Fokusiert

Fokusiert

Sometimes high-yielding funds prove to be only a mirage, driven by financial engineering gimmicks on the part of managers. Other times, especially in the high-yield world, they are truly supported distributions, with Western Asset Mortgage Opportunity Fund Inc. (NYSE:DMO) being such an example. The fund is a fixed income CEF focused on mortgage bonds, which offers a large supported 12% yield.

We covered this name before here, more than a year ago, where we highlighted what is very particular about this fund, namely the fact that it is pursuing a different strategy than most mortgage funds in the market. Most vehicles you see out there, mainly the mREITs such as Annaly (NLY) and equivalent CEFs, purchase AAA Agency MBS bonds and leverage them up to make a spread. DMO, on the other hand, purchases junior and subordinated tranches of MBS bonds, thus taking true credit risk. The main risk factors in this fund are represented by housing prices and borrower defaults, factors which have been extremely resilient despite the recent run-up in mortgage rates.

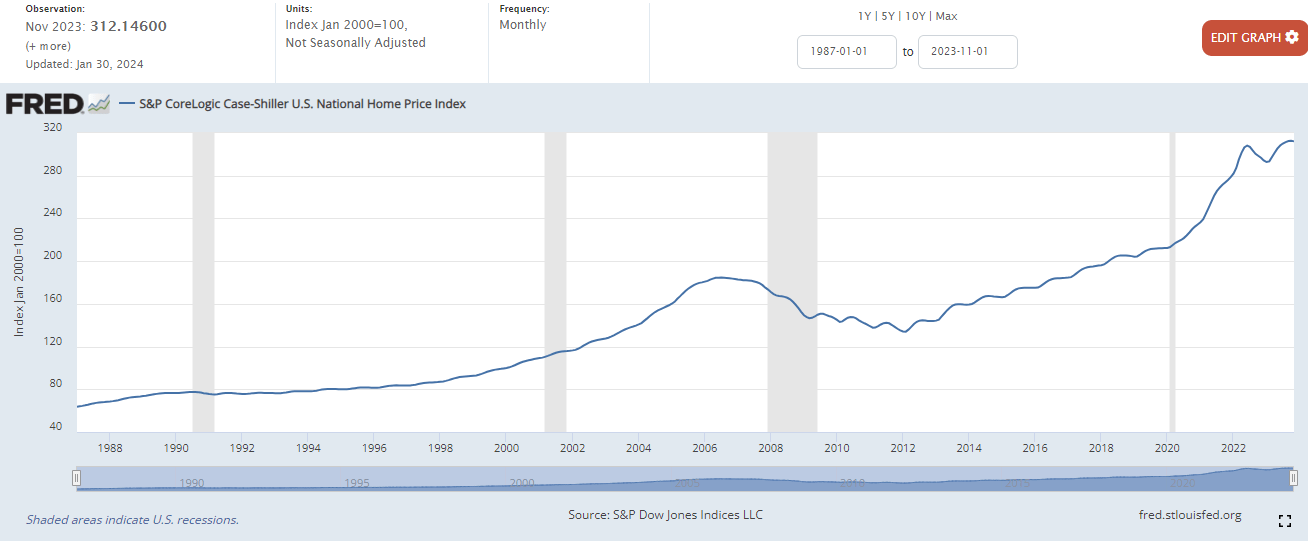

With rates higher for longer, we have seen a very interesting phenomenon. Instead of a housing crash, we are seeing a stuck housing market, with many borrowers who have low mortgage rates unwilling to move or sell given the perceived attractiveness of their mortgages. Although adjustments are taking place in house prices in certain 'hot' markets, we are seeing prices trying to get back to their 2021 levels, rather than crash:

Case-Shiller House Price Index (The Fed)

The Case-Shiller home price index paints that picture, with the housing market far from unwinding its run-up in levels after the 2020 pandemic.

DMO is a unique fund that takes advantage of this dynamic via its collateral composition, collateral which will only get written down on the back of a -40% to -50% housing market price collapse, coupled with borrowers defaults. At this juncture, DMO represents a buying opportunity given its disconnect from traditional corporate credit and the unique set-up of the housing market where a significant shortage of stock coupled with legacy low mortgage rates for homeowners has resulted in an extremely resilient market.

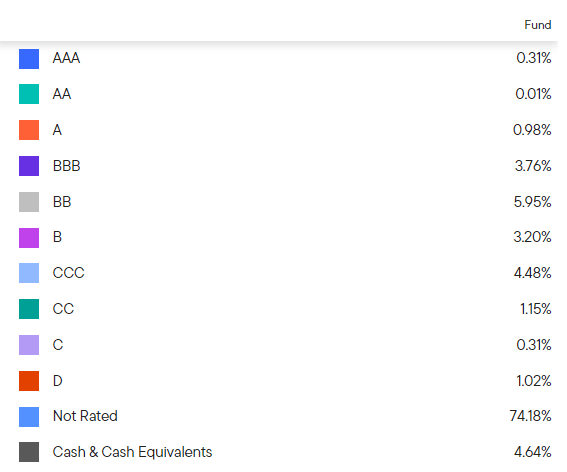

The CEF focuses on junior and subordinated tranches, and thus has a very high 'Not Rated' bucket:

Ratings (Fund Fact Sheet)

In a section below we are going to go into detail through one of the fund's holdings and thus you will be able to better understand the bond features. However, do note that rating agencies often do not rate junior and subordinated MBS bonds due to the many risk factors that can impact their average lives and ultimate recoveries.

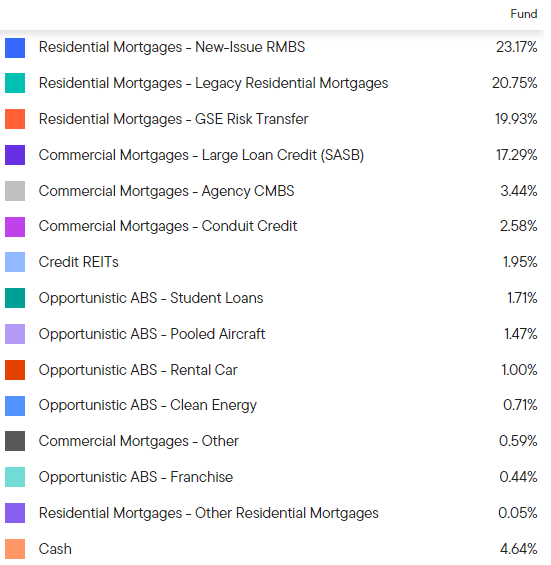

DMO focuses on residential mortgages via its composition:

Composition (Fund Fact Sheet)

We can see new issue, legacy and GSE risk transfer securities making up over 60% of the collateral pool in the CEF.

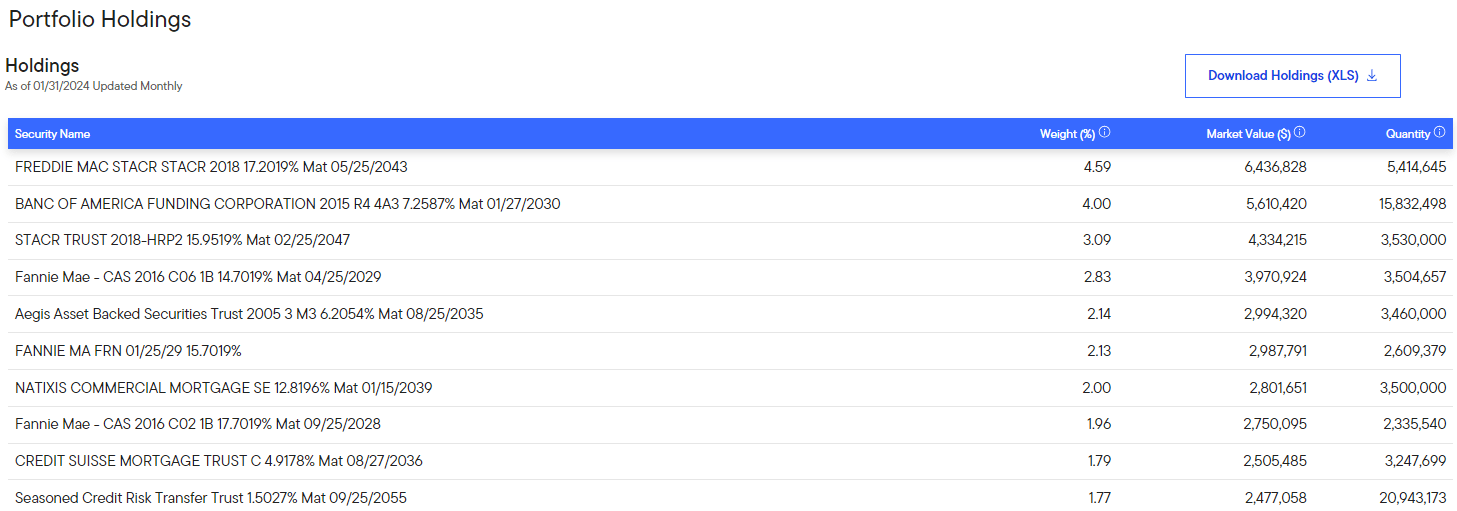

One of the largest holdings in the DMO portfolio is the Freddie Mac STACR 5/25/43 bond, which has the largest weighting in the portfolio:

Top Holdings (Fund Website)

In this section, we are going to do a deeper dive into this bond, so that investors have a better sense of how these securities work, and the risk and rewards associated with such bonds.

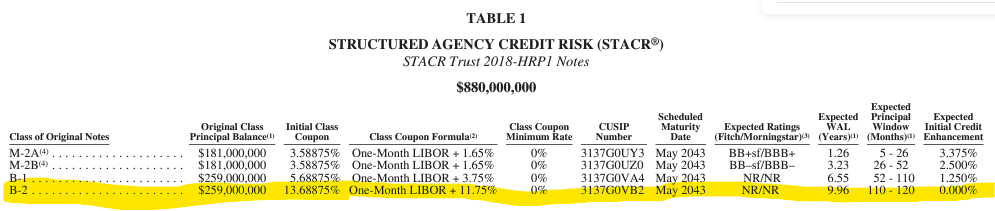

This security was issued in 2018, and its offering documents can be found here. Agencies such as Freddie Mac insure the value of the covered mortgages, and thus are important players in the development of the housing market. However, due to capital reasons, on occasion they sell securities such as the STACR transaction, to cover any potential losses. Such a transaction helps them achieve regulatory capital relief. The transaction structure is as follows, with the highlighted tranche being the one held by DMO:

STACR Capital Structure (Prospectus)

DMO holds the most risky tranche, namely B-2, which pays 1 month Libor (now SOFR) plus 11.79%. Given current SOFR levels, which amounts to over 17% in yield in today's world. As can be noticed from the transaction documents, the B-2 tranche is not rated, being the riskiest in the capital structure. This is a typical example of a bond held by DMO, and thus explains why so much of the fund's collateral is not rated.

Upon the issuance of the transaction, Fitch wrote this in respect to the underlying collateral pool:

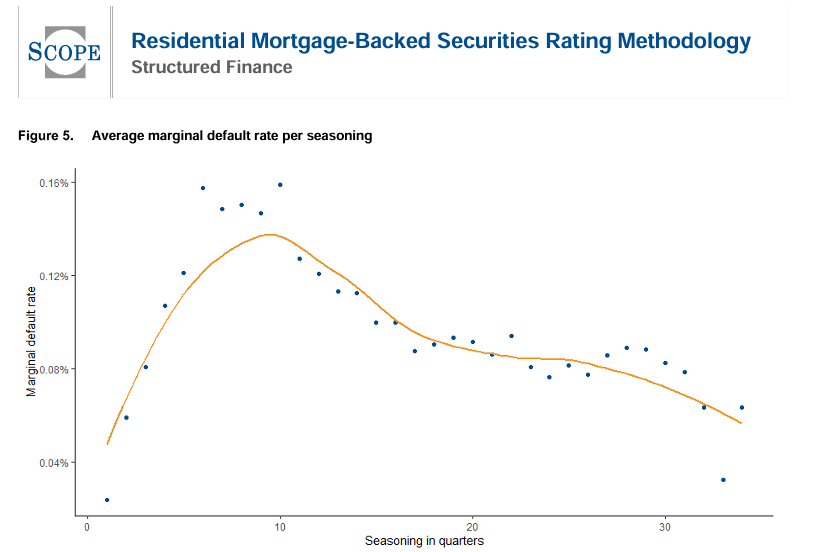

Seasoned Performing Loans (Positive): The reference pool consists of 163,624 fixed-rate, fully amortizing loans with terms of 241-360 months, totaling approximately $29.08 billion, acquired by Freddie Mac between Jan. 1, 2012 and March 31, 2013. The pool is seasoned over five years with a weighted average (WA), non-zero, updated credit score of 745 and a WA original loan-to-value ratio (LTV) of 120%, compared to 98% for STACR-2017-HRP1. Roughly 96% of the pool has been current for the prior 36 months with only 2.5% experiencing a delinquency seven to 24 months ago. The current mark-to-market (MtM) combined loan to value (CLTV) ratio has improved to 85% from 127% at the time of the relief refinance loan.

We are looking at a pool of residential mortgage loans given out to very creditworthy purchasers (FICO of 745), which are very seasoned since they were issued in 2012/2013. 'Seasoning' references the outstanding time for a mortgage. The longer it has been outstanding, the lower the probability of default and the higher the overall recovery. This is fairly simple because equity builds up in the house as time passes by, and the principal balance becomes lower:

Default Rate by Seasoning (SCOPE)

The above table represents an average marginal default rate per seasoning in quarters. We can see default rates rising only in the first 3 years of a mortgage, with the curve then slowly moving down.

So the STACR bond is a home run for the CEF given its ample seasoning, low LTV, and high interest payments of over 17%. The main remaining risk factor here is an absolute and sudden crash in housing values (more than 50% to 60%) across the country. We believe this is not the case, with the housing market stuck because of legacy low rate mortgages outstanding, and a general shortage in housing stock.

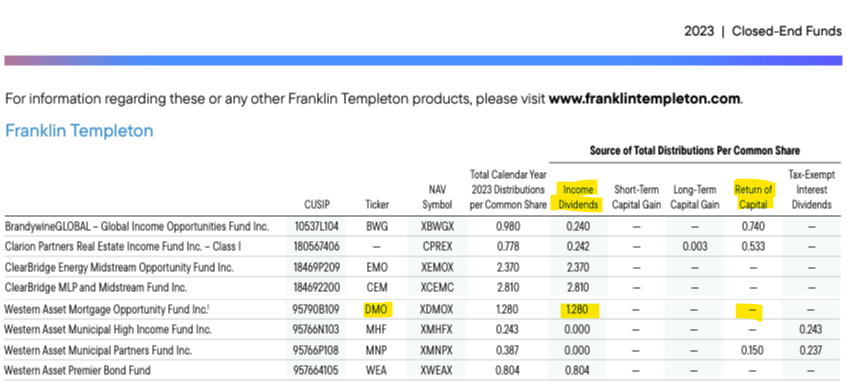

The fund is one of the rare CEFs that fully supports its high dividend:

Distribution (Fund Website)

The reason behind this state of affairs is the floating rate collateral that has adjusted higher as rates have moved up. In fact, as you can see from the Seeking Alpha Dividend History tab, the CEF has increased its dividend in the past year as the realized cash-flows have moved up via rates. While rates have peaked in our opinion, they will not be cut anytime soon, thus providing a great opportunity to be in this fund.

Another attractive trait for this name is its low volatility, as exhibited by its 6% standard deviation and market beta of only 0.5. Rather than pure credit spreads, the CEF is very much impacted by mortgage rates and the mortgage market dynamic, which gives it a unique diversification trait in a high-yield portfolio.

When mortgage rates started climbing in 2022 on the back of the Fed hikes, the market abounded with doom stories on the impeding 'housing crash'. What we got was something completely different, namely a 'stuck' market with very resilient prices. The result has been an increased attractiveness for floating rate GSE Risk Transfer bonds like the Freddie STACR transaction we analyzed, where the risk decreases as time passes by, yet the security is currently paying an eye watering 17% dividend.

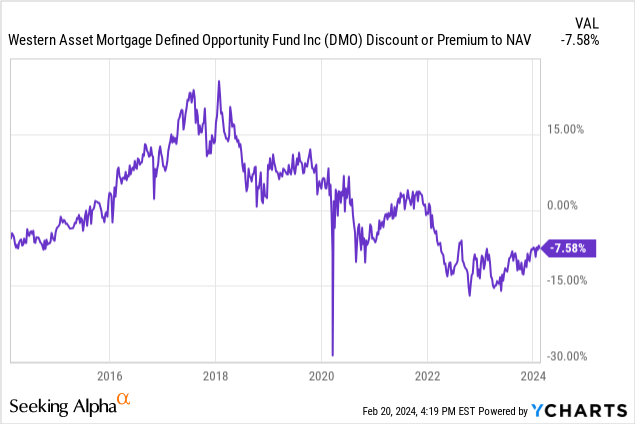

DMO has benefited from the developments in the housing market via a narrower market price vs NAV, yet it remains cheap at a -7% discount:

The fund usually trades flat to NAV or at a premium, and was driven to a very wide discount on the back of fears regarding a housing market collapse. As those fears abate, we will see the CEF move back to flat to NAV, all while collecting a very attractive and fully supported 12% yield.

We are not aware of any other GSE Risk Transfer focused CEFs in the market, with the only other mortgage CEF covered, namely BlackRock Income Trust (BKT) concentrated on the AAA MBS Agency bond trade, rather than junior MBS trances.

The supported high 12% yield looks very appealing in today's environment, especially when traditional credit metrics such as credit spreads are very tight. What is unique about DMO is that it has a high beta to the mortgage market dynamics.

Currently, we are witnessing a very favorable development for DMO in the housing market - rather than a collapse, we are seeing a 'stuck' housing market. With many borrowers having gained access to low rate mortgages in 2020/2021, they are unwilling to sell or move, seeing their mortgage loans as an 'asset' rather than a liability.

While some pockets of the housing market have cooled down, the overall market has been extremely resilient. These factors have translated into lower prepayment rates (thus longer duration for the underlying DMO assets), and very low default rates and losses for junior tranches in Agency risk transfer assets.

Higher for longer translates into DMO's collateral producing a high yield for longer, with little in the market dynamics indicating principal impairments. DMO is not dependent on corporate default rates, thus a deteriorating economy for corporates and consumers will only impact DMO to the extent it coincides with a catastrophic fall of at least -40% in house prices. DMO thus represents a good portfolio diversifier for corporate credit CEF portfolios.

DMO is a mortgage CEF with a supported 12% yield and -7% discount to NAV. Unlike other instruments in the mortgage world, the fund does not invest in AAA Agency securities, but takes true mortgage market credit risk via junior and subordinated MBS tranches. The fund's holdings will be impaired if the housing market falls by -40% to -50% from current levels, and the underlying house buyers default on their mortgages.

The current housing market dynamics are very favorable to DMO, with a 'stuck' market on the back of high mortgage rates and a general unavailability of housing stock. Higher for longer rates are favorable for DMO via its floating rate collateral and lower prepayment speeds for the underlying collateral.

DMO represents a good portfolio diversifier away from corporate credit risk, and today's housing market developments are highly favorable for this fund.