A close-up view of water flowing from the tap into a glass.

by sonmez

A close-up view of water flowing from the tap into a glass. by sonmez

As a dividend growth investor, I am drawn to regulated water utilities for their consistency. For more on what I mean, readers can check out my article on American Water Works (AWK) from January.

The crux is that water is critical to the modern economy and standard of living. This is what makes it so indispensable. Coupled with boundless water infrastructure modernization opportunities in the next 20 years (~$750 billion) per the Environmental Protection Agency, this is why I like water utilities.

That's why, over the years, I have covered the likes of AWK, American States Water (AWR), California Water Service (NYSE:CWT), Essential Utilities (WTRG), and York Water (YORW).

Now, that's not to say that there aren't risks with regulated water utilities. California Water Service's ongoing General Rate Case or GRC with the California Public Utilities Commission or CPUC is the latest reminder. Originally, the 2021 GRC was going to be completed on Dec. 31, 2022, with rates effective the next day. After many months of litigation, the CPUC-assigned Administrative Law Judges or ALJs issued a Proposed Decision that was close to CWT's requested revenue requirement. Unfortunately, the assigned CPUC Commissioner issued an Alternate Proposed Decision more aligned with the consumer advocacy arm of the CPUC, Public Advocates (info sourced from CWT's Q4 2023 Earnings Press Release).

This regulatory delay is why shares of CWT dipped 7% since I began coverage in November, as the S&P 500 (SP500) surged 16% higher. In that time, CWT also shared its financial results for the fourth quarter that ended Dec. 31, 2023. I will examine those results, discuss the 2021 GRC, and highlight the valuation to explain why I am keeping my buy rating for now.

Dividend Kings Zen Research Terminal

CWT's 2.5% dividend yield scores a D- in Seeking Alpha's Quant System for dividend yield. This is because it is meaningfully below the 4.1% median for the utility sector. But what CWT lacks in starting yield, it makes up for with growth and consistency. The company just hiked its annualized dividend per share by 7.7% to $1.12 (or $0.28 quarterly), which will be its 57th consecutive year of dividend growth. That earns it an A+ for dividend consistency from Seeking Alpha's Quant System.

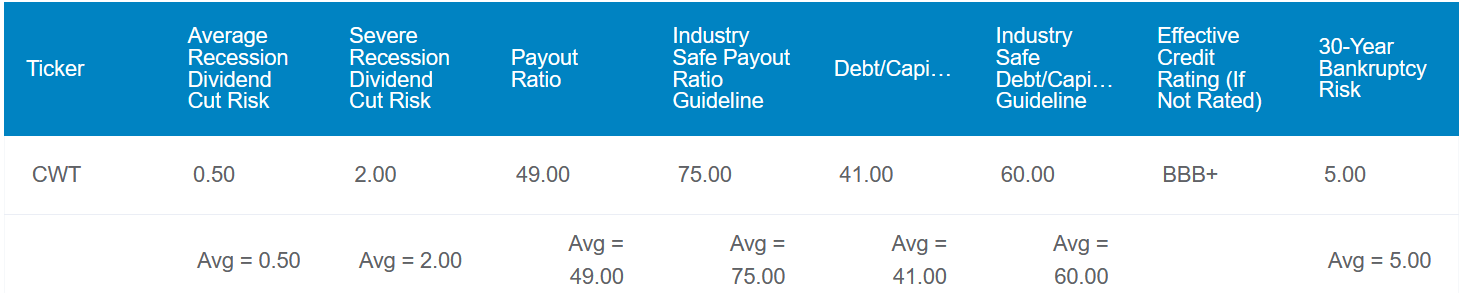

Not to mention that I believe CWT can keep delivering solid dividend growth in the years to come. That's because the company's 49% EPS payout ratio is significantly less than the 75% EPS payout ratio that rating agencies project is safe for the water utility industry. This is better than the 55% from when I last covered CWT.

The company's debt-to-capital ratio has also improved from 44% to 41% since I last highlighted it. That's leaps and bounds below the 60% debt-to-capital ratio that rating agencies like to see from water utilities. This suggests that CWT's balance sheet is quite healthy. That is why Dividend Kings thinks the company's effective credit rating is BBB+, which suggests a 5% probability of bankruptcy in the next 30 years.

Considering these factors, Dividend Kings estimates that the risk of a dividend cut in the next average recession is 0.5%. If the next recession was severe, that risk would increase to 2%. For what it's worth, these are the lowest possible risks in the Zen Research Terminal.

Dividend Kings Zen Research Terminal

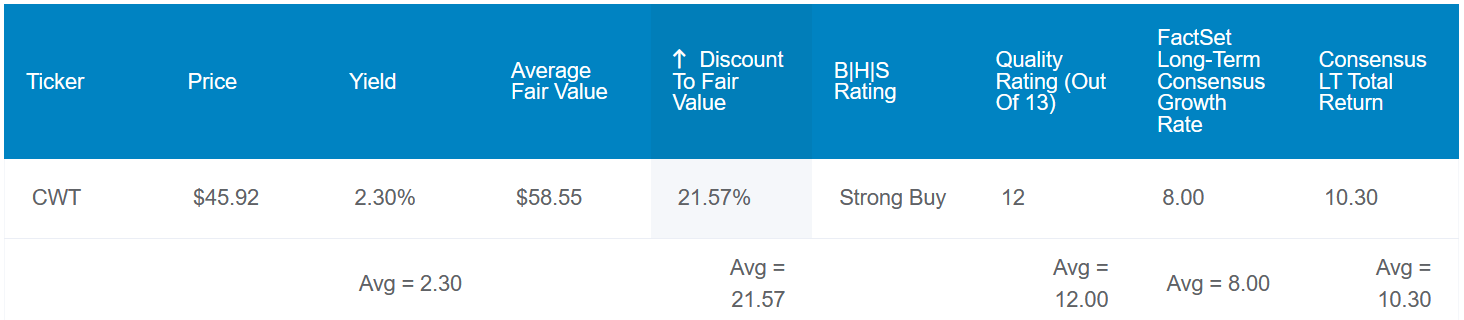

The recent pullback in CWT's valuation has arguably increased its appeal. The five-year average dividend yield of 1.6% suggests the fair value for the stock is $63 a share per the Dividend Kings Automated Investment Decision Score Tool feature. Blending that with a 13-year average dividend yield of 1.9% and a fair value of $54 a share, CWT is still quite undervalued. Finally, based on the historical P/E ratio of 26.4 and the 2024 EPS analyst consensus, shares are worth nearly $60 each.

Averaging out these fair values, CWT's shares could be fairly valued at almost $59 apiece. Relative to the $46 share price (as of March 1, 2024), the stock could be priced at a 22% discount to fair value.

If CWT can meet the growth consensus and revert to its mean valuation, these are the total returns that may be in store in the coming 10 years:

CWT Q4 2023 Investor Presentation

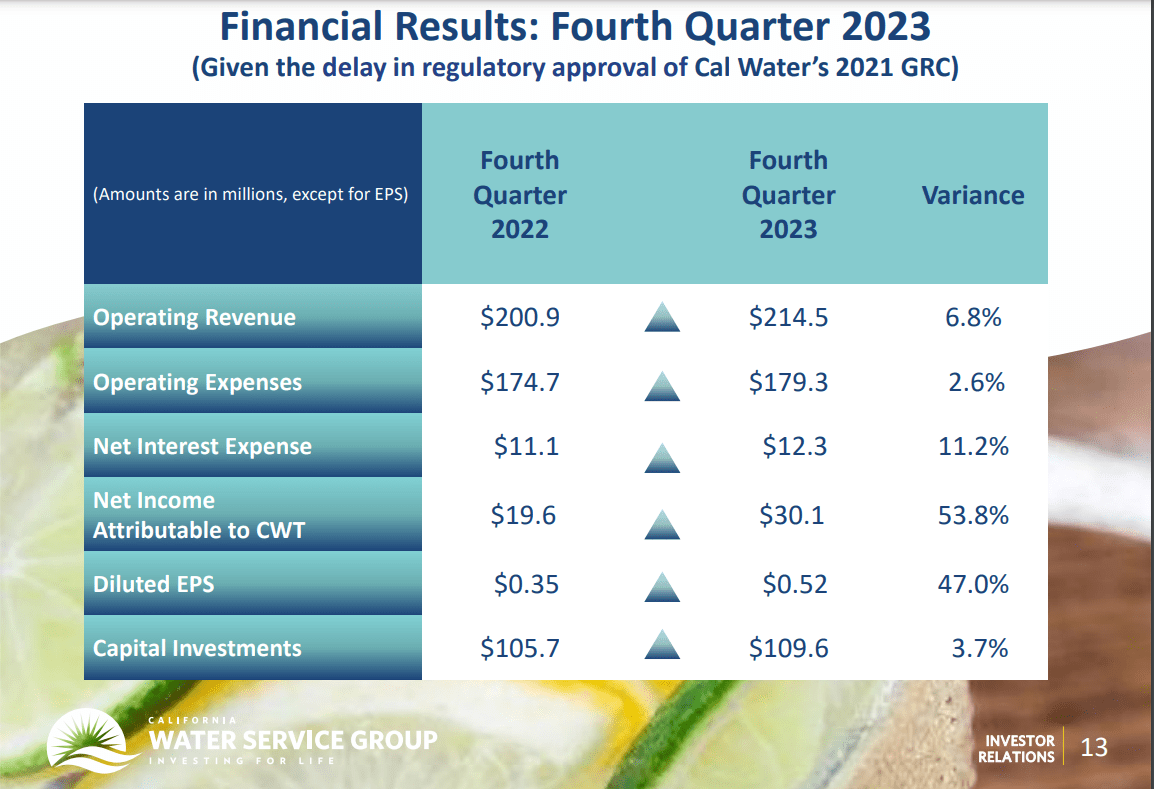

Without the proper context that I alluded to a bit in the opening, CWT's fourth-quarter results would appear to indicate that something is fundamentally wrong with the company. The water utility's operating revenue grew by 6.8% year-over-year to $214.5 million during the quarter, but this missed the analyst consensus by $59.1 million per Seeking Alpha.

This topline growth was the result of a few elements. First off, rate increases contributed to $13.8 million in operating revenue growth. Next, a decrease in deferred revenue of $12.3 million was another operating revenue growth driver. Third, an increase in customer water usage helped lead operating revenue higher by $3.3 million. A $2.1 million boost in accrued unbilled revenue was the final tailwind.

These tailwinds were partially countered by an $18.1 million decrease in Water Revenue Adjustment Mechanisms or WRAM and Modified Cost Balancing Account or MCBA revenue. That was because of the delay in CPUC's approval of the 2021 GRC, which is why these mechanisms ended after 2022.

The expectation from analysts was that these mechanisms would be put back into place by the time Q4 results were shared. Since that didn't happen, CWT couldn't include these mechanisms in its Q4 results (or 2023, for that matter). That is why the operating revenue miss was so wide.

CWT's diluted EPS surged 48.6% higher over the year-ago period to $0.52 in the fourth quarter. That was $1.01 short of the analyst consensus according to Seeking Alpha, which was again due to the delayed GRC approval.

In 2023, diluted EPS came in at $0.91 (pending the resolution of the 2021 GRC). That was down 48.6% from $1.77 in 2022. But when considering the $1.10 per share headwind throughout the year of the decrease in WRAM and MCBA revenue and the $0.29 per-share income tax benefit, diluted EPS was relatively steady.

CWT Q4 2023 Investor Presentation

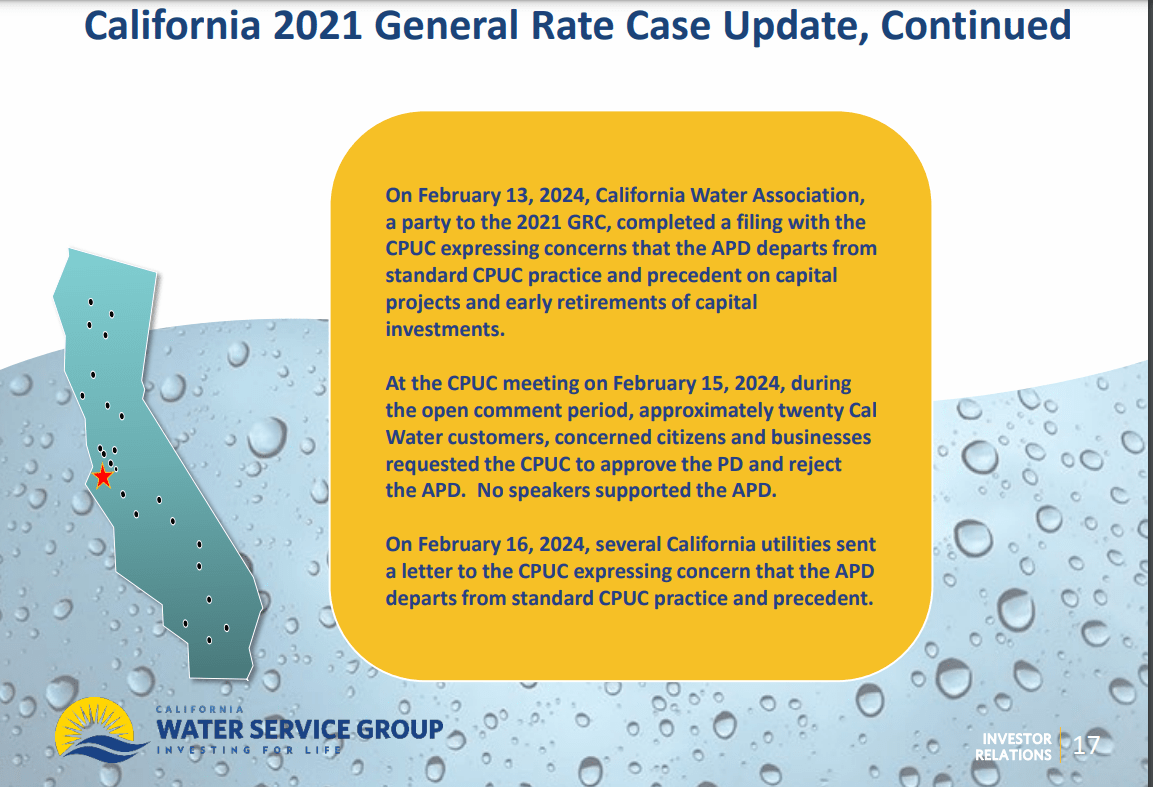

It isn't completely clear how the 2021 GRC will turn out. But both analysts and myself agree, there are reasons to err on the side of optimism.

CWT wasn't alone in its concerns about the precedent the APD would set for water utilities in California. On Feb. 13, the California Water Association finished a filing that expressed concerns the APD would be harmful to the overall industry.

Two days later, at the CPUC meeting, around 20 of CWT's water customers, concerned citizens, and businesses spoke supporting the PD that was more aligned with CWT. Yet, there wasn't a single speaker in favor of the APD present at the CPUC meeting.

A day later, several other California water utilities sent a letter to CPUC voicing their concerns toward the APD.

All of this opposition to APD may fall on deaf ears. However, this would make zero sense because everybody would end up a loser from such a decision. Water utilities would be less incentivized to make necessary upgrades to water infrastructure. Consumers and businesses would suffer as a result.

Politics aside, I believe the most likely outcome is that there will be a second or third APD. These may not be quite as favorable as CWT was initially hoping, but they also won't be most of what Public Advocates wanted, either (unless otherwise noted or hyperlinked, all details were sourced from CWT's Q4 2023 Investor Presentation and CWT's Q4 2023 Earnings Press Release).

As strange as it may sound with a company boasting 50+ years of dividend growth, I think CWT has plenty of years of dividend growth left in the tank.

The FAST Graphs analyst consensus is $2.26 in diluted EPS for 2024, $2.40 for 2025, and $2.61 for 2026. Even adjusting for a 10% margin of error (i.e., a slightly unfavorable regulatory outcome), CWT could post $2.03 in diluted EPS in 2024.

Against $1.12 in dividends per share that are slated to be paid during the year, that's a 55.2% payout ratio. This would remain a sustainable payout ratio for a water utility.

All things considered, CWT's business is doing fine. However, there are risks involved with an investment.

According to page 7 of 140 of the most recent 10-K filing, CWT's California operations made up 90.6% of total consolidated operating revenue in 2023. If the 2021 GRC is resolved closer to the way that Public Advocates would like, that could be moderately negative to CWT's growth prospects.

As I also discussed in my previous article, this geographic concentration exposes the company to natural disasters. Such events could disrupt the company's operating results.

Another risk to the company is the possibility of stricter water quality regulations. That could cause operating costs to rise, which may not be approved by regulators to be recovered from customers.

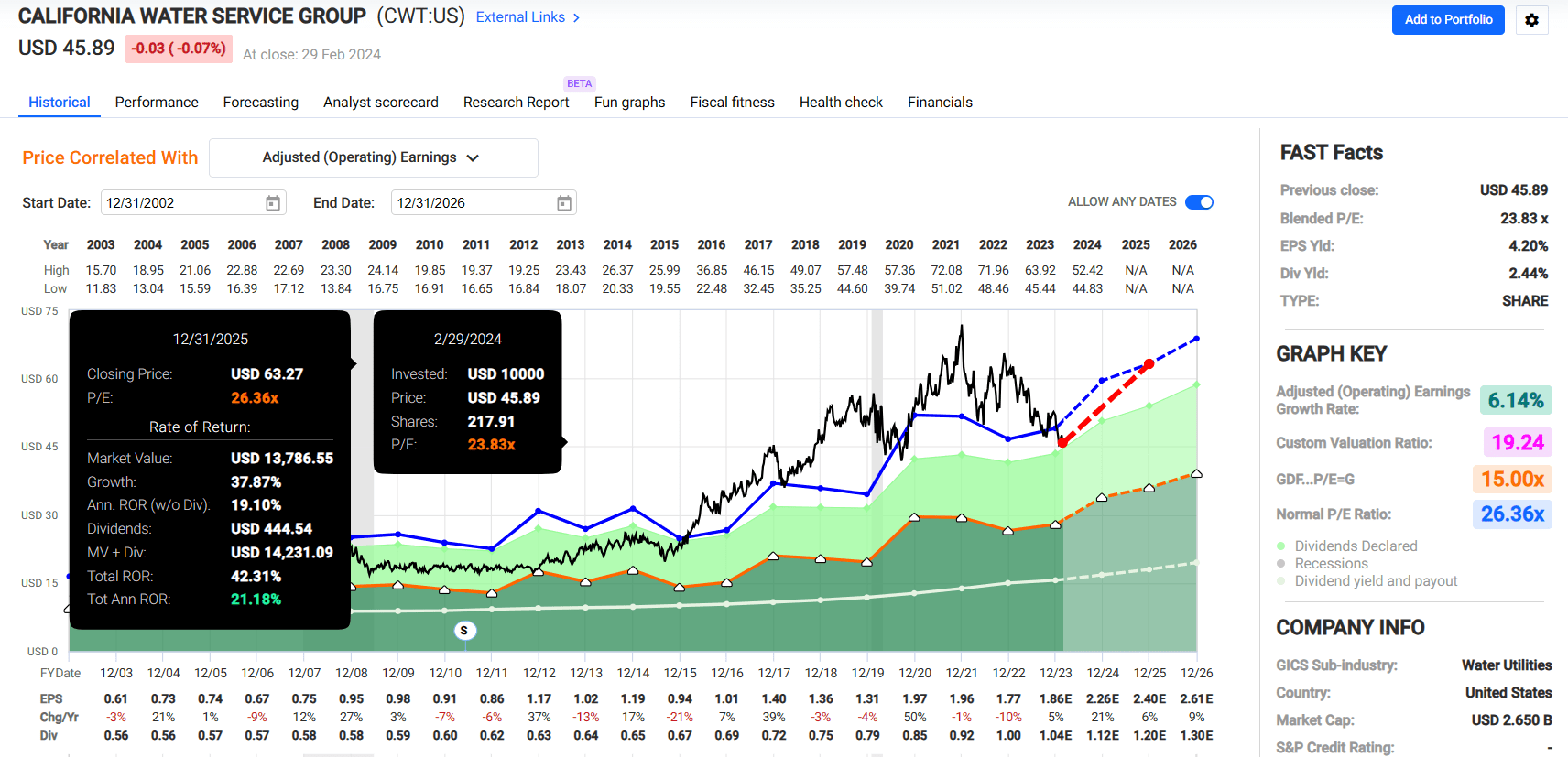

FAST Graphs, FactSet

CWT is a great business that is facing regulatory uncertainty right now. If the 2021 GRC is resolved as I anticipate, I believe a reversion from a 23.8 P/E ratio to 26.4 could be in order. That could produce 42% cumulative total returns through 2025. Even if the decision ends up being a bit less favorable to CWT, the margin of safety appears to be still there for double-digit annual total returns through 2025. That's why I am standing by my buy rating.