Jacob Wackerhausen/iStock via Getty Images

Jacob Wackerhausen/iStock via Getty Images

Dynatrace (NYSE:DT) is a cloud-based observability and security platform that has severely underperformed the indices in YTD. The company recently announced its Q3 FY24 earnings report, where we see that revenue is slowing down sequentially. This has undoubtedly driven investors away from the stock.

However, I believe that the sell-off has created a unique opportunity, as the company’s management is making investments in the right direction by strengthening its partnerships with global system integrators (GSIs) and hyperscalers, while building its internal sales team to effectively target enterprise customers to deepen product adoption. This is also happening at a time when cloud spending is expected to grow in 2024 and companies increasingly consolidate their siloed, ad-hoc solutions into a unified observability platform. Coupled with the management’s financial discipline, I believe the company is well-positioned to drive sizable returns of at least 29% over a 5-year investment horizon. As a result, I would rate this stock a “buy” at current levels.

Dynatrace is an observability and security platform that utilizes artificial intelligence to enable organizations to better monitor, analyze, and optimize their IT operations and deliver software faster for better business outcomes.

Dynatrace’s platform is integrated with multiple cloud ecosystems, including AWS, Azure, Google Cloud, VMware Tanzu, and others. The company leverages its proprietary real-time mapping system and an open artificial intelligence engine called Davis to simplify the complexity of multi-cloud environments by providing visibility and actionable insights to application and operation teams.

The company utilizes a combination of direct sales and a network of partners to acquire customers. This approach enables Dynatrace to leverage its own sales force while also tapping into the expertise of partner organizations to expand its market reach and drive growth.

In terms of its business model, the company operates on a subscription-based pricing model, with subscription revenue expected to account for 95% of its total sales in FY2024.

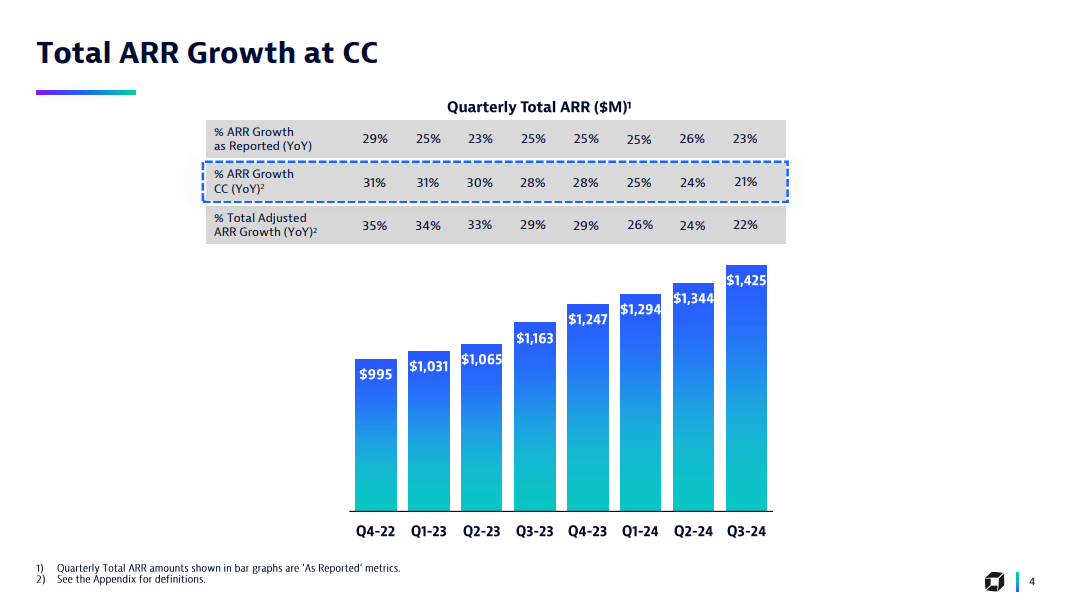

Dynatrace recently posted its Q3 F24 earnings, where revenue grew 21% YoY to $365M, beating analyst expectations by 2.2%. Subscription revenue contributed 95% of the total revenue. The company added 209 new logos in Q3, while the average ARR per new logo in the trailing 12 months (TTM) grew 17% to $140,000. There is no doubt that the company is seeing a sequential slowdown in revenue growth QoQ.

Q3 FY24 Earnings Slides: Dynatrace's Revenue growth

However, I believe that the company should be ready to turn the tide, based on the management’s commentary during the earnings call and the strategic initiatives that the company is embarking on to strengthen ties with GSIs and hyperscalers to effectively win large deals and drive adoption.

During the earnings call, the management sounded optimistic about the traction they are seeing so far with their investments with GSI partners that include Accenture (NYSE:ACN), Deloitte, DXC (NYSE:DXC), and Kyndryl (NYSE:KD). According to the management, it was through one of the GSI partners that they successfully closed a seven-figure win with a social media platform in Q3. At the same time, the company is also investing in targeted internal sales capacity to efficiently target enterprises, which would allow it to optimize its Annual Recurring Revenue (ARR) per customer with deeper adoption, thus allowing it to gain higher economies of scale.

The company reported a Net retention rate (NRR) of 113% in Q3. And as per management, there is room for growth, as can be seen below in the commentary from Jim Benson, CFO at Dynatrace. Therefore, given the management’s strategic vision, I believe that the company is moving in the right direction by building partnerships with GSIs and strengthening its sales team, which should enable it to deepen its market position among enterprise customers.

“When we think about our net retention rate, there are three areas that drive customer expansion: one, growth of existing observability workloads; two, adding new observability workloads; and three, cross-selling new solutions like log management, analytics, or application security. We estimate that our customers are observing only 20% to 30% of their workloads today. We believe these three growth vectors provide us with a significant opportunity to expand further within our installed customer base.”

Finally, software and IT services segments are expected to see double-digit growth in 2024, as per Gartner at 13.8% and 10.4%, respectively, as companies continue to accelerate their workloads to the cloud. Simultaneously, as companies increasingly consolidate their existing observability tools on a unified platform, I believe it creates a unique opportunity for Dynatrace to turn the tide in the coming quarters, coupled with its partnerships with GSIs.

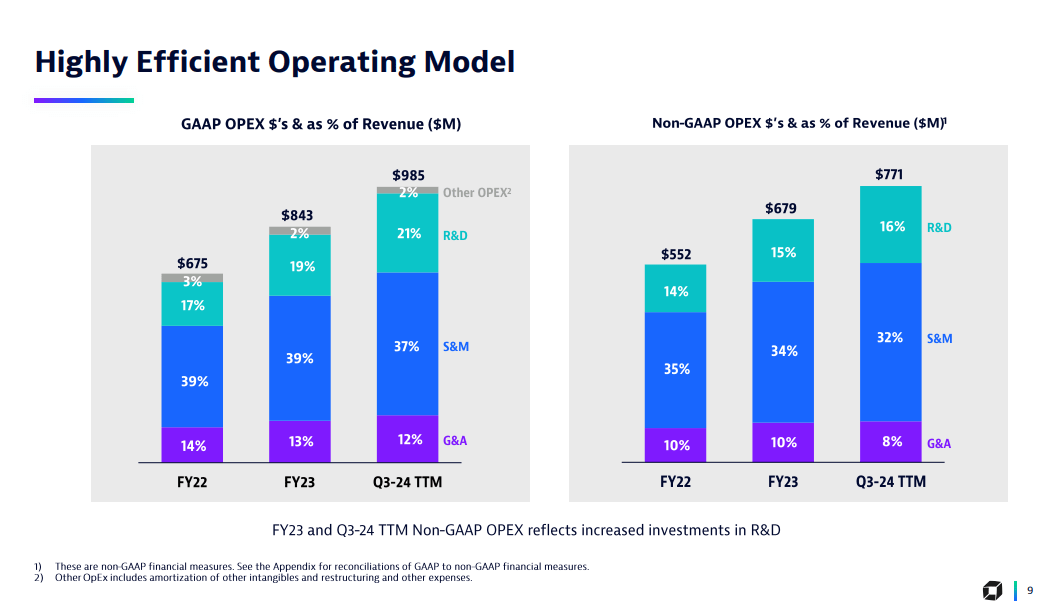

Shifting gears toward profitability, Dynatrace management is laser-focused on expanding margins. As of Q3 FY24, the company generated $105M in non-GAAP operating income, representing a margin of 29% and an improvement of 200 basis points (bps) from the previous year. The main driver for the expansion in margins can be attributed to the narrowing in operating expenses relative to revenue, especially in sales and marketing.

Q3 FY24 Earnings Slides: Dynatrace's improving profitability

Looking forward, the management revised revenue guidance for FY24 by 100 bps to $1.42-$1.43B. This would represent a YoY revenue growth rate of 23%. At the same time, subscription revenue growth estimates have also been revised upwards by 150 bps to $1.35-$1.36B. As for profitability, the company is expected to generate $388-$393M in non-GAAP operating income, which was also revised upward, representing a margin of 27.25–27.5%, compared to 25% in FY23.

Dynatrace is in direct competition with Datadog (NASDAQ:DDOG), which has been a growth leader in the data observability space. So far, I believe that Dynatrace has seen success by penetrating into legacy players’ market share, as can be seen in the Gartner Magic Quadrant Analysis. While Cisco (NASDAQ:CSCO) has demonstrated its intentions to compete with Dynatrace by acquiring Splunk (NASDAQ:SPLK), I believe that the rapid scale of Dynatrace’s product iteration has allowed it to launch products that are highly differentiated from other legacy players in the market. At the same time, Dynatrace continues to mirror Datadog when it comes to emerging areas of the target market, such as DevSecOps and AI Ops. As a result, I believe that Dynatrace is well positioned given the company’s robust pace of innovation and product delivery plans, although this would require the company to continue to invest heavily in R&D, which could suppress margins should we see a demand slowdown.

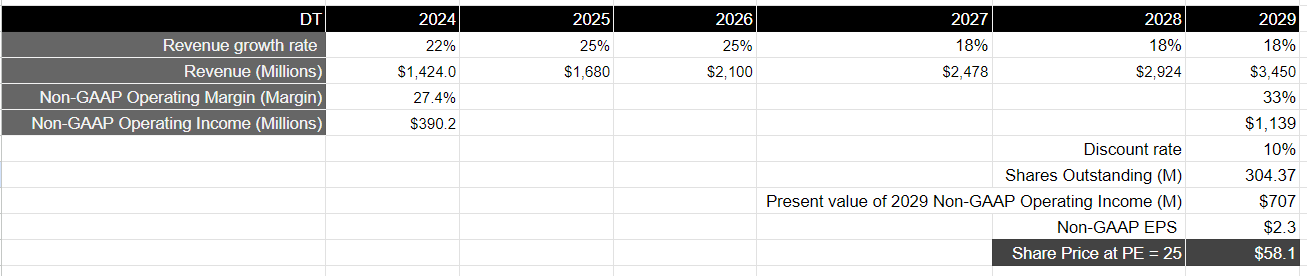

Assuming that Dynatrace is able to drive revenue growth in the mid-20's until FY26, followed by a normalization in the higher teens until FY29, it should produce a total revenue of approximately $3.45B. I believe the company should be able to achieve it, as it drives deeper market penetration, driven by its rapid scale of innovation as well as its partnership efforts with GSIs.

In the meantime, I believe that the management can continue to drive higher margins, given its track record of operational excellence so far. Plus, as the company drives deeper adoption of its products through existing and adding new observability workloads and successfully cross-selling new solutions, it should gain higher economies of scale. As a result, I believe the company should grow its non-GAAP operating margin to 33% by FY29, which would translate to a present value of $700M in non-GAAP operating income when discounted at 10%.

Taking the above assumptions into consideration, I believe that the forward price-to-earnings ratio for Dynatrace in FY29 should be at least 1.5x the forward multiple of the S&P 500, where its companies grow their earnings by 8% annually on average over the last 10 years, with a forward multiple in the range of 15–18. This would result in a price target of $58 for Dynatrace, looking at a 5-year investment horizon, which would translate to an upside of 29% from its current levels.

Author's Valuation Model

I believe that the sell-off in Dynatrace has created an amazing opportunity for long-term investors. While short-term investor concern remains on sequential revenue slowdown, I believe the investment case remains intact when we look at the big picture, where we see the company driving strategic initiatives, strengthening its partnerships with GSIs to deepen market share, and expanding its profitability while building robust solutions at pace.