FreshSplash

FreshSplash

The holiday earnings season for retailers is nearly wrapped up, with most having reported results from mid-February through mid-March.

The current earnings season brought generally better-than-feared results for most reporting, though many continue to be bogged down by declining sales.

In some cases, investors have been willing to overlook a weaker revenue outlook in favor of expanding profitability. And looking ahead, many retailers may gain a topline reprieve with favorable prospects for lower interests and declining inflationary pressures.

As the reporting period concludes, here’s a roundup from the key retailers who have reported thus far.

The quarterly retailer-specific earnings season mostly tied to the final fiscal quarter of 2023 kicked off in earnest in mid-February with the release of results from home improvement retailer, Home Depot (HD), as well as from Walmart (WMT). The initial reports from these bellwethers were then followed by results from HD’s lead competitor, Lowe’s (LOW) towards the end of February.

After Macy’s (M) tone-setting report in the Broadline Retail group and TJX Companies’ (TJX) charge in off-price retail, a deluge of reports rolled in through the first half of March. Notable results that followed included electronics retailer Best Buy (BBY).

The trading week of March 4 then provided investors with a powerhouse lineup of retail results from the likes of Target (TGT), Foot Locker (FL), and Costco (COST), to name a few. More under-the-radar plays such as Abercrombie (ANF) were also included in the mix. One should also not overlook the results of mall-based and department store names such as Nordstrom (JWN), Victoria’s Secret (VSCO), and Kohl’s (KSS).

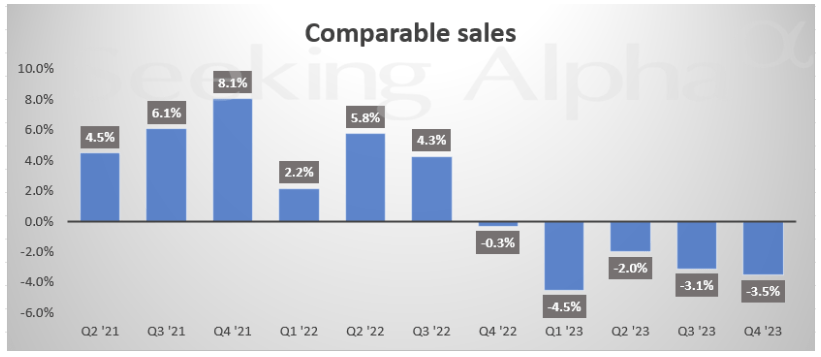

It was a mixed bag for some of the early reporters. The two primary home improvement retailers both reported disappointing comparable sales figures. HD reported a decline of 3.5%, its fifth straight quarter in the red. Lowe’s fared worse with a decline of 7.4%. The forward outlook was also not all that promising for either. HD guided for a 1% decline in comparable sales in FY24, while LOW saw the same metric down in the range of 2% to 3% for its full fiscal year.

Seeking Alpha - Quarterly Chart Of Comparable Sales Growth For HD Stock

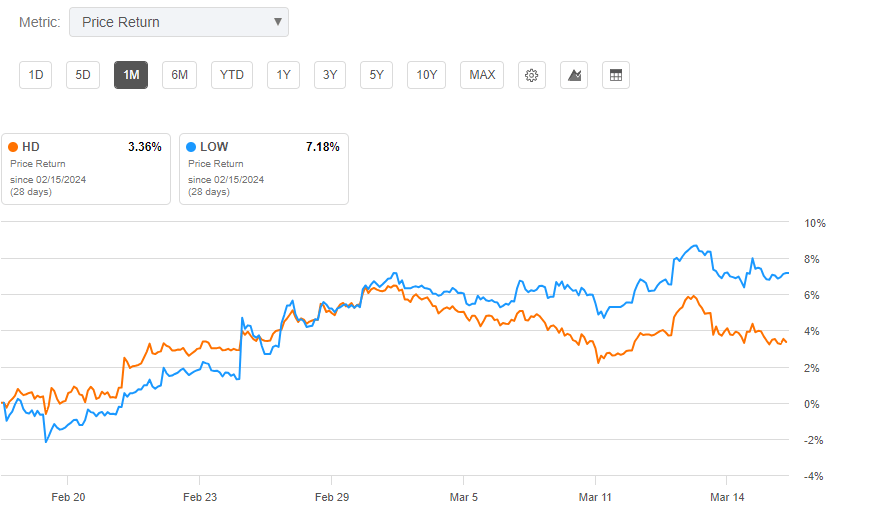

Despite initial dips following results, both home improvement retailers have remained in the positive over the past month, with HD up about 3.5% to LOW’s 7%, each ahead of the broader S&P’s (SP500) 2.2% gain in the same period.

Seeking Alpha - 1M Return Of HD And LOW Stock

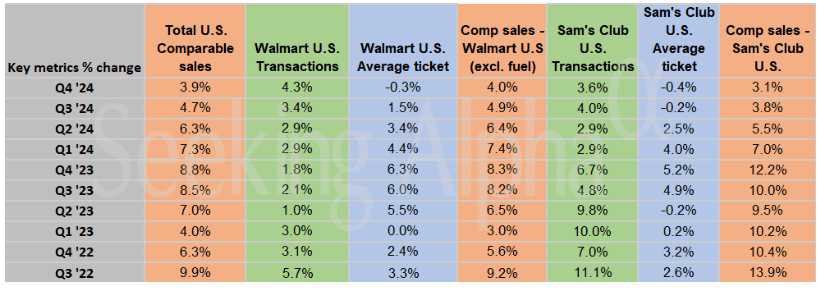

Walmart shined where the home improvement retailers didn’t. In their holiday quarter, WMT reported comparable sales growth of 4%, over 120 basis points above consensus estimates. The gains came even as average tickets declined 0.3%. These declines were offset by a 4.3% increase in transactions as eCommerce and holiday-based traffic gained throughout the quarter.

Seeking Alpha - Topline Sales Metrics By Quarter For WMT Stock

Positive holiday toppers were generally the theme as the prints rolled in from various retailers. In some cases, results came in much better than feared. This was the case with Macy’s as the department store operator reported a sales decline of 1.7%. While still a decline, it was +$30M better than estimates. Investors also cheered rising margins as quarterly gross margins rose 340 basis points to 37.5%.

Improving profitability was the main theme at Target as well. The company reported an operating margin rate of 5.8% compared to 3.7% in the same period last year. The gains at the operating level were driven principally by a 290 basis point improvement in the gross margin rate. While declining sales remains a concern, investors have been willing to overlook the trend in favor of the stronger earnings potential. Recently, the stock hit a new 52-week high as more have become bullish on the company’s forward prospects.

Others trading in the upper-end of the annual price range include off-price retailer, TJX. Over the past year, the company has been a winner in an era of higher prices and financing rates. The company continued to prove its worth in the holiday quarter, with another comparable sales beat. TJX also increased their buyback program. The outperformance of TJX follows a bullish article I wrote in mid-2023, where I cited TJX as the retailer most likely to gain the most during a period of consumer trade down.

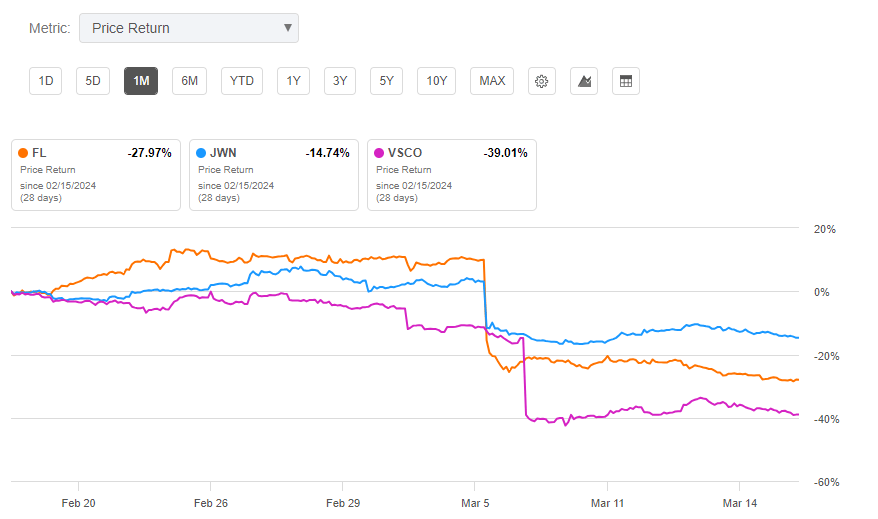

Fortunes were less promising for many other retailers. This includes Foot Locker, Nordstrom, and Victoria’s Secret, who all posted double-digit percentage declines following mediocre results which were paired with disappointing forward guidance.

Seeking Alpha - 1M Returns Of FL, JWN, And VSCO Stock

Likewise, investors were generally apathetic to results from market shocker, Abercrombie, which is up a meteoric 370% over the last year but pulled back some despite impressive quarterly results. The pullback could have been attributable to some investors cashing in on the stock’s outsized returns. Results from Kohl’s and widely-followed Costco were similarly neutral in the eyes of most investors.

In prior periods, I’ve consistently favored off-price retailers as winners for the current market environment. While I remain positive on the outlook, I view shares as fairly valued for the retailer worth the most attention, TJX. Currently, TJX commands a forward multiple of nearly 24x earnings and is trading at the top end of its 52-week range, with a hold assessment from Seeking Alpha’s quant scoring system. While consensus Wall Street estimates see 13% remaining upside potential in the stock, I believe shares are more likely to trade in a tight range in the coming months.

The prospects of lower interest rates in conjunction with continuing strength in the labor market may bode well for the more discretionary retailers; Target is one such example of a company attracting increased attention. Foot Locker could also benefit from an improved inventory position, as well as new initiatives in the growth market of India.

At this moment, however, I am most bullish on the dollar store retailers; specifically, Dollar Tree (DLTR). In advance of its Q4 results, I provided bullish commentary supported in part by its earnings potential and expanding customer base. Shares, nevertheless, were pummeled after it missed expectations and provided underwhelming guidance. The company also announced that it was closing nearly 1,000 of its Family Dollar stores.

Despite investor disappointment in the stock, I remain bullish. CEO Rick Dreiling has guided for $10/share in EPS by 2026, and the company is well on its way to getting there through its current turnaround efforts. The store closures may also support SG&A leverage in the periods ahead, especially considering DLTR’s Family Dollar chain has been an underperformer over the years.

At a 20X multiple of anticipated 2026 EPS, DLTR would be valued at $200/share or about 60% above current trading levels.

Investors seeking more diversified exposure could also opt for the SPDR S&P Retail ETF (NYSEARCA:XRT). The ETF includes the dollar stores among its holdings. It also includes top performing names, such as Abercrombie. The stock, however, may have already run its course, with yearly gains of over 20%, including 5% YTD.

As a supplement to retail stocks with upside potential are those providing an attractive quarterly dividend payout. Two notable names worthy of your attention are Best Buy and Kohl’s.

For 13 consecutive years, Best Buy has increased their annual dividend payout. And over the last five years, the company has increased it at a compound growth rate of over 15%. The consistent rate of growth provides an offset to the annualized yield, which presently stands at around 4.8%. While that would have been attractive in a lower rate environment, comparable risk-free alternatives provide about the same yield to investors seeking less risk exposure.

For those seeking yield, Kohl’s payout is currently yielding over 8%. The management team has also reaffirmed their commitment to the payout in recent earnings commentary. The company’s financials also support the optimistic take by management. The payout ratio, for example, hovers around 70%. Though above sector averages, it still indicates adequate coverage from current earnings.

The holiday season afforded most retailers the best chance of turning in a better than expected print to investors. Names such as Walmart and TJX lived up to expectations, with strong results at the topline. The continued sales strength also reflects consumers continued desire for value in a period of rising prices and higher interest rates.

One would have expected the dollar stores to share in success with their value-based peers. But the two major players, Dollar General (DG) and Dollar Tree failed to live up to the hype. The latter suffered a more pronounced defeat at the hands of pessimistic investors. In my view, I believe the selloff was overdone.

Other department store and apparel retailers such as Foot Locker, Nordstrom, and Victoria’s Secret posted results that were not wildly out of line with expectations. Investors, however, showed disappointment in forward guidance that continued to show flat or declining sales.

Selective retail stocks remain a good investment, in my view. The consumer desire for value will likely remain higher for longer even in the face of rising prospects of lower inflation and interest rates. This should benefit off-price retailers such as TJX, as well those with greater offerings of value-oriented products; Walmart, for example.

Investors are also rewarding those with improved outlooks on profitability. Target has been the most notable beneficiary thus far. But on this, it’s likely much of the optimism is already baked into share prices. A pull forward effect from a highly accommodative freight environment may also pose a comparative headwind in the new fiscal year.

Diversified exposure via the XRT may remain a positive bet for investors seeking to capitalize on generally positive retail data. But in my view, the Dollar Stores currently present the most attractive risk/reward proposition. Dollar Tree, specifically, is best suited, given its ongoing turnaround efforts and realistic path to double-digit EPS.

Overall, In my view retailers with value-based offerings remain promising investments for investors, while the dollar stores offer the most bang for investment dollar.