TomasSereda

TomasSereda

DNOW Inc. (NYSE:DNOW) continued to experience reduced sales, primarily in the Canada segment, due to reduced project spend in the region. However, overall revenue saw 8.7% growth for FY23. The company's near term still appears to be weak due to continued pressure in the U.S. and Canada region, however, strength in the International segment should support the company's revenue growth in FY24.

However, the long term looks promising due to the company's continued focus on capitalizing on increasing projects through higher investment by DNOW's customers over energy evolution. The margin prospect also looks good, as the company continued to look for M&As with higher profitability. The company's stock is currently at an attractive price point, which makes it a decent buying opportunity considering the company's good longer-term prospects.

DNOW Inc. is one of the leading global suppliers and distributors of energy and industrial products. The company’s products and offerings are used across the energy industry in all sectors from upstream drilling and completion, midstream transmission and processing to downstream petroleum refining and petrochemicals. The company provides consumable maintenance, repair, and operating supplies, pipes, valves, fittings, fasteners, gaskets, artificial lifts, and other related offerings. The company mainly operates under three reportable segments based on its geographical presence:

United States

Canada

International

DNOW supplier network consists of thousands of vendors across 40 countries. The company has expanded globally organically and through M&As in countries like Australia, Brazil, Colombia, Egypt, England, India, Indonesia, Netherlands, UAE, and a few others.

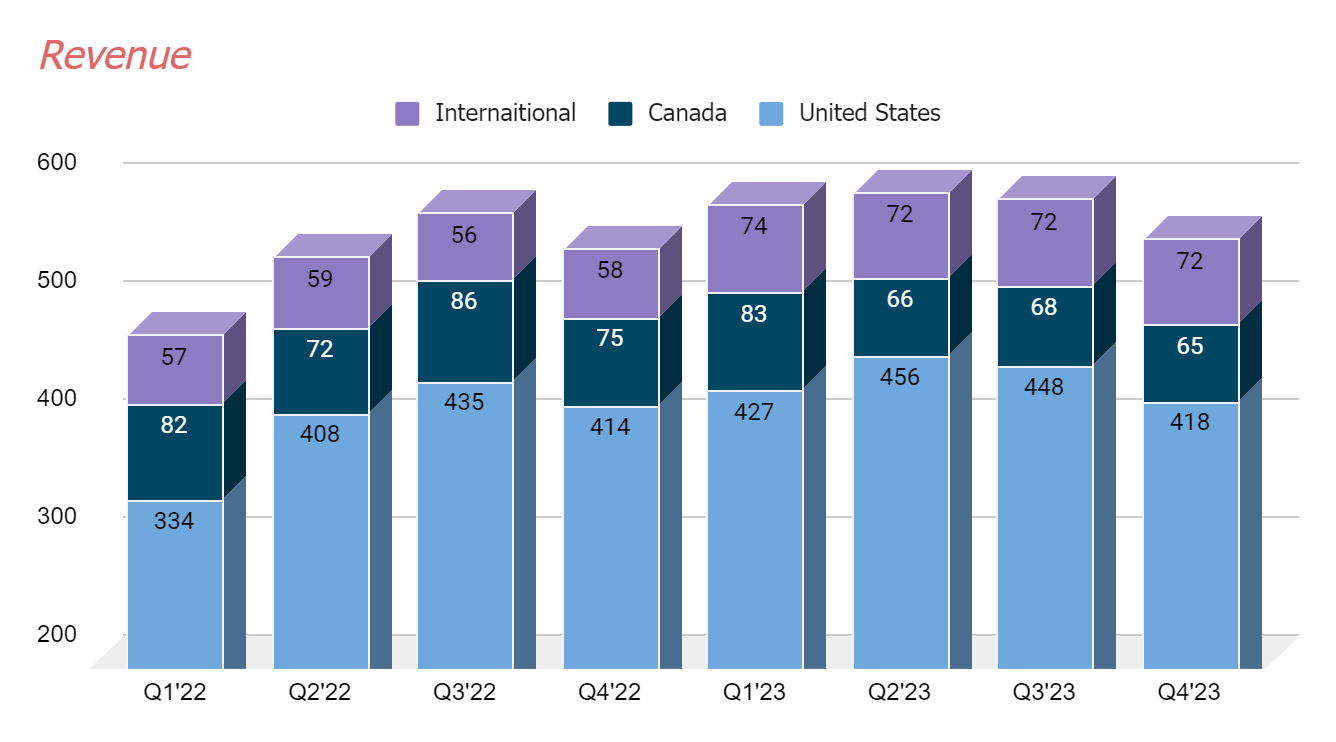

The first half of 2023 was strong for the company’s top line as its topline expanded in double-digits. However, the second half of 2023 experienced weaker growth in the low single digits due to seasonal headwinds in the Canada Segment paired with reduced project spend, which resulted in full-year revenue growth of 8.7% to $2.32 billion in 2023 versus FY22, while Q4’23 was up only 1.5% versus the prior-year quarter.

Segment wise revenue (Research wise)

The United States segment was also weak during the second half of the year again with seasonal impacts with decreased U.S. rig count and decreased U.S. completion by 4% and 8% respectively. However, the segment managed to deliver positive growth in the last quarter, as the company’s model supplying products for workover rig activity was stable during the quarter. The Canada segment, as we talked about earlier, was down 13.3% due to some headwinds during the quarter.

The International segment, on the other hand, was strong throughout the year, delivering topline growth in strong double-digit with 24.1% growth during the last quarter of 2023. The growth was primarily driven by strong project activity in Australia and Kuwait, as well as continued investment in new and alternative energy technologies.

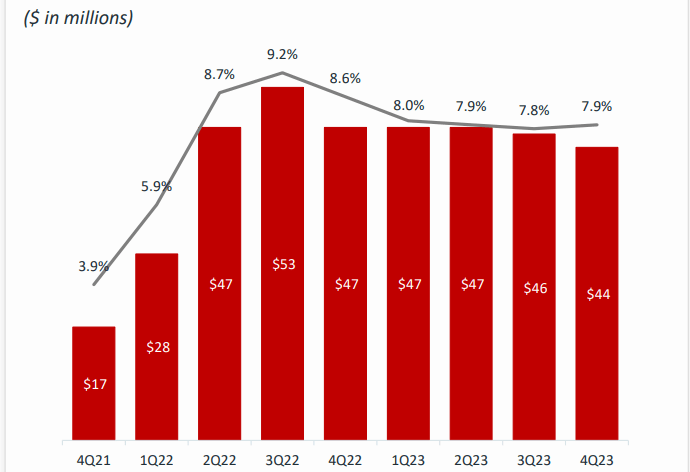

The company’s consolidated adjusted EBITDA margin for Full Year 23 was slightly down by 30 bps to 7.9% as compared to the prior year quarter, however, was near the company’s expectation of 8%. This was due to the negative impact of higher operating expenses and volume deleverage in Canada and the U.S. during the latter half of the year. Overall, the results met the management's expectation of revenue growth between 8%-12% and an EBITDA target of 8% for the full year 2023.

historical EBITDA (Company presentation)

While the International segment looks promising to deliver topline growth in the coming quarters, the continued weakness in both the United States and Canada segments should have a negative impact going forward.

I anticipate that the company's top line should continue to remain under pressure at least for the first half of 2024 due to market headwinds across the U.S. and Canada. In the U.S. segment, customer spending is expected to be allocated just to maintain the current level of production as the customer cuts on their budget as some large (Capital Allocation Companies) CAC companies are announcing modest production growth in the Permian Basin, one of the major oil and gas producing regions. As a result, average rig counts are also declining across all the regions, primarily in the U.S. and Canada regions, which experienced a sequential decline of 4% and 3% in their average rig count respectively, however, are poised to grow in the latter half of 2024, which should support the company’s revenue growth for FY24. Overall, for the near term, I expect that the Company’s revenue growth should be flat or in the low single digits for the Full year 2024.

While topline growth in 2024 is expected to be almost flat, the company’s long-term looks good as the company continues to focus on increasing the number of projects and investments in decarbonization and the renewable fuels market. Under the company’s long-term strategy, DNOW is primarily working towards unlocking new revenue sources as well as developing the existing ones through customers' investment in midstream, energy evolution, and industrial markets including water, mining, and chemical processing, which should benefit the company’s top line in the coming years.

In the current environment of energy evolution, where demand for energy transition products is rising, DNOW is helping its customers decarbonize by eliminating routine flaring and methane by replacing power gas pneumatic devices with industrial-grade compressed grade systems, which should further benefit the company’s business in the coming years.

Apart from this energy evolution landscape, there is also a growth opportunity, particularly in the water infrastructure investment followed by a rising population across the United States and a significant part of the population migrating toward warmer places. Additionally, the mining market also appears to be strong due to continued investment by the company's customers to bring some rare earth elements to the market which are required in certain types of technology and AI applications, which should further drive the company’s top line in the coming years.

While DNOW is well positioned to capitalize on many growth opportunities organically in the coming years, the company remains highly acquisitive and continues to look for quality companies that give value-added solutions and help in end-market diversification while enhancing its earnings. The company also announced its next acquisition of Whitco Supply, which is expected to bring together 2 complementary businesses and help the company expand into the midstream space.

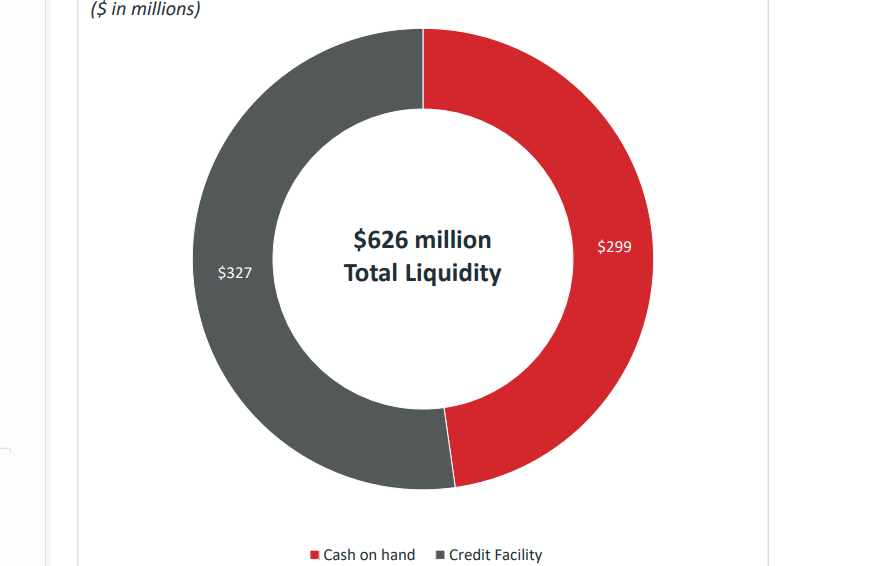

DNOW's liquidity distribution (Company presentation)

The good thing is that DNOW is a zero-debt company, which significantly reduces a company’s financial risk and free cash outflow from the business, which can be used for the company’s strategic acquisition. The company’s liquidity position is strong as well, with total liquidity of $626 million, with about $299 million in cash. The strong financial position of the company should support the company in pursuing accretive acquisition in the future, which should drive the company’s top line as well as profitability in the coming years.

Post the latest earning release, DNOW's stock price has increased more than 23% as the figures in the earning release beat the market estimates. The market was expecting a slight decline in the top line, but it came to a positive 1.5% growth versus the prior-year quarter. EBITDA margin was 7.9% for FY23, also near management estimates of 8%, however, down versus Q4'22.

Currently, the company's stock is trading at a forward P/E ratio of 11.76, based on FY 24 EPS estimates of $1.03. The current valuation appears to be at a significant discount to its five-year average of 42.52. While compared to its sector median, DNOW's stock is also at a discount of about 38.8%. I anticipate the company's top line to be flat or grow in the low single digits. However, in the longer term, the company's revenue should grow, which, along with the company's focus on accretive acquisition with higher profitability, should drive the company's margin expansion in the coming years, which should further improve the company's valuation in the longer term.

The company's EBITDA margin has been strong throughout 2023 despite some headwinds in the U.S. and Canadian markets, which are relatively higher-margin segments. I am anticipating that the company margin should expand in FY24, as these regions are expected to recover in the latter half of 2024. My thesis is also built upon this anticipation of market recovery in these regions. However, if these segments, primarily the Canada segment continue to be under pressure further, the company's overall margin can be impacted which could potentially deteriorate the company's valuation, leading to poor stock performance in the future.

As we discussed, the company's stock is currently trading at a decent discount to its historical average as well as sector median. The company's long-term prospect also looks good as the company continues to work towards growing in decarbonization and renewable fuel markets. Additionally, the company also continues to look for companies for acquisition purpose, that are aligned with the company's focus on end-market diversification while earnings growth, which should support the company's margin growth in the coming years. Considering the promising longer-term prospects of the company, and an attractive valuation, I would recommend a "BUY" rating on this stock.