blackdovfx

blackdovfx

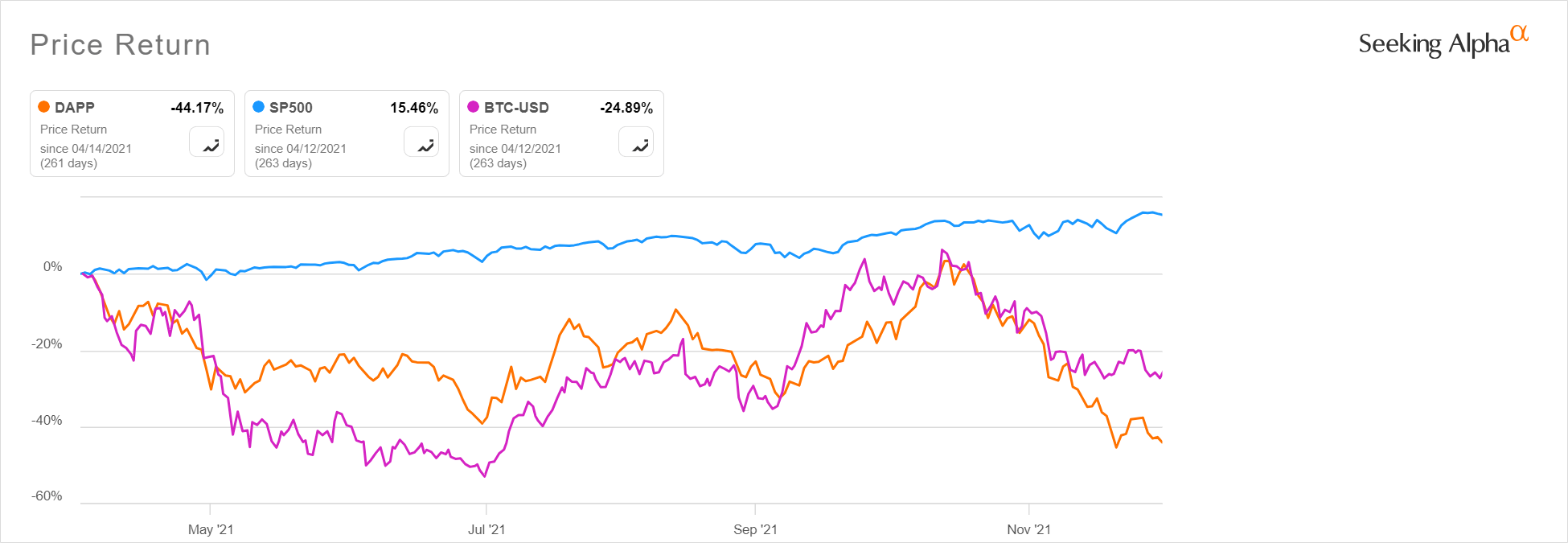

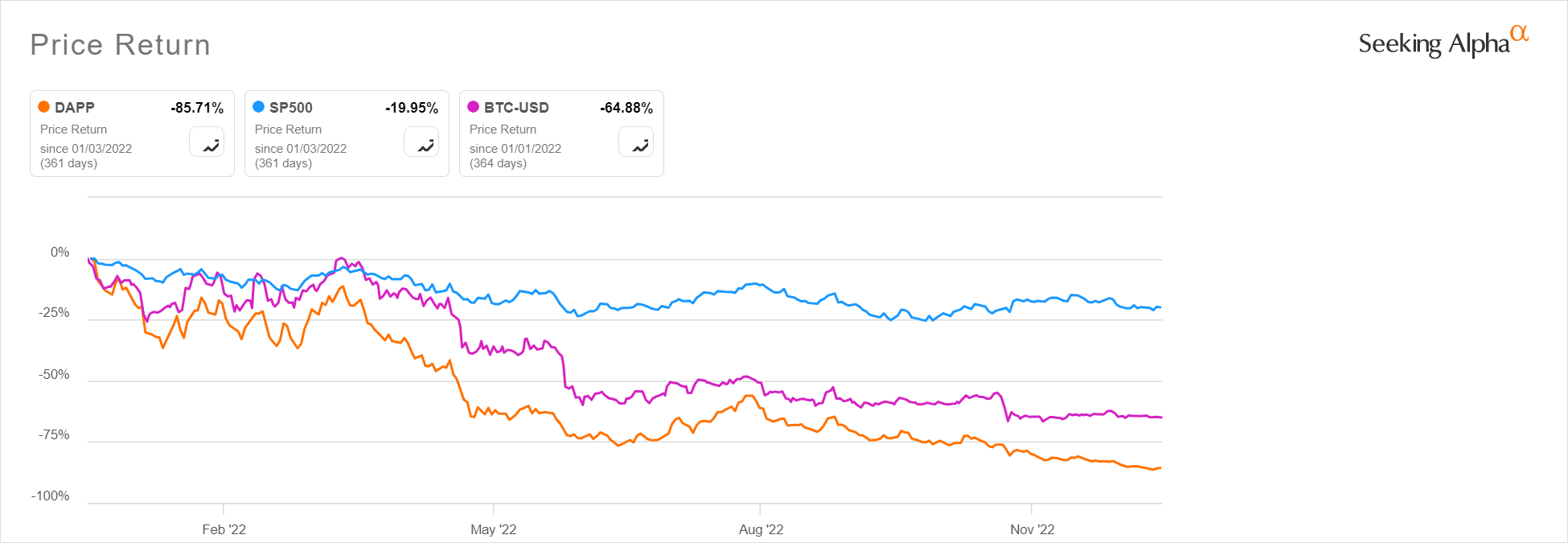

The VanEck Digital Transformation ETF (NASDAQ:DAPP) (the "Fund") began trading on April 12, 2021. Its timing could not have been much worse. The crypto bear market started in earnest in the fall of 2021, causing the Fund to fall more than 40% in 2021. That large decline was followed by a further decline in 2022 of over 85%. See the charts below, which also compare this exchange-traded fund ("ETF") against the S&P 500 and Bitcoin (BTC-USD) ("Bitcoin") for 2021 and 2022, respectively.

2021

Seeking Alpha

2022

Seeking Alpha

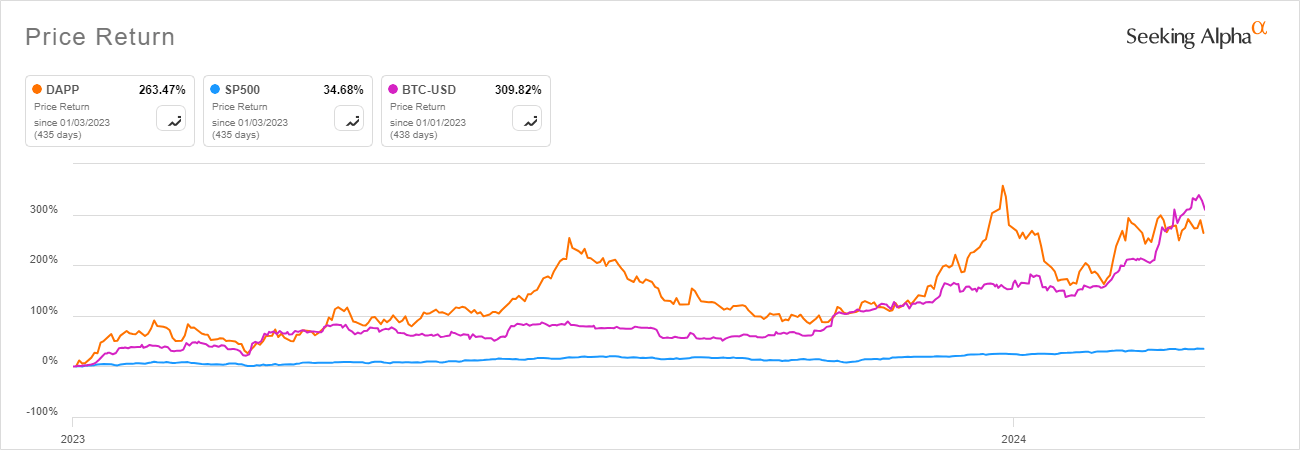

From 2023 through March 15, 2024, the Fund has had a material bounce, up more than 250% during the period (see chart below), but it is still not even close to breaking even since its inception.

January 1, 2023 to March 15, 2024

Seeking Alpha

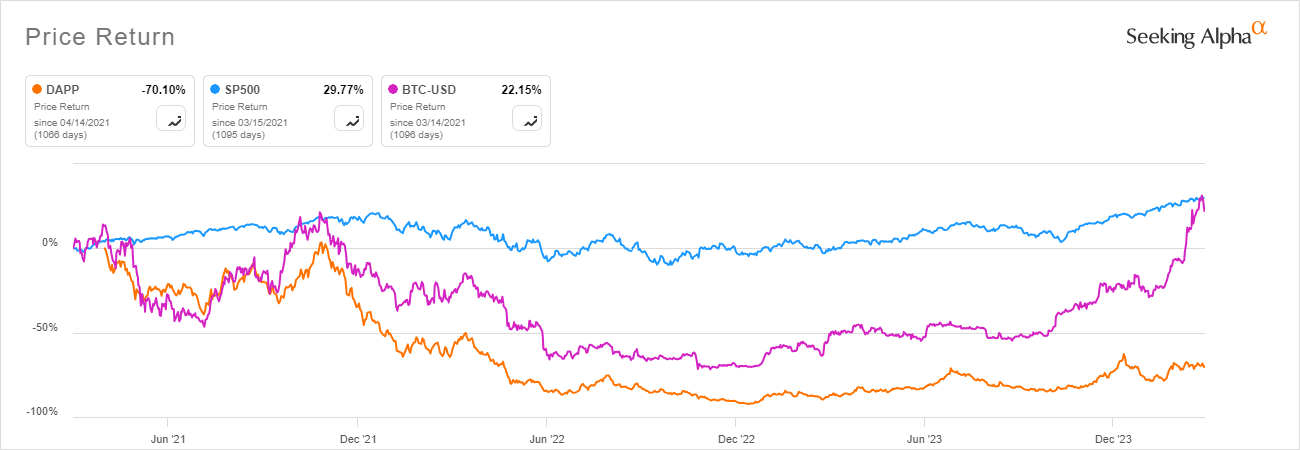

Total cumulative loss since inception is 70.10%, as shown in the chart below. Notably, Bitcoin has fared much better than the Fund.

Seeking Alpha Seeking Alpha

Needless to say, in its brief history, this is a volatile Fund that is not for everyone. It is a HOLD at best in my view.

Presently, I would not be buying the Fund. In fact, I would not be buying any blockchain-related funds that are passively managed. The blockchain industry is not mature enough yet to successfully invest in an index. In my view, you are better off investing in an actively managed ETF, like BLOK, rather than passively investing. Alternatively, and perhaps even better, just buy Bitcoin and HODL.

Additionally, I am not a fan of the Fund because it is too concentrated, adding risk and volatility to an already super-volatile ETF. The Fund is also too exposed to over-priced companies and unprofitable companies, which I will discuss in some detail below.

According to its website, the Fund seeks to track the price and yield performance of the MVIS Global Digital Assets Equity Index (the "Index"). The Index tracks the performance of the largest and most liquid companies in the digital assets industry. It is a modified market cap-weighted index, meaning it only includes companies that generate at least 50% of their revenue from digital asset services and products, covering at least 90% of the investable universe of such companies.

Per the Prospectus of the Fund (the "Prospectus"), the Fund is non-diversified under the Investment Company Act of 1940. The Fund's assets under management are approximately $100 million, according to the Seeking Alpha quote page.

The expense ratio for the Fund is 0.51%. This is among the higher expense ratios in the space for a passive product. Other passive competitors include the Fidelity Crypto Industry and Digital Payments ETF (FDIG) ("FDIG") at 0.39%; and BlackRock's passive offering, iShares Blockchain and Tech ETF (IBLC) ("IBLC"), at 0.47%. Meanwhile, the management fee for the Amplify Transformational Data Sharing ETF (BLOK) ("BLOK"), an actively managed competitor ETF, is 0.75%.

Below I compare the Fund to three competitor ETFs: BLOK, FDIG, and IBLC.

| The Fund | BLOK | FDIG | IBLC | |

| Management Fee | 0.51% | 0.75% | 0.30% | 0.39% |

| 2022 Performance | (85.60) | (62.36) | N/A | N/A |

| 2023 Performance | 285.0% | 99.53% | 166.0% | 201.57 |

| 2024 Year to Date | 1.85% | 16.01 | (3.93) | (4.37) |

Asset Under Management ($ millions) | 103 | 963.2 | 94.5 | 21 |

Top 10 Holdings % | 65.21% | 41.56% | 68.98% | 73.68% |

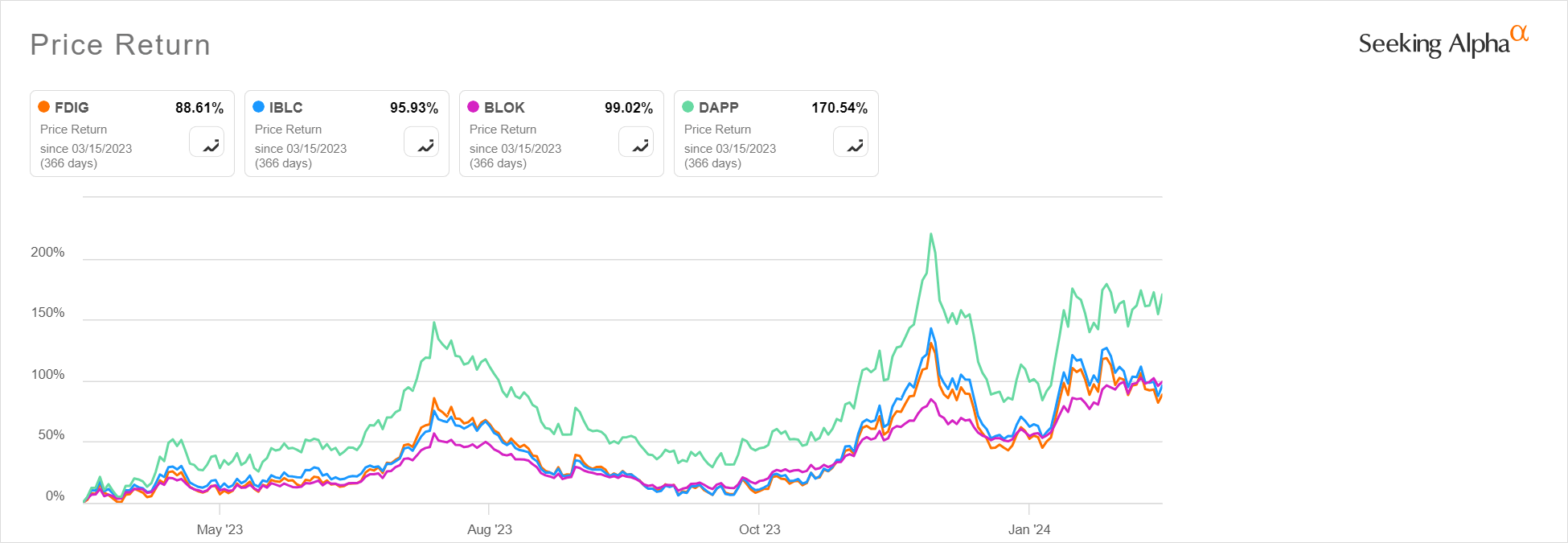

For the one-year period ended March 15, 2024, the Fund has outperformed its competitors.

March 15, 2023 to March 15, 2024

Seeking Alpha

Overall, with respect to performance, the Fund is extremely volatile, but so is the performance of its competitors, with actively managed and more diversified BLOK providing less downside risk.

For the reasons described below, however, I am not confident in the Fund's long-term performance going forward. Moreover, I believe an actively managed ETF such as BLOK can do better in the space over the long term given the immaturity of the Blockchain industry.

As of March 14, 2024, the Fund's portfolio included 22 holdings. Certain of the Fund's material holdings are as follows, including all holdings with more than a 5% weighting, as well as a couple of other holdings I find notable:

MicroStrategy Inc. (MSTR) 18.56%

Coinbase Global (COIN) 10.59%

Block, Inc. (SQ) 7.29%

CleanSpark (CLSK) 7.18%

Marathon Digital Holdings (MARA) 5.81%

Galaxy Digital Holding (GLXY:CA) 5.28%

Bitfarms (BITF) 4.47%

Canaan (CAN) 2.79%

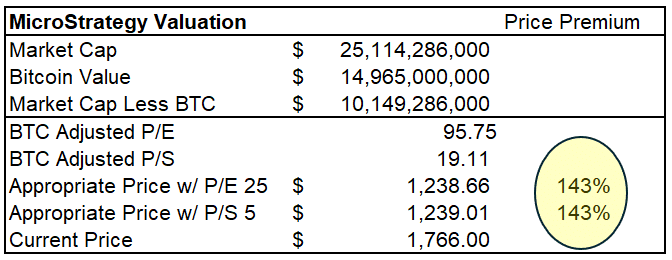

First, MicroStrategy, run by Bitcoin legend Michael Saylor, is effectively a closed-end fund trading a large premium to its underlying assets. The table below, provided by Michael Lebowitz and Lance Roberts (writing for RIA Advice):

RIA Advice

While I would argue that a slight premium might be merited given MicroStrategy's ability to engage in certain financial engineering transactions to accumulate more Bitcoin, a 43% premium is not warranted. Even though MicroStrategy in 2020-21 was my best trade of all time (a 10x), it is very overvalued and, as a consequence, I think an investor would be better off investing in one of the Bitcoin ETFs.

Second, speaking of overvalued, Coinbase, the second largest holding of the Fund, is extremely overvalued per data from Morningstar:

Price/Book 9.35

Price/Cash Flow 66.67

Price/Sales 19.84

Price/Earnings 655.20

Notably, the current price-to-sale ratio of the S&P 500 is 2.79, and the record high for the S&P 500 is 3.14.

Coinbase's price-to-sale ratio is now near 20. After the internet bubble burst in 2000, the CEO of Sun Microsystems, Scott McNeely, famously had the following to say about the lunacy of his company having a price to sale ratio of 10 prior to the internet bubble bursting:

At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don't need any transparency. You don't need any footnotes. What were you thinking?"

Seeking Alpha provides Coinbase an "F" valuation grade, confirming the overvaluation.

In summary, the top two holdings of the Fund's portfolio, which make up nearly 30% of the portfolio, are severely overvalued. For this reason alone, I think investors should be cautious about the Fund. Unfortunately, because it is an index ETF, the Fund is unable to take profits on those overvalued securities. In fact, if the price of those companies rises, the Fund will have to buy more. Hence, a reason I favor active management for blockchain investments.

In addition, my research on the bitcoin miners, of which the Fund has several holdings, is also showing me that, as a whole, these companies are not progressing toward profitably fast enough. They also skyrocketed in 2023 and are due for a material pullback. I wrote about these issues recently with respect to Bitfarms, a Bitcoin miner making up nearly 4.5% of the portfolio.

Finally, the Fund's nearly 3% holding in Canaan, Inc. is unwise in my view. I wrote about this company in March 2021, giving it a sell rating at that time. Since that time, Canaan's stock has been down more than 90% and it really has not recovered. Canaan lost over $400 million in 2023. It is a terrible business, but again, because the Fund is passively managed, it simply has to buy this holding because it is in the Index. While that type of investing might make sense in a mature industry, I reiterate that I do not think passive investing is the way to go for an immature industry like Blockchain.

The Prospectus for the Fund outlines the key risks of holding shares in the Fund. The biggest risk I see, however, is that many of the Fund's holdings (as discussed above) are overvalued and/or unprofitable. Moreover, the Fund is very concentrated, thus increasing the risks associated with its over-valued holdings. Another key risk is government interference in the industry. It does not go unnoticed that the 2023 IRS 1040 Tax Form includes a Digital Assets query right up front at the top of the application. No one wants to be audited, but it seems abundantly clear that the federal government is putting in place the infrastructure to target crypto investors for audits. Investors should not underestimate the fact that many politicians detest crypto, seeing it as a destabilizing force. Anti-crypto policies and practices, including Bitcoin mining taxes, could adversely affect the companies held by the Fund.

For the reasons outlined above, the Fund is a HOLD (at best). Do your own due diligence.