Tetiana Voitenko

Tetiana Voitenko

Amid a record high for the S&P 500, the right move (at least in my view) is to chase value-oriented plays, but we should stay away from over-rotating toward value traps. And though it's hard to define exactly what a value trap is, I'd say nonexistent growth is one of the telltale signs.

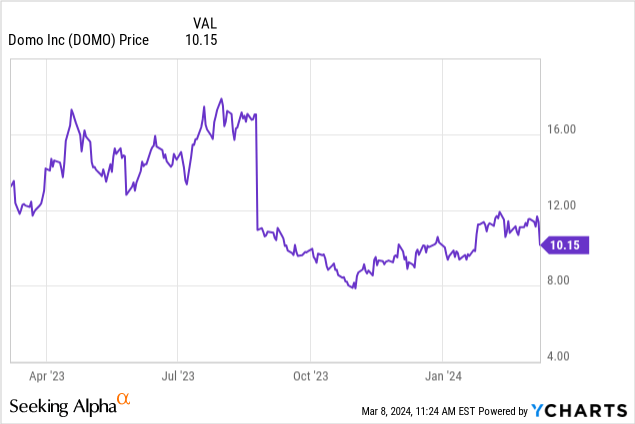

Such is the case with Domo (NASDAQ:DOMO), the BI (business intelligence) software vendor that just reported dismal Q4 results and an even worse outlook for FY25 (the year for Domo ending in January 2025). The stock sank ~10% after the earnings release, contributing to an already-bad ~20% decline over the past year (while most fellow software companies have gained that amount or even twice that amount over the same timeframe).

I last wrote a bearish opinion on Domo in December; and unfortunately, while the stock is still hovering around the same levels as back then (briefly, Domo rose in sympathy with the rest of the market, before the reality of its poor fundamental execution kicked in and erased those phantom gains), its outlook and business trajectory has gotten much worse. With this in mind, I remain quite bearish on Domo going forward.

It must be noted as well that many investors may still be holding on to Domo for the hope of a buyout. Many beleaguered tech companies have enjoyed that rescue over the past year (Alteryx (AYX) is one such example). But we note that Domo has had a sub $500 million market cap for years, and with no bites at all, it has become clear that Domo is an unappealing target with a rather saturated product and a corporate structure that is losing cash every quarter.

Here's a reminder to investors as to the biggest red flags for Domo:

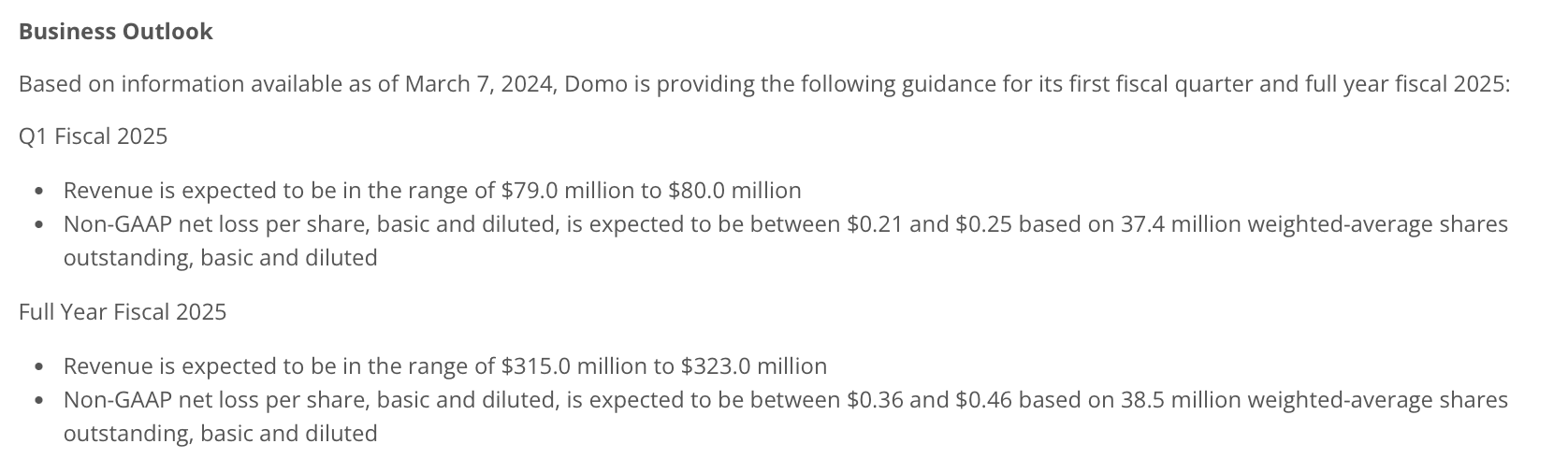

Perhaps the most sobering news of all: Domo is not expecting a turnaround whatsoever in 2024; in fact, the low end of its guidance range implies a y/y decline in revenue.

Domo outlook (Domo Q4 earnings release)

The company's $315-$323 million range represents anywhere from -1% y/y to a +1% y/y growth rate. Considering revenue has already flatlined over the past few quarters, and without any meaningful catalysts to prompt a recovery, I'd say an even bigger decline is highly possible. Domo's biggest hope for growth is its pivot to a consumption model - but again, with challenged IT budgets, meaningful expansion from within the customer base is not very likely to happen.

Steer clear here: there's a lot of risk for very little reward.

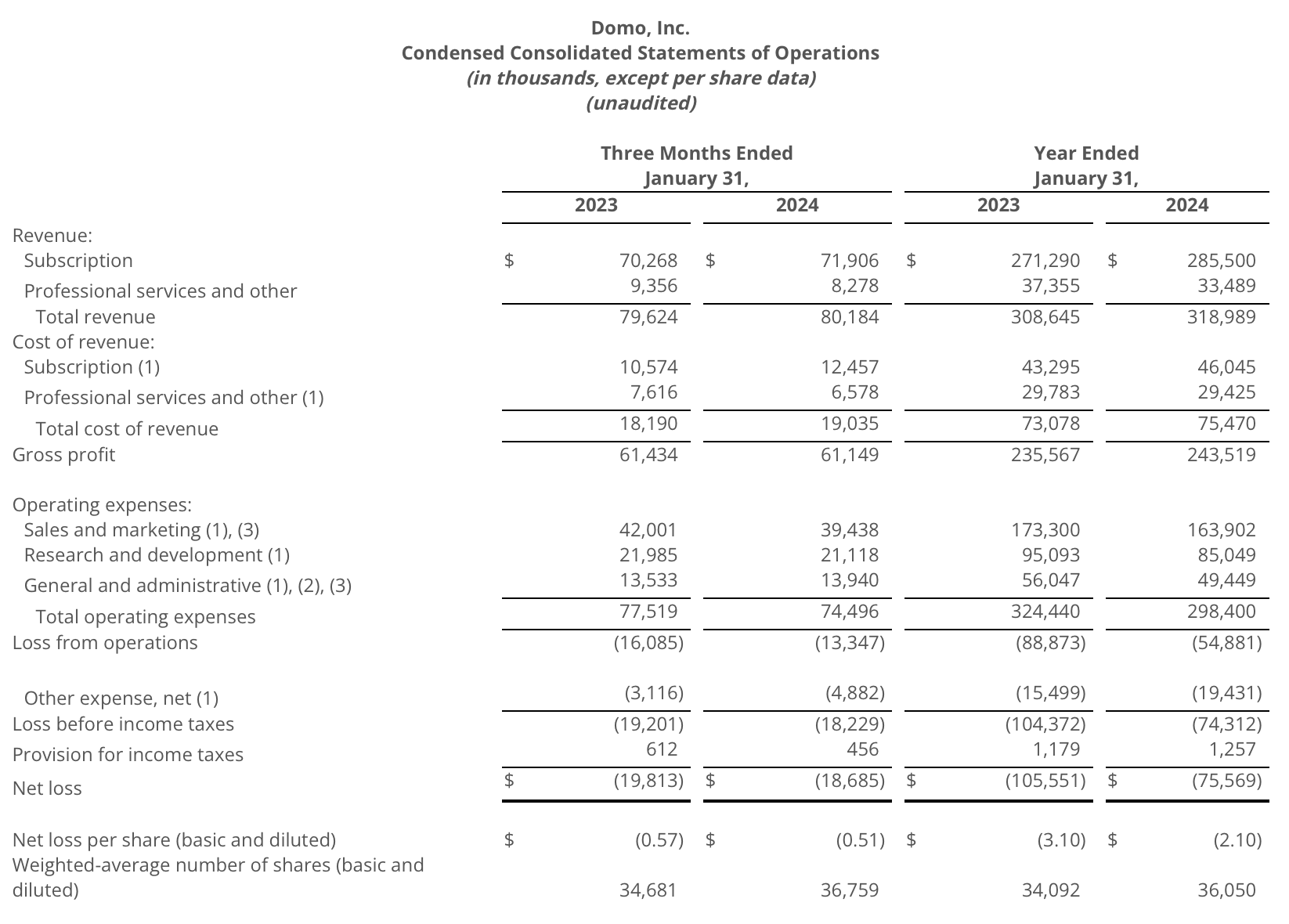

Let's now go through Domo's latest quarterly results in greater detail. The Q4 earnings summary is shown below:

Domo Q4 results (Domo Q4 earnings release)

Domo's revenue grew only 1% y/y to $80.2 million, essentially in-line with Wall Street's expectations of $79.7 million (flat y/y) and in-line with last quarter's 1% y/y growth pace. Billings of $105.4 million also grew only 1% y/y, erasing hopes of a revenue acceleration in future quarters (as seasoned software investors are aware, billings is a great forward-looking predictor of a subscription company's eventual future growth rates). The reason that billings eclipse revenue on a nominal dollar basis is that in the fourth calendar quarter of the year, many IT departments try to exhaust their annual budget allocations.

Again, Domo has pinned its hopes on recovery on its consumption model: hoping that its customers will pay more for the privilege of boosting their usage of Domo over time. Per CEO Josh James' remarks on the Q4 earnings call:

Over the last two quarters, our consumption customer base has doubled, just two quarters doubled.

In Q4 consumption deals accounted for over 90% of the dollar value of our new logo deals. Very significantly of our consumption customers that have already been on the consumption model for at least six months around half of them are already pacing to use more credits than what they originally contractually purchased.

Now we anticipate this number will increase meaningfully as that time span increases from six months to nine months and 12 months, and we believe this will lead to many more upsell opportunities in the year.

And again, our interests are aligned with our customers, they are getting more value as their credits are being consumed and we believe this is a fantastic leading indicator that we just recently discovered.

These results showcase compelling indicators of future revenue growth and we are even more committed and even more poised to move the majority of our customers onto the consumption model this year."

The company has switched to a "freemium" model, a common concept for users of many apps. It's hoping to hook new customers based on free trials and converting them into high-usage consumption customers later.

On profitability: Domo improved marginally on pro forma operating margins, up to 4.0% in the quarter (+60bps y/y). Still, alongside virtually zero growth, it's challenging to see how Domo can scale; and note as well that in FY24 the company still burned through $9 million of free cash flow.

At current share prices near $10, Domo trades at a market cap of $374.2 million; and after we net off the $66.5 million of cash and $108.6 million of debt on Domo's most recent balance sheet, the company's resulting enterprise value is $416.3 million.

Against the midpoint of Domo's $315-$323 million revenue range for the year (which implies flat y/y growth), Domo trades at just 1.3x EV/FY25 revenue - but again, this stock is quite cheap for a number of reasons and red flags. The only true "upside risks" here are 1) the small chance that the company's consumption model takes off and drives incremental revenue growth, or 2) that a miracle acquirer comes out of left field to take Domo private.

Don't fall into this value trap; as I don't see either of those conditions materializing. Steer clear and invest elsewhere.