ktsimage

ktsimage

Ginkgo Bioworks (NYSE:DNA) reported soft results in the fourth quarter of 2023 and gave weak guidance for 2024. While much of this can be attributed to the macro environment, Ginkgo’s business looks nothing like the supposed synthetic biology powerhouse that was expected when the company went public in 2021.

I have been skeptical of Ginkgo's business for a while but felt the company would need time to demonstrate the strength of its business model. There is an increasing number of signs that Ginkgo's business has issues though.

A combination of modest growth, high cash burn and a lack of downstream value creation could further undermine investor confidence in the business in coming years, risking continued share price declines.

Ginkgo recently announced the Ginkgo Technology Network, a partnership program where Ginkgo is integrating the capabilities of a range of companies into its platform to help drive success in customer R&D programs. The network initially contains over 25 partners with capabilities in areas like AI, genetic medicines, biologics and manufacturing. Ginkgo also expects to add new partners over time.

This represents a slight shift in strategy for Ginkgo, and it is not really clear what the company is trying to achieve in my view. The network could be because Ginkgo needs to expand its capabilities to support biopharma companies, but feels it is not feasible to acquire or develop capabilities in all areas.

Ginkgo Bioworks recently announced a number of acquisitions which add to the capabilities of its platform:

These acquisitions support Ginkgo's expansion efforts in biopharma. I would not count on them to meaningfully alter Ginkgo's prospects though.

Ginkgo continues to announce new partnerships across a broad range of areas, including:

Ginkgo has also announced a number of biosecurity partnerships. This includes a collaboration with Illumina (ILMN) to develop biosurveillance technologies. The two companies will work together to demonstrate the use of Illumina products with Concentric’s bioradar.

A number of Ginkgo's past partnerships have also recently reached more conclusive outcomes, both positive and negative.

Light Bio is now selling its bioluminescent petunias in the US with USDA approval. 50,000 plants are available for 29 USD each, with shipping expected in April. Light Bio also continues to work on developing brighter plants, more plant varieties and more colors. While this is all positive, the 50,000 plants only amount to 1.5 million USD revenue for Light Bio, with any potential value accruing to Ginkgo likely minimal.

Synlogic recently decided to discontinue its Synpheny-3 study after initial data indicated the study was unlikely to meet its primary endpoint. Synlogic is now ceasing operations and will reduce its workforce by over 90%, while considering strategic options (acquisition, merger, sales of assets, dissolution, etc.). While this isn’t necessarily a reflection on Ginkgo, it does highlight the risk of relying on downstream value.

Ginkgo’s work with Cronos appears to be progressing steadily from a technical perspective, but the commercial benefits for both Ginkgo and Cronos are less clear. In June 2022, Ginkgo announced the achievement of its third (THCV) out of eight target productivity milestones. Cronos is now selling products containing CBG, CBC and CBN, which presumably means Ginkgo has achieved target productivity for at least 4 molecules, bringing Ginkgo’s Cronos holdings to 8.8 million shares. Cronos currently has a negative enterprise value though, indicating the market has little confidence in the company’s future.

Despite these technical successes, Cronos' recent actions suggest that it is moving away from precision fermentation. Cronos purchased an 84,000 square foot facility in Canada in 2019 to produce cannabinoids through fermentation. In August 2023, Cronos announced that it would be closing the facility. The facility reportedly had around 60 employees, and Cronos expects its closure to save the company 10-15 million USD annually. Cronos will reportedly still supply the market through the use of alternative forms of production and potentially third-party manufacturers.

Cronos has also exited the US CBD market as it tries to reduce cash burn. These developments seemingly suggest that fermentation production costs are high, and that demand is soft.

Ginkgo recently announced a partnership with OneOne Biosciences to develop nitrogen fixation microbial products. Ginkgo will perform assays to test OneOne’s concept and create optimized strains. OneOne is focused on developing a Livepod for nitrogen fixation, potentially a 100 billion USD market.

This project is interesting primarily because it competes directly with Ginkgo’s own nitrogen fixation program, which started with the creation of Joyn Bio in 2017. Ginkgo is probably still at least a few years away from having a product to sell. The company hasn’t given out any information about its nitrogen fixation efforts recently, though.

The existing Haber-Bosch production method is relatively inexpensive, making it difficult to commercialize alternatives. The fact that Gingko is willing to partner on a program competing directly with its own, could mean that the company hasn’t had any success.

Allonnia was launched in 2020 and has already released a microbe solution for removing 1-4 dioxane from water. The company is developing sustainable biological solutions for removing containments, decarbonization and plastics upcycling.

Allonnia has a partnership with EPOC Enviro to commercialize EPOC's Surface Active Foam Fractionation technology in North America. SAFF is used to remove PFAS from contaminated water. Allonnia plans on introducing additive enhancements to SAFF which will help remove target long and short chain compounds from contaminated water.

In July 2023 Allonnia received a 30 million USD investment, with BHP ventures participating in the deal. Allonnia is also working with BHP to purify iron ore using microbes.

Cell engineering is Ginkgo's core business, and while it has been struggling from a revenue perspective, Ginkgo continues to attract new programs. Customers are increasingly coming from the biotech and pharma industries, which is unsurprising given the issues facing Ginkgo's platform strategy. Something that I have previously discussed.

Ginkgo's Cell Engineering business has been progressively shifting towards large pharma and biotech companies, including Pfizer (PFE), Novo Nordisk (NVO), Merck (MRK) and Boehringer Ingelheim:

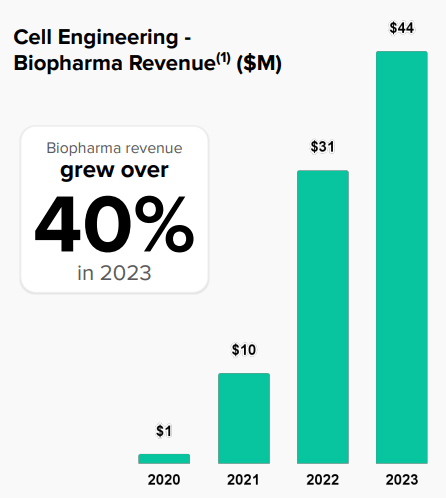

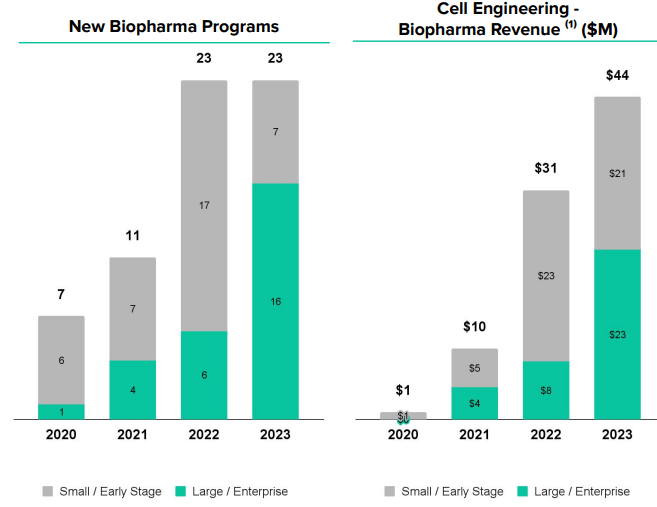

Figure 1: Ginkgo Biopharma Revenue (source: Ginkgo Bioworks) Figure 2: Ginkgo Biopharma Programs (source: Ginkgo Bioworks)

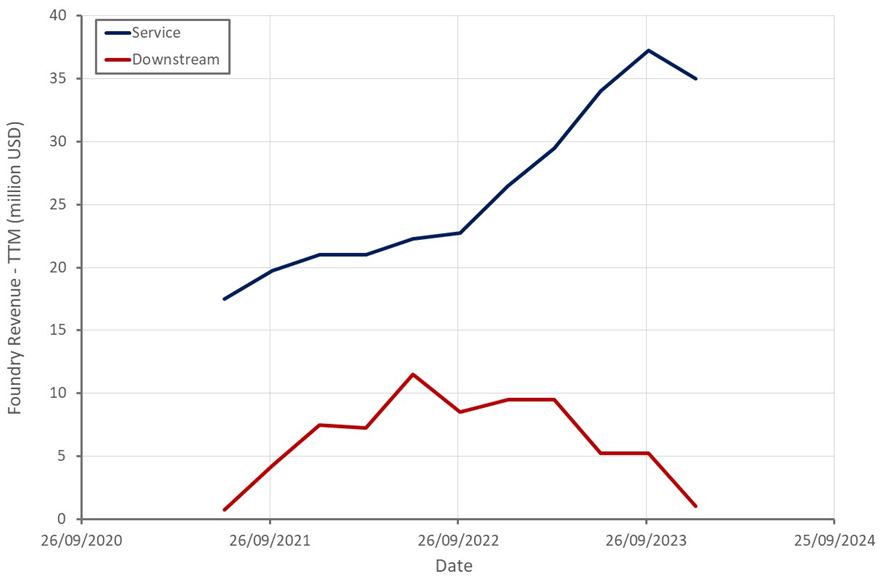

Ginkgo's fourth quarter results were weak, and combined with forward guidance, should be starting to cause investors concern. Ginkgo recognized very little downstream cell engineering revenue in 2023, and cell engineering service growth decelerated throughout the year.

Service revenue was down YoY in the fourth quarter, but Ginkgo suggested that this was more of a timing issue, with underlying activity levels fairly constant QoQ.

Ginkgo expects 100-102 new programs in 2024, which represents a 41% increase YoY at the midpoint. Cell engineering revenue is expected to be 165-185 million USD, up 22% YoY at the midpoint, excluding any potential downstream value. Ginkgo has suggested that downstream value recognition in 2024 could be an order of magnitude higher than any previous year though.

Figure 3: Ginkgo Cell Engineering Revenue (source: Created by author using data from Ginkgo Bioworks)

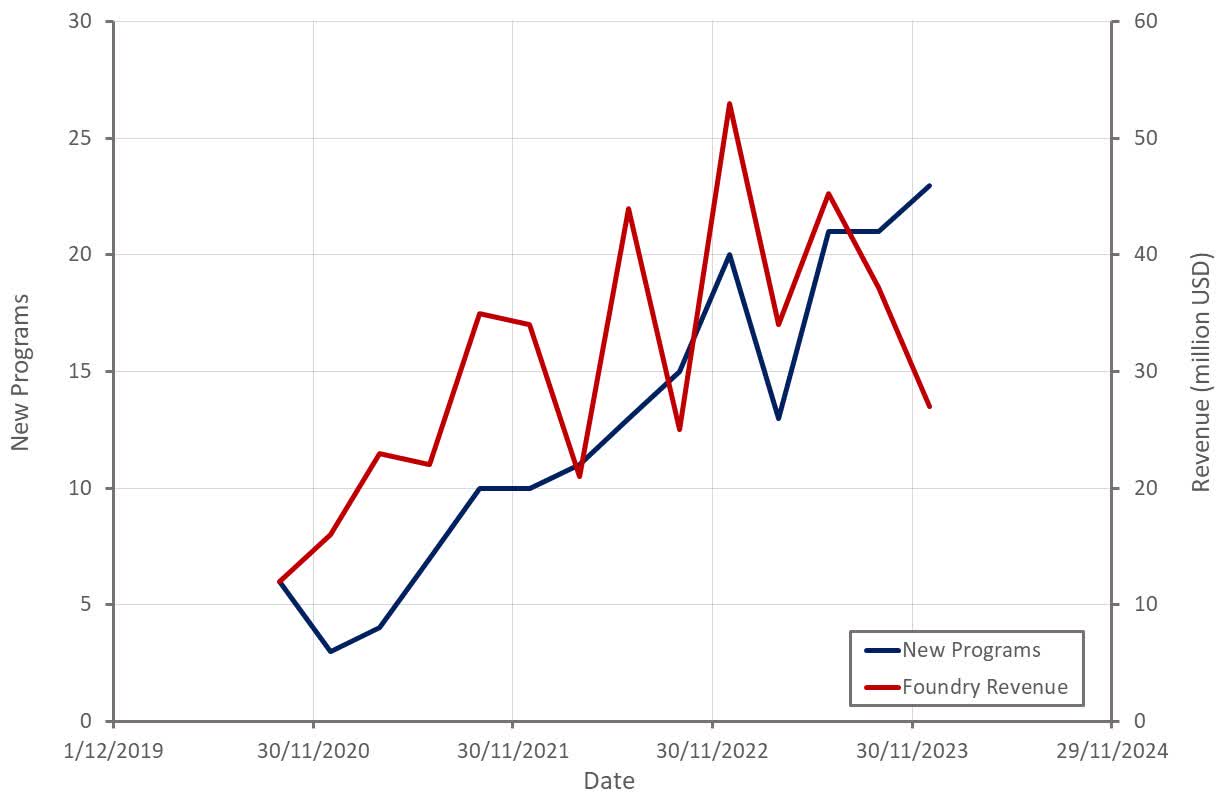

Ginkgo continues to add new programs at an increasing pace, but it is incurring large losses to execute these programs. Downstream value share is supposed to justify this situation, and yet, there has been little evidence of this occurring so far.

Figure 4: Ginkgo New Cell Engineering Programs (source: Created by author using data from Ginkgo Bioworks)

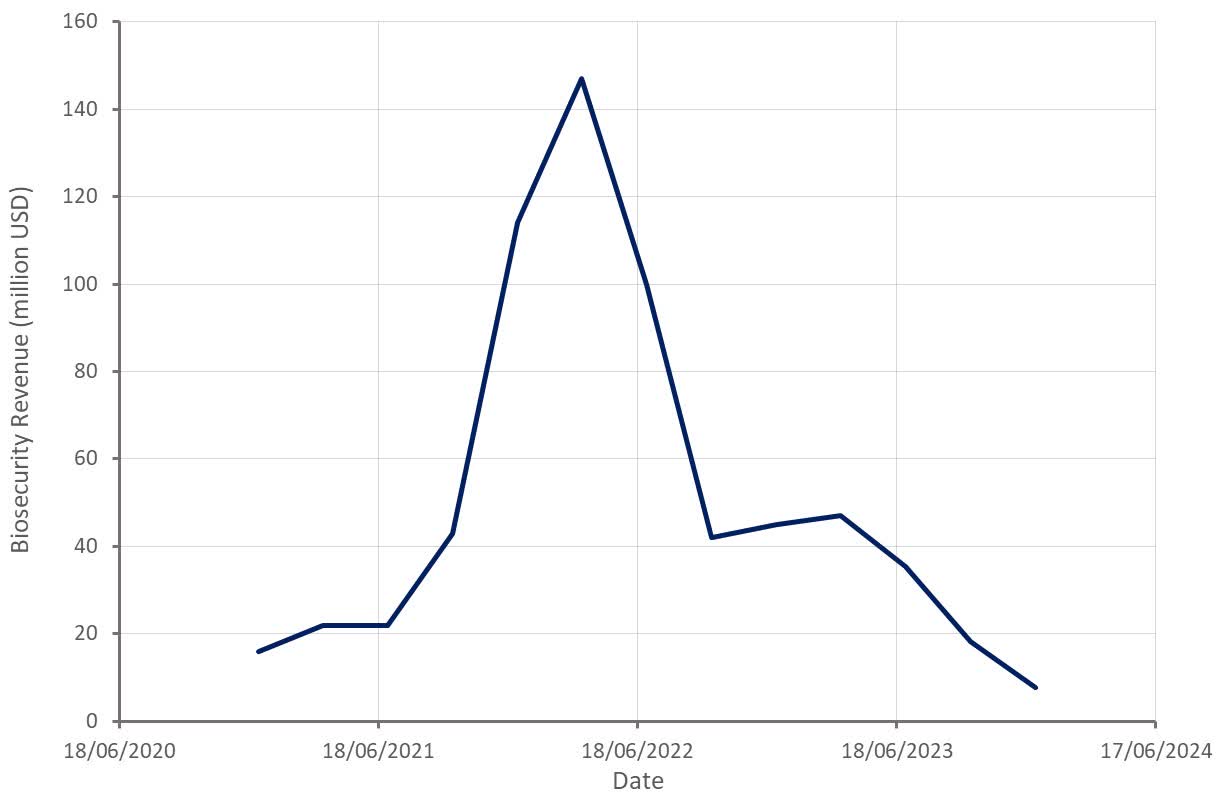

Biosecurity revenue unsurprisingly continues to plummet as COVID testing programs wind down. The biosecurity business generated 8 million USD in the fourth quarter of 2023, with a gross profit margin of only 15%. Biosecurity revenue is expected to be in excess of 50 million USD in 2024, potentially down 54% YoY.

Figure 5: Ginkgo Biosecurity Revenue (source: Created by author using data from Ginkgo Bioworks)

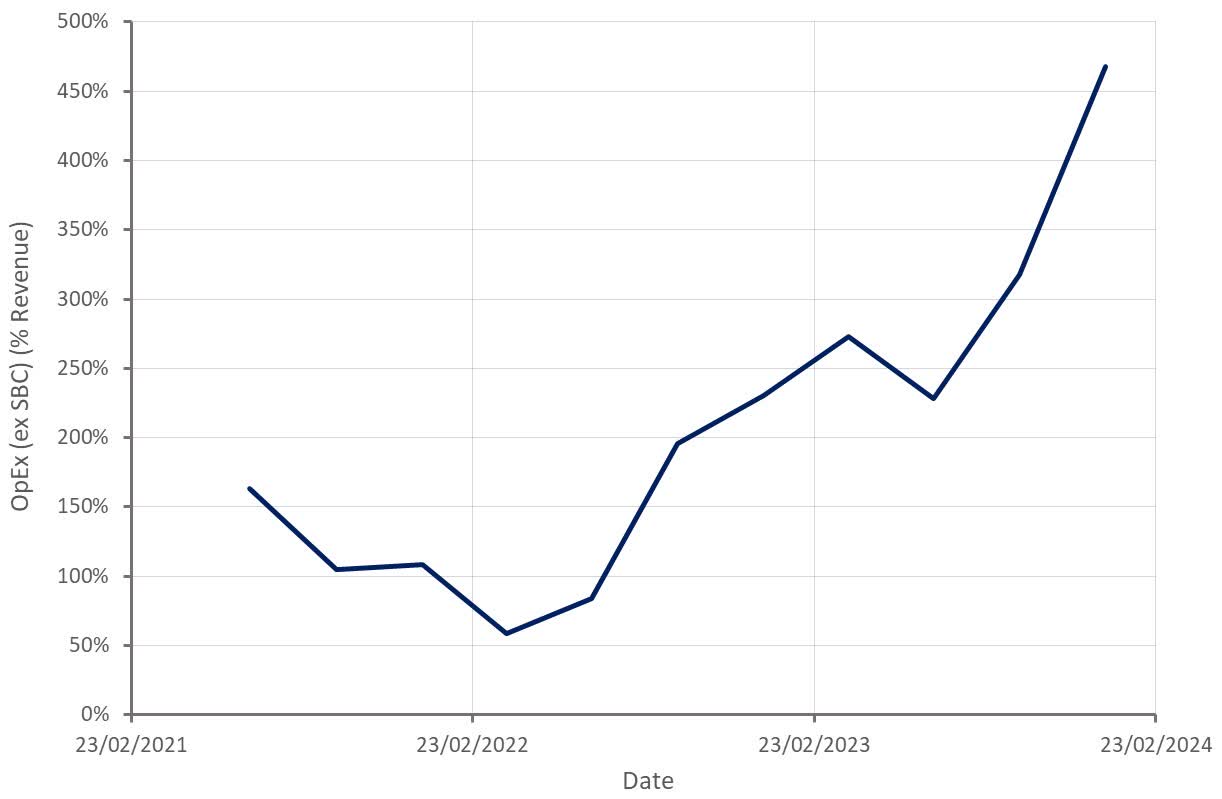

With OpEx remaining elevated in 2023 and revenue falling significantly, Ginkgo's losses have increased dramatically in recent quarters. This is expected to reverse somewhat going forward, with OpEx expected to fall in 2024 and revenue increasing modestly. Absent any large downstream value recognition, Ginkgo's cash losses are likely to remain in the hundreds of millions annually for at least the next few years though.

Figure 6: Ginkgo Operating Expenses (source: Created by author using data from Ginkgo Bioworks)

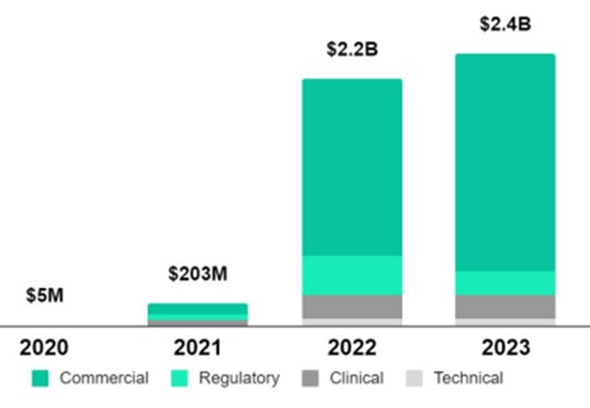

While Ginkgo's financials look extremely poor at the moment, the company's value is supposed to derive from downstream value participation. Ginkgo potentially stands to receive approximately 2.4 billion USD in milestone payments alone. Nearly 1.5 billion USD in potential milestone payments were added in 2023, but just over 1 billion USD in milestone payments were removed due to program cancellations. Little explanation was given for this, although Ginkgo suggested that it primarily came from one customer.

Figure 7: Ginkgo Milestone Pool Opportunity (source: Ginkgo Bioworks)

While Ginkgo continues to build out an interesting technology platform, there are an increasing number of signs that the company is worth far less than many expected. There is little evidence of data and scale driving improved program outcomes at lower cost, and many of Ginkgo's high-profile programs have failed. The company's entire narrative is built around downstream value participation, and yet Ginkgo recognized virtually no downstream value in 2023. Large losses, modest growth and a dwindling cash balance will likely force investors to confront these issues over the next 1-2 years.