% and is very low compared to 4.53% on 2-year treasuries. The growth in dividends over the last 10 years is about 31%, which implies no real growth because the CPI index was up over 29% over the same period of time. I am not impressed. Total dividends in 2023 increased only 1% to $2.03 from $2.01 in 2022 and were actually lower than the prior year after adjusting for inflation. The dividends are fairly safe because in 2023 they were only 24.9% of free cash flow, which was a very strong improvement from 49.2% in 2022.

Ten Year Dividend Per Share Percent Change

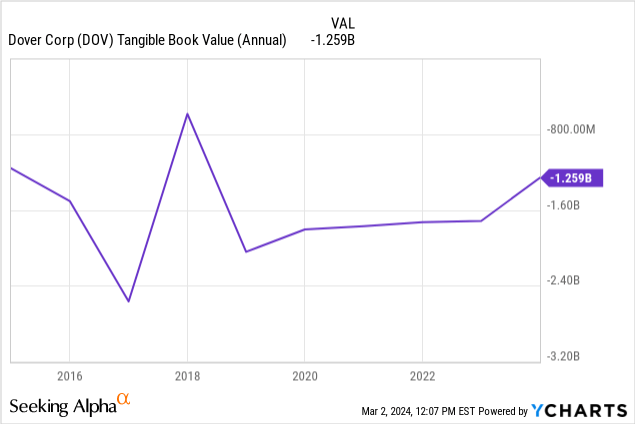

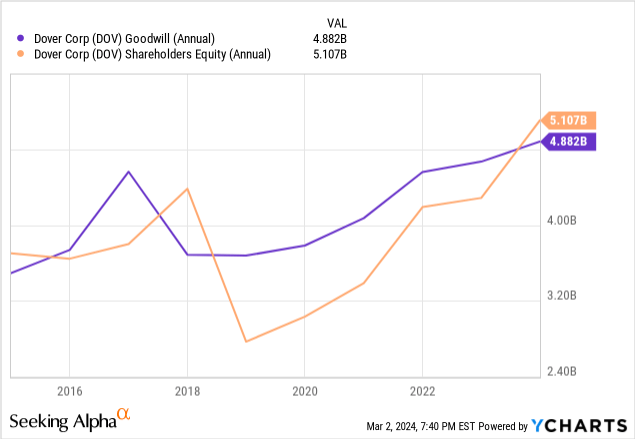

Another "old school" metric that some investors always looked at is book value. Dover has a negative tangible book value of $1.259 billion. There are two major reasons for this huge negative value. First, they have $4.882 billion of goodwill on their balance sheet from buying companies over that company's book value Second, they repurchased $6.798 billion of their stock that reduces shareholder equity.

Tangible Book Value

Total Shareholder Equity and Goodwill

Another popular metric is price/earnings. During their February 1 conference call management gave a 2024 EPS guidance of $8.95 - $9.15. Using the midpoint of $9.05 per share and the latest DOV price of $169.23, the forward P/E is 18.7x. Given their anemic growth the last few years, 18.7x might be a little high given the current high level of interest rates that should be used to estimate the present value of future earnings. It is important to note that their guidance was "largely driven on specific products and end market exposure rather than AG, the Fed's going to drop interest rates and GDP is going to expand".

While this is not actually a metric it is an issue that many investors look at - recent insider buying/selling. CFO Brad Cerepak filed a Form 4 on February 27 disclosing he sold 18,410 shares of DOV at an average price of $163.014 per share on February 23. He still owns 23,909 shares and an additional 2,959 in a 401k plan. He also has 181,754 vested shares subject to stock-settled appreciation rights. I consider this a major negative, especially after he sold 14,000 shares last December 5 at $142.

Dover Corp. manufactures a wide variety of industrial products in the middle of the supply chain. Almost none of their products are sold directly to individual consumers. Dover's actual business model, however, is to buy and eventually sell/spin-off businesses. I have followed this stock since the early 1980's and this has been their business model for decades, but their long-term record has been disappointing relative to the rest of the market.

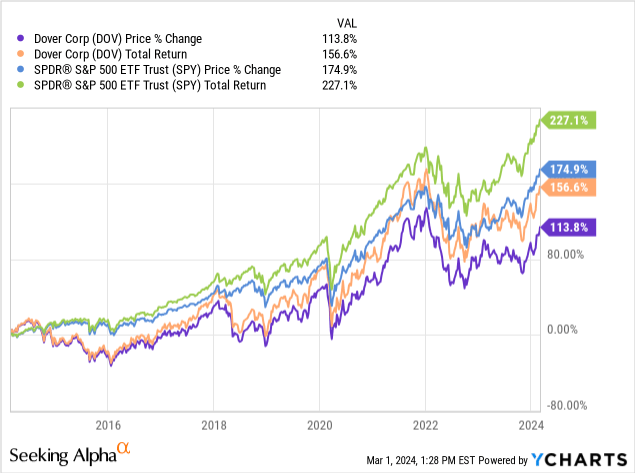

Dover's Total Return vs S&P 500

From 2013 to 2023 Dover purchased 54 companies for $5.86 billion or an average of $108.5 million. Recently they bought FW Murphy for $530 million. During this same time period they sold or spun-off a number of companies. In 2014, Knowles Corp (KN) was spun-off (0.5 shares of KN for one share of DOV) and in 2018 Apergy (formerly APY) was spun-off (0.5 shares of APY for one share of DOV). They just completed the sale of De-Sta-Co for $680 million.

Investors are not really able to evaluate specific acquisitions because the company does report detailed financial results. A new acquisition is often lumped in with the other companies within the segment. So, you are not able to see if synergies were actually achieved, for example.

It is also unclear what Dover brings to the table. In B-school we are taught that, in theory, a major reason for acquisitions is that the purchaser has more and/or cheaper capital than the acquired company. Since Dover has a BBB+ debt rating by S&P and their net debt to net capitalization is a fairly strong 37.3%, it is highly likely that Dover has cheaper capital than many of the acquired companies. Another reason for acquisitions is that the purchaser has better management/better expertise. I don't see that with Dover based on their operating results. Revenue and profits have been weak, especially after adjusting for inflation. This might be a major reason why their long-term performance has not been impressive - no or little value added by the purchaser's management.

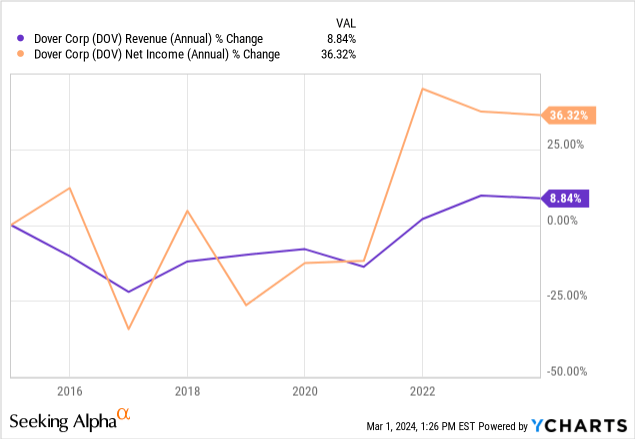

10 Year Revenue and Net Income Percent Change

Dover currently has five segments. Within these segments are many separate companies. The problem for investors is the frequent and constant changes to the make-up of these sectors because of the continued buy/selling of individual companies.

Quarterly and Annual Revenue and Earnings by Segment

sec.gov

I conducted a search on specific companies and most of them have sales brochures with a very long list of products. Dover literally sells thousands of different products. For example, newly acquired FW Murphy has a huge list of products, including pneumatically controlled dump valves, which is shown below. (So, if readers need a pneumatically controlled dump valve, they can buy it from FW Murphy for $400-$600.)

FW Murphy Dump Valves

www.fwmurphy.com

There are other Dover products, however, that individual consumers come in contact with daily such as refrigerated display cases made by Hillphoenix.

Hillphoenix Refrigerated Display Case

www.hillphoenix.com

Having so many products also means having so many different raw materials and suppliers. This means that there could be serious future supply chain problems such as what happened in 2021 and 2022. With a relatively financially strong parent company, individual companies are able to carry inventories without being squeezed by their vendors, especially when there are weaknesses in that specific industry. If a company faces serious financial problems often vendors have strict terms, including C.O.D., but companies owned by Dover would most likely not face such problems. This is a major competitive advantage.

Dover has a significant exposure to the energy industry, especially natural gas. The domestic natural gas industry has been doing well the last few years in part because of exports of LNG. From a long-term view, this is part of an industry that much of the world wants to "terminate". They also have exposure to clean energy that could benefit from the "Inflation Reduction Act" and the "Bipartisan Infrastructure Law". If Trump is elected will some of these tax incentives for "clean" hydrogen projects be scaled back or even eliminated?

The year-end bookings imply that revenue for 2024 could be lower than 2023 because year-end bookings have historically been 95% to 105% of the following year's revenue. Management's EPS guidance of $8.95-$9.05, which compares to $7.52 in 2023, could be a challenge, in my opinion. In order to reach their guidance, margins would have to increase significantly from 2023 year's margin of 21%.

Year-End 2023 Bookings and Change from Prior Year

Engineered Products $2.097 billion +4.6%

Clean Energy & Fueling $1.746 billion (4.1)%

Imaging & Identification $1.121 billion (2.9)%

Pumps & Process Solutions $1.677 billion (1.9)%

Climate & Sustainability Technologies $1.349 billion (19.2)%

4Q and Annual Income Statement 2023 and 2022

sec.gov

I sold all my DOV stock last Friday and this morning (Monday) along with a number of other stocks because I thought the entire market was overpriced. I only bought DOV a few months ago as a trading stock. For decades Dover Corp. has been difficult to analyze because their holdings and thus their industry exposure keeps changing. The reality is many investors buy/hold DOV stock not because of specifics related to their operations but based on management's ability to buy and sell companies profitably.

I consider DOV stock a long-term neutral/hold because there are some potential positive developments, such clean energy, but at the same time there are long-term negatives, such as being in the fossil fuel industry that much of world is trying to "terminate". In addition, their P/E of 18.7x is not a bargain. I would not, however, hold DOV based solely on their 1.2% dividend yield because there are other better dividend-based investments.