Sergio Delle Vedove/iStock Editorial via Getty Images

Sergio Delle Vedove/iStock Editorial via Getty Images

Investors can be forgiven if they hear about Nippon Telegraph And Telephone Corporation (OTCPK:NTTYY) and think it is an obsolete company not worth their time researching. While it's true that it is perhaps time to drop the word "Telegraph" from its name, and perhaps "Telephone" too while they are it, this is a company that is far from obsolete.

It owns one of the leading mobile operators in the world, with excellent 5G coverage, and it is one of the most important data center operators globally. In fact, it is widely recognized as the third largest data center operator in the world, only behind Equinix (EQIX) and Digital Realty (DLR). We believe this gives investors a great opportunity to gain exposure to this attractive industry while offering a valuation multiple closer to that of AT&T (T) or Verizon Communications (VZ).

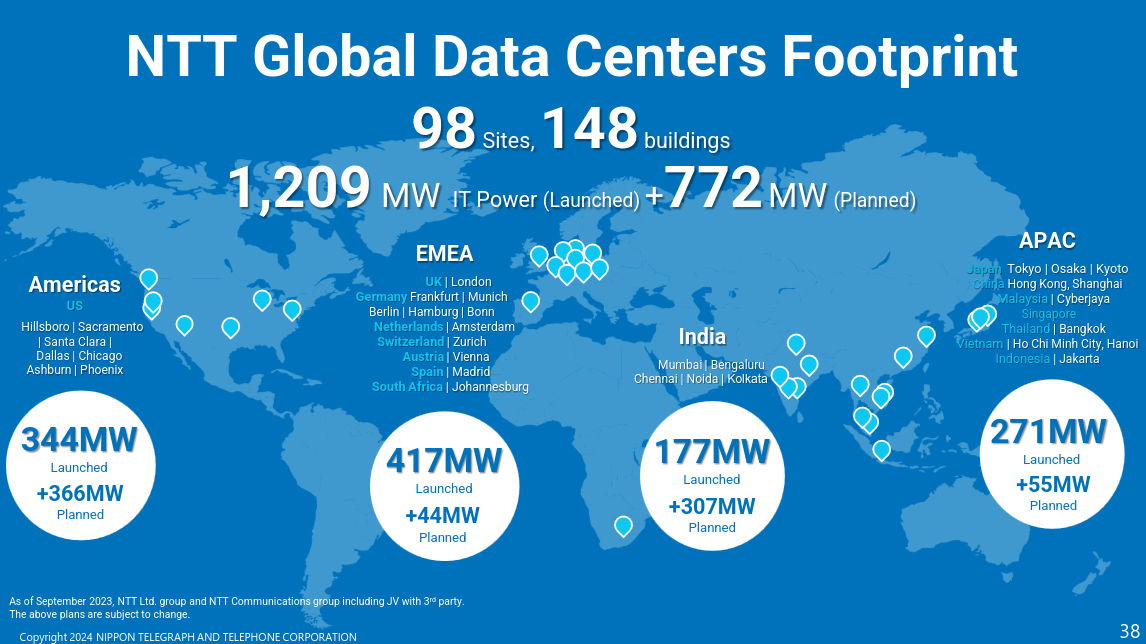

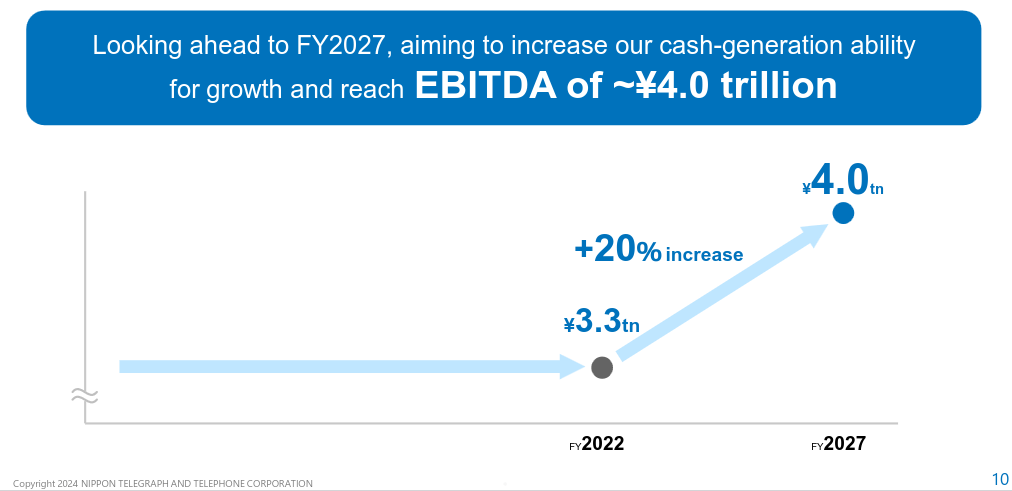

In fact, the data center business is seen by the company as its main growth engine. It plans to increase EBITDA by 20% over the next few years to ¥4 trillion by fiscal 2027 (roughly $27 billion USD). A significant contributor is expected to be growth in the data center business. Key data center markets are showing high demand and rising lease rates, and demand from Generative AI is expected to further increase current projections. While the mobile phone and broadband internet businesses derive most of their revenues from Japan, the data center business is truly global. For example, NTT has the largest market share in India and has a large footprint in Europe and the U.S. The company has already warned there will be an uptick in capex, as NTT sees insatiable customer demand. NTT has already committed to invest ¥1.5 trillion into data centers by 2027, and it is planning to do this while paying close attention to sustainability, as it has a target of 100% renewable energy use by 2030.

While data centers are becoming an increasingly important part of the business, and perhaps the main growth engine, the mobile phone business continues to deliver most of the profits. This subsidiary is called NTT DOCOMO, officially an abbreviation of the phrase, "do communications over the mobile network", and it is also a play on the word "doko mo", which means "everywhere" in Japanese.

This is a massive business with more than 89 million customers in Japan (~41% market share), making it one of the world's largest mobile communications operators. It is also still growing, as it gained almost 5 million customers compared to the previous year. There is significant competition, with three major operators including NTT DOCOMO, SoftBank Corp. (OTCPK:SOBKY), and KDDI (OTCPK:KDDIY). NTT DOCOMO is known to have excellent coverage and very fast 5G performance. NTT consolidated NTT DOCOMO in 2021 aiming to extract synergies and improve overall operational efficiency.

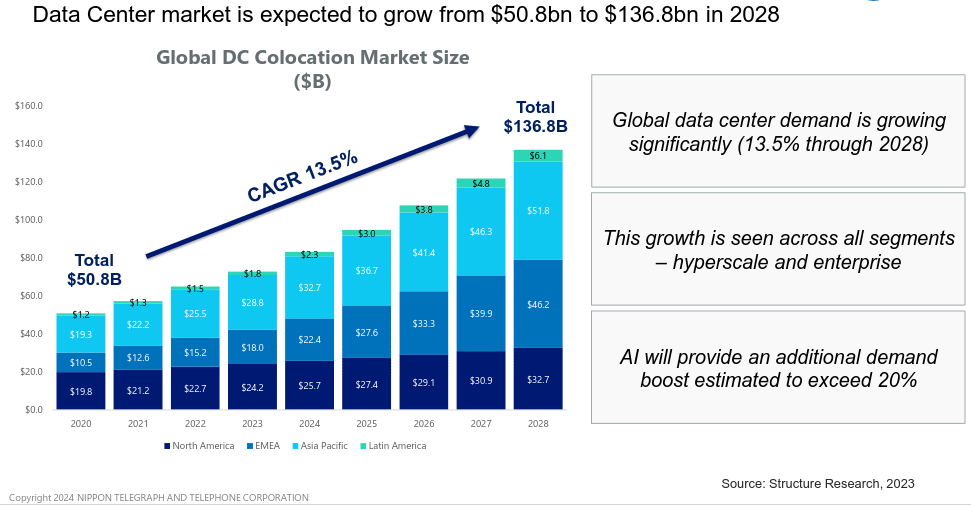

We have already discussed the data center opportunity for NTT, but let's go into more detail. The company has the capital to heavily invest in what is expected to be a growth market going from roughly $50 billion globally today, to $136 billion in 2028, or a ~13.5% CAGR according to the company based on a 2023 Structure Research report.

This could even be underestimated, as analysts are adjusting their expectations given the additional demand boost that AI could create. With a very tight data center supply, all of this is helping create favorable pricing and absorption trends.

NTT Investor Presentation

Importantly, the company is not following a build and see if the customer shows up approach. Instead, it is working closely with its customers, and it has shared that bookings now exceed installed capacity, as the prevalence of pre-lets has significantly increased. The healthy bookings backlog gives the company a line of sight on future revenues and de-risks the development program. Its occupancy is already trending past 96%, which is higher when compared to its peer group. Interestingly, the average EV/EBITDA valuation multiple for its public data center peer group is currently around 20x.

NTT Investor Presentation

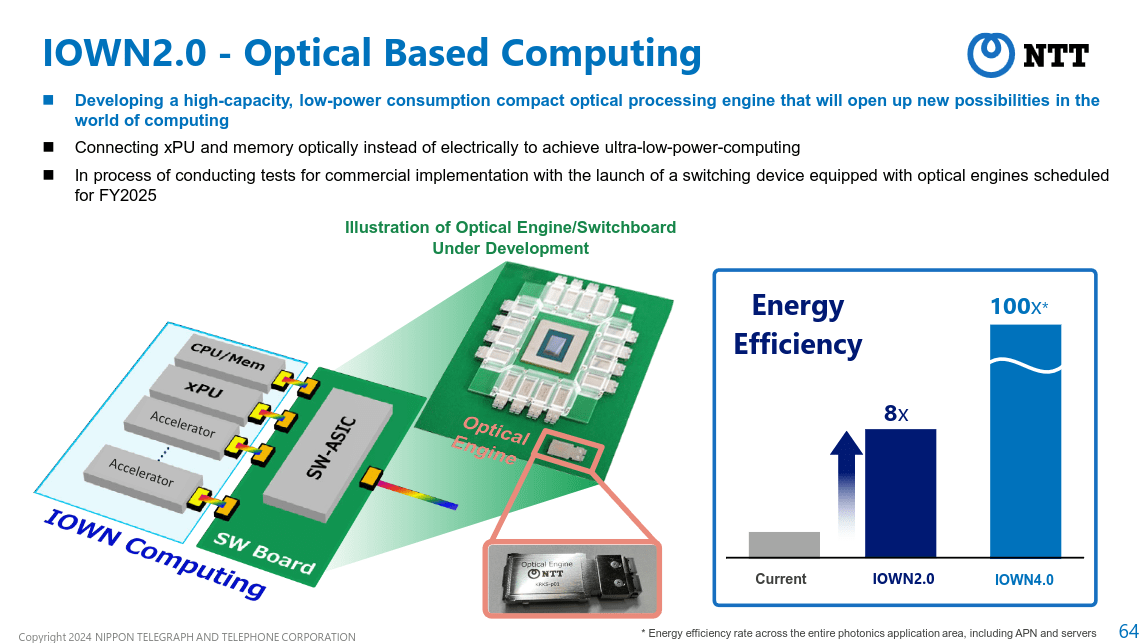

The company has developed significant technical and operational know-how to develop and operate these data centers. It is going even beyond, by investing in foundational R&D that can make them significantly more efficient. For example, it is working to rapidly commercialize photonic-electronic convergence devices that achieve low power consumption. It was recently reported that Intel (INTC), South Korea's SK Hynix, and NTT are teaming up to develop optical chips. Japan plans to provide a ~$300M subsidy to companies working on using light to speed up data transmission and reduce IT power consumption. This technology should also help make it possible to use multiple data centers as if they were a single data center.

NTT Investor Presentation

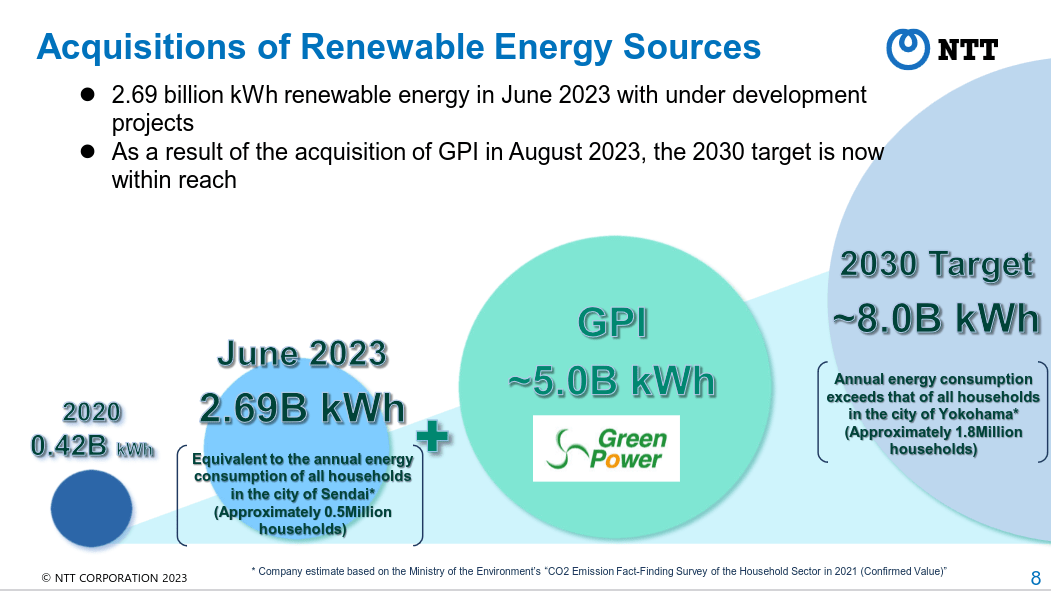

At the same time that it is looking for new technologies to reduce data center energy consumption, it is looking to expand renewable energy generation. Both for its own operations, as well as to supply customers and even governments.

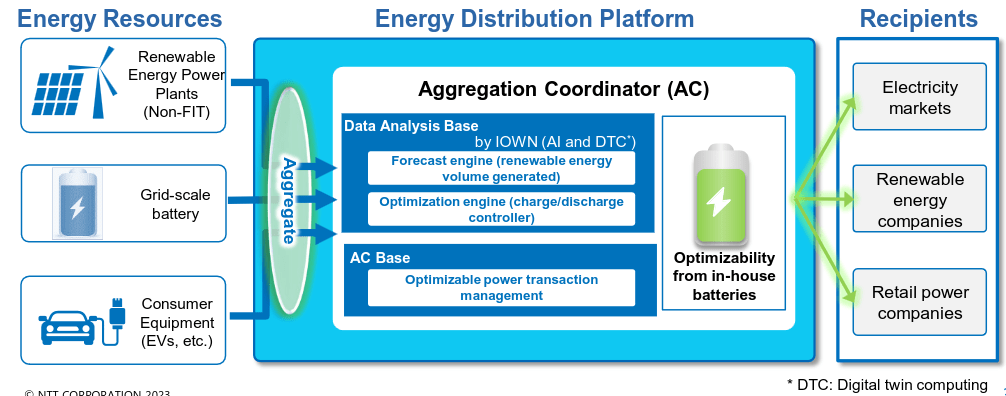

NTT is also developing advanced forecasting technologies to estimate power generation, energy demand, and be able to make adjustments accordingly. Other technologies it is developing include drone surveying of solar panels and wind turbines.

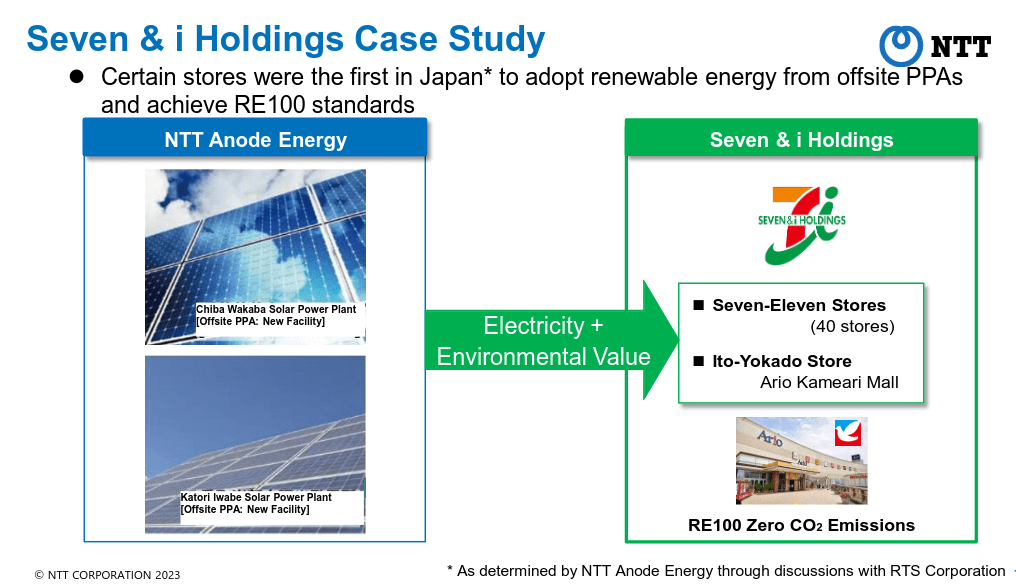

It calls its energy business NTT Anode Energy, and it aims to offer several different clean energy solutions for companies and even local governments. This can be particularly attractive for companies looking for long-term electricity contracts that would reduce the risk of a sudden rise in electricity prices. They would also benefit from the added sustainability benefits. One case study NTT shared was the work they did with one of the largest convenience store chains in Japan, Seven & i (OTCPK:SVNDY), where they supplied clean electricity to roughly forty stores.

NTT Investor Presentation

This clean energy solutions business is targeting ¥1 trillion (~$6.7 billion) in revenue by 2030. To accelerate their vision they acquired Tokyo-based Green Power Investment for approximately ¥300 billion (~$2.18 billion).

NTT Investor Presentation

They plan to combine all of these elements, the forecasting algorithms, the renewable energy generation, and energy storage, to create a unique energy distribution platform that enables clean energy generation and use at scale.

NTT Investor Presentation

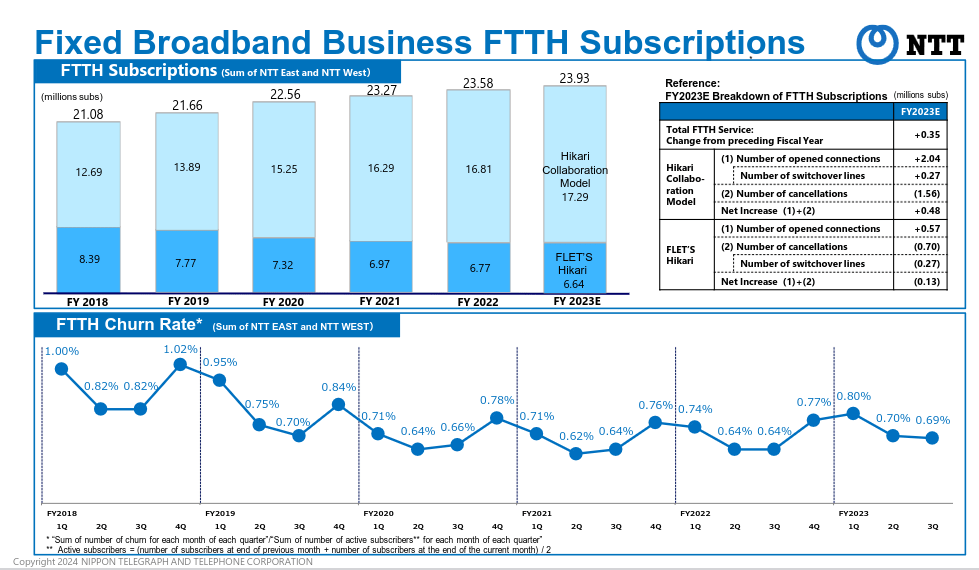

Another important business for the company is fixed Internet broadband, which is a similar business to that of Comcast Corporation (CMCSA), and usually given a relatively low EV/EBITDA valuation multiple of around 7x. The good news with NTT is that despite being a mature business, it continues growing, and they have actually made significant improvements to the churn rate.

NTT Investor Presentation

While we have already discussed the most important businesses for NTT, it has several others, including corporate IT solutions, fixed-line telephone service, real estate, and even e-books. NTT happens to be one of the largest e-book distribution services in Japan with roughly 1.15 million e-books, more than 750,000 e-comics, and more than 35 million monthly users.

The company also has made small investments in areas including smart store technologies, land-based aquaculture, next-generation green houses and drone technology. Additionally, the company makes VC investments through NTT DOCOMO Ventures and they are partners in NTTVC.

NTT Investor Presentation

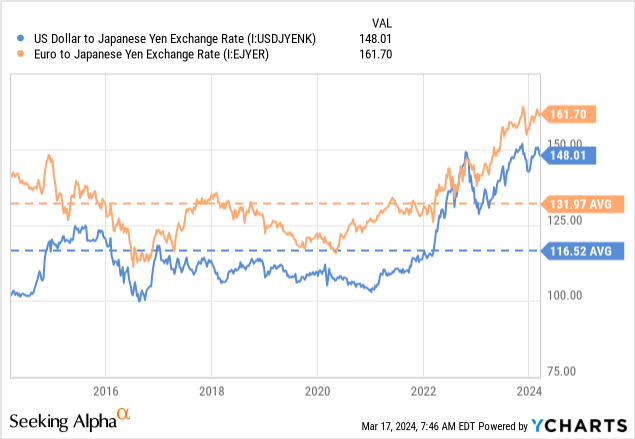

The Japanese Yen (FXY) is currently very undervalued against major currencies like the US dollar and the Euro (FXE). We see this as an added bonus, as dividends are denominated in yen, meaning foreign investors would see their dividends rise should the yen strengthen. Should the exchange rate against the dollar return to the ten-year average, that would provide an added 27% boost to U.S. investors, and a 22% boost for European investors. Some Japanese stocks have an inverse relationship with the yen, as a stronger yen makes their exports less competitive, but this affects significantly more export-oriented companies like Toyota Motor (TM) and Honda Motor (HMC).

NTT has a strong balance sheet with an outstanding credit rating. Whether looking at its S&P Global (SPGI) or Moody's (MCO) ratings, they are several notches higher compared to AT&T and Verizon, even if these competitors are still considered to have an investment grade credit rating.

NTT Group Website

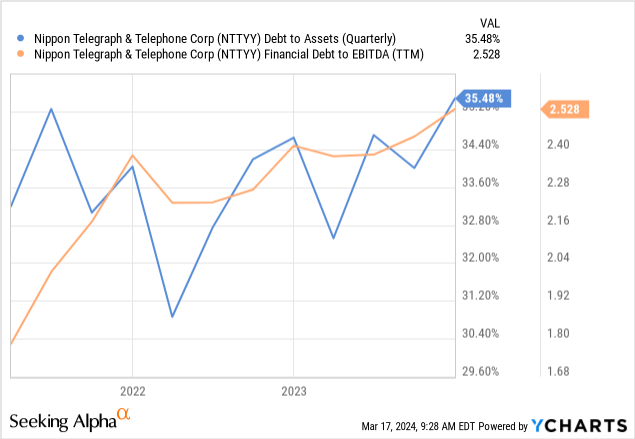

While significant capital investments and the consolidation of DOCOMO meant slightly higher leverage, the company still has very solid credit metrics, and it plans to further reduce its debt-to-EBITDA ratio to ~2x in the next few years. Looking at long-term debt to total capital, we see NTT is in a stronger position than its competitors with 37%. For example, using Seeking Alpha's stock comparison tool, we see that Deutsche Telekom (OTCQX:DTEGY), T-Mobile (TMUS), AT&T, Verizon, and Equinix are all above 50%, while Digital Realty is in the mid-40s.

While some of NTT's businesses are either regulated or commoditized, we still see some competitive advantages. These include economies of scale, as the company is the leading mobile phone operator and can distribute fixed costs over a much larger user base. It also has proven to be a well-managed company, with strong capital allocation discipline. There are also some synergies and cross-sell opportunities among its various businesses.

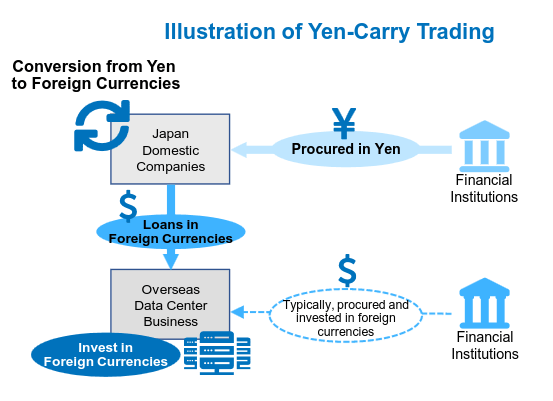

It also has a financing advantage, especially compared to its data center peers like Equinix and Digital Realty. The company has developed funding methods to reduce its financing costs amid rising interest rates. It is able to borrow at very low rates in yen to fund its overseas data center investments in foreign currencies. It is able to do this thanks to its strong relationships with Japanese banks and having local assets to back these loans. It also utilizes inverted yield curves in some foreign markets to partially convert loans to fixed interest rates.

NTT Investor Presentation

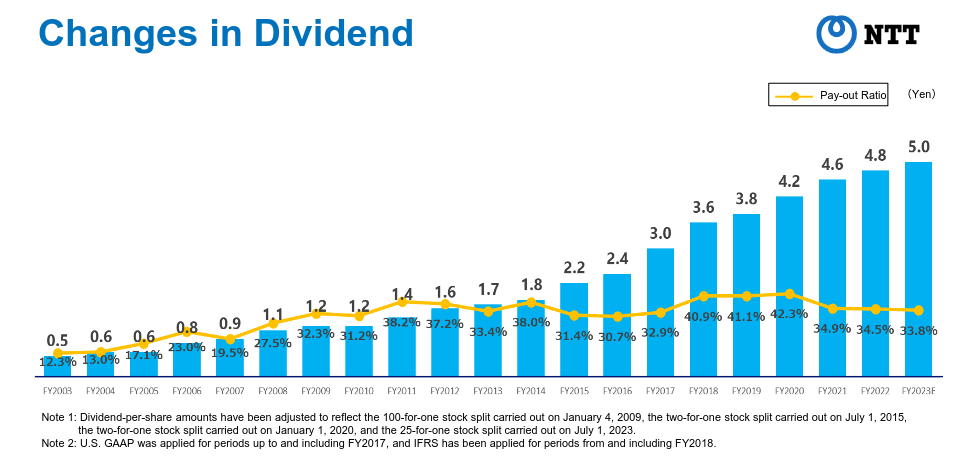

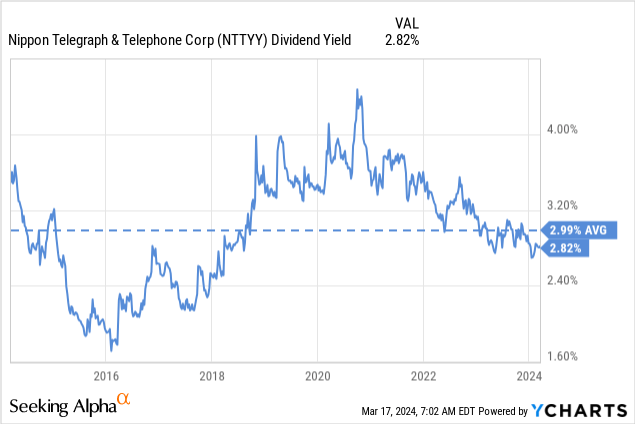

While the dividend yield looks relatively low, especially when compared to AT&T and Verizon, it is important to remember that the payout ratio is low at ~35%, making the dividend very safe and likely to be increased in the future. In fact, the company has been consistently increasing the dividend over the last few years at a very decent pace and has been buying back significant amounts of shares. In other words, while the dividend yield is around 3%, the shareholder yield which includes repurchases is about twice that amount.

NTT Investor Presentation

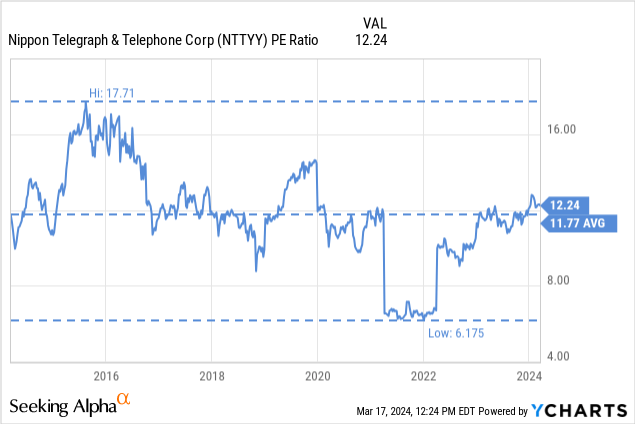

The current dividend yield is very close to its ten-year average, but we believe shares are now more attractive given the growing importance of its growth businesses.

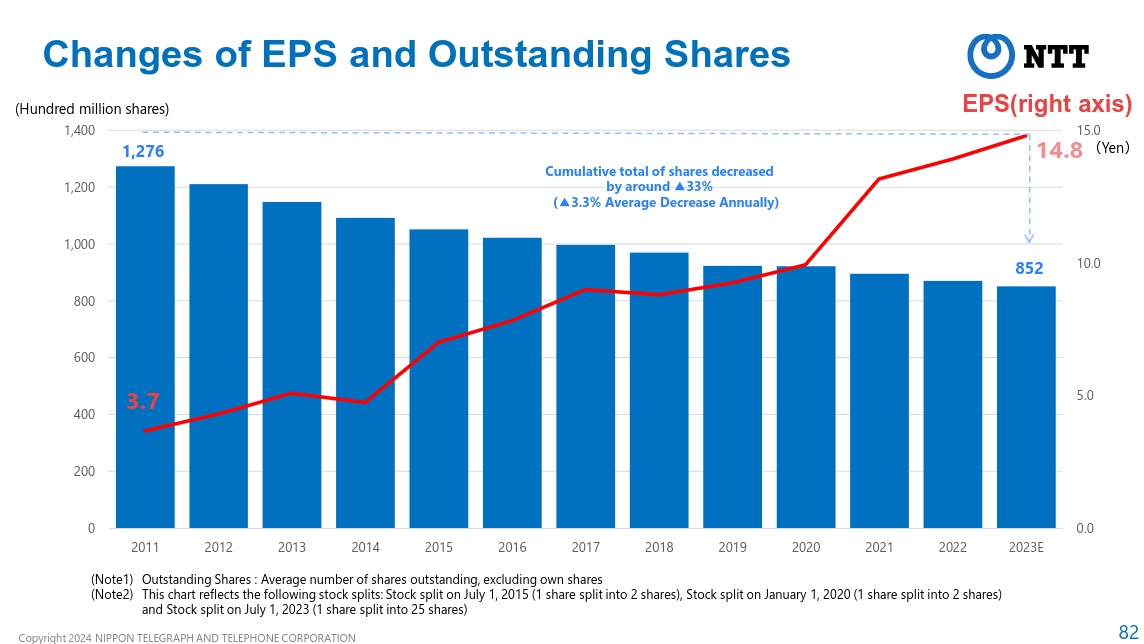

Given the huge tailwinds in the data center business, we think a premium to the historical valuation is well deserved. The company has been incredibly consistent in buying back shares, with an average decrease in share outstanding of 3.3% per year. This puts the shareholder yield around 6%, which we think is attractive, and the company still has some earnings left to reinvest in its business.

NTT Investor Presentation

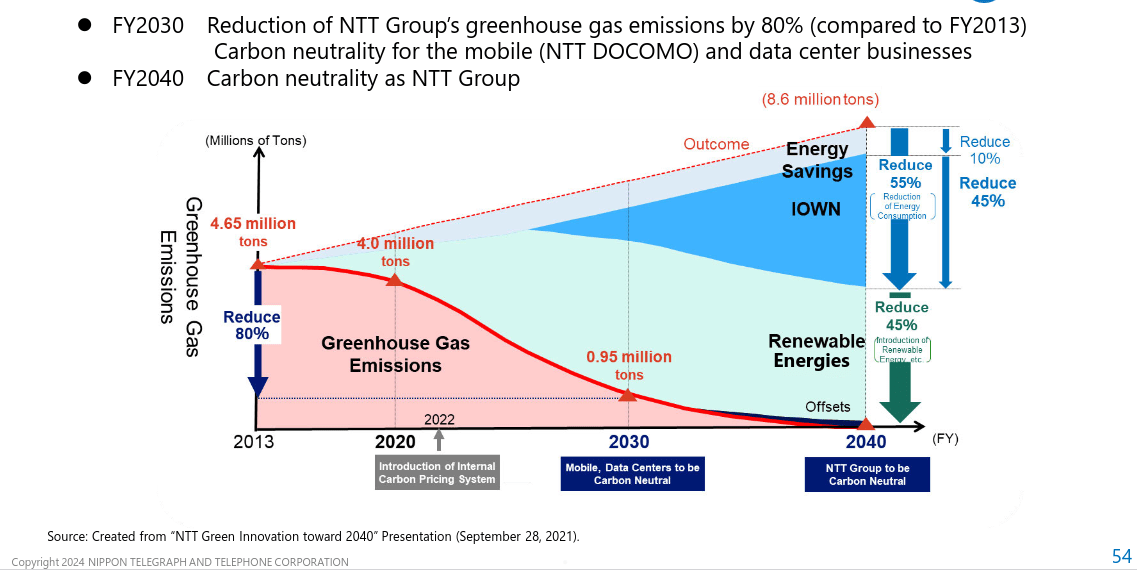

NTT takes sustainability very seriously, even using in some of its presentations the slogan "Innovating a Sustainable Future for People and Planet". It has been recognized by the non-profit CDP with an 'A' grade regarding its commitment to fight climate change, which was an improvement from 'A-' it received in 2022. The company is targeting the year 2040 for carbon neutrality at the group level.

NTT Investor Presentation

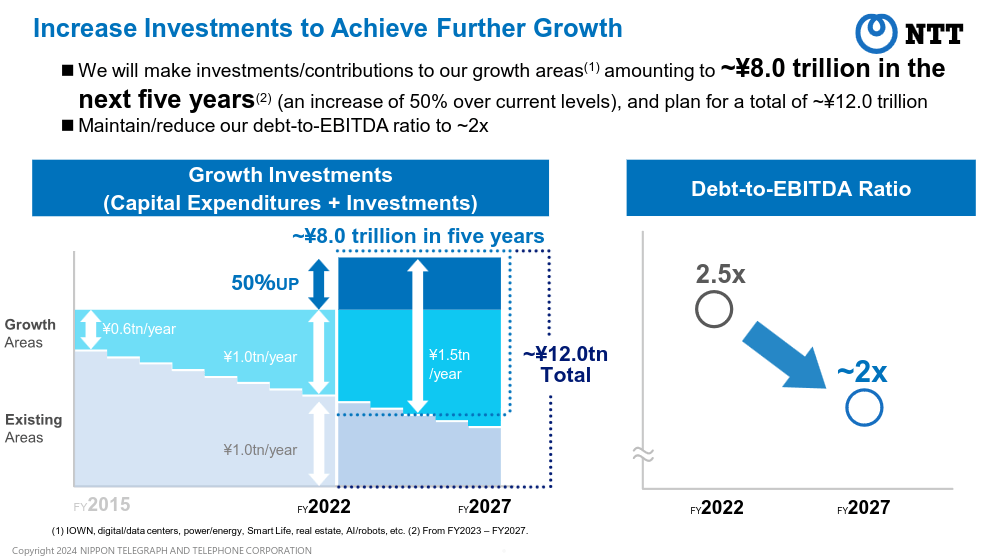

NTT is planning to invest roughly ¥8.0 trillion (approximately $54 billion) in its growth businesses over the next 5 years. This is roughly two-thirds of the total planned investment of ¥12.0 trillion (about $81 billion).

NTT Investor Presentation

This investment should help increase EBITDA by ~20% by FY27, and reduce the debt-to-EBITDA ratio to ~2x, given that the company plans to maintain debt relatively stable while reinvesting profits to grow the business and increase its EBITDA.

NTT Investor Presentation

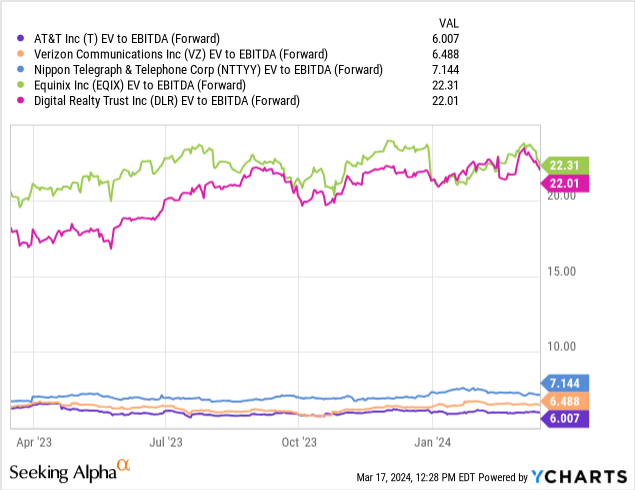

It would appear the market is giving NTT very little credit for the strength of its balance sheet, the huge data center opportunity, or its other growth businesses. Looking at its forward EV/EBITDA the company is only slightly more expensive compared to Verizon and AT&T, with all three trading with a multiple close to 7x. T-Mobile is trading with a ~9.5x multiple, probably deserved given the higher growth it has delivered.

When it gets really interesting is when we look at the forward EV/EBITDA multiples of the data center competitors, which are in the 20's, or roughly 3 times NTT's multiple. In other words, we think investors can participate in this attractive part of the business without having to pay a premium for it. The company is clearly getting little credit for its data center and energy businesses, or the potential of its optical communications technology.

The Price/Earnings ratio is close to its historical ten-year average, but given the increasing importance of its growth businesses, we think an argument can be made that the company deserves some multiple expansion.

We would be willing to pay a small premium for the forward EV/EBITDA ratio of the company over Verizon and AT&T, given its stronger balance sheet and capital allocation track record.

Given that growth businesses currently account for about a third of EBITDA, and the more stable legacy businesses for two-thirds, we think it could be argued the same should be done to its multiple. If we give the legacy businesses a 6x multiple, and growth areas a 20x multiple, the expected forward EV/EBITDA multiple would be closer to 11x.

While we believe NTT shares have below-average risk, there are still many threats to consider. One is that the Japanese Yen could depreciate even more. While we believe it should eventually move closer to its historical average, there is a risk the yen could move even lower. There is also regulatory risk, as was seen a few years ago when the government pushed mobile operators to lower prices. There is also the risk of intensifying competition with the entrance of some low-cost operators. Still, low cost operators like Rakuten Mobile (OTCPK:RKUNY) have only gained modest market share. We believe some of these risks are mitigated by the company's business and geographic diversification, and its very strong balance sheet.

We believe NTT is a decent investment at current prices, as the market is not giving much credit to the company for its growth opportunities, including its fast-growing data center business. With a ~6% shareholder yield, the company only has to grow profits by 3% to 4% annually to deliver 10%+ total returns to investors, assuming valuation multiples stay unchanged. Should valuation multiples expand, investors could experience even higher total returns.

We also see NTT as an opportunity to lock in dividend payments denominated in Japanese Yen, which would become more valuable for most foreign investors should the yen move closer to its average historical exchange rates. For these reasons, we are giving the company a "Buy" rating, especially because we think it is a way to get exposure to the attractive data center business without paying a significant premium.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.