SerrNovik/iStock via Getty Images

SerrNovik/iStock via Getty Images

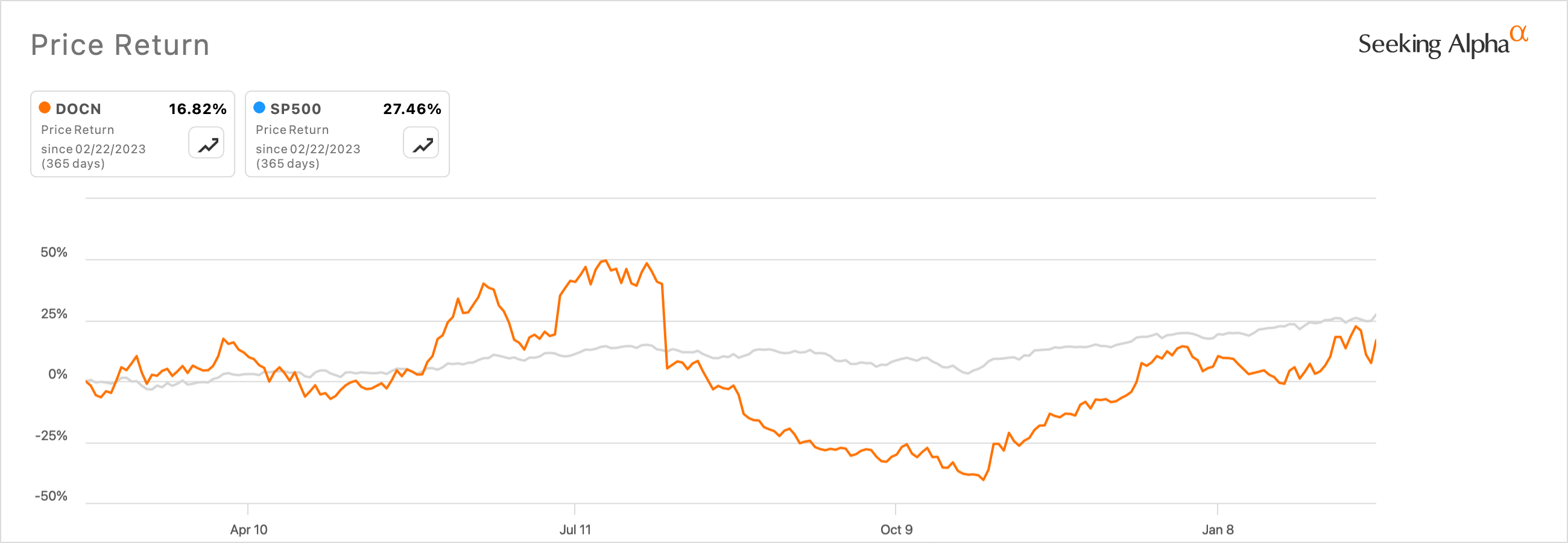

A lot has changed for DigitalOcean (NYSE:DOCN) in the past 14 months. Let's start by doing a sanity check on the company's stock performance. DigitalOcean, or DO as the company sometimes calls itself, underperformed the benchmark index by scoring a ~17% return, ~10% under the S&P 500 index (SP500) over the past year.

sa

Last year, the company's Q2 FY23 results shocked its investors after it announced in that report that customers were churning and spend was falling on their platform in addition to the revenue and EPS misses in that quarter. Two weeks after that call, their CEO announced his resignation, and the stock continued its freefall, dropping 60% from its FY23 high last year.

The company announced their full year FY23 earnings last week, and while the results were slightly better, many fundamental questions still remain, causing me to rate this as a Hold, despite my model showing upside.

DigitalOcean was founded in 2012 with the aim of offering simple & affordable cloud computing solutions for developers. The company's products are spread over two markets in the cloud computing space: Infrastructure-as-a-Service (IaaS) and Platforms-as-a-Service (PaaS). The company's Droplets product was its first and most famous product to date that allowed developers to easily manage virtual machines (VM) in the cloud. Developers usually find DO's UI to be comparatively easy to scale and deploy applications in the VM as compared to other cloud computing products offered by AWS, Google, Microsoft, etc.

DO does not break out its revenue by segments, despite the company breaking out its TAM by IaaS and PaaS market segments. The company focuses on regular SaaS metrics such as Annual Recurring Revenue (ARR) and $-based Net Retention Rate (NDR).

In the past 15 months, DO's executive management has changed hands in the CEO's chair as well as the CFO's chair.

At the outset of the Q4 FY23 call, DO's new CEO announced 5 growth pillars that he and his management team will be focused on moving forward. Two pillars are focused on product and platform product initiatives, while the third is related to its AI/ML strategy by building on its acquisition of Paperspace last year. The fourth initiative touched upon a new managed service offering called Autonomous, which was launched a month ago.

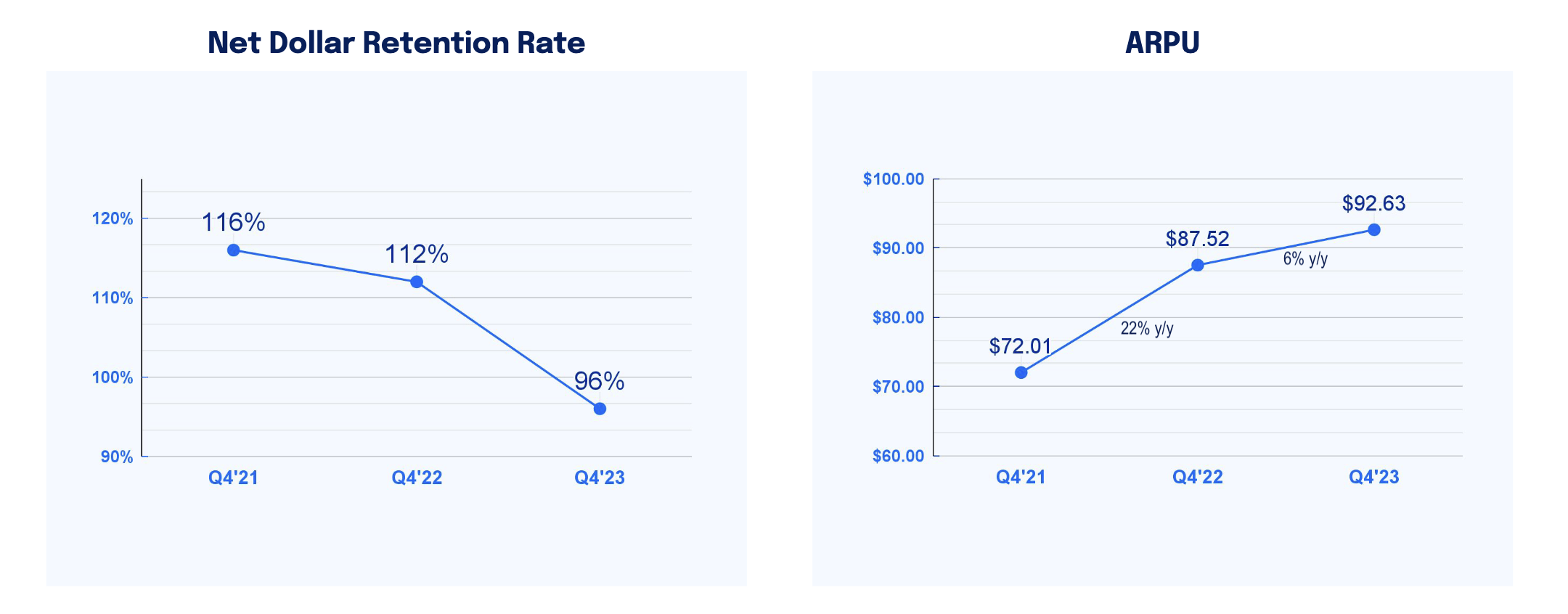

My initial impression of the Autonomous offering is that DO wants to tap into the segment of its target market that prefers assisted services as they scale capabilities on DO's platform. I suspect management is rolling out these four initiatives as they are in a dire situation to arrest the decline of its NDR, which continued to languish below 100 for the second straight quarter.

DigitalOcean's Customer Economics, Q4 FY23 Investor Presentation

On the call, management indicated that while churn had not changed on a y/y basis, it was essentially spent on the platform by their existing cohort of customers that contracted. This is one of the reasons that NDR did not contract further but still stubbornly stayed at the 96% level, unchanged on a sequential basis. Here is some commentary from the CFO that alludes to my point:

The churn has not changed. It's right around where it was even a year ago. The contraction is a little bit elevated, but it's been fairly stable over the last, now seven, eight months. Where we saw the most pressure year-over-year, last year was in expansion. And that expansion was customers owned businesses just weren't growing as fast, and so they didn't need more compute. And so we didn't see as much growth in the core kind of droplet part of the business.

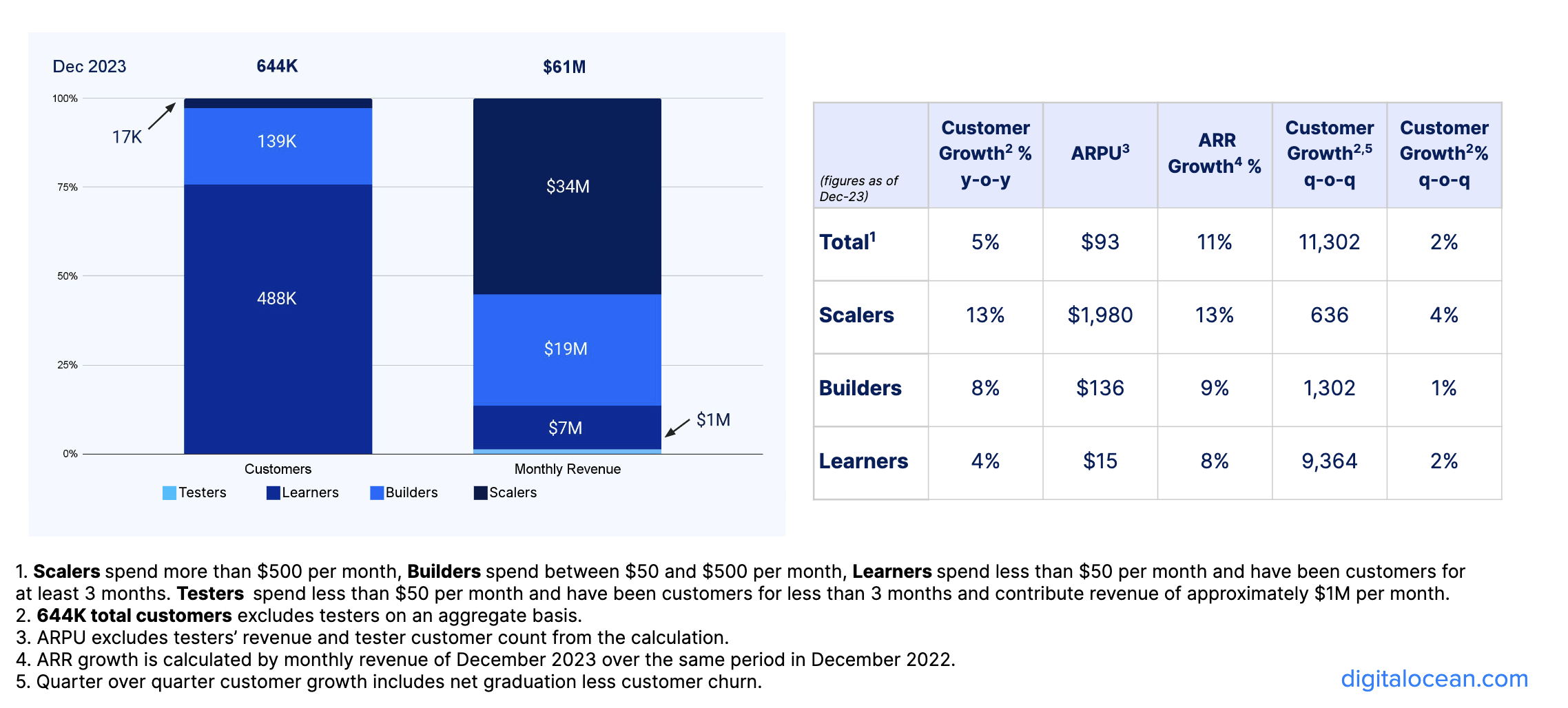

Another interesting observation in the commentary above was the CFO's reflections on the pressure the company saw on expansion because its customers did not need more compute. I believe, DO experienced this spend dynamic because of its customer mix, which, per its most recent quarter, is heavily skewed towards its Learners and Builders customer cohorts, which, as per the chart below, had slow sequential growth.

DigitalOcean's Customer Metrics, Q4 FY23 Investor Presentation

Learners and Builders tend to be smaller customers, or SMBs, whereas Scalers are their larger customers. Per its FY23 10-K, Learners account for 3/4th of DO's 644k customer base, Builders make up a fifth of DO's customer base, and the rest are Scalers. My strong sense here is that DO's price increases rolled out in 2022 may have played a part in the churn in DO's SMB customer cohorts. Most of these customers were also acquired via its self-service sales model.

This brings me to the final and fifth initiative that the CEO mentioned. Management will be focused on ramping up its sales strategy and its customer success strategy. I believe this is the need of the hour for DO, as it becomes highly important for DO to tap into larger customers while incentivizing existing customers to spend more on the platform, which will boost its growth rates.

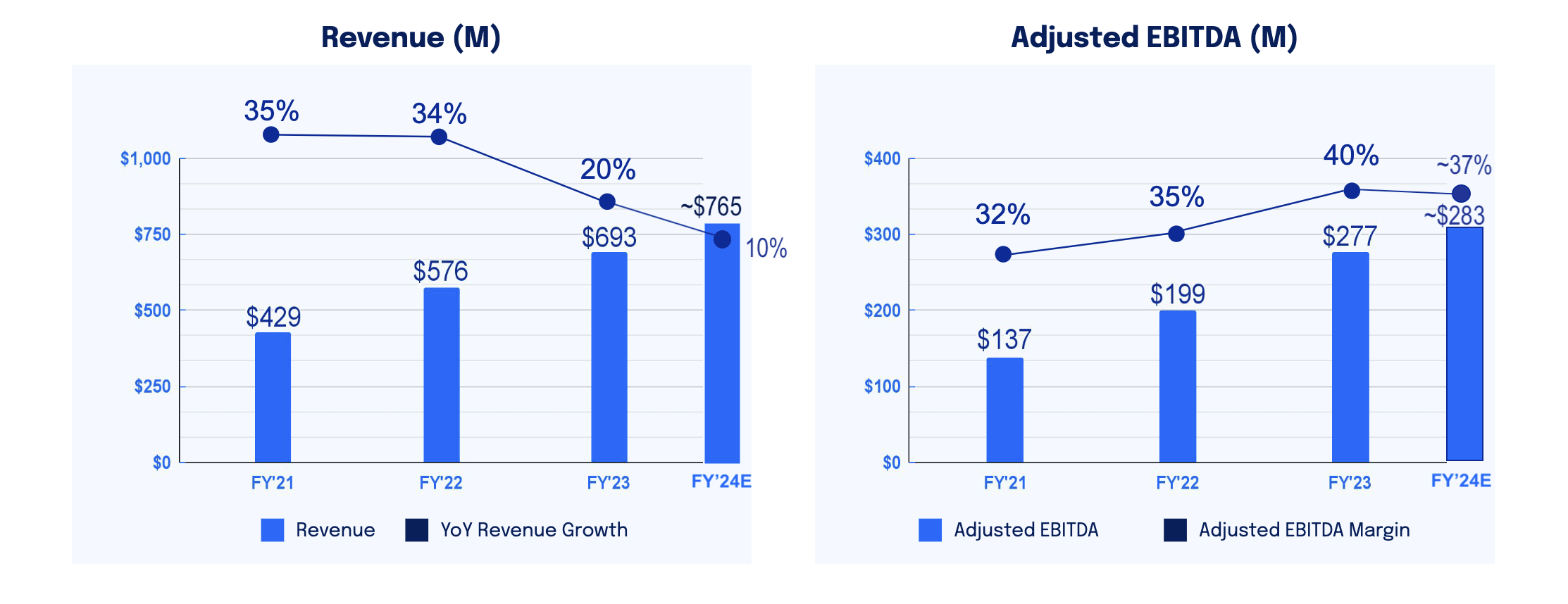

So far, DO has seen slow growth rates in its revenue, as can be seen in the chart below. And based on guidance from management, growth is expected to slow even further to 10% this year. DO's ARR has also slowed to just 11% y/y to $730M. Compared to the 36% y/y growth seen in Q4 FY22 and 37% y/y growth seen in FY21, it looks like DO's best days are behind it-unless management is able to deliver on its 5-point growth plan within this year itself.

DigitalOcean's Revenue & adj. EBITDA, Q4 FY23 Investor Presentation

The company did see its adjusted FCF trend rise last year to 22%. On the top, it looks promising, but stock-based compensation (SBC) continues to be a big driver of the adjusted FCF, with SBC margins at 12.7%, lower than the 18.7% in FY22. Still, the company earned 20 cents per share, or $1.59 cents per share, on an adjusted basis, which also helped its adjusted FCF margins of 22%.

It is important for the company to continue generating free cash moving forward to help it maintain its $1.5B in senior notes that are due in 2026. The company's current cash position of $317M will not be enough to service its debt, and it will have to either generate free cash at a faster rate or raise more debt to service previous debt.

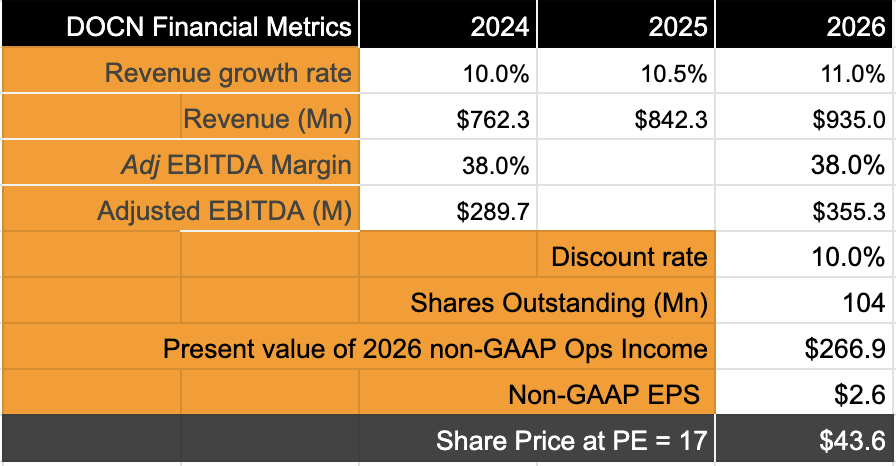

To conduct my valuation, I have assumed management's own projections for FY24 while factoring in consensus estimates for the remaining years. For its adjusted EBITDA margins, I have assumed no expansion as it continues to spend on scaling its sales strategy. These assumptions imply revenue and adjusted EBITDA will be growing at a CAGR of ~11% through FY26. This model does imply about 12% upside, but I will prefer to be neutral given the impending uncertainty about turnover DO's management as well as the transition of strategies this year.

Author

The reason I do not have confidence in issuing a buy at this point, despite the math suggesting it, is because DO has failed to grow per its target market. Per a previous investor presentation, DO projected its TAM would grow at a CAGR of 27% from FY20 to FY24. Unfortunately, the company's revenue will grow at a CAGR of ~24.9% over the same time period if DO manages to beat the upper end of its FY24 revenue guidance of $775M this year.

Competition is a factor that may affect the company's prospects. In 2022, Akamai acquired Linode, a direct competitor to DO, to build out their own developer-friendly solutions. Linode tends to have an edge over DigitalOcean in the larger customer segment, which may pose a problem for DigitalOcean's aspiration plans as it moves to acquire more Scaler customers. Moreover, DO also competes indirectly with Amazon's AWS, Google's Google Compute Engine, and Microsoft's Azure Virtual Machines, which may pose a significant threat should these companies position themselves to directly compete with DO.

While my model suggests marginal upside, I would prefer to wait for a couple of quarters to review the performance of the company's new strategies. Any positive development the company would make during this time period would restore confidence in the company's ability to reclaim its growth rates. For now, this is a Hold.