Funtay

Funtay

Dorchester Minerals, L.P. (NASDAQ:DMLP) reported a Q4 2023 distribution that was just over $1 per unit. This was lower than I expected back in November, and appears to be due to various factors including lower sales volumes (compared to Q3 2023) and weaker commodity prices.

Despite the dip in sales volumes compared to Q3 2023, Dorchester is still showing strong year-over-year sales volume growth. Dorchester's Q4 2023 sales volumes were 16% higher than its Q4 2022 sales volumes. Most of this growth appears to be organic growth, with its unit count going up 3% year-over-year to help pay for some acquisitions.

Based on current strip prices, I expect Dorchester to declare distributions of $3.00 to $3.20 per unit related to 2024 results (or $0.75 to $0.80 per quarter).

This would be a bit lower than its 2023 distributions, which added up to $3.52 per unit. However, Dorchester's 2023 distributions were boosted by some large lease transactions.

I am maintaining my estimate of Dorchester's value at $33 per unit, based on long-term $75 WTI oil (CL1:COM) and $3.75 NYMEX gas (NG1:COM). Those prices would support an annual distribution of near $3.30 per unit based on projected 2024 sales volumes, while further growth (beyond the mid-single digit growth from Q4 2023 levels that I've modeled) would increase the distribution.

Dorchester Minerals announced a $1.007874 per unit distribution for Q4 2023. This was somewhat lower than I had expected, given that there were a couple of large lease transactions during the quarter that added approximately $11.8 million (or $0.30 per unit) in lease bonus income. Dorchester reported a total of $12.4 million in lease bonus and other (such as interest) income during the quarter.

Dorchester's Q4 2023 distribution would have been approximately $0.14 per unit lower than its Q3 2023 distribution, excluding the large amount of lease bonus income. This $0.14 per unit difference appears to be due to a combination of lower sales volumes, weaker commodity prices, and timing of cash receipts. About $0.05 per unit of the difference appears to be due to lower sales volumes in Q4 2023 compared to Q3 2023. A similar $0.05 per unit difference appears to be due to the weaker commodity prices. The remainder of the difference appears to be due to timing of cash receipts, which may vary a bit from quarter to quarter.

Dorchester's total sales volumes (in BOE) went down -2% from Q3 2023 to Q4 2023, while its oil sales volumes went down by -5% over that period. However, Dorchester's year-over-year sales volume growth was strong. Dorchester's total sales volumes went up +16% from Q4 2022 to Q4 2023, while its oil sales volumes went up +15% over that period.

Most of that growth appears to be organic. Dorchester did make a number of acquisitions that it paid for with common units, but its common unit count has only increased by 3% year-over-year. This is much less than its sales volume growth.

| Q4 2022 | Q1 2022 | Q2 2023 | Q3 2023 | Q4 2023 | |

| Royalty natural gas sales (mmcf) | 1,078 | 1,330 | 1,153 | 1,344 | 1,283 |

| Royalty oil sales (mbbls) | 319 | 302 | 335 | 477 | 404 |

| NPI natural gas sales (mmcf) | 495 | 864 | 475 | 412 | 550 |

| NPI oil sales (mbbls) | 185 | 269 | 158 | 135 | 178 |

As noted above, Dorchester's sales volumes per unit increased by double-digits in Q4 2023 compared to Q4 2022. I am going to assume that Dorchester's sales volumes per unit in 2024 average mid-single digits above Q4 2023 levels.

At current strip prices (including nearly $77 WTI oil and $2.50 NYMEX gas) and the aforementioned growth in sales volumes per unit, I estimate that Dorchester can pay out around $0.75 to $0.80 per unit in distributions per quarter. This assumes that there are no very large lease bonus payments during 2024 and that the lease bonus payments are under $1 million per quarter on average.

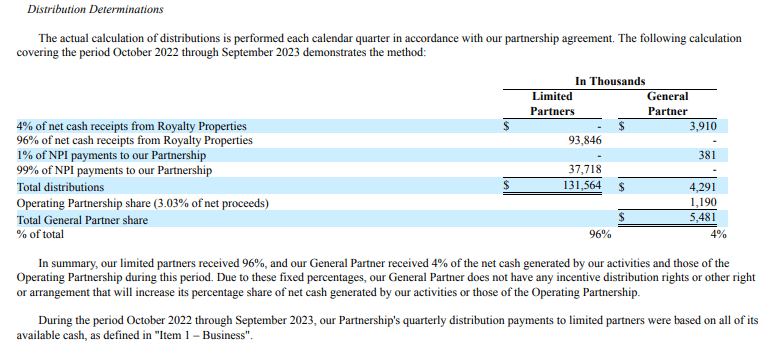

In general, Dorchester's limited partners receive 96% of the net cash generated by Dorchester's activities, while the General Partner receives the other 4%.

Dorchester's Distribution Determinations (dmlp.net (2023 10-K))

I am keeping my estimate of Dorchester's value at $33 per unit at longer-term (after 2024) $75 WTI oil and $3.75 NYMEX gas. Dorchester's yield (with $0.75 to $0.80 per unit in quarterly distributions for 2024) would be approximately 9% to 10%.

The current strip for 2024 involves slightly higher oil prices and markedly lower natural gas prices compared to my long-term commodity prices. Dorchester's quarterly distribution using projected 2024 sales volumes and $75 WTI oil and $3.75 NYMEX gas would be around $0.03 per unit higher than the 2024 projections.

Dorchester's sales volumes dipped a bit in Q4 2023 compared to Q3 2023. However, Dorchester's sales volumes also were up around +16% in Q4 2023 compared to Q4 2022. While there is some quarter-to-quarter variability in sales volumes, the longer-term trend appears to involve sales volume growth that significantly outpaces the growth in Dorchester's outstanding common units.

I am currently modeling a mid-single digit increase in sales volumes for 2024 compared to Q4 2023 levels. At current strip prices, this would result in Dorchester averaging $0.75 to $0.80 per unit in quarterly distributions in 2024, without the benefit of any major ($1+ million) lease bonus payments.

This would be a roughly 10% forward yield based on Dorchester's current unit price. I am maintaining a $33 per unit estimated value for Dorchester (based on longer-term $75 WTI oil and $3.75 NYMEX gas). When combined with the expected distribution over the next year, this would imply a roughly 16% total return for Dorchester, so I am maintaining a buy rating on it at its current price.