Rodin Eckenroth/Getty Images Entertainment

Rodin Eckenroth/Getty Images Entertainment

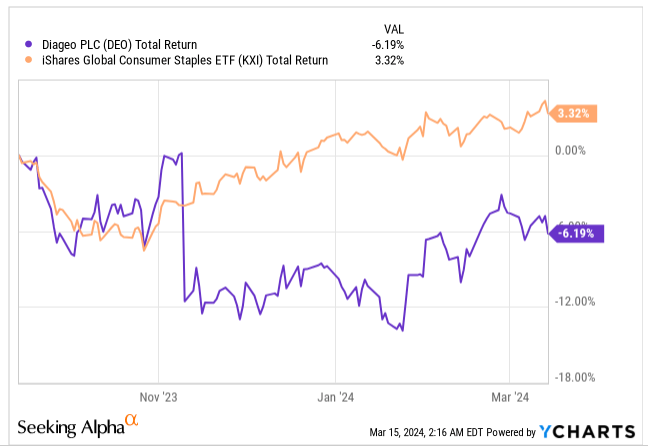

The ADR of Diageo, PLC (NYSE:DEO), one of the top three players in the total beverage market, and the leader in the International Spirits category has proven to be a disappointment of sorts off late. Over the past 6 months, whilst other global consumer staple stocks have managed to eke out steady returns of over 3% on average, DEO has lost ground, giving up 6% of its value.

YCharts

To get some sense of the underperformance, note that DEO’s medium-term organic net sales target is to hit levels of 5-7% p.a., but as of H1-24 (the company follows a June year ending calendar), this metric is down by -0.6%.

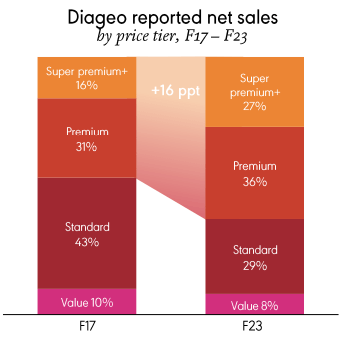

Much of the organic weakness is being driven by what’s happening in their Latin American and Caribbean regions (LAC), where the topline is down by a whopping 23% YoY. Admittedly, this region has had to contend with a strong base effect where the topline was up in double-digit terms last year, but it’s also fair to say that management may have over indexed the COVID super-cycle euphoria back then, leading to a bloating of inventories in the channel (adjustments of which will continue through June 24). Over the last 6 years, DEO management has also been very keen to highlight the underlying theme of premiumisation (super premium and premium categories taking over a larger share of the mix relative to standard and value categories) in the spirits market, but in the LAC region, we currently have the reverse trend of downtrading (particularly in Mexico) which certainly puts a spanner in the works.

H2 presentation

Higher marketing spend, weak volume trends, coupled with a shift to low-ticket items will weigh on the operating profit base as well, and we’ve seen this come off by 5.4% on an organic basis (meanwhile organic operating margins are down by 167bps.

Some investors may also have concerns with the growing level of financial gearing in a high interest rate environment. DEO’s adjusted net borrowings are up by 12% YoY, and currently stand at levels of almost $21bn. Also note that the target leverage ratio (net debt to EBITDA) of 2.9x, is now at the high-end of management’s target of 2.5-3x.

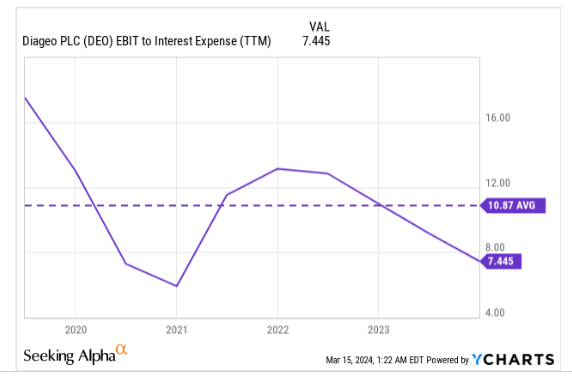

Note that DEO’s net interest charges are up by 36% in H1 on a YoY basis, whilst the ability of its EBIT to cover these interest expenses have been on a downward trend since FY22 and is below the long-term average.

YCharts

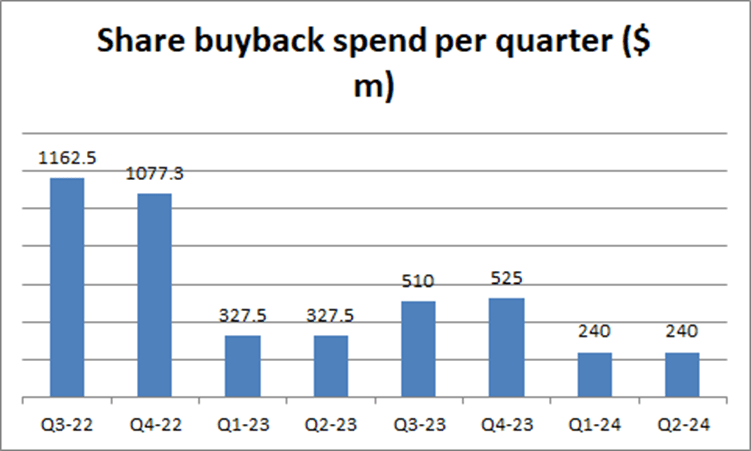

A fair few may also have some concerns over the declining trend of share buyback spend per quarter, particularly at the cheap valuations (more on this later) suggest that it would be an opportune time. Note that over 3 years back they were spending over $1bn per quarter; this year the cadence has slowed to less than $0.25bn per quarter. Looking ahead, one can expect similar ballpark numbers over the next two quarters, as this year’s buyback target is only $1bn.

Seeking Alpha

H1 may not have gone well, but we feel things are not going to get much worse from here, and are more likely to improve.

The run-rate on organic revenue will most certainly improve from the negative level of -0.6%, management suggested that the LAC region will see much lower weakness of - 10 to -20% (compared to the -23% levels seen in H1). Meanwhile their top regional exposure- North America should see “gradual” organic sales growth, whilst other regions such as Europe, Asia Pac, and Africa will also see “continued growth in H2”.

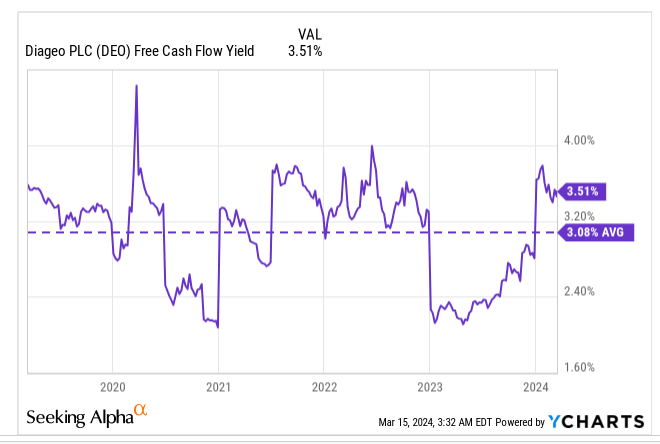

What’s particularly key is that the inventory position (not just in LAC) is expected to be a lot leaner. On the H2 call, the CFO referenced some of the structural changes they’ve made with processes, data analytics, and technology that are likely put the group days in inventory (DIO) in a better spot. Even without the potential inventory adjustments on the anvil, note that FCF had already improved by close to $0.5bn in H1, so much so that the stock is already yielding an FCF figure that is over 40bps more than its 5-year average.

YCharts

Even better FCF dynamics should reflect well on DEO’s high financial gearing. Besides that, we’re also encouraged to note some murmurs around the stake-sale of non-core assets such as Pimm’s, which should also help bring down the leverage.

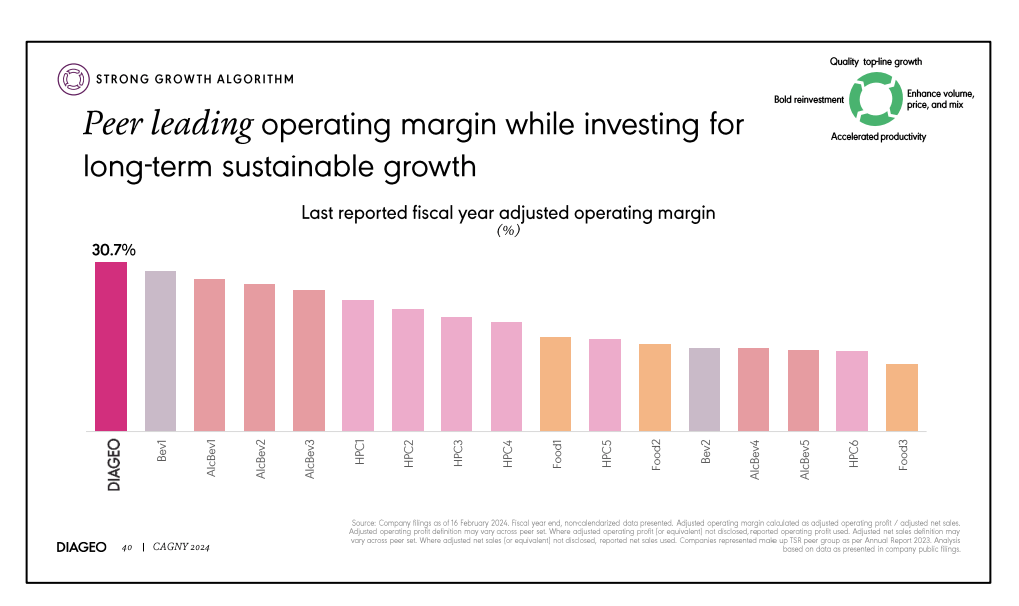

On the operating profit front, it’s worth considering that even though DEO has taken a hit in H1, at 30.7%, it is still best-in-class within the CPG universe.

H2 presentation

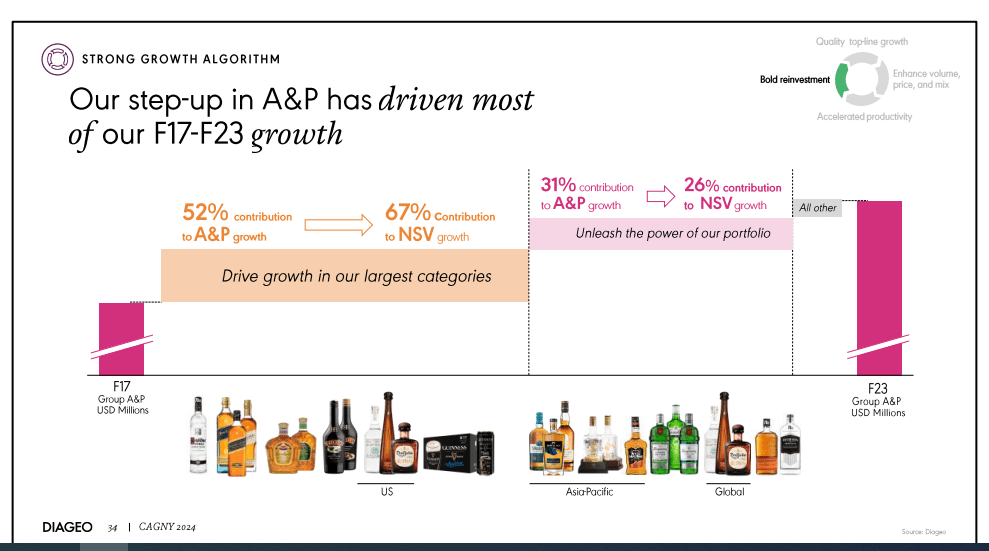

Whilst the LAC impact will ebb in H2, the other major tailwind for margins-advertising & promotional spend (70bps impact on margins in H1) should not be construed as overly negative, as DEO has a recently showed that it can double-down on A&P spend, and then extract solid business growth over time.

H2 presentation

Don’t also forget that DEO is currently in the midst of beating its 3-year productivity target of $1.5bn which should reflect well on the cost base (much of this is supply-chain related). In H1 alone they were able to extract benefits worth $335m, taking the aggregate total to $1.375bn. If they can maintain anything close to the $300m ballpark, they could exceed the cumulative target by close to $200m. Crucially progress here won’t come to a halt by the end of FY24. Through FY25-FY7, the goal is to bring through another $2bn of benefits.

Then, also note that DEO has a long track record of increasing its dividends for 23 years now (more recently over the last 5 years dividends have grown at a CAGR of 4.1%, with the most recent H1 hike coming in at a higher threshold of 5%), and that consistency has also seen it make it to the esteemed international dividend achievers club, which focuses on 50 international stocks (also includes ADRs and GDRs) who have raised their annual cash dividends consistently for 5 straight years.

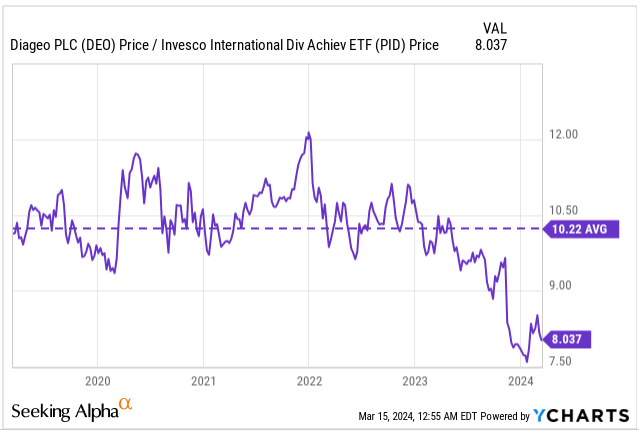

If you’re looking for beaten down candidates in this space which could potentially benefit from some mean-reversion, then DEO certainly should be on your watch list. Over the past 5 years DEO’s relative strength versus its peers from the global dividend achievers space has averaged around 10.22; now it is around 21% lower than the mean.

YCharts

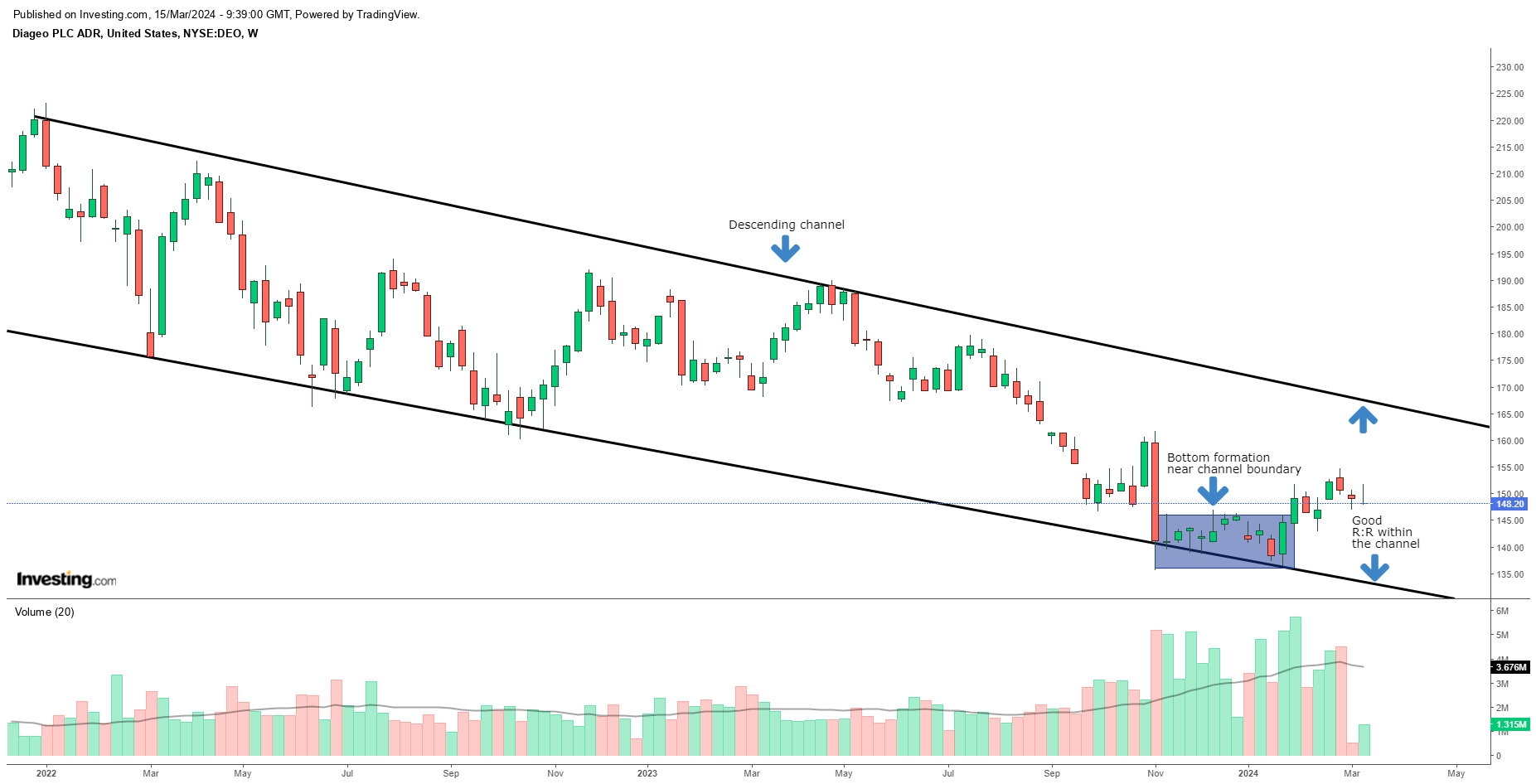

Diageo’s weekly price imprints over the last three years or so have taken place within a certain descending channel (area within the two black lines in the chart below). From Nov 2023 to Jan 2024, we saw the price flatten out near the channel boundary, implying an intermediate bottom. After that over the past two months the stock has built up some decent bullish momentum which has encouragingly not also gone over the top.

Investing

Now, if one were to contemplate a long position at CMP, using the two boundaries of the channel (currently at $132 and $168) as pivot points, you’re looking at fairly encouraging reward to risk of 1.39x.

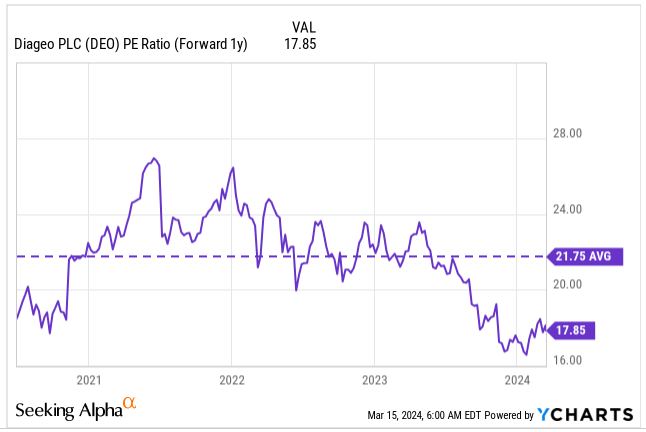

Finally, also note that the stock’s forward P/E valuations, look rather attractive compared to its historical average. Based on YCharts consensus EPS of $8.3 for FY June 2025, the stock can now be picked up at a 18% discount, relative to its 5-year rolling average of 21.75x.

YCharts

To conclude, we think DEO would represent a good BUY at these levels

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.