BalkansCat

BalkansCat

BNP Paribas SA (OTCQX:BNPQF) is currently offering a high dividend yield that is sustainable over the long term, and its valuation is not demanding compared to peers, making it a good income play right now for long-term investors.

BNP Paribas is a French bank, being one of the largest banking groups in Europe and across the globe. At the end of 2023, its total assets were above $2.8 billion, a level that is close to HSBC Holdings (HSBC) and higher than other European peers, such as Credit Agricole (OTCPK:CRARY), Societe Generale (OTCPK:SCGLY) or Deutsche Bank (DB). Its current market value is about $75 billion, and it trades in the U.S. on the over-the-counter market.

BNP currently operates in about 65 countries across the globe and has some 195,000 employees, spread across its operations in retail and commercial banking, specialized financing, corporate and investment banking, asset and wealth management, and insurance.

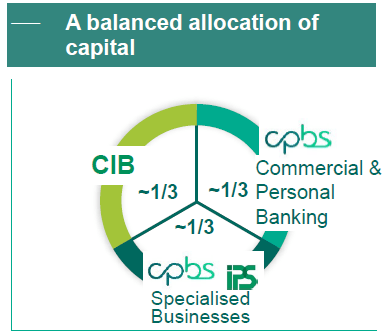

Its business is organized into three main business units, namely:

From a capital perspective, BNP has a very balanced allocation between its three units, a profile that it wants to maintain over the long term.

Capital allocation (BNP Paribas)

Its business is well diversified across its different segments, even though retail and corporate and investment banking can be considered its ‘core businesses’. Indeed, its largest segment is retail banking, being responsible for about one third of its total earnings, with France, Belgium, and Italy being its most important retail markets.

While these markets are relatively concentrated and there are some barriers to entry for new players, leading to attractive profitability levels for established banks, these are also countries with a high penetration of the banking system and relatively low economic growth prospects. Therefore, its international operations, such as in Poland or Turkey, have better long-term growth prospects, but should maintain a relatively low weight within the group.

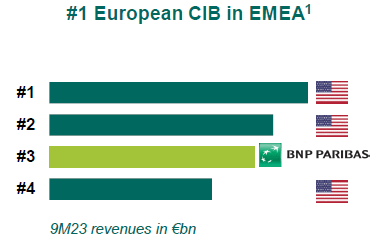

In Corporate and Investment Banking, BNP has improved considerably its competitive position over the past few years, being nowadays one of the most competitive banks in Europe and one of the few that still aim to compete with the U.S. investment banks. Indeed, historically Deutsche Bank or Credit Suisse were the European banks that tried to compete with U.S. peers, but fundamental issues led to a much weaker position, and currently in my opinion, BNP Paribas has now a strong position in CIB and is one of the best European banks in this segment.

This is also seen in its leadership position in Europe, Middle East and Africa measured by revenues in this segment, with BNP being the only European bank among the four leading banks in this region.

CIB rankings (BNP Paribas)

While this segment can be volatile because it’s quite related to volumes in the capital markets, BNP has a diversified business model, allowing it to not be overly exposed to short-term issues. This is a business profile more similar to JPMorgan (JPM) for instance, which also balances a strong retail and commercial banking presence with investment banking.

Due to its large size and exposure to Europe, BNP growth prospects aren’t particularly impressive over the long term, thus much of its earnings growth should come from market share gains in its most important segments and efficiency improvements, through cost-cutting initiatives and digitalization of its processes to improve profitability.

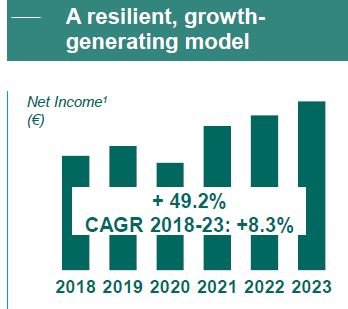

Despite that, the bank has a positive track record over the past few years, growing its earnings at high-single digit rates over the past five years, as shown in the next graph. This means BNP’s fundamentals are solid, a trend that I expect BNP will be able to maintain in the near future.

Net income (BNP Paribas)

Regarding its financial performance, BNP has delivered a solid performance over the past few years, with the only exception being 2020 due to the pandemic. More recently, its results were also boosted by higher rates in Europe and in the U.S., even though BNP is not among the banks more geared to rates.

Indeed, in 2023, its revenues were up by only 3.3% to nearly €47 billion, which is not a great outcome compared to other European banks during the same period. As I’ve analyzed recently on Credit Agricole, French banks are not much geared to rates due to some specific issues of the French banking system, namely regulation regarding deposit rates. This is a headwind for net interest income growth in its most important retail market, which justifies BNP’s muted revenue growth over the past year. By segment, its Commercial, Personal Banking & Services division performed better, reporting revenue growth of 4.3% YoY, while CIB (+0.6% YoY) and Investment & Protection Services (-3.8% YoY) were the laggards.

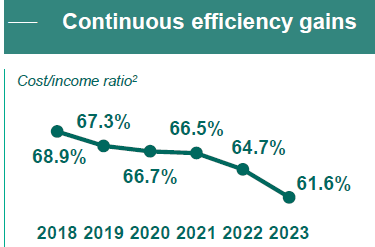

Regarding costs, despite the inflationary environment and pressure to raise wages across its most important markets, BNP reported strong cost control given that its operating expenses declined by 1% YoY, to €29.5 billion in 2023. Its cost-to-income ratio was 61.6%, a level that is above the sector’s average, but has been improving over the past few years, showing that BNP’s measures to improve efficiency are bearing fruit.

Cost-to-income ratio (BNP Paribas)

Another positive factor for its earnings growth has been its sound credit quality, given that its cost of risk ratio has been stable over the past few years, with the exception of 2020 when management increased provisions in a prudent way. In 2023, its provisions amounted to €2.9 billion (-3.2% YoY) and its cost of risk ratio was 29 basis points (bps), which is below its annual target of below 40 bps, showing that credit quality has remained resilient during a tough period for individuals and corporates, due to the cost of living crisis, higher rates, and the inflationary environment.

Its net income for the year was €11.2 billion, up by 14% compared to 2022, and its earnings per share amounted to €9.21 (+18% YoY), a higher increase than its net income due to the share buyback program executed in 2023. Its return on tangible equity, a key measure of profitability in the banking sector, was 11%, a good level of profitability compared to peers.

This is close to its 12% target by 2025, showing that BNP’s profitability is on a good level and further improvements should come mainly from improved efficiency, as rates are expected to come down in the coming months, which will be a headwind for revenue growth in 2024 and 2025.

Regarding its capital position, BNP’s CET1 ratio was 13.2% at the end of 2023, above its internal target of about 12-12.5% over the next couple of years, thus the bank has a good buffer to distribute a large part of its earnings to shareholders.

Indeed, its capital return policy is to distribute about 60% of its annual earnings to shareholders, through dividends and share buybacks.

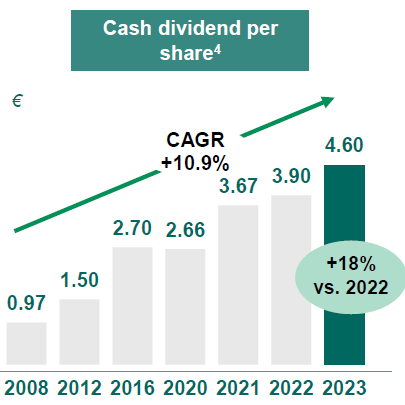

Its last annual dividend was set at €4.60 per share, to be paid next May, an increase of 18% YoY. Investors should note that, like many European companies, BNP only pays one dividend per year, which can reduce somewhat its income appeal. On the other hand, at its current share price, BNP offers a forward dividend yield of about 7.4%, which is quite attractive to income investors.

Dividends (BNP Paribas)

While sometimes a high dividend yield can be a warning sign of poor sustainability, this is not BNP’s case given that its dividend payout ratio was only 50%, thus its dividend is clearly sustainable. On top of that, BNP also announced a share buyback program of more than €1 billion to be performed during 2024, enhancing even further its shareholder remuneration.

BNP Paribas is a solid bank in Europe and has an interesting position in the CIB segment, while on the other hand it’s not much geared to rates. This was somewhat negative over the past few quarters, but now that rates are expected to gradually come down, this may lead to more stable revenues and earnings for BNP in the near future than for many of its European peers.

This weaker growth in recent quarters seems to justify its current discounted valuation, considering that BNP is trading at 0.6x book value while the sector is trading closer to book value, a valuation that is in-line with its historical long-term average. Therefore, I see BNP Paribas SA's high dividend yield as the main attractive feature of its investment case, considering that it’s yielding above 7% and its dividend is sustainable over the long run.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.