Eoneren

Eoneren

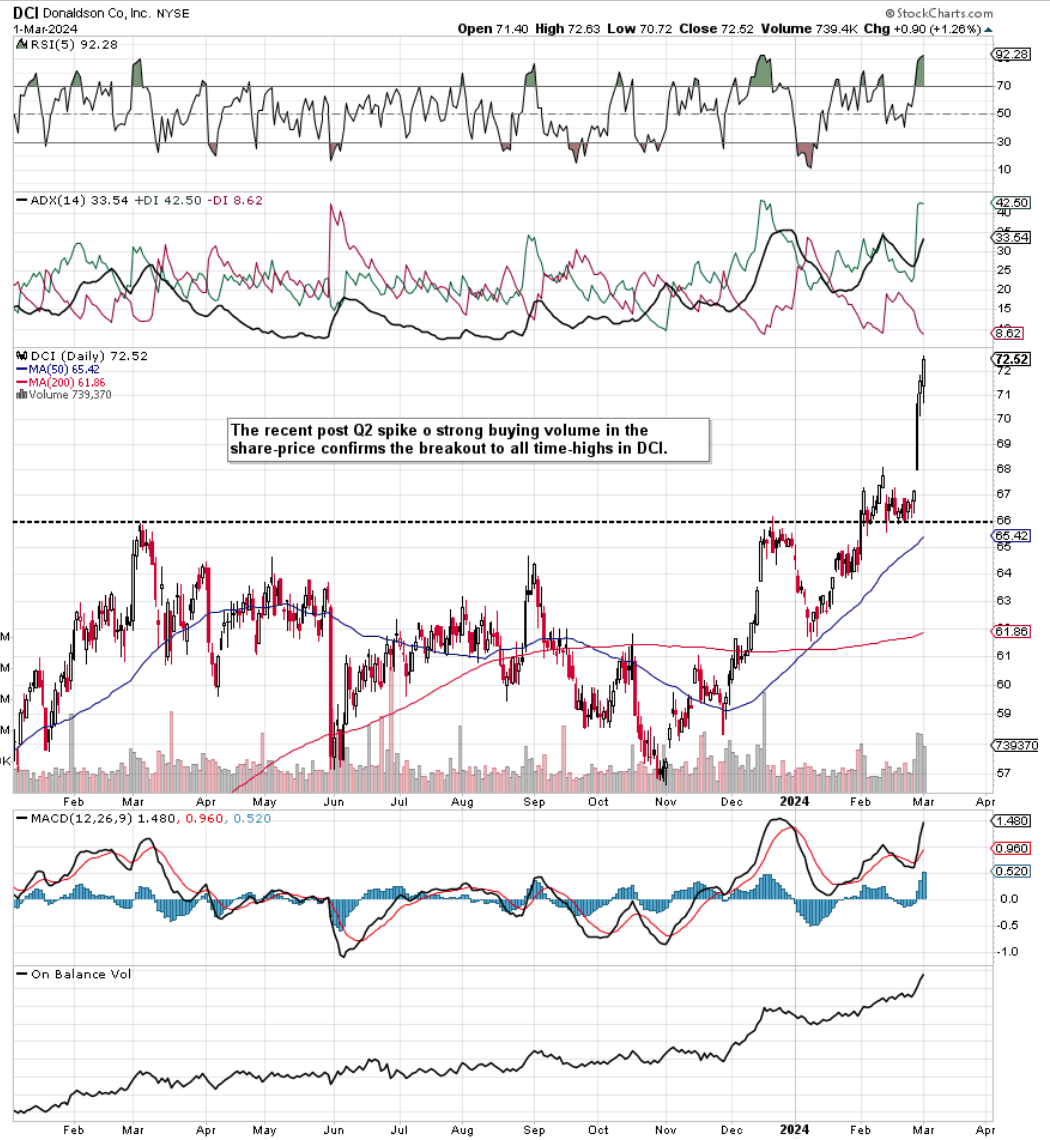

We wrote about Donaldson Company, Inc. (NYSE:DCI) (Specialty Industrial Machinery) in September of last year when we implied that any sustained downward in the stock would not gain significant traction to the downside. Given that a bearish decline in the stock was in motion at the time, we rated Donaldson a 'Hold' until further developments. With shares trading at just above $62 a share at the time, the downtrend did indeed continue until late October, when shares finally bottomed just above $57 a share. Since then, shares have entered rally mode, tacking on approximately $15 a share or 25%+ which sees shares currently trading above $72 a share.

Recent bullish action in Donaldson Company gives credence to our price target of approximately $90 a share, which we evaluated in May of 2023. In fact, given how shares spiked on the release of the recent Q2 earning beat, we are upgrading our rating to a 'Buy' for the following reasons. First though, taking into account our valuation projection for Donaldson ($90 per share) based on a popular dividend discount model plus the fact that the stock's recent breakaway gap or runaway gap was driven by strong volume, we believe investors can place a low-risk long-entry into Donaldson stock at present.

What we mean by this is that the underside of the post-Q2 upside gap comes in at approximately $68, which is roughly 6% below the stock's prevailing share price. Now, given that this most recent up move also confirmed a breakout in the stock to all-time highs, if the breakout is for real, shares of Donaldson have no business dropping below the ($67 to $68 level) going forward. Therefore, investors can buy stock and subsequently place a stop-loss just below the underside of the recent upside gap, providing a low-risk entry into a proven dividend aristocrat.

Donaldson Company Post Q2 Spike To The Upside (StockCharts.com)

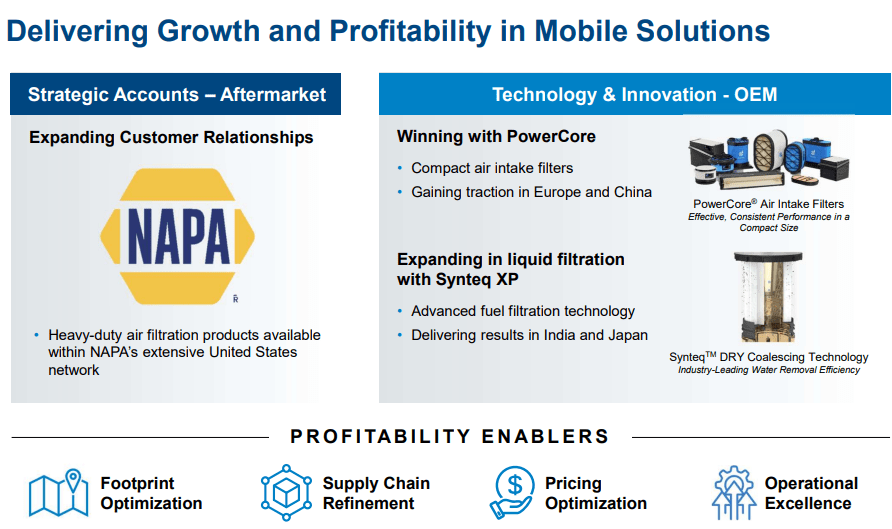

What investors need to digest here is that Q2 gains this year did not come about solely from pricing, but more so from volume gains (demonstrating increasing demand for the company's technology). In particular, a strong showing in Aftermarket (buoyed by strength in both independent & OE) powered sales in the Mobile Solutions segment to $550 million for the quarter. As we can see below, Donaldson has plenty of growth triggers that can keep Mobility growing aggressively. Whether this be expanding relationships (such as NAPA) in Aftermarket or realizing the potential of the company's Synteq XP advanced fuel filtration expertise in liquid, management's priorities concerning footprint optimization & operational excellence are bound to result in sustained growth given the present state & fundamentals of respective end-markets.

Donaldson Mobile Solutions Fundamentals (Seeking Alpha)

We believe more share-price gains are on the cards for Donaldson because of the strong fundamentals of all three of the company's operating segments (Mobile Solutions, Industrial Solutions & Life Sciences). Sales increased by 6% in Q2 compared to the same period of 12 months prior, coming in at $877 million for the quarter. Earnings per share of $0.81 came in 8% higher over Q2 of fiscal 2022 and beat the consensus estimate by a large $0.07 per share.

Industrial & Life Sciences segments grew by 7% & 6%, respectively, in the quarter, where underlying trends point to sustained growth in Industrial Filtration Solutions (due to growing market share) as well as a long-awaited upturn in disk drive sales. Furthermore, the sheer scale of the company's therapy pipeline in Life Sciences leads us to believe that a significant number of advanced life-changing offerings will be brought to market over the forthcoming years. (sustained growth)

In inflationary times, many companies find it very difficult to protect profitability (bottom-line earnings) even in the face of robust top-line growth. However, Donaldson reported gross margin of 35.2% in its recent second quarter, which was a 70 basis point improvement over the prior year. This enabled the company's net profit margin to come in at 11.25%, which is well ahead of the corresponding trailing 12-month average of 10.82%. Therefore, concerning being able to grow market share in its segment consistently, Donaldson's above-average margins compared to the sector in general demonstrate a key advantage over the competition for the following reason.

Considering that $568+ million made up Donaldson's cost of goods sold in Q2, it was encouraging to see an increase in gross margin in the quarter. In essence, the company's rising sales continue to compensate for the higher costs, all things remaining equal. Gross margin in inflationary times is usually the worst-hit metric on the income statement, but Donaldson continues to buck the trend here. An elevated gross margin means that income & cash flow are being protected on the back-end. Suffice it to say, the bigger the divide remains between Donaldson's gross margin & its peers, the more aggressive Donaldson can be with its investments on a relative basis, which should result in sustained market-share growth in the long run. Incidentally, management hiked its full-year bottom-line guidance to approximately the $3.28 mark.

The macro-picture brings the biggest risk to Donaldson's financials, no more so than the Chinese market, as we learn from the CEO's comments below. Whether stagflation in China is a sign of things to come or a lagging indicator remains to be seen, but growth acceleration will undoubtedly be more favorable for Donaldson if this key market can begin to cooperate.

The market continues to be very challenging. Sales were approximately flat versus 2023 and increased 3% in constant currency. Aftermarket showed particular strength in the quarter, offsetting significant declines in first-fit. It is important to note that while year-over-year performance improved this quarter, the prior year's results were negatively impacted by COVID lockdowns and the inclusion of Chinese New Year a year ago. This resulted in fewer shipping days in the prior year period.

Furthermore, if the macro picture were to break down somewhat, investors have the luxury of trading a stock that just recently broke out to all-time highs. Therefore, that stop-loss should most certainly be obeyed where long positions should be liquidated if indeed support gets broken.

To sum up, we are upgrading our rating on Donaldson due to the company's strong fundamentals in all three of its operating segments, its growing margins, and encouraging forward-looking earnings revisions. Let's see if the momentum can continue. We look forward to continued coverage.