Frank Rothe/The Image Bank via Getty Images

Editor's note: Seeking Alpha is proud to welcome Long Term Capital as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Frank Rothe/The Image Bank via Getty Images

Delek US Holdings (NYSE:DK) is an integrated energy company with operations in refining, logistics, and retail segments through its network of convenience stores and gas stations. Despite consistently returning capital and persistently seeking to unlock the discount to its sum-of-the-parts valuation, the company trades at a significant discount. While the process has been slow thus far, given the current valuation and continued capital returns, the downside is well protected. Moreover, if management follows through on its plans, there is potential for at least a 47% upside from the current levels.

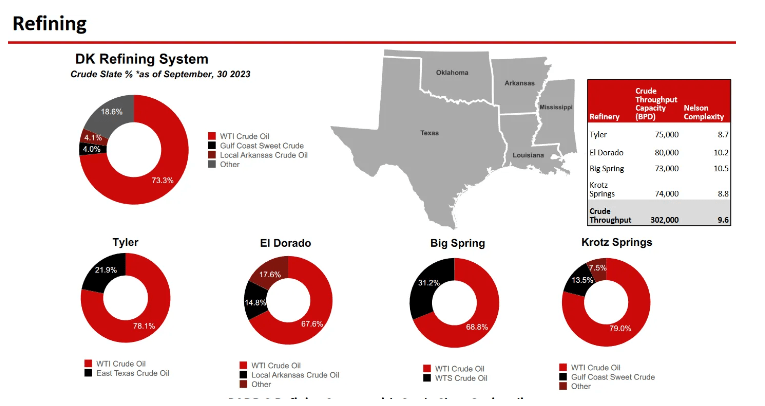

The key operation of DK is its Refining business. In this segment, DK owns 4 refineries in two Texas with the remaining two in Arkansas and Louisiana. The throughput capacity of these four refineries is about 302k barrels per day. The company has been carrying out modernization activities on all of its facilities in recent years. Going forward, the earning power of each facility should improve with the modernization expected to be completed by the end of 2024.

Investor Deck

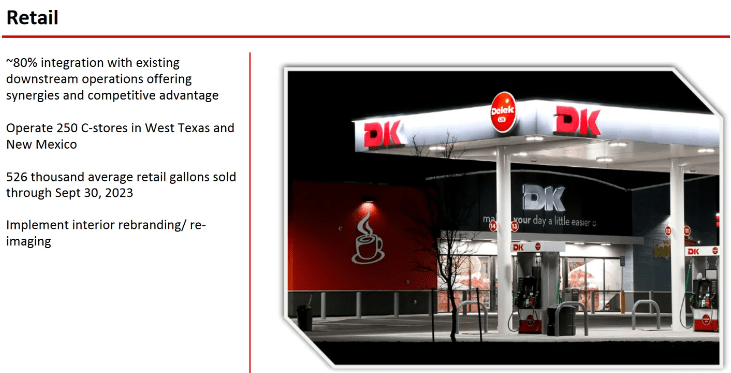

Delek's retail business includes a network of 250 gas stations and convenience stores in West Texas and New Mexico. DK operates these locations under two brands, Delek and Alon, later of which was fully consolidated by Delek in 2017 after they sold off its MAPCO-branded operations.

Investor Deck

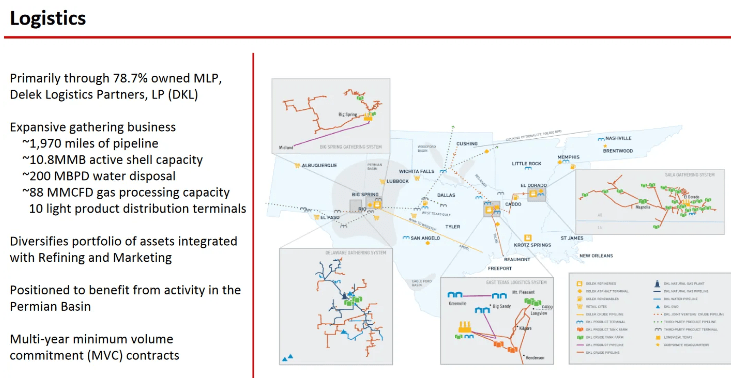

The logistics segment essentially comprises Delek Logistics Partners (DKL), a publicly traded MLP of which DK owns 79%. This is a robust business with stable cash flows and minimum volume commitment contracts, guaranteeing stability even with largely one client, Delek. It operates as a traditional midstream energy operation with a network of pipelines and storage facilities for crude oil and natural gas.

Investor Deck

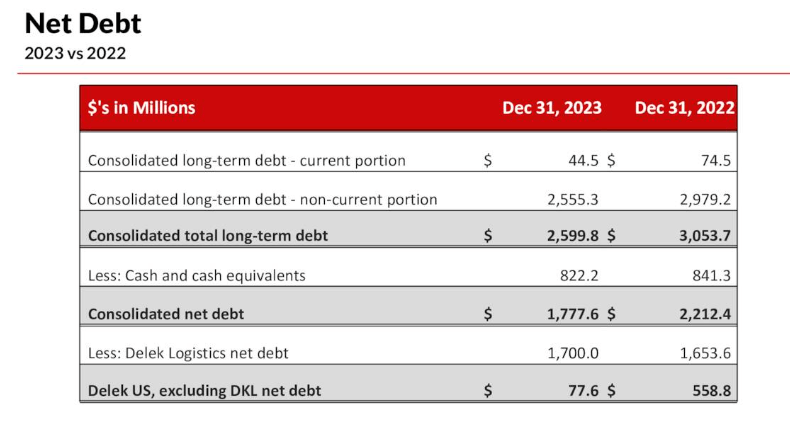

Delek appears to be overlooked by many investors due to its seemingly high debt load and complex holding structure. However, it's important to note that most of the debt stems from the consolidation of its majority stake in DKL, the logistics operation associated with DK. If we exclude the DKL net debt, the company has just $78m in net debt vs $560m a year prior (see the table below). The DKL debt is non-recourse to DK, so considering it as a key impediment to investment seems unreasonable. Meanwhile, given the structure of the midstream operation and the stability of cash flows in the business, debt levels seem more than manageable at DKL. Since 2012, DKL's normal level of net debt to EBITDA has hovered around the 4-5x range, and in the same timeframe, its valuation has stayed within a 7-10% dividend yield. The current 10% dividend yield and 4.6x LTM net debt/EBITDA are exactly within historical norms.

Investor Deck

Before we proceed to the rest of the investor concerns, it is important to note how management plans to unlock value here. One of the most obvious ways to realize the SOTP gap is to get rid of the consolidated debt on DK's balance sheet from DKL. Management has communicated on multiple occasions that they are looking to do just that, most recently in the Q3 earnings call. Even though we do not know the exact mechanism, it is likely to be accomplished either through a spin-off or a sell-down of the majority stake in DKL. Another option to close the SOTP gap is via a sale of the retail operations. This has also been communicated on multiple occasions, including on the latest call. During the call, management confirmed that all options are on the table when asked about the potential sale of the retail segment.

Let's circle back to other reasons for a persisting discount. Investors are concerned about the prolonged timeline around the potential value-unlocking event, which was first announced in September 2022. The reason why investors are worried about the prolonged timeline likely relates to the perceived difficulty in finding a buyer for both of the assets. I believe these risks are overblown.

Mainly, DKL and DK operations are highly dependent on one another. Therefore, a potential buyer may be concerned about buying a stake in a midstream operation that is largely focused on satisfying DK's volumes. However, this interdependence, in my opinion, creates a stable equilibrium within which both parties operate, and the fact that one cannot operate without the other makes this relationship sustainable even with different owners. Moreover, the usual relationship between downstream and midstream operations in energy markets is carried out through long-term (5-10 year) contracts that are easily renewable. I believe that during negotiations with a potential buyer, a mutually beneficial deal could be reached with the appropriate contract length and standard minimum volume commitments. Thus, the fear that the DKL stake could not be sold is likely overblown.

The same goes for fears of a sale of the retail operation, which is also technically tied to DK's core refining business. However, as long as the location of the gas station is not remote, finding a new supplier should not pose too much difficulty. Moreover, DK has a history of selling similar retail operations, so I don't think it will be a problem this time around either. In 2016, DK sold its Mapco Express operations without any issues and at rather high multiples too (more on this later).

In the recent earnings call, management confirmed that all options are on the table. Unlike previous quarters, however, much less was discussed about the value-unlocking event. Despite this, I do not think the thesis has changed in any material way. The key part of my thesis is the fact that management continues to insist that the strategic review is progressing, and over the last year and a half, the management has proven to be prudent allocators of capital, which gives me the confidence to hold the stock even if the plan eventually fails. In the meantime, the company is cheap on mid-cycle earnings, and I am more than happy to collect dividends and enjoy the continued buybacks.

Speaking of capital allocation, the management navigated the recent industry upcycle very well by paying down debt and returning capital to shareholders. Just last year, the company paid down $480 million in corporate-level debt and returned $146 million through buybacks and dividends, or about 9% of the current market capitalization. All the while, the company went from $560 million to just $78 million in net debt at the corporate level. Meanwhile, the company has recently raised its dividend to $0.245/share per quarter, and at the current dividend rate, they are paying a 4% yield along with continued buybacks. On top of this, the company reduced its corporate costs by $80m YoY with $20m still to go.

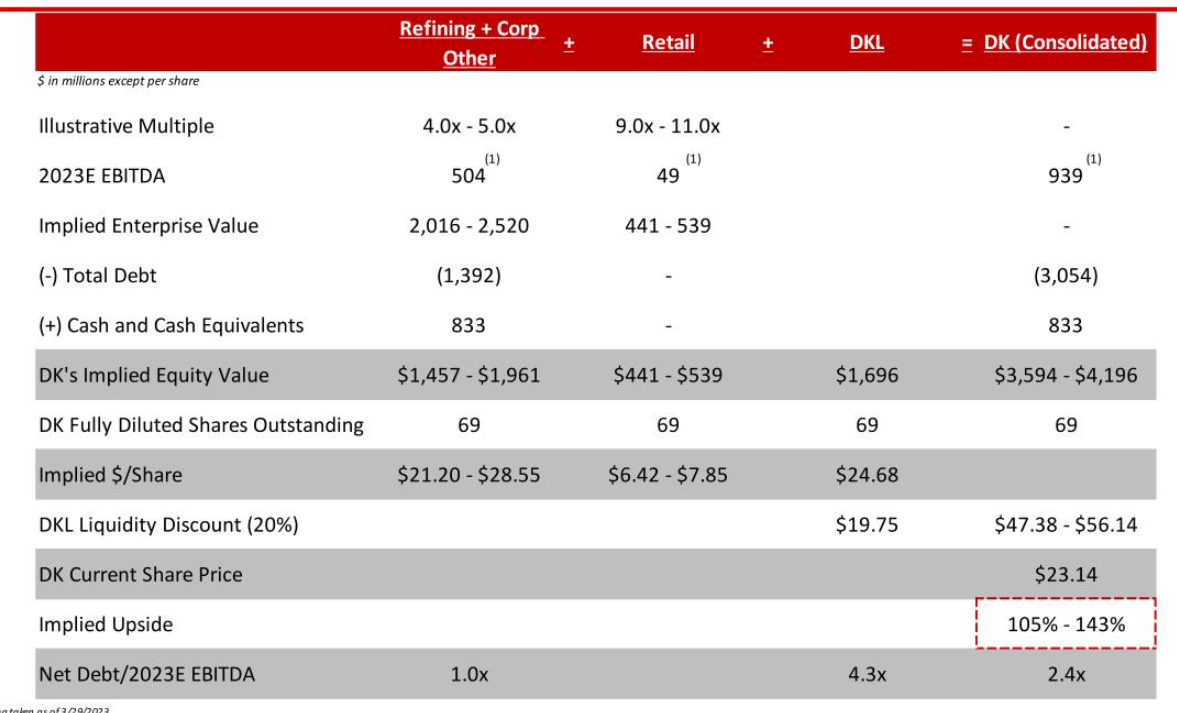

Valuing DK appropriately is not the easiest task given the cyclical nature of the business and the complicated corporate structure. Below, you can see the table from one of the investor presentations on how management thinks about the sum-of-the-parts (SOTP) value here. According to their estimates, the fair value of the company's assets is $47-56 per share, representing about a 70-100%+ upside from current levels.

Investor Deck

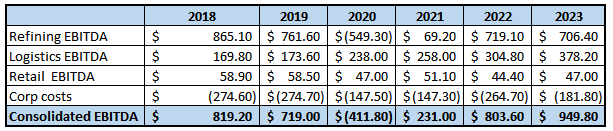

Quite a few things have changed since so below is my attempt at SOTP analysis. I will try to break it down a bit more, including assumptions behind mid-cycle earnings. First of all, here's the breakdown of the segment earnings since 2018 for reference.

DK Financials

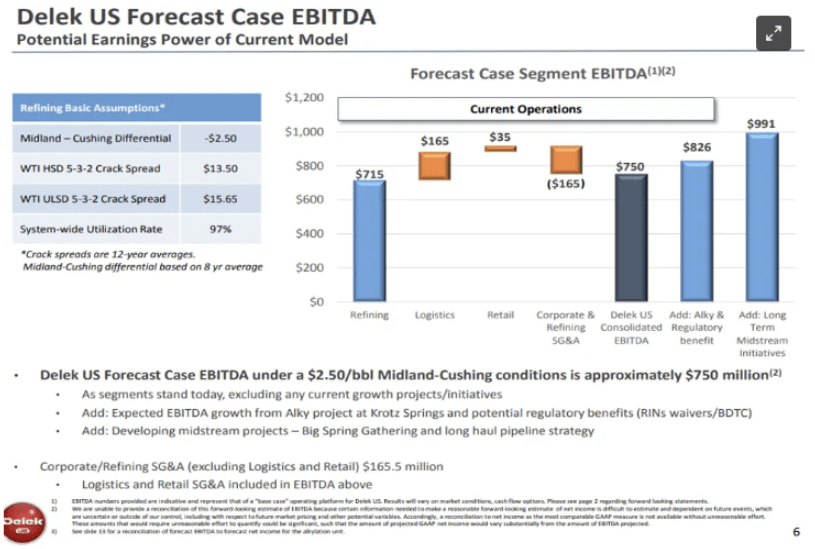

Let’s start with the refining business and its mid-cycle earnings assumption. For one, the company is currently operating at mid-cycle levels, as per management's recent comments. In the Q2 earnings call, management noted that at mid-cycle levels, the company will be earning between $400-500 million in EBITDA. Those estimates already account for corporate costs for the segment. For instance, back in 2018, management also discussed the mid-cycle earnings for the business, given the normalized crack spread levels, and there as well, mid-cycle earnings after corporate costs were at $550 million.

$165 million covers corporate and refining SG&A. Logistics and Retail segments already account for their respective overheads in the chart. (Investor Deck)

In my estimates, I simply take the midpoint of the management numbers, or $450 million in EBITDA, and value the refining business at a 4.5x multiple for a total of $2 billion. For the retail business' mid-cycle level of earnings, I take $50 million, which seems reasonable for the C-store operation given the historical track record (see the table above). I assign a low-end management multiple of 8x to this business, resulting in a total value of $400 million. As another reference point, in January 2024, Sunoco sold 204 C-stores to 7-Eleven for about $1 billion (DK currently has 250 stores). While location differences are important, this deal does demonstrate the potential of DK’s C-store operation. Moreover, back in 2016, DK itself sold its Mapco Express stores for 13.5x EBITDA, so an 8x multiple for current operations seems more than reasonable.

I believe that given the cash flow stability of DKL operations, its current 9% dividend yield valuation is fair. Therefore, for the 79% stake in DKL, I simply take the market value and discount it by 20% due to the stock's low liquidity, arriving at $1.3 billion.

The last remaining piece is the corporate costs for the logistics and retail operation. Since management does not provide the numbers on this, I had to improvise. In the 2019 investor presentation, the company noted that corporate costs and SG&A for the Refining segment were at $165 million. I take that number and subtract it from the reported overall corporate expenses in 2019, which was $275 million (see the financials table above), and I arrive at $110 million. I apply a 10x multiple to this for a total value of $1.1 billion. This is a highly conservative estimate, especially considering the recent corporate cost reductions. However, due to the limited visibility, I feel more comfortable with conservative estimates here. This, of course, makes the thesis even more compelling, with potential surprises to the upside.

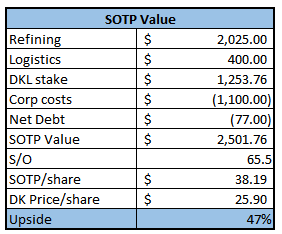

After putting all this together, the SOTP value of DK is $38 per share, representing about a 47% upside from current levels.

My Estimates

To finish up, it's important to note that the company's capex historically was roughly equal to D&A. Recently, the CAPEX levels were slightly elevated due to modernization works on the refining facilities. In 2023, DK completed a major turnaround in its Tyler facility, and now the company plans to largely complete modernization efforts in the Big Springs and Krotz Spring refineries by 2024. The majority of the capex would be spent in 2024 on these two refineries, and once complete, we should see a more normalized level of capex spending in line with D&A. Capex guidance for 2024 is around $330 million, already way below 2023 ($389m) levels due to the completion of the Tyler turnaround. I would expect improved FCF conversion in the coming years, both due to modernization and cost-cutting efforts. This should become especially visible in 2025 once all the facility improvements start to show up.

Investor Deck

In a nutshell, DK is an undervalued energy company with a complex holding structure weighing down on its valuation. Management is clearly aware of this and has been insisting on unlocking the value. Most importantly, while investors are waiting for a potential value-unlocking transaction, they are being compensated by consistent capital returns through both buybacks and dividends.