Yevhen Smyk/iStock via Getty Images

Yevhen Smyk/iStock via Getty Images

In my previous coverage of Casella Waste Systems (NASDAQ:CWST), I recommended a buy rating as I believed the volume decline was not an issue to be worried about given that the pricing growth remained very healthy. Turns out, the reiteration of a buy rating was right as the stock rallied from ~$80 to ~$91 today, inching closer to my target share price. This post is to provide an update on my thoughts on the business and stock. I am staying with a buy rating for CWST as I see a visible catalyst that could result in CWST beating consensus FY25 estimates.

CWST reported strong 4Q23 revenue growth of 32% to $359.6 million. Revenue was driven by newly closed and roll-over impacts from acquisitions, offset by weak volume. Collection revenue was robust in the quarter, growing 55% to $214.7 million, and disposal revenue grew 8% to $63 million. In terms of volume and pricing dynamics, volume continued to stay soft, down 1.4%, while pricing remained solid, growing 6.7%. As a result, the 4Q23 EBITDA margin expanded 210bps to 22.6%, and EBITDA came in at $81.5 million.

The CWST 4Q23 headline results were solid, in my opinion. While the volume continued to be soft, I believe it is a result of the CWST decision to continue shedding low margin accounts. More importantly, I thought it was encouraging to see solid waste volumes improve sequentially from -3.3% in 3Q23 to 4Q23 -1.4% yoy, which was primarily driven by a recovery in special waste volumes. A similar recovery trend could be seen in landfill tons, which were down 3.7%, a major step up from the -10.1% seen last year as special waste and MSW volumes were flat. At this rate of recovery, my expectation is that volume will turn positive either in FY24 or FY25.

A major catalyst ahead is the McKean rail infrastructure, which is expected to be online in mid-to-late 2024, which I think will help CWST beat its own guidance. For background information, the rail at McKean enables CWST to bring its services closer to the major population centers in the northeast of the country. The expansion in capacity would be massive, as it allows 1.6 million tons of annual in-take compared to just 100,000 tons per year that the site takes in today. This massive expansion in capacity has a huge positive financial impact, as the additional capacity will carry a high incremental margin since it is on the same rail. That said, my guess is that it might take some time before CWST can fully ramp up utilization, as it takes time to shift demand to this rail as it comes online. Importantly, the rail infrastructure will provide CWST visibility on placing acquired customer volumes, creating an opportunity to take on incremental volumes that would otherwise have to be moved outside the Northeast. Assuming CWST can achieve 80% utilization on the incremental capacity, which is around 1.2 million tons, at $35.7 revenue/ton (FY23 level), this translates to an incremental revenue of $42 million in revenue (40% of FY23 landfill revenue). If I simply attach the consolidated margin (23.3% EBITDA margin) to this $42 million, it translates to ~$10 million of incremental EBITDA, which already implies a 4% growth in FY23 EBITDA. However, note that these are incremental capacities, so the incremental margin should be way higher than the consolidated figure. CWST is also working on increasing permitting at its Hyland landfill in Western, New York, to bring annual volumes from 460,000 tons a year to around 1 million tons per year at this landfill. Doing the same math here (80% incremental utilization at $35.7 revenue/ton and 23.3% EBITDA margin), I got an incremental EBITDA of $4.2 million. Collectively, these will drive EBITDA growth of at least 5% on top of the organic EBITDA growth that CWST is experiencing.

Another EBITDA upside catalyst is the CWST’s Juniper Ridge facility (which has a capacity of 700,000 MMBtu/year) and North Country landfill gas facility (which has an approximate . capacity of 600,000 MMBtu/year), which are on track to come online in 2024. Juniper is expected to go online first by 1H24, and North Country is expected to be up by 4Q24. The impacts from these projects are likely to be minimal in FY24. However, as we approach FY25, the EBITDA contribution will be in larger magnitude on a percentage basis relative to FY24, given the easy base. Notably, these revenues come at high incremental margins given that CWST generates a royalty stream from the sale of gas and RINs with no capital requirements.

Finally, we expect our first RNG project at our Juniper Ridge Landfill to be online in the first half of 2024. RKF or BP will own and operate the facility, while Casella generates a royalty stream from the sale of gas and RINs with zero capital investment.

Our one facility associated with our North Country landfill in New Hampshire is close to commercial operations. It's still -- they're working on a couple of details to get online, and we hope that will be online in either the fourth quarter or first quarter. 4Q23 earnings results call

One final point to bring up is that the CWST balance sheet remains healthy with a leverage ratio of 2.8x EBITDA, below the previous levels of >3x. As such, I don’t see any imminent liquidity risk. CWST should be able to continue executing its M&A strategy (they acquired seven targets in FY23) to expand their geographical footprint.

Own calculation

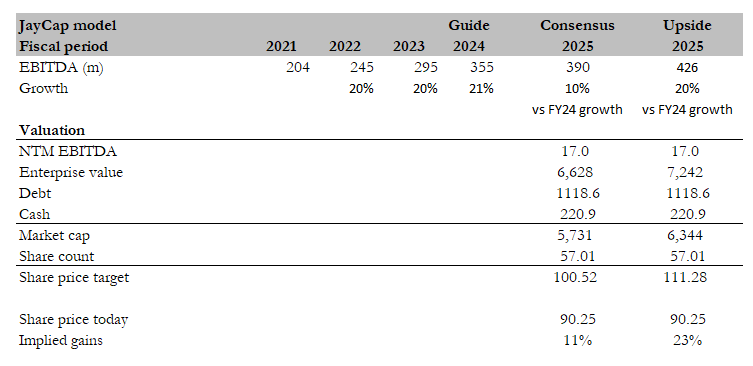

I have changed the way I value CWST from a long-term DCF to a relative EBITDA multiple model as I think there is potential for near-term upside. Using management guidance for FY24 ($355 million) as a baseline for my FY25 estimates, I believe the stock provides a minimum upside of 11% using the consensus estimate of $390 EBITDA in FY25 and the CWST current forward EBITDA valuation of 17x. However, as I mentioned above, there are two key catalysts that could drive higher upside. Suppose the utilization rate of the new landfill capacity and revenue per ton go up higher than expected, EBITDA growth could continue at the current pace of ~20%. If so, EBITDA could reach $426 million in FY25, and at the same multiple of 17x, the stock is worth 23% more. The reason for using 17x in both scenarios is because it is the historical average (5-year) that CWST has traded at.

CWST has enjoyed positive pricing growth so far; however, there is a limit to how much prices can continue to grow. Suppose pricing starts to fall and volume does not recover. This could result in very bad near-term performance as these volumes have high decremental margins. Aside from this, if disposal cost inflation accelerates faster than CWST pricing growth, it could also impact margins.

CWST continues to exhibit strong performance, with robust 4Q23 results and a positive outlook. While volumes remain soft, the trend suggests that it could reach positive growth in FY24/FY25. The upcoming McKean rail infrastructure is a significant catalyst for growth, potentially driving incremental revenue and EBITDA. CWST also ended the year with a healthy balance sheet, which should enable it to continue fund its M&A strategy. I maintain a buy rating, anticipating a minimum 11% upside based on consensus estimates for FY25 EBITDA. However, the potential for higher upside exists if new landfill utilization and revenue per ton surpass expectations, potentially yielding a 23% upside.