sefa ozel

sefa ozel

Dynagas LNG (NYSE:DLNG) is an LNG carrier owner. It has a fleet of six vessels with an average age of 13.3 years. Three have 150,000 cbm capacity and are equipped with steam turbines, and the other three have 155,000 cbm capacity and are fitted with TFDE (triple fuel diesel-electric) propulsion.

The company is highly undervalued compared to its NAV and its backlog. DLNG trades at 25% PNAV. It seems a severe drawback that DLNG does not distribute dividends on its common shares and has a fleet with obsolete propulsion. However, we have to dig deeper to discover company strengths. DLNG has two issues of preferred units, class A and class B. It distributes dividends with a FWD yield above 8%. 100% of the company's fleet is contracted for the next four years, while 50% of the ships are employed under contracts after 2030. The key word here is the backlog. Having a locked long-term contract means DLNG will probably continue collecting its revenue, hence paying dividends on its preferred units.

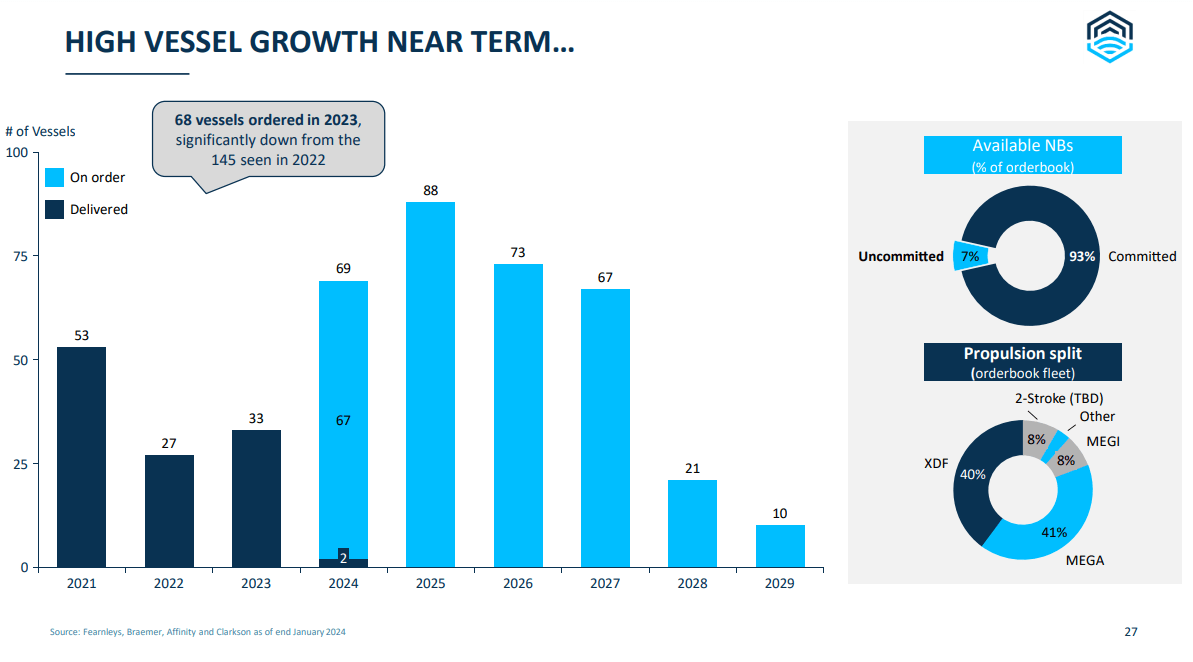

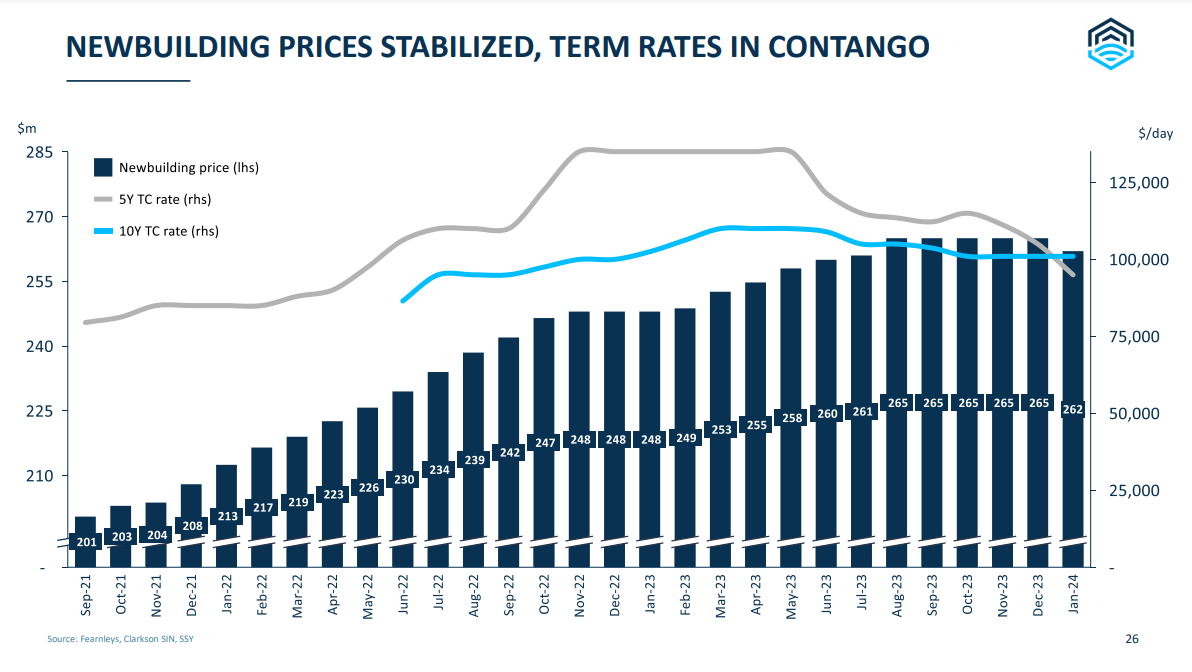

As I stated in my article on FLEX LNG (FLNG), the LNG market seems to be oversupplied, looking at the 51% order book. It is the highest compared to all ship types. The chart below from the FLNG presentation details LNG carriers' supply side.

FLNG presentation

The crucial variable here is propulsion. Steam turbines are obsolete due to their inefficiency. TFDE and DFDE come next. However, they’re costly to build and maintain compared to the new generation of two-stroke engines installed on LNG carriers. They still run on two or three fuels, utilizing boiling gas ("BOG"). It is the losses occurring during the storage of LNG. Due to the external heat, some slight evaporation occurs in the cargo, up to 0.10%-0.15% per day. BOG is reliquefied and used as a fuel for the main engines. These engines fall into the X-DF, ME-GI, and ME-GA categories. The latter is the last iteration of those types of propulsion plants. They emit much less greenhouse gases (more than 20%) and NOx (40%) than conventional engines running on HFO. Ships equipped with steam turbines are at risk of being redelivered from contracts due to their lower efficiency.

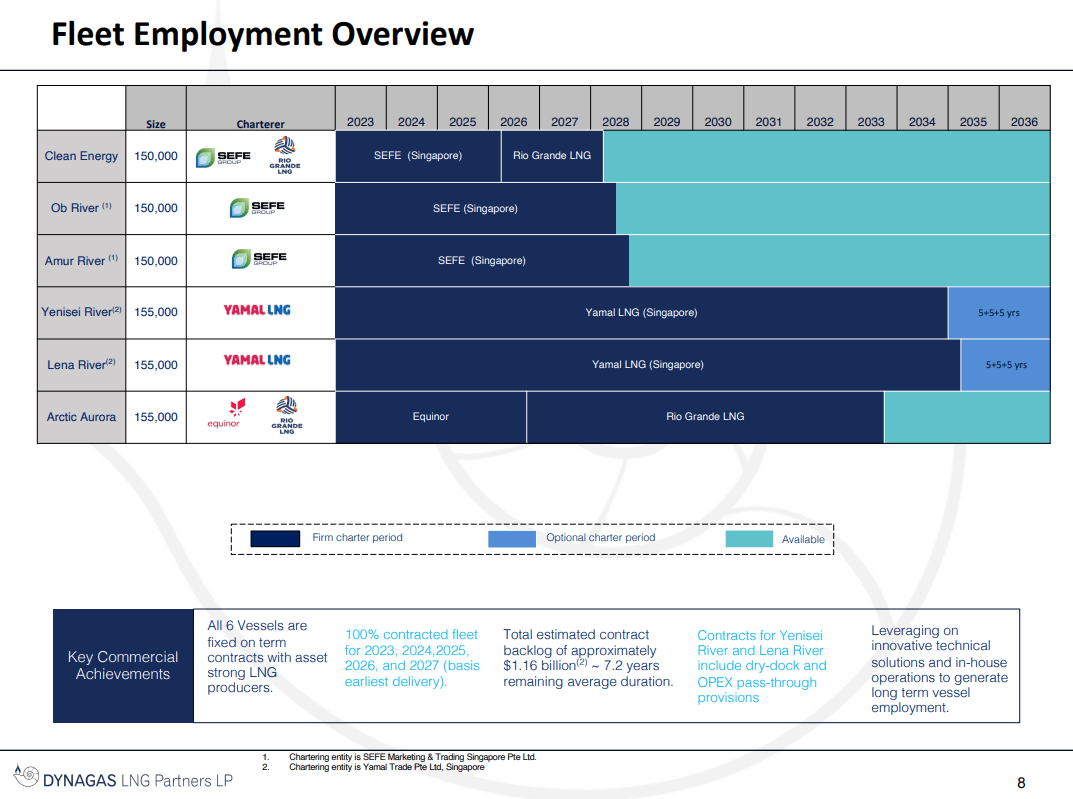

DLNG has six vessels under fixed long-term contracts. Five of the company’s ships are ice class. DLNG has the most obsolete fleet compared to FLNG and Cool Company (CLCO). FLNG has 69% of its ships equipped with MEGI, while 31% with XDF. FLNG has the most modern fleet compared to CLCO and DLNG. CLCO falls in the middle with nine TFDF vessels and two MAGI vessels. Its fleet average age is 8.4 years. The table below from 3Q23 presentation shows the company’s employment schedule for the next 12 years.

DLNG 3Q23 presentation

The average time charter duration is 7.2 years. DLNG has an impressive backlog of $1.16 billion. It is x10 company’s market cap. If we subtract total liabilities from the backlog, it still x6 DLNG market cap.

Customers are primarily Yamal LNG and SEFE Group. The former is JV between Novatek (50.1%), Total (20%), CNPC (20%), and Silk Road fund (9.9%). It operates one of the largest gas fields in Russia, located in the Yamal Peninsula in Siberia. Russian LNG still flows in vast quantities to Europe despite the calls for sanctions. SEFE Group is a mid-stream company based in Germany involved in trading and freight.

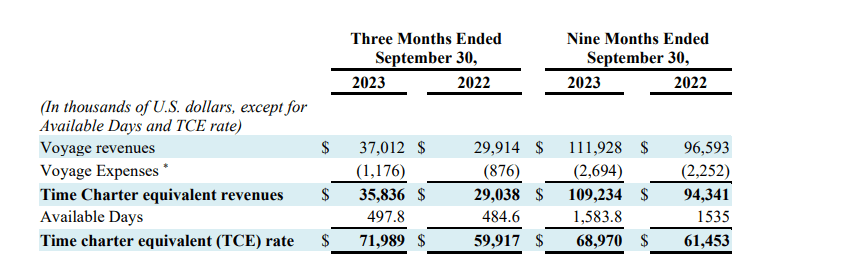

Now, let’s look at the 3Q23 results. The table below is from the 3Q23 company’s report.

DLNG 3Q23 report

The TCE rates increased from $59,917/day in 3Q22 to $71,989 in 3Q23. Vessel daily OPEX jumped by 51% YoY, reaching $19,288/day. Fleet utilization remained strong at 99.8%. 3Q23 was a strong quarter for DLNG. The company delivered $37.01 million in revenue, or $7.1 million higher than 3Q22. Voyage expenses increased from $876 thousand to $1.176 million in 3Q23. TCE revenue grew by 23% YoY, reaching $35.83 million in 3Q23.

Looking at 9M23, DLNG delivers strong results, too. TCE rates increased from $61,453 in 9M22 to $68,970 in 9M23. Daily OPEX per ship changed from $13,438 9M22 to $15,896 9M23. Fleet utilization declined from 100% in 9M22 to 97.1% in 9M23. The rising TCE rates pushed TCE revenues to $109.2 million for 9M23, a 15.9% increase YoY.

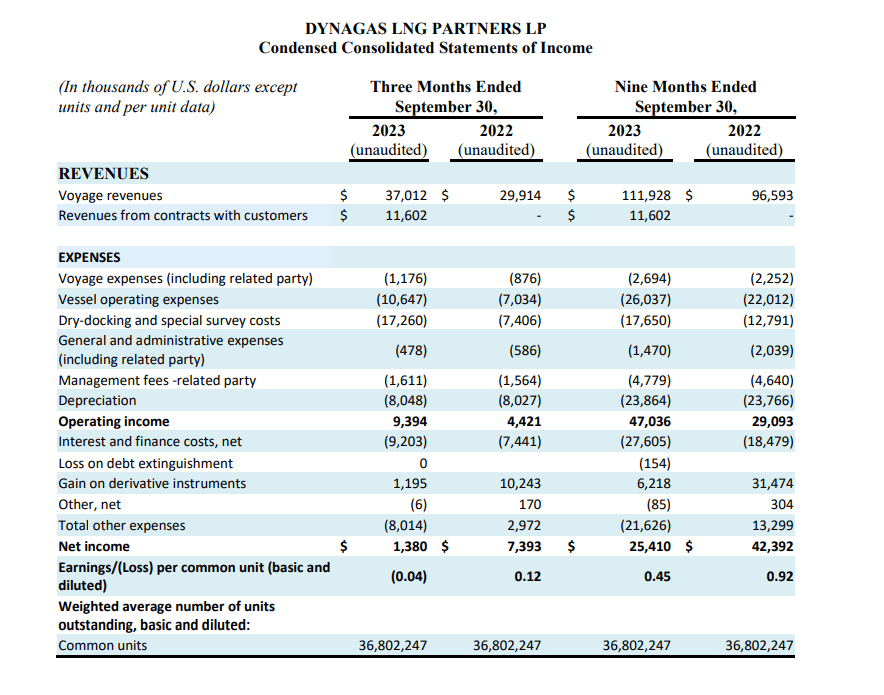

The table shows the company’s income statement for 3Q23.

DLNG 3Q23 report

In 3Q23, drydock costs increased by $9.8 million compared to 3Q22. In the third quarter of 2023, three vessels, Yenisei River, Aric Aurora, and Lena River, completed scheduled drydocks. A Ballast Water Treatment (BWT) system has been installed on all of them. BWT does not directly impact the company's bottom line. However, from September 2024, it will be mandatory for all vessels over 400GT following the Ballast Water Management Convention.

The operating income grew by 113% YoY. However, rising financing costs and lower derivative gains squeezed the company’s net income. Interest and financing costs increased by 24% in 3Q23, while derivative instruments gains dropped by 87%. Looking at 9M23 and 9M22, the picture is similar. Interest costs grew while derivative gains declined.

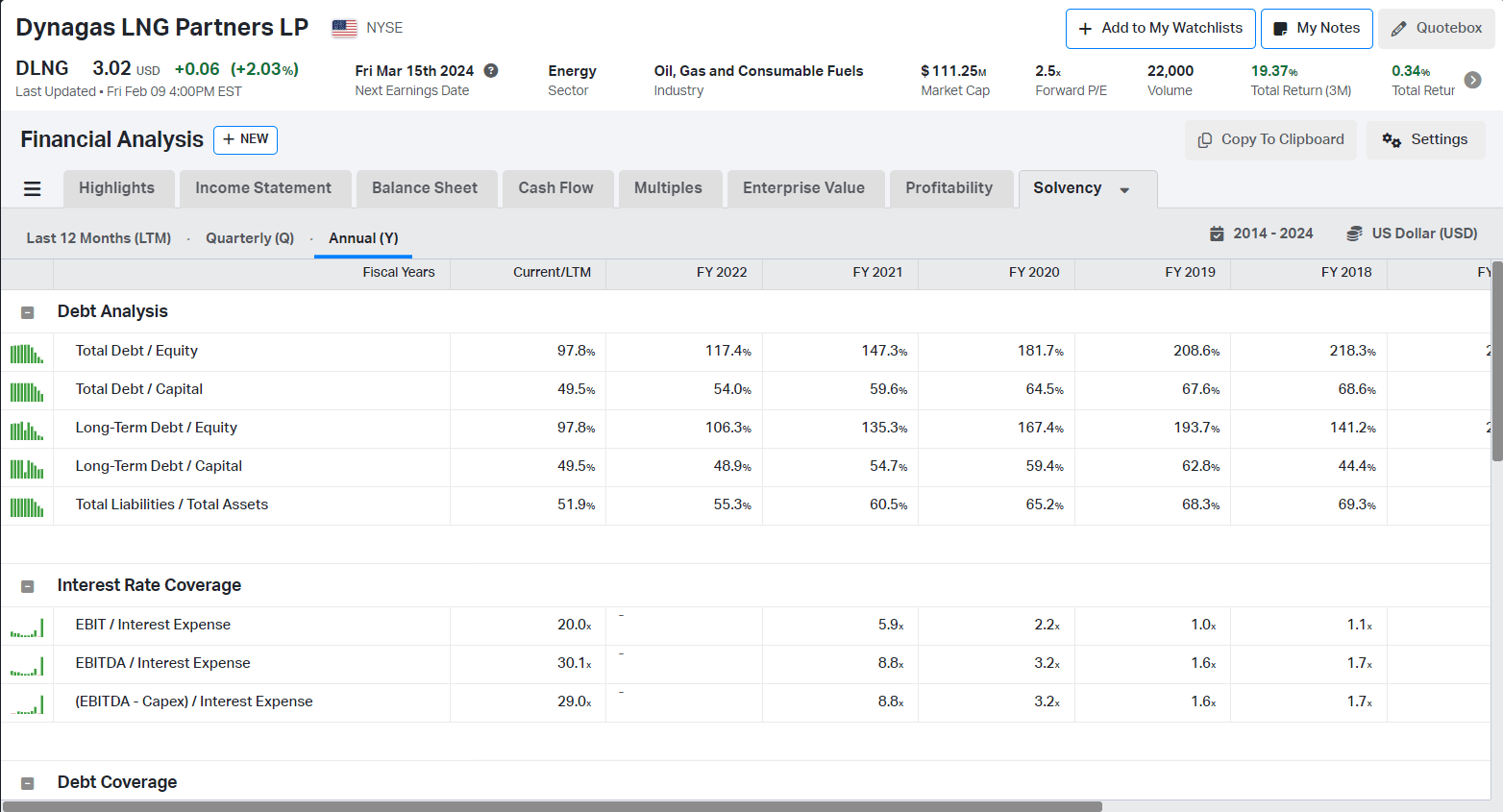

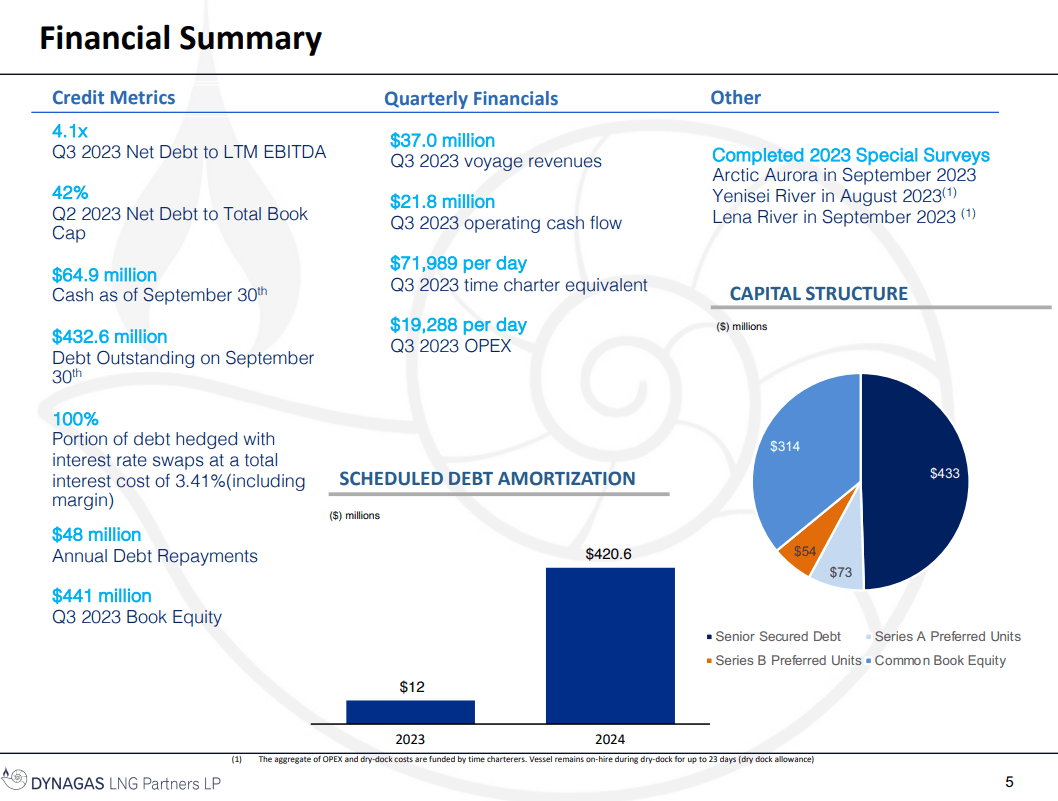

DLNG has significantly reduced its debts over the last five years. The total debt/equity dropped from 218% in 2018 to 97.8% in 2024. DLNG has $64.9 million in cash and $431 million in total debt. The table below shows the company’s capital structure and its interest coverage.

Koyfin

DLNG has ample liquidity, delivering $57.6 million LTM operating cash flow and $63 million operating income, while LTM net interest expenses are $2.3 million. DLNG has a $432.6 million debt due in 3Q24. The chart below shows the company debt amortization schedule.

DLNG 3Q23 presentation

Given the company’s strengths ($1.16 billion backlog and long-term contracts), I believe it will amend the credit facility agreement, extending the maturity further. Of course, a few known variables may cause an issue. The obsolete fleet means a higher risk of redelivering so that the lender may ask for a higher risk premium, i.e., higher rates. Another way to reduce lenders’ risk is to estimate lower values of the company’s vessels used as collateral and lend a lower percentage based on LTV. In my opinion, DLNG can handle higher interest payments, given its operating cash flow and operating income. A lower value estimate might require the lender to extend credit facility covenants to include one more vessel as collateral.

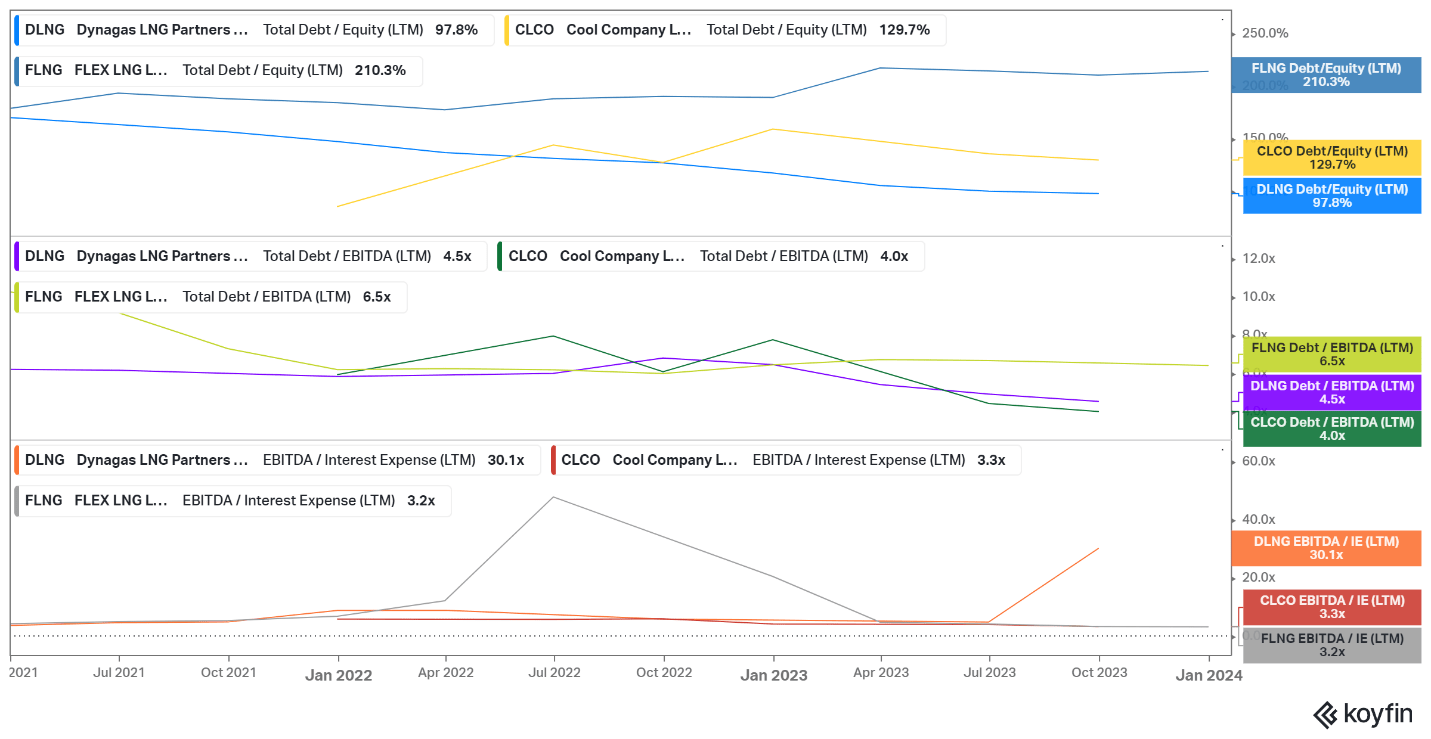

Despite the large portion of debt maturing in 2024, DLNG has a prudent capital structure. The chart below compares DLNG, FLNG, and CLCO.

Koyfin

DLNG has the best total debt-to-equity and EBITDA/Interest expenses. The company’s debt (blue line) has declined significantly over the last few years, as seen in the top section of the chart. CLCO has the lowest total debt to EBITDA ratio, but has higher total debt to equity and EBITDA/Interest expenses.

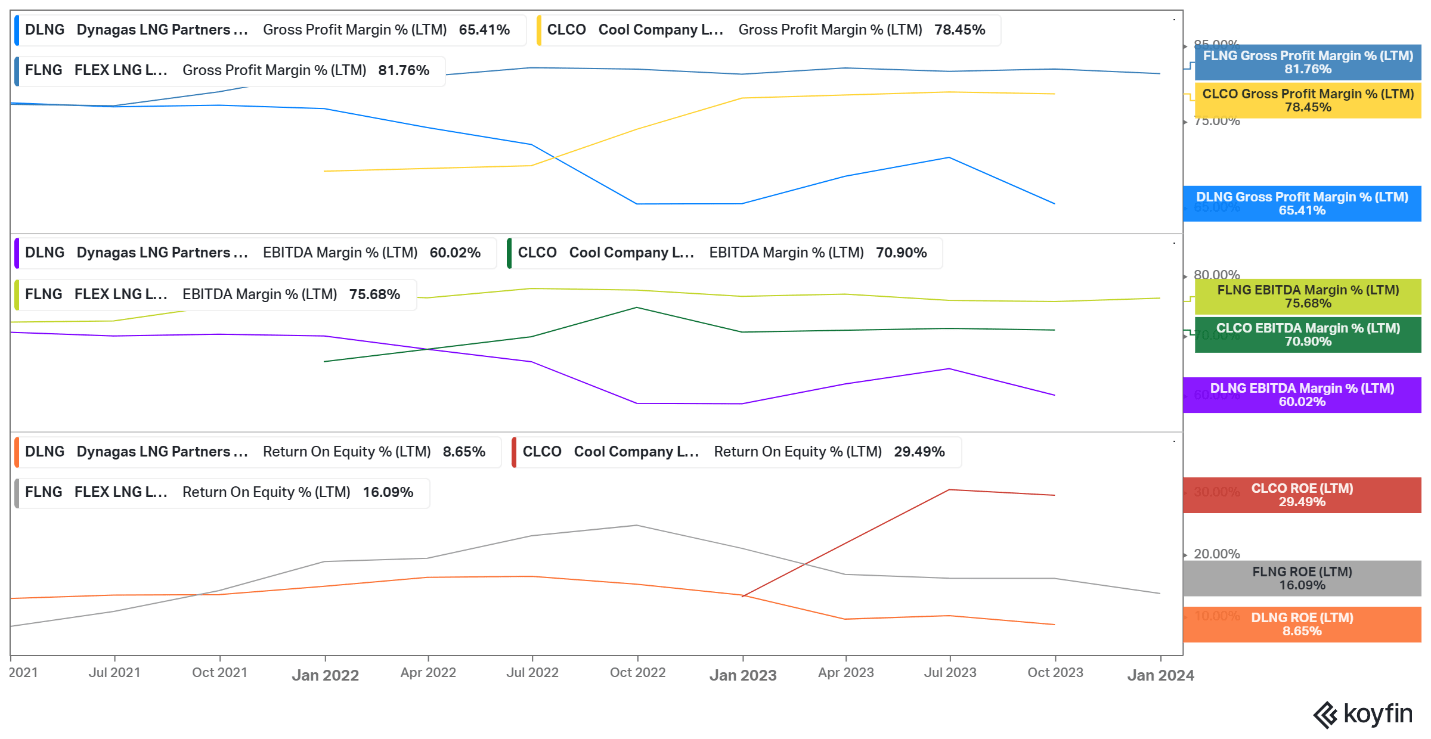

Let’s look at the LNG carriers' margins and returns. All figures are LTM.

Koyfin

DLNG is the laggard in the group due to its focus on long-term contracts. FLNG, too, employs its ships under time charters; however, it does so for shorter periods and sometimes uses spot contracts. FLNG has the newest fleet with the last generation of propulsion plants, which means lower CAPEX and OPEX, so larger margins.

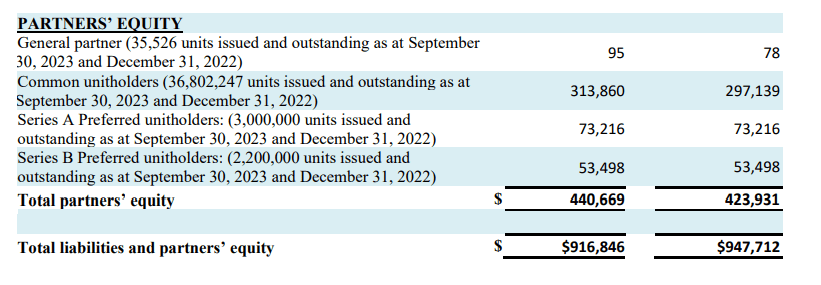

DLNG does not pay dividends on its common shares. However, it distributes cash on its preferred units, classes A (DLNG.PR.A) and B (DLNG.PR.B). The table below shows DLNG's equity structure.

DDLNG 3Q23 report

Series A TTM yield is 8.96%. The last payment for 4Q23 is $0.5625/share, resulting in a TTM rate of $2.25/share. Series B yield is 8.33%. 4Q23 cash distribution is $0.717/share, resulting in a TTM rate of $2.19/share.

To estimate DLNG NAV, I use the FLNG’s estimates for new-build prices shown in their 4Q23 presentation.

FLNG presentation

Since DLNG’s fleet is 13.3 years old, I have to discount the price of new vessels. I use a discount factor of 5%.

The list below shows my price estimates:

Inputs for the DLNG equation are:

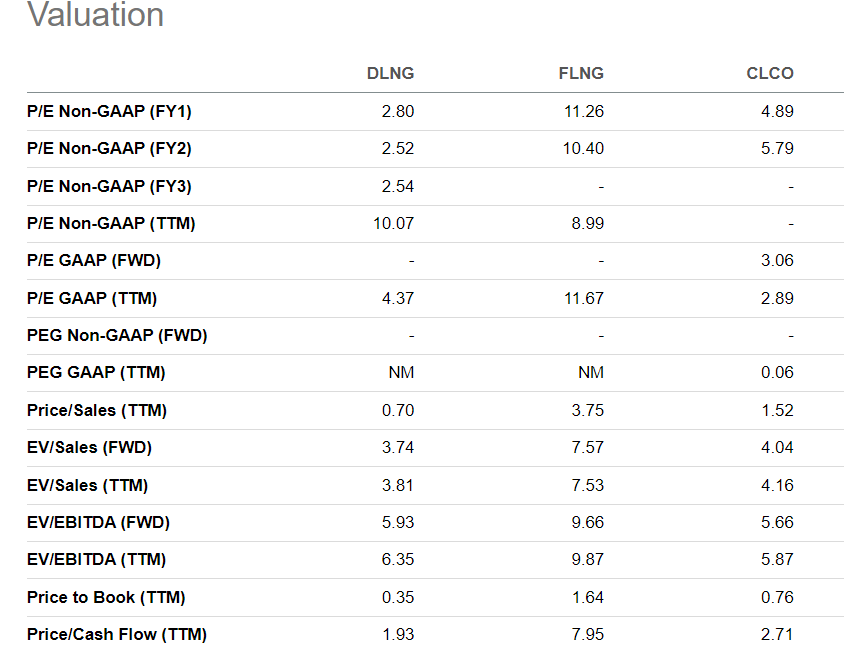

DLNG's market capitalization is $111 million, while its net asset value is $444 million. Hence, DLNG trades at 25 % P/NAV. For reference, FLNG trades at 106% P/NAV and CLCO at 68%.

DLNG trades at 3.81 EV/Sales, 6.35 EV/EBITDA, and 0.35 P/BV. It is dirt cheap compared to FLNG and CLCO.

Seeking Alpha

I believe the lower valuation is due to the perceived political risk related to Yamal contracts and the older fleet. However, preferred units are exciting proposals for income-minded investors.

DLNG is a tricky investment. At first glance, it does not pay dividends and owns an old fleet with outdated propulsion plants. On the other hand, the company has a long-term contract with an average length of 7.2 years, a backlog of $1.16 billion, and attractive yields on its preferred units. On top of that, DLNG trades at 25% PNAV.

Investing in DLNG comes with two pronounced risks: potential sanctions on Russian LNG imports to the EU and its old fleet. Since the Ukrainian war started, there have been voices to ban Russian LNG imports to Europe. Until now, those ideas have not gained traction. I assume it is a possible scenario, though not so probable. The obsolete fleet is another potential issue. As pointed out, vessels with steam turbines and TFDE/DFDE will be replaced by new generation power plants equipped with MEGI/MAGI engines. Steam turbine vessels will be the first to suffer from strengthened environmental regulations. I am not saying it will be banned directly; however, the charterers will shift their preferences to ships equipped with newer propulsion plants in the coming years. DLNG three steam turbine ships (Clean Energy, Ob River, and Amur River) are contracted until 2027/2028. So, DLNG has a few years to plan fleet updates.

I have some DLNG-preferred units, class A. I like the company’s long-term contracts because they mitigate the risk of obsolete ships, at least for the coming few years. The DLNG balance sheet is healthy, though we must consider the debt repayment due in 3Q24. I believe the company will find a way to amend the credit facility without endangering its solvency and liquidity. The most pronounced risk is the ban on Russian LNG imports to the EU. Preferred shares deliver dividends with attractive yields to compensate for the sanctions risk. I give DLNG a buy rating.