Brandon Bell

Editor's note: Seeking Alpha is proud to welcome The Antagonist Investor as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Brandon Bell

In this article, I will discuss what Dollar General (NYSE:DG) is doing to improve operating performance, latest trends and what the market seems to be pricing in: a very slow recovery of margins (below historical levels in the long-term), coupled with very conservative growth assumptions (terminal growth at roughly historical CPI, also falling short of DG's historical SSS of +3.5%). In my view, the market seems to be overemphasizing short-term headwinds, and as a result, failing to properly price in the potential of DG, despite its historically strong operational performance and initial signs of improvement of the turnaround plan. Assuming very conservative estimates, valuation could still yield +20% potential upside, with upside risks if management delivers consistent results.

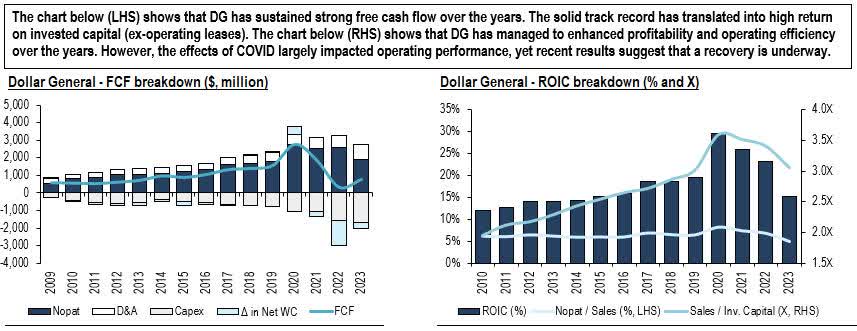

Dollar General is the largest discount retailer in the United States by number of stores, with 19,986 units (+1.4X the number of units of the closest peer, Family Dollar), and it offers everyday low prices (typically <$10) through a portfolio largely concentrated within consumables, accounting for 82% of sales. From 2010 to 2019, the company sustained robust free cash flow generation (average annual growth of ~11%) and high return on invested capital ex-operating leases (from 12.0% to 19.5%), with growth mainly attributed to better operational efficiency.

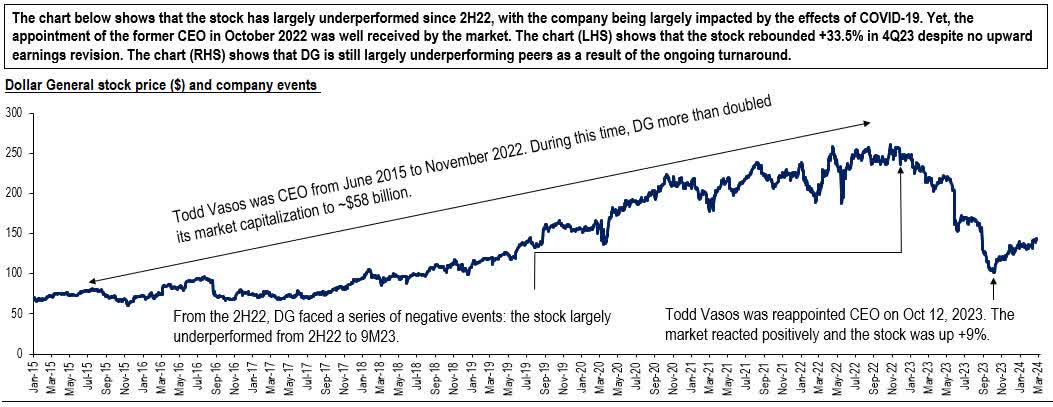

However, the stock has underperformed over the last 1.5 years, with shares falling -58.7% from 2H22 to 2023 lows. This can be largely attributed to the effects of COVID-19 that impacted operating results. The company has recently reappointed the former CEO, and should the new management take corrective action, I believe the stock could experience a strong rebound.

Image created by author with data from Dollar General

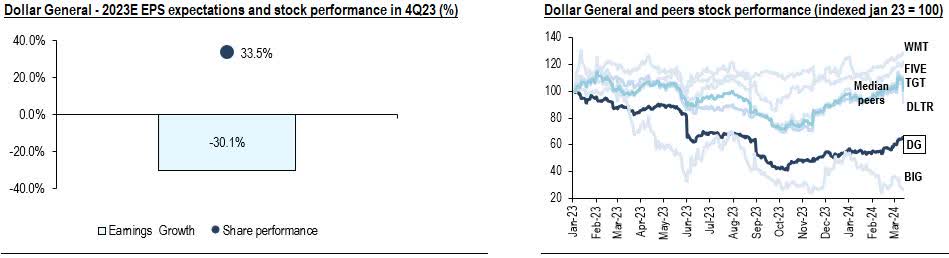

DG operating results have been impacted by the effects of COVID-19, which included a temporary shortage of warehouse capacity, increased shrinkage/damage, and inflationary pressure. Additionally, the company witnessed a notable shift in the product mix, moving away from consumables toward more discretionary categories. These changes further strained the supply chain and added complexity to inventory management and distribution. As a result, Todd Vasos, who doubled the market capitalization (~$58bn) of DG from June 2015 to November 2022, was reappointed as CEO on October 12, 2023. The news resonated well with the market, with the stock soaring +33.5% in 4Q23 after the announcement, despite no upward earnings revision.

Image created by author with data from Dollar General Image created by author with data from Dollar General

The stock was down -5.1% after 4Q23 results, despite +5.8% positive earnings surprise, as investors likely focused on the guidance for the full-year, where headwinds should persist in the 1H24 and a recovery will be centered in the back half of the year. On the short-term, management noted that they expect higher promotional markdowns and shrink to be an ongoing headwind to gross margin in the first part of the year, the latter resulting in a >100bps negative impact in 2023. Also, mix should also add pressure; pre-pandemic sales mix leaned towards consumables, but in 2020 and 1Q21, the mix shifted to the non-consumable category. However, from 2Q21 onwards, the mix reverted to historical trends (consumables), and has been impacting gross margin as essential products command lower margins.

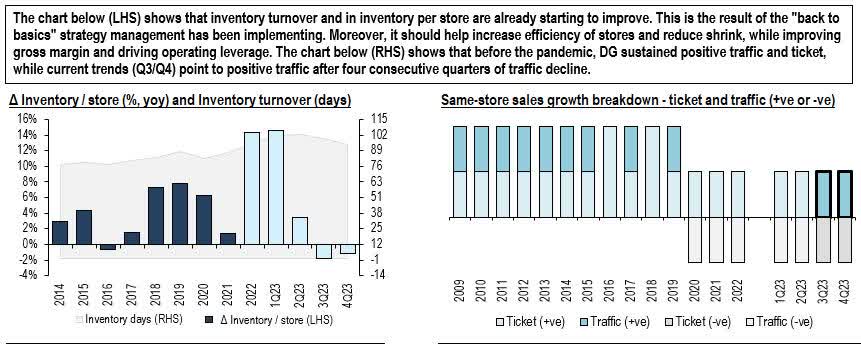

In my view, an improvement in operating performance should come mainly through improved gross margin and greater operating leverage. Management strategy aims to decrease shrink and enhance customer satisfaction across service, on-shelf availability, and convenience. The company is also improving the supply chain by streamlining inventory in distribution centers, increasing inventory turns and minimizing the use of temporary external warehouses for storing products. However, improvements should start to become more visible in the back half of the year and into 2025, as current initiatives should prove as important mitigation levers. Yet, results have already been improving. In 4Q23, the company accelerated market share gains in consumables and decreased inventory on a per store basis for the second consecutive quarter (+14.7% yoy in 1Q23 to -1.8%/-1.1% yoy in 3Q23/4Q23, respectively). Also, on the SSS front, despite recording -1.3% decline in 3Q23, it turned positive (+0.7% yoy) in 4Q23, while traffic was positive in both periods following four consecutive quarters of decline. Management also noted that these trends continued in 1Q24 and remains confident in strong traffic growth in the quarters ahead, hence providing guidance for SSS in Q1 of +1.5% to +2.0%.

Image created by author with data from Dollar General

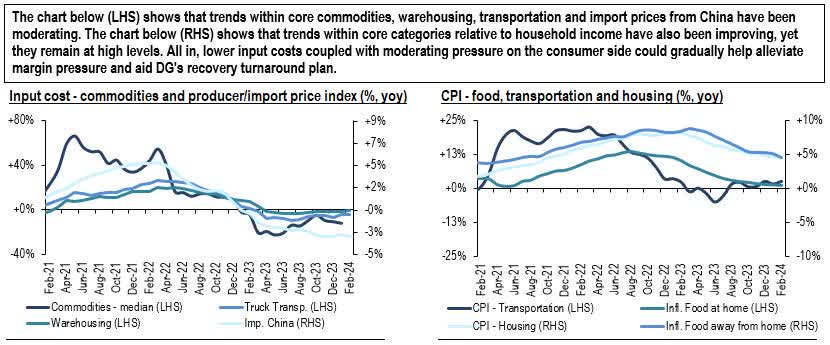

In February 2024, median commodity prices showed a decline of -11.8% yoy, while transportation and warehousing costs were down -4.3%/-0.5% yoy (-4.4%/-1.6% yoy in January 2024, respectively). Furthermore, import prices from China continue to decrease, registering -3.1% yoy (-2.9% in January 2024). On the consumer front, certain categories have also been gradually moderating. In February 2024, food at home inflation, housing, and food away from homeincreased by +1.0%/+4.5%/+4.5% yoy (+1.2%/+4.6%/+5.1% yoy in January 2024, respectively), whereas transportation remains under pressure at +2.8% yoy (+1.7% yoy in January 2024). Cost inflation remains high, but these trends may gradually help alleviate cost pressure on both the P&L/consumer front and support DG's recovery throughout the year. Furthermore, management mentioned in 4Q23 that they are starting to see a trade down across every cohort, another positive trend as it can translate into long-term growth of top-line.

Image created by author with data from U.S. Bureau of Labor Statistics, U.S. Bureau of Economic Analysis, International Monetary Fund, U.S. Energy Information Administration

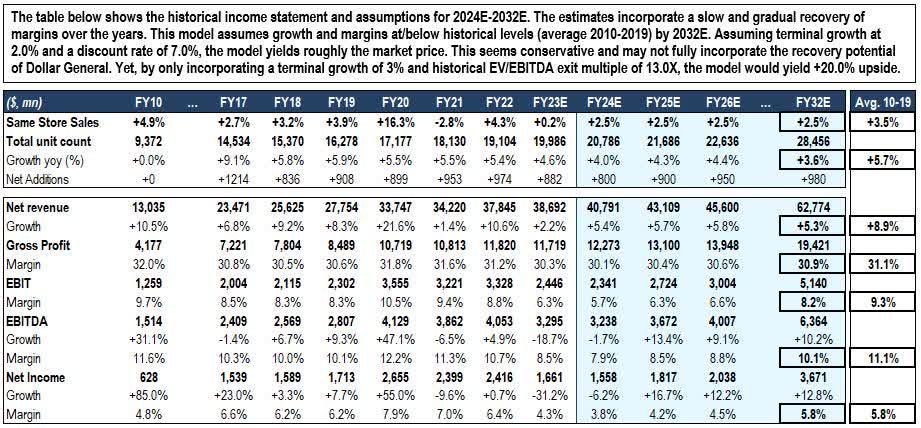

In my view, the market is overemphasizing short-term events in detriment of the long-term potential of Dollar General. Moreover, there are no signs of a structural shift that would suggest that the company cannot deliver historical operating margins of >8% over the medium/long-term. In fact, there are long-term opportunities in shrink reduction, portfolio expansion (i.e., private-label brands and produce), expansion of coolers, global sourcing, inventory optimization, and transportation efficiencies. Nevertheless, at current price the market seems to be pricing in margins at c.100bp below historical levels. In addition, this baseline would only be achieved within the next 9 years and grow at terminal rate of roughly historical average CPI (~2.0%), which is also below historical average SSS of +3.5%.

The stock experienced a strong multiple re-rate (+66%) since the appointment of the new CEO, which came without earnings revisions. In my view, the story is one in which things get worse before they get better; management guided for an EPS in 1Q24 of $1.50 to $1.60 (versus consensus of $1.83), so it is likely that earnings revisions will follow. Important to note, however, that the guidance incorporates a one-off negative impact of $0.50 EPS in 2024 due to higher incentive compensation expense. However, on the medium/longer-term, current price seems to be incorporating very conservative assumptions and disregard the solid track record of the new management. The upside risk, in my view, lies in gradual easing of headwinds in the back half of the year and in increasing visibility of positive results of the ongoing implementation of the "Back to Basics" turnaround strategy. As a result, as this trend becomes clearer, the market may revise earnings to reflect margins at/above historical levels sooner than what is currently priced in. In that case, the market should reprice the stock.

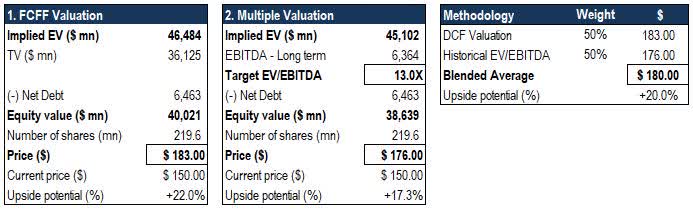

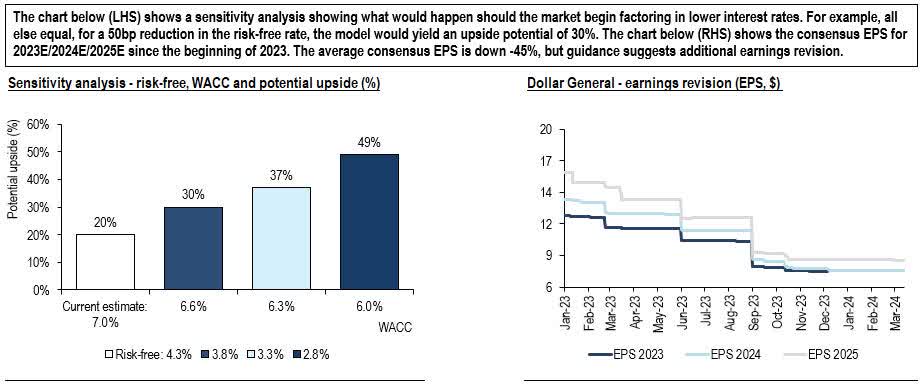

To illustrate how the market seems to be pricing in Dollar General stock, assuming a DCF model (margins below historical levels only at year 9, terminal growth at 2.0%, WACC at 7.0% (cost of equity: 8.5%, cost of debt: 5.5%, tax rate: 25.0%, and risk-free: 4.3%), this methodology yields a price of $148.00, roughly the current price of $150.00. I use a DCF component in the methodology as I believe management's strategy and business model anchored on the expansion of stores provides sufficient ground. Yet, for illustrative purposes, if we also incorporate expectations for growth using a methodology with 50% DCF and 50% exit EV/EBITDA multiple of 13.0X (in-line with historical average), and set our terminal growth to +3.0% (closer to historical SSS of +3.5%), the methodology yields a price of $180.00, or +20.0% potential upside. Lastly, the valuation incorporates a risk-free rate of 4.3%. Yet, should the market begin factoring in lower discount rates in the foreseeable future, this could add upside risks to valuation: for example, all else equal, a 50bp reduction in the risk-free rate could yield +30% potential upside.

Image created by author with data from Dollar General and own estimates Image created by author with data from own estimates Image created by author with data from Dollar General, own estimates and FactSet

In my view, the biggest risk for Dollar General concerns management execution. This is key to the investment thesis as it requires management to deliver consistent results (especially within shrink and inventory management) so the market can fully incorporate the potential recovery of Dollar General, both in terms of free cash flow and margins. With that, earnings revisions and repricing of the stock should follow. Other risks to the thesis rest on whether inflationary pressure (or eventually a recession) would further weight on consumer spending at a point where DG and peers decide to start an intense promotional activity that could hurt margins. Trade restriction, albeit less likely on the short-term, is also a risk considering that a large percentage of the portfolio is exposed to imports (mainly from China), so any trade barrier could disrupt the supply chain and lengthen the recovery process. Lastly, deflation is also a theme that worth tracking. Although recent comments from DG and peers suggest that this is not a major concern at the moment, if this trend gains strength, companies may decide to pass on lower input costs to consumers, and potentially hurt sales.

The current headwinds faced by Dollar General are being fully addressed by the new management through the "Back to Basics" turnaround strategy. In my view, the market is overemphasizing short-term events in detriment of the long-term potential of Dollar General. As a result, the market is not properly pricing in the company, despite the historically strong operational performance and initial signs of improvement. For this scenario to unfold, management must deliver consistent results, with improved inventory management being key to the investment thesis. The short-term will remain volatile, but if management executes according to plan, the market may start reflecting margins at/above historical levels sooner, potentially leading to a repricing of the stock.