M.photostock/iStock via Getty Images

M.photostock/iStock via Getty Images

DocuSign (NASDAQ:DOCU) experienced explosive growth during the global pandemic period, and nowadays their billing growth starts to normalize coming out of the pandemic. They reported their Q4 FY24 result on March 7th after market close, showing healthy billings growth. I initiate with a ‘Buy’ rating with a fair value of $75 per share.

In 2000, Bill Clinton signed The Electronic Signatures in Global and National Commerce ((E-Sign)) Act, making the e-signature legal in the U.S. market. The work-from-home situation during the pandemic stimulated demand for the e-signature market, contributing explosive growth for DocuSign. However, the market started to normalize as the pandemic receded, and additionally, the market is getting more and more competitive. DocuSign is facing strong competition from Adobe Document Cloud, as well as bunches of new players. For example, Dropbox (DBX) acquired HelloSign in January 2019 to enter the e-signature market. BOX (BOX) acquired SignRequest in January 2021.

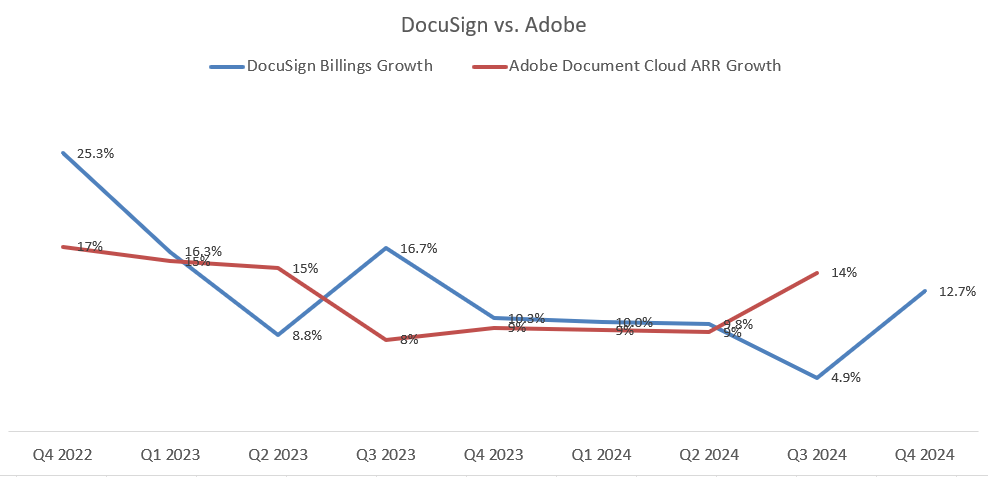

Adobe’s (ADBE) Document Cloud covers editing, sharing, reviewing, scanning, and signing, a comprehensive solution for the e-document preparation and executions. As depicted in the chart below, Adobe’s Document Cloud business growth has followed a trajectory similar to that of DocuSign.

DocuSign and Adobe Quarterly Results

The rising competition can be attributed to several factors. The total addressable market is substantial, and DocuSign estimates the market size is around $50 billion. Manual signatures remain common in many agreements, creating a huge penetration growth opportunities for all players in the e-signature space. The lucrative market is definitely attracting many new players to enter this space.

Furthermore, the e-signature technology is not inherently complex or high tech. The vendors need to address the cloud hosting, security, credibility, and account verification etc. For e-signature companies, the primary success factors lie in effective sales and marketing, as well as distribution channels.

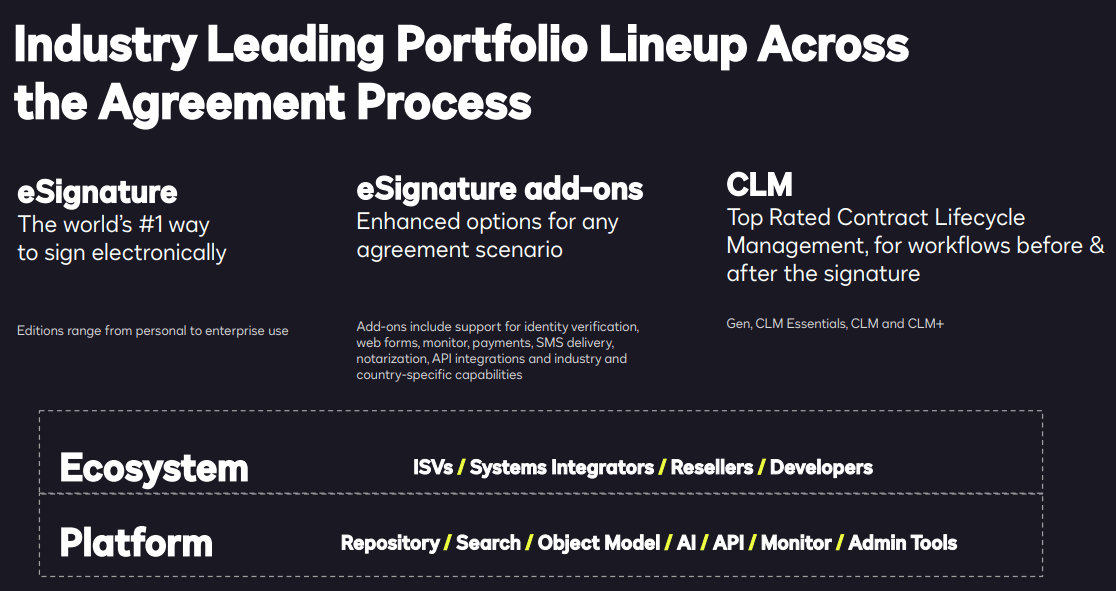

I anticipate the competition in the e-signature market will intensify in the near future. DocuSign has the leading advantage, however its growth would depend on how quickly they can penetrate more enterprises customers, as well as expand their product offering beyond e-signature, including add-ons and Contract Lifecycle Management as exhibited in the slide below.

DocuSign Investor Presentation

In order to sustain their growth trajectory in the future, DocuSign has been expanding their product offerings beyond their core e-signature market. In recent years, DocuSign has pursued several acquisitions to scale up their Contract Lifecycle Management system (CLM). One of the most significant acquisitions was the purchase of SpringCM for $220 million in 2018. SpringCM’s solutions could connect and automate the entire agreement lifecycle. The combination of agreement management and e-signature could benefit enterprise customers to simply and automate the contract process.

In addition, DocuSign is expanding their services into the notary market. In most cases, notary is a regulated market. Currently, they offer online notary services. The company is broadening their DocuSign product to include notary, identity verification and monitoring services. This strategy of expanding service offerings around their e-signature core appears to be a smart move in my opinion.

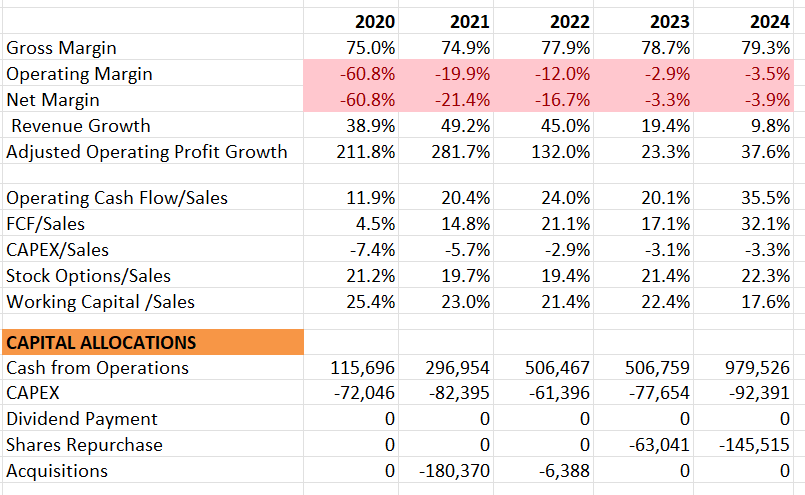

Following an explosive growth period during the global pandemic, their sales growth has began to normalize, with 9.8% revenue growth in FY24. However, it is impressive to see their profit growth and cash flow margin improvement, as illustrated in the table below.

DocuSign 10Ks

DocuSign’s adjusted operating profits was up 37.6% year-over-year in FY24, and the free cash flow margin expands to 32.1% in FY24. They initiated their shares repurchase from FY23, and bought back $145 million of own shares in FY24. I am encouraged by their margin improvement and enhanced capital allocation policy.

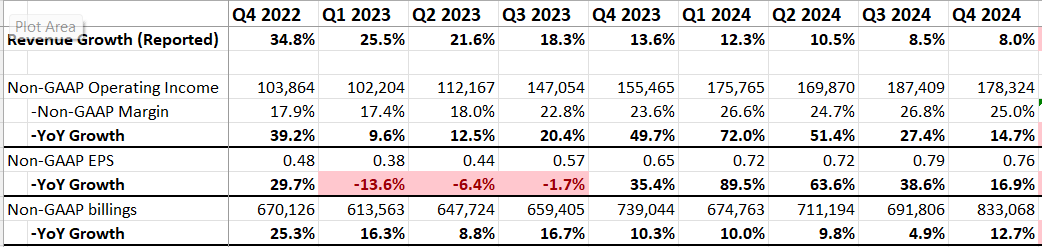

My biggest takeaway from their Q4 FY24 is the double-digit billing growth. The billing growth is a leading indicator for their future revenue growth. In Q3 FY24, DocuSign only guided $758 to $768 million in billings for the Q4, representing 3% year-over-year growth at the midpoint. The actual billing growth in the quarter surpassed their internal expectations, which is quite remarkable!

DocuSign quarterly results

The impressive billing growth indicates the normalization of enterprise spending optimization and IT budget scrutiny. I anticipate DocuSign’s business will continue to normalize, with the company focusing on margin improvement and new areas. During the earnings call, their management highlighted that their solid executions around renewals with large customers contributed to their billing acceleration in the quarter. In addition, they signed some new customer in the quarter, contributing to almost half of the billing acceleration.

The company had $1.2 billion in cash with no debt, a quite strong balance sheet indeed.

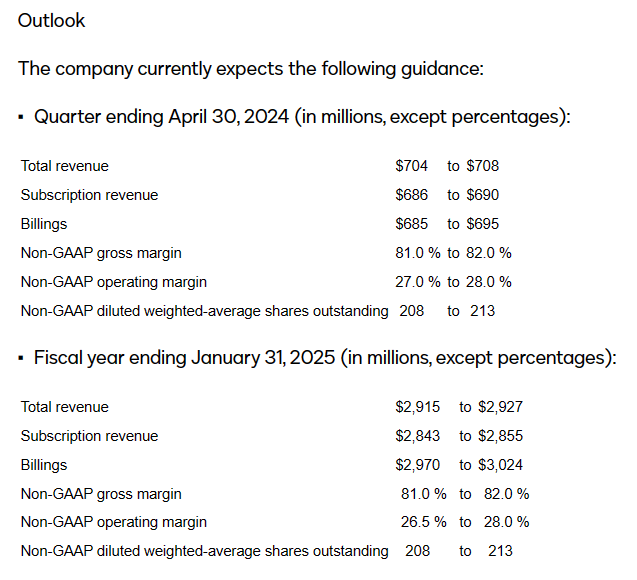

Their guidance implies 5.7% revenue growth and 3% billing growth for FY25. In addition, they forecast the adj. operating margin to be 26.5%-28% in FY25, which represents a notable expansion compared to 25.8% in FY24.

DocuSign Q4 FY24 Release

Regarding the growth in FY25, the following aspects need to be assessed:

Early Renewal: As discussed previously, half of their billing acceleration in the quarter was due to the strong renewal with large customers. Some of these belong to early renewals that would negatively impact their FY25’s billing growth. The company forecasts the dollar net retention to be flat to slightly down in the first quarter of FY25.

International Growth: DocuSign is still a U.S. centric business, with more than 70% of revenue exposure. Their international revenue doubled in the quarter, now representing 27% of total revenue. I agree with the management that international expansion represents a significant growth opportunity for the company.

Headcount Reduction: DocuSign has 6,840 employees now, which is 6.7% lower than last year. The layoffs definitely contributed to their margin expansion in the near term. As a result of the layoffs, the company is able to maintain their SBC cost flat in FY25, as communicated during the earnings call.

Considering these factors above, I believe their guidance for FY25 is quite achievable. With there strong billing growth of 9.4% in FY24, the company should be able to achieve their revenue growth target.

The FY25 assumptions are based on the midpoint of their guidance. DocuSign has proactively expanded their core offerings beyond the e-signature market. As discussed previously, the Contract Lifecycle Management (CLM) has been leveraging DocuSign’s extensive customer base. During the earnings call, their management disclosed that CLM grew faster than the total business, and growth accelerated from Q3 to Q4. Overall, they are witnessing strong adoption among enterprise customers.

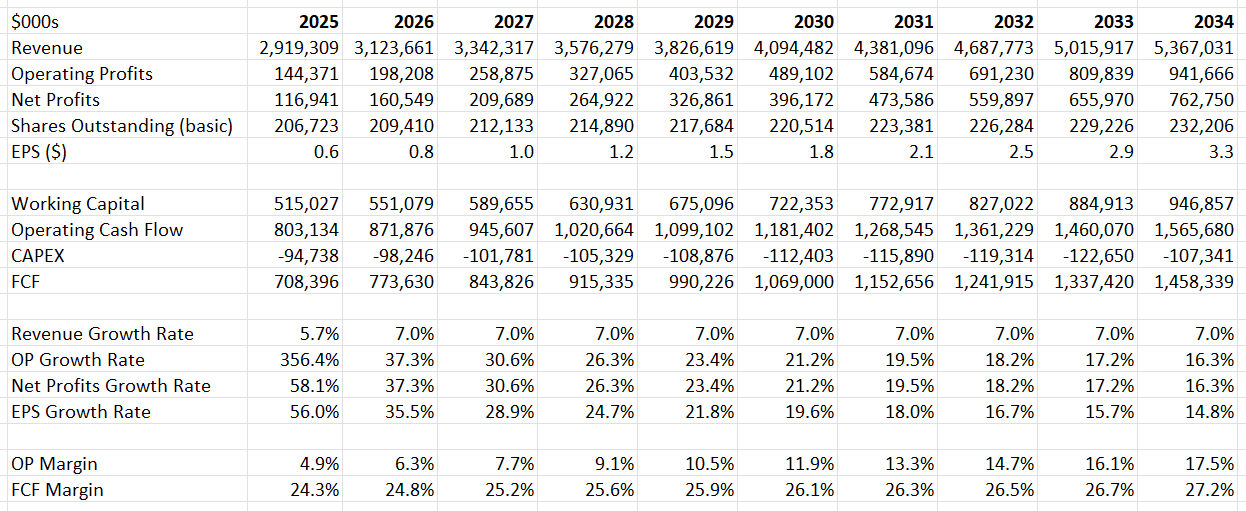

Consequently, for the normalized growth, I forecast 7% revenue growth in the model. This assumption includes 2% growth from core e-signature business, 2% growth from international expansion, and 3% from new service offerings including CLM.

Due to their cost control initiatives, I anticipate their operating margin will continue to expand. I estimate their operating expenses will grow 2% lower than their topline growth, leading to strong operating leverage. I forecast their OPM to reach 17.5% by FY34, a quite conservative figure compared to other mature software companies.

With these parameters, the total present value of future free cash flow to firm (FCFF) is calculated to be $13.5 billion in total assuming 10% WACC, a consistent discount rate I use across all my models. To estimate the equity value, I adjust their enterprise value with the projected cash balance of $1.55 billion and zero debt. The total equity value is calculated to be $15.4 billion in total; thus, the fair value is calculated to be $75 per share in them model assuming 207 million basic shares outstanding. The current stock price is trading at around 15x fwd. free cash flow, a quite cheap multiple in my view.

DocuSign DCF - Author's Calculation

Stock Options: SBC accounts for 22.3% of total revenue in FY24, a quite high level compared to other tech firms. The good news is that the company expects SBC to remain flat in FY25, indicating a decline in the SBC/Revenue ratio. Of course, the layoff attributed a lot.

Cyber Security: cyber security is extremely important given the nature of DocuSign’s business. Any significant cyber incident could potentially compromise the agreements stored in the cloud.

Competition from Adobe: Frankly, this is my biggest concern for their e-signature business. Adobe is a quite respected tech company, and they have all the resources including capital and talents to strengthen their document cloud offering.

I am encouraged by DocuSign’s expansion into adjacent areas, and their impressive margin and free cash flow improvements. The stock price is undervalued and I initiate with a ‘Buy’ rating with a fair value of $75 per share.