Steve Jennings

Steve Jennings

Dolby Laboratories, Inc. (NYSE:DLB) has diversified income streams from its audio and imaging technologies.

I previously wrote about Dolby in September 2023 with a Buy outlook on its prospects for continued growth.

However, fiscal 2024 now looks to be flat on revenue and free cash flow is trending materially lower.

I'm downgrading Dolby Laboratories, Inc. shares to a Hold until management can reignite growth and improve free cash flow generation.

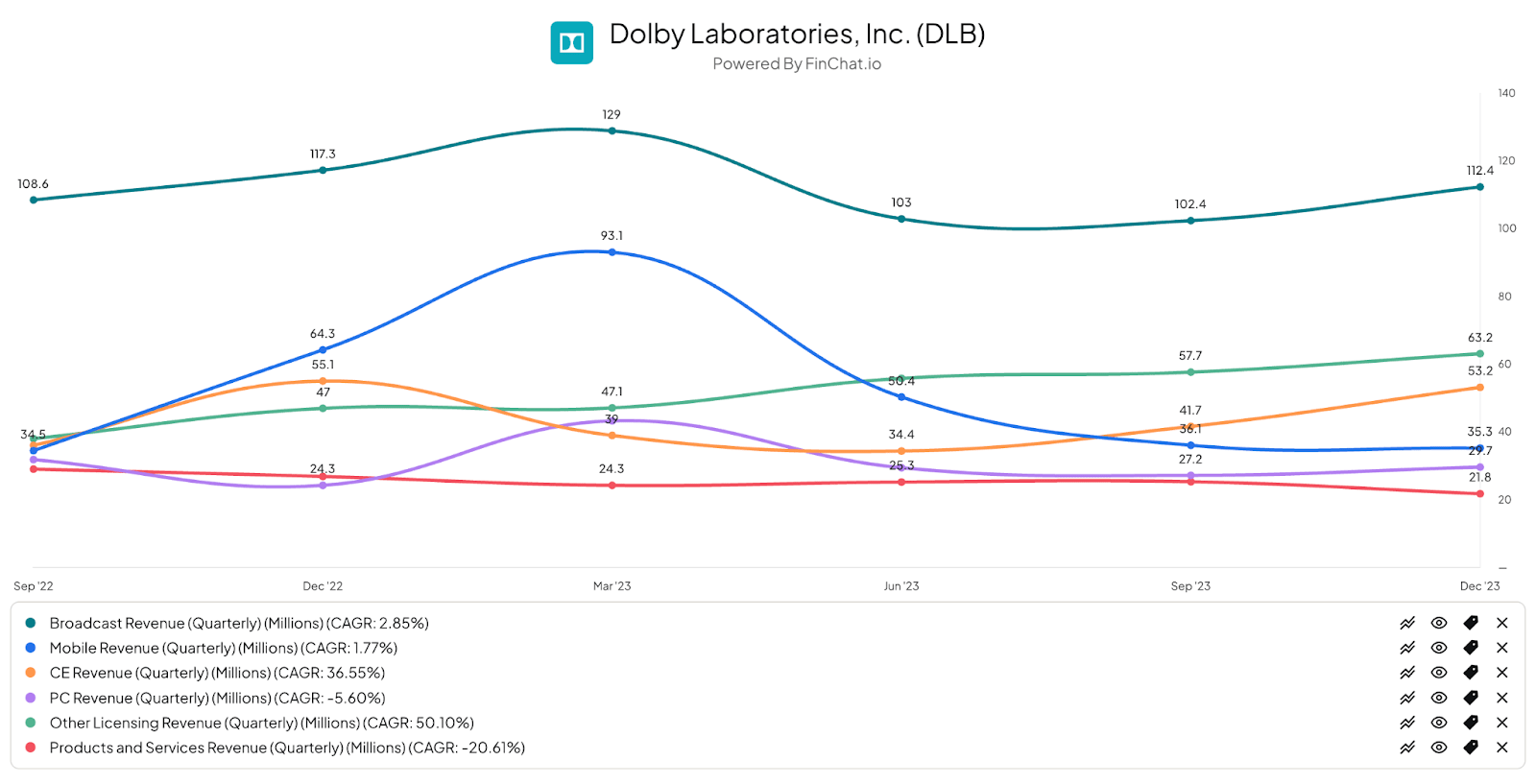

Dolby sells or licenses its technologies into a variety of markets, including broadcast, mobile, consumer electronics, PCs, and other licensing categories.

Below is a six-quarter chart showing a breakdown of the revenue contribution for each of the company's business segments:

FinChat.io

While Broadcast revenue accounts for the largest amount by source, Other Licensing revenue has grown the fastest over the past six quarters, at a CAGR of 50.1%, to now be the second-largest revenue stream for the company.

Its Other Licensing Revenue is composed of DD+, Dolby Atmos, and AC-4 for audio, and Dolby Vision for imaging, which have seen strong growth in usage in recent periods.

CE Revenue has also grown impressively while Mobile revenue has dropped materially from its peak in Q1 2023.

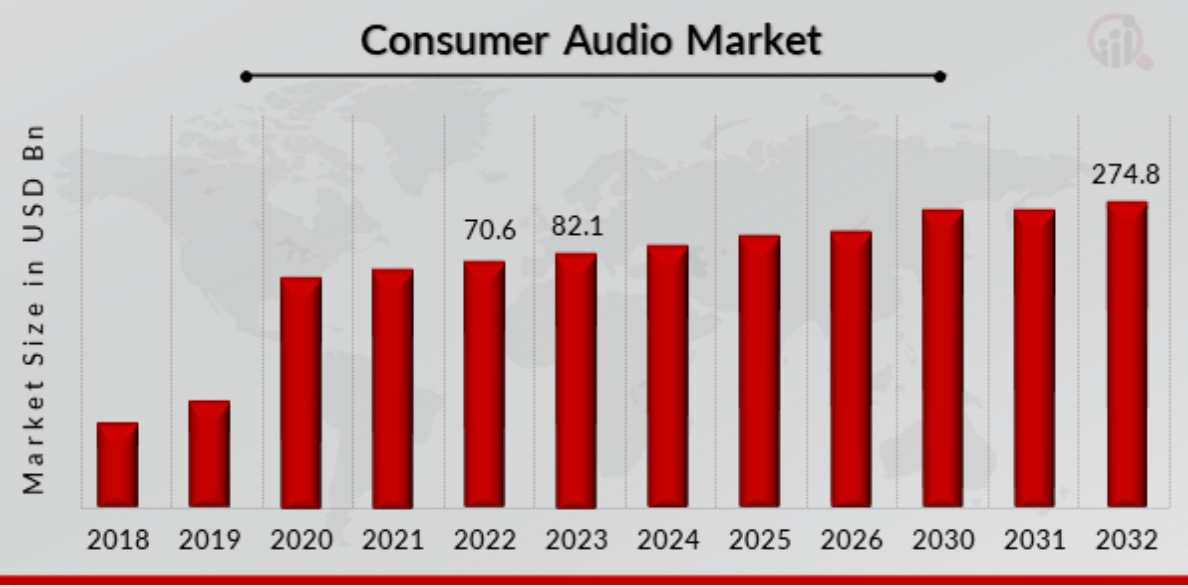

According to a 2023 research report by Market Research Future, the global market for consumer audio products of all types was an estimated $70.6 billion in 2022 and is forecasted to exceed $274 billion by 2032, as the chart shows below.

Market Research Future

This represents an expected CAGR of 16.3% from 2022 to 2032.

But, the challenge for incumbents is that the industry is continuously evolving as consumers increase their spending and reward new technologies with increased adoption.

Dolby competes with a wide variety of capable competitors in several markets, including:

Sony Corporation.

DTS.

Bose Corporation.

Harmon International.

THX Ltd.

Sennheiser.

IMAX.

Others.

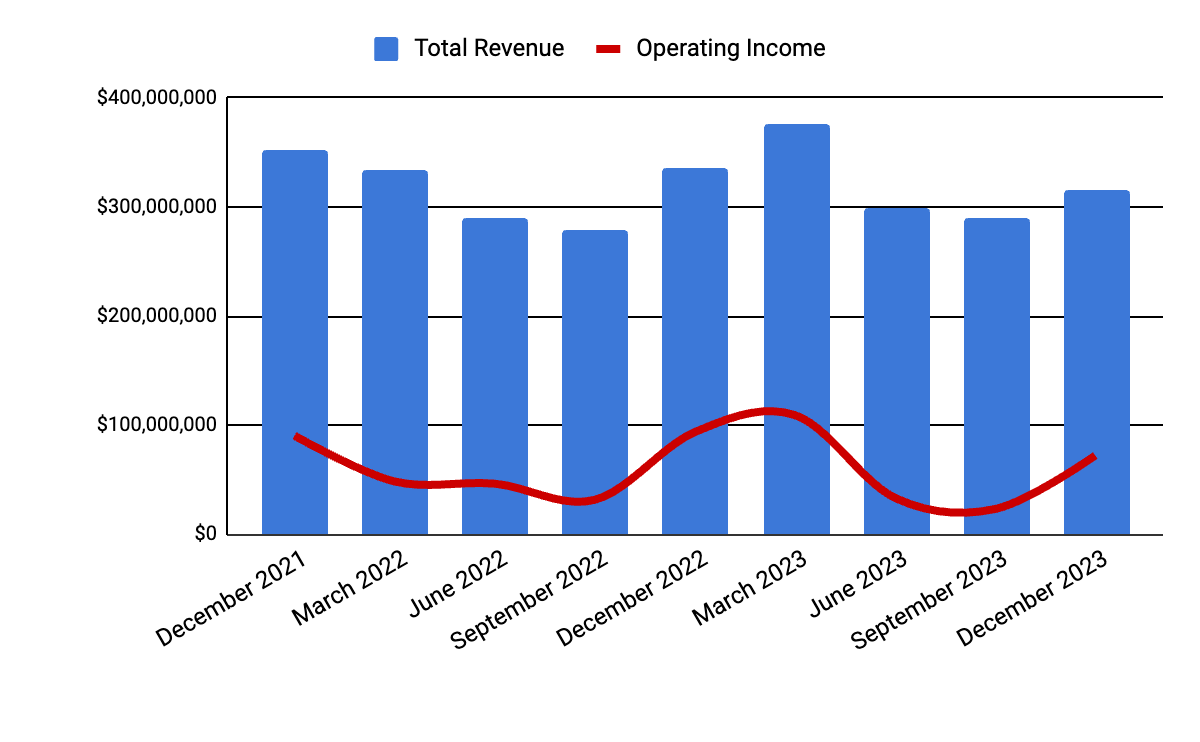

Total revenue by quarter (columns) has trended lower due to a drop in PC and Products and Services revenue; Operating income by quarter (line) has fallen because of higher SG&A costs.

Seeking Alpha

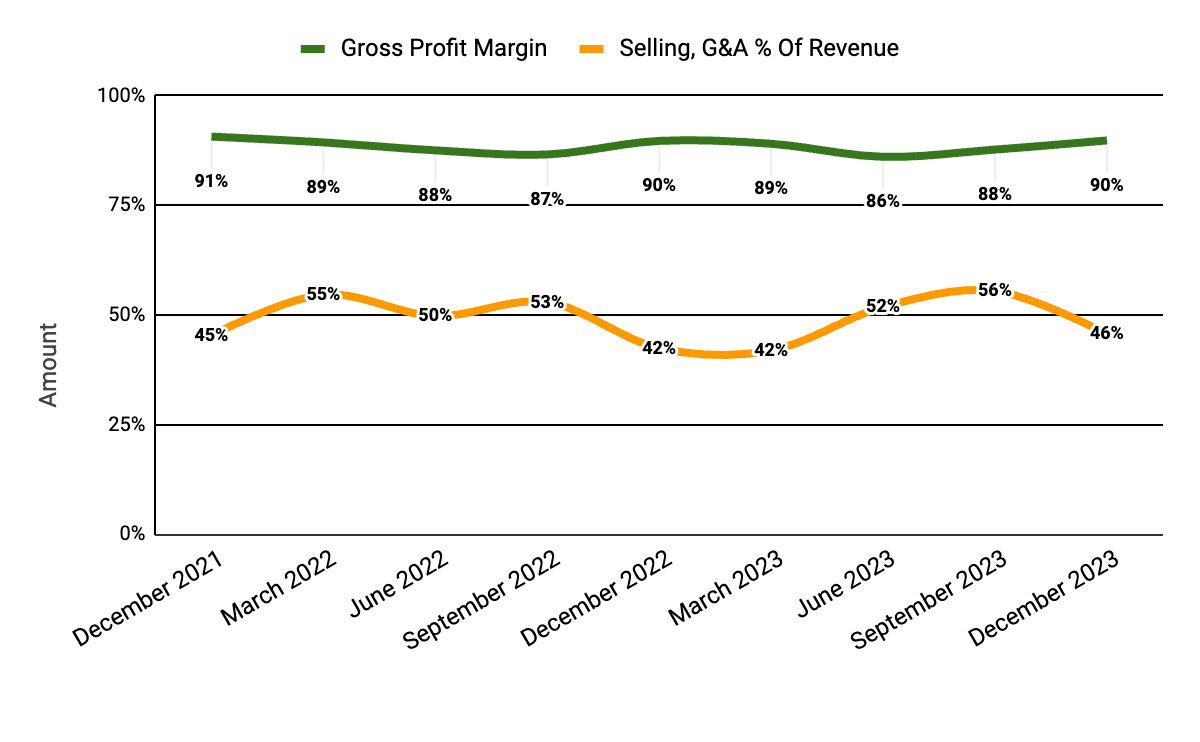

Gross profit margin by quarter (green line) has been flat as a result of various puts and takes depending on its particular business segments; Selling and G&A expenses as a percentage of total revenue by quarter (orange line) have risen in recent quarters, contributing to reduced operating income.

Seeking Alpha

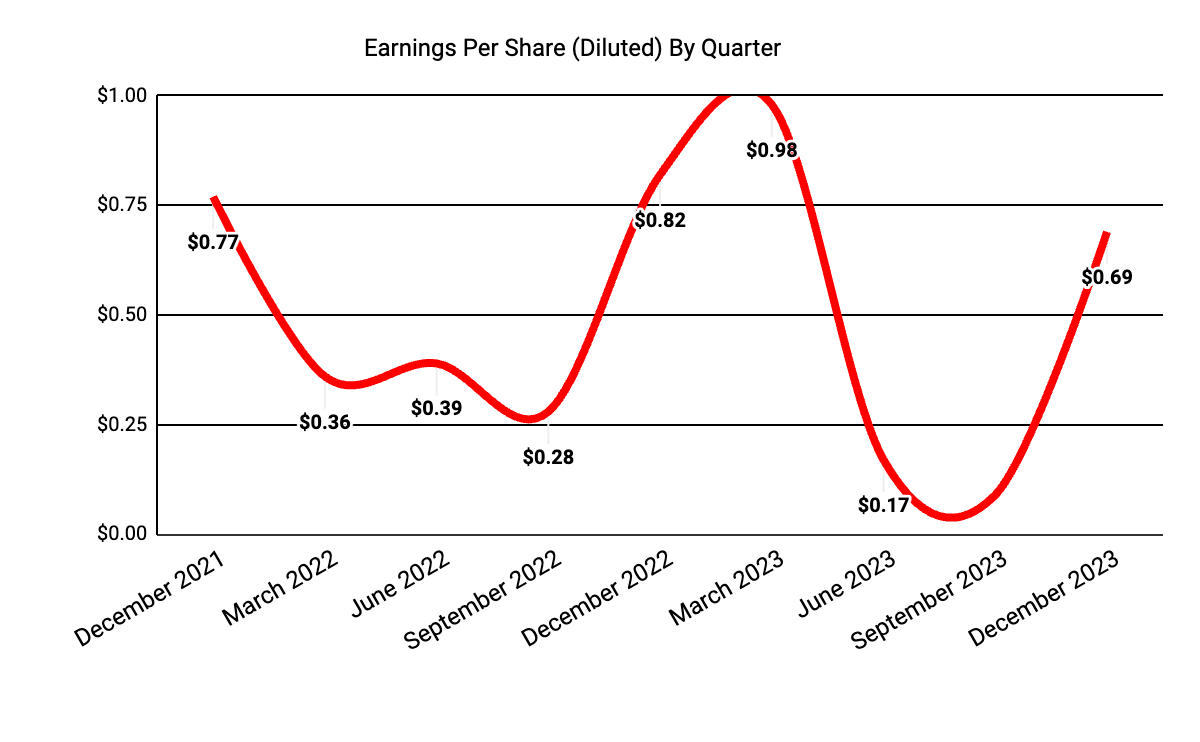

Earnings per share (Diluted) have fluctuated highly in recent quarters, as the chart shows here:

Seeking Alpha

(All data in the above charts is GAAP).

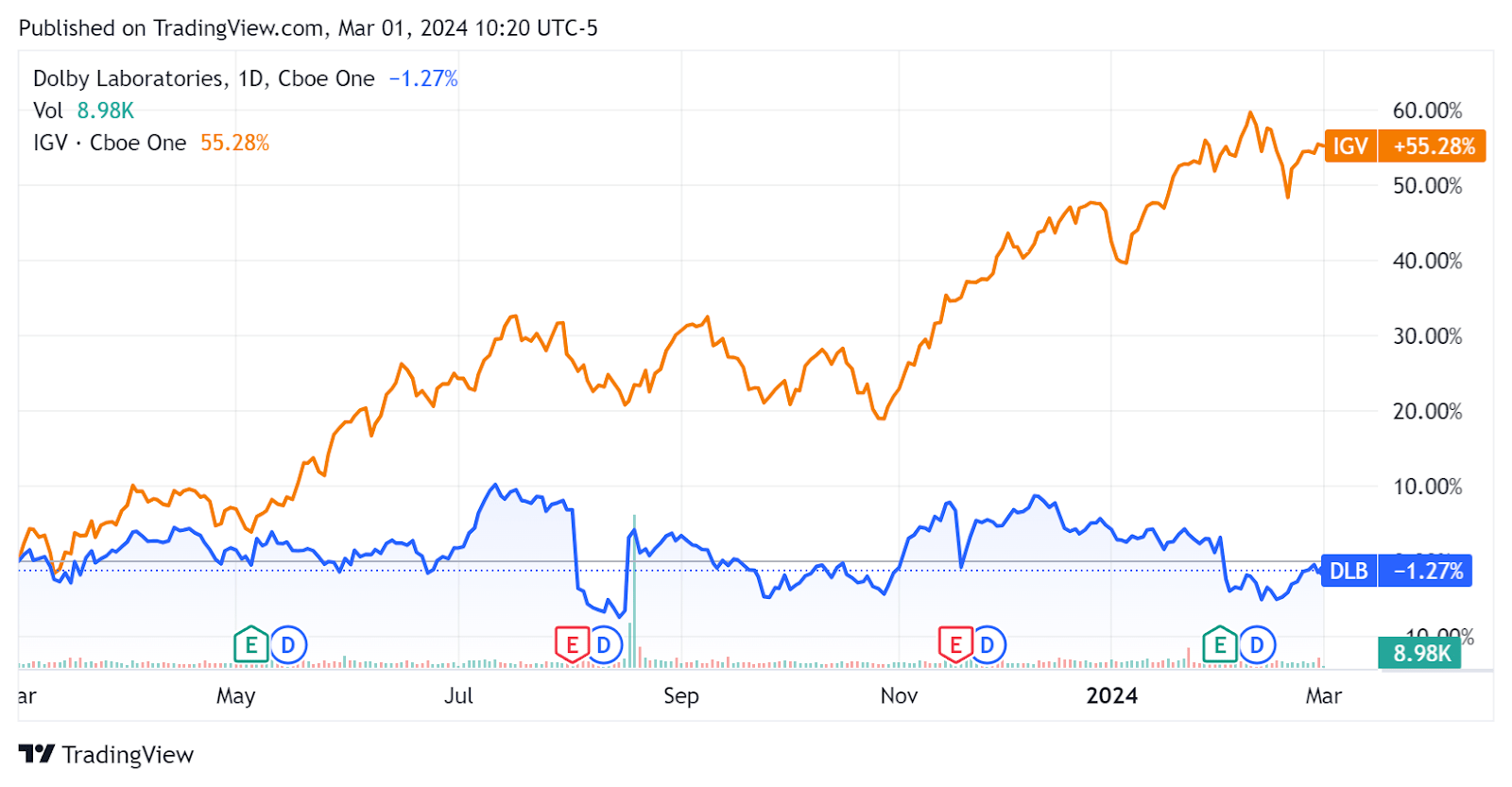

Compared to the iShares Expanded Tech-Software Sector ETF's (IGV) performance of 55.3% over the past twelve months, DLB has substantially underperformed, losing 1.3% in value:

Seeking Alpha

Below is a table of major financial metrics for Dolby:

Metric | Amount |

EV/Sales ("FWD") | 5.2 |

EV/EBITDA ("FWD") | 14.1 |

Price/Sales ("TTM") | 5.9 |

Revenue Growth ("YoY") | 3.5% |

Net Income Margin | 14.7% |

EBITDA Margin | 25.2% |

Market Capitalization | $7,530,000,000 |

Enterprise Value | $6,800,000,000 |

Operating Cash Flow | $319,100,000 |

Earnings Per Share (Fully Diluted) | $1.93 |

2024 FWD EPS Estimate | $3.70 |

Rev. Growth Estimate ("FWD") | 2.8% |

Free Cash Flow/Share ("TTM") | $3.03 |

Seeking Alpha Quant Score | Hold - 2.95 |

(Source: Seeking Alpha).

The firm's Rule of 40 performance is instructive and has shown net deterioration due to lowered operating margin on slightly higher topline revenue growth:

Rule of 40 Performance (Unadjusted) | FQ3 2023 | FQ1 2024 |

Revenue Growth % | 2.1% | 3.5% |

Operating Margin | 27.3% | 22.9% |

Total | 29.4% | 26.4% |

(Source: Seeking Alpha).

Dolby is likely to produce roughly no revenue growth in the current fiscal year if management's guidance turns out correctly.

The market appears to have responded to that by reducing its EV/Revenue multiple to 5.2x, and I see no reason to argue with that.

However, earnings may surprise to the upside, if recent past history of earnings meets or beats is any indication of future results.

This potential is clouded by increasing volatility in its recent earnings results, so it's difficult to get too excited about any consistency there.

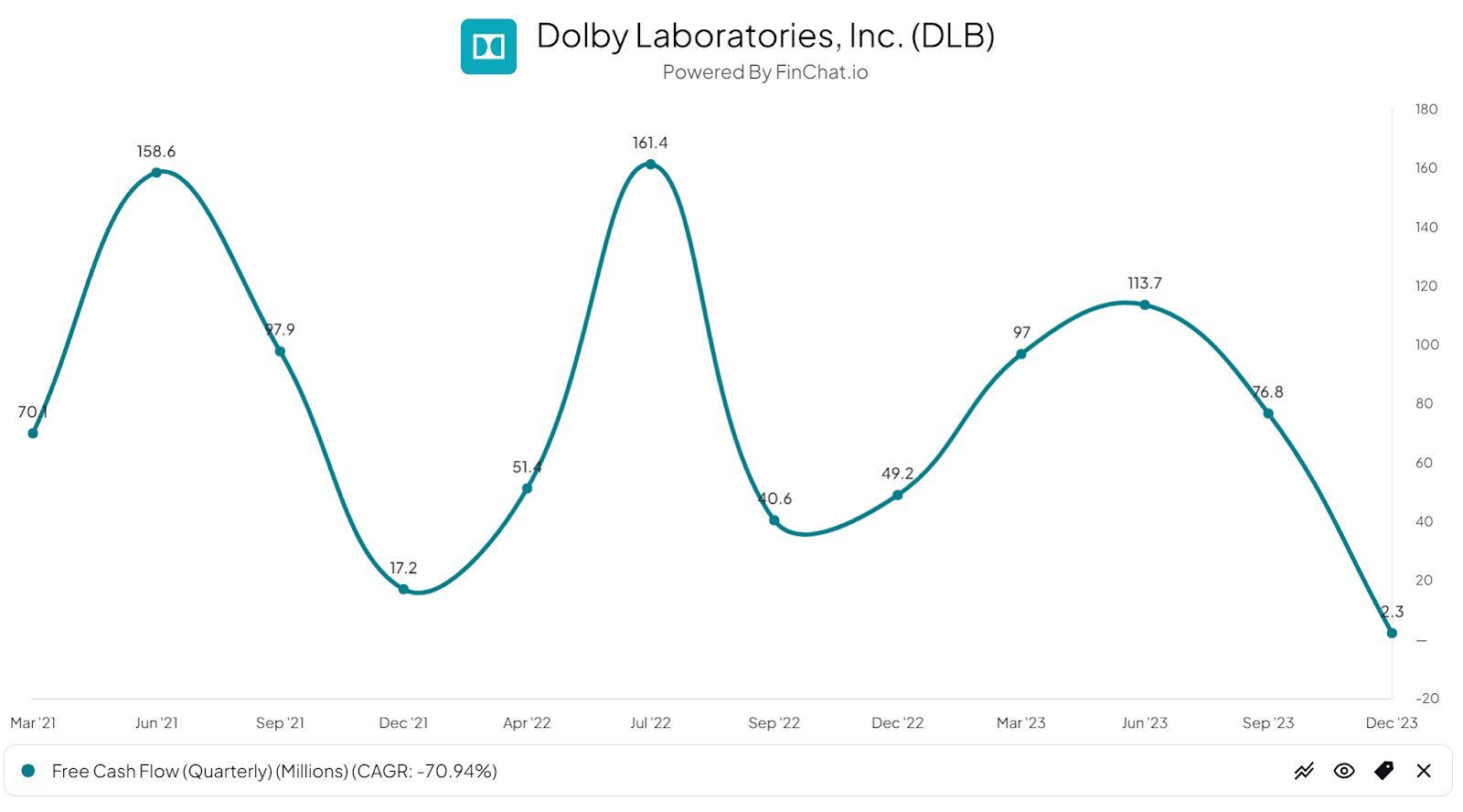

Free cash flow has been extremely variable, too, as the chart shows below:

FinChat.io

As the chart illustrates, the firm has produced lower highs and lower lows in free cash flow in 2023, driven by a worsening operating environment that is dragging on cash flow.

While management has recently increased the dividend, the stock currently has a 1.5% forward dividend yield, but it's no great enticement to most investors.

The problem has been a continued drop in device shipments, driving down licensing and mobile revenue.

Leadership wants to continue to focus on the automobile market and has had significant success with Chinese EV manufacturers, so that's a potential bright spot going forward.

And, Dolby's balance sheet is quite strong, with no debt and significant liquidity.

But, in an environment of flat revenue growth at best, it's difficult to believe that money placed in DLB will be highly rewarded in 2024.

Accordingly, I've changed my previous outlook for Dolby Laboratories, Inc. stock from a Buy rating to a Neutral Hold due to flat revenue and the trend toward worsening free cash flow generation on higher operating costs.