michaelbwatkins

michaelbwatkins

As a retired Navy veteran and someone who spent a great deal of their career onboard Naval ships, I thought it was only right to cover shipbuilder Huntington Ingalls (NYSE:HII), a company I became very familiar with throughout my 21-year career. In this article, I discuss the company's financials, projected growth outlook, and why they may be one for investors looking for strong fundamentals and long-term dividend growth.

For those unfamiliar with Huntington Ingalls, the company has been around since the late 1800s and is headquartered in Newport News, Virginia. This is also home to the largest Naval Base in Norfolk.

In short, the company builds the majority of ships for the U.S. Navy. And also build ships for the United States Coast Guard. They operate in three divisions: Ingalls Shipbuilding, Newport News Shipbuilding, and the newer division Mission Technologies, implemented in 2016.

Furthermore, the company builds and provides C5ISR systems and operations; application of AI and machine learning to battlefield decisions. These include unmanned vehicles, defensive and offensive cyberspace strategies, fleet modernization, and critical nuclear operations.

They are also the sole builder of our largest warships the U.S. Aircraft carriers. I've never had the luxury of being stationed on one of these as I spent most of my career on smaller ships such as frigates and destroyers. As an 18-year-old kid joining the Navy straight out of high school, I've had my fair share of traveling the world on many deployments, mostly in Asia and the Middle East.

I've also sailed many seas and oceans as I spent over half of my career on 7 different ships. I enjoyed my time in the Navy, especially on deployments. Some were boring as we conducted operations day in and day out for what seemed like an eternity. Others were more fun as we got to work with other countries' militaries, providing training while also projecting our sea power. But, enough about my military history, let's get into the meat and potatoes of what makes HII a dividend stock you should consider owning.

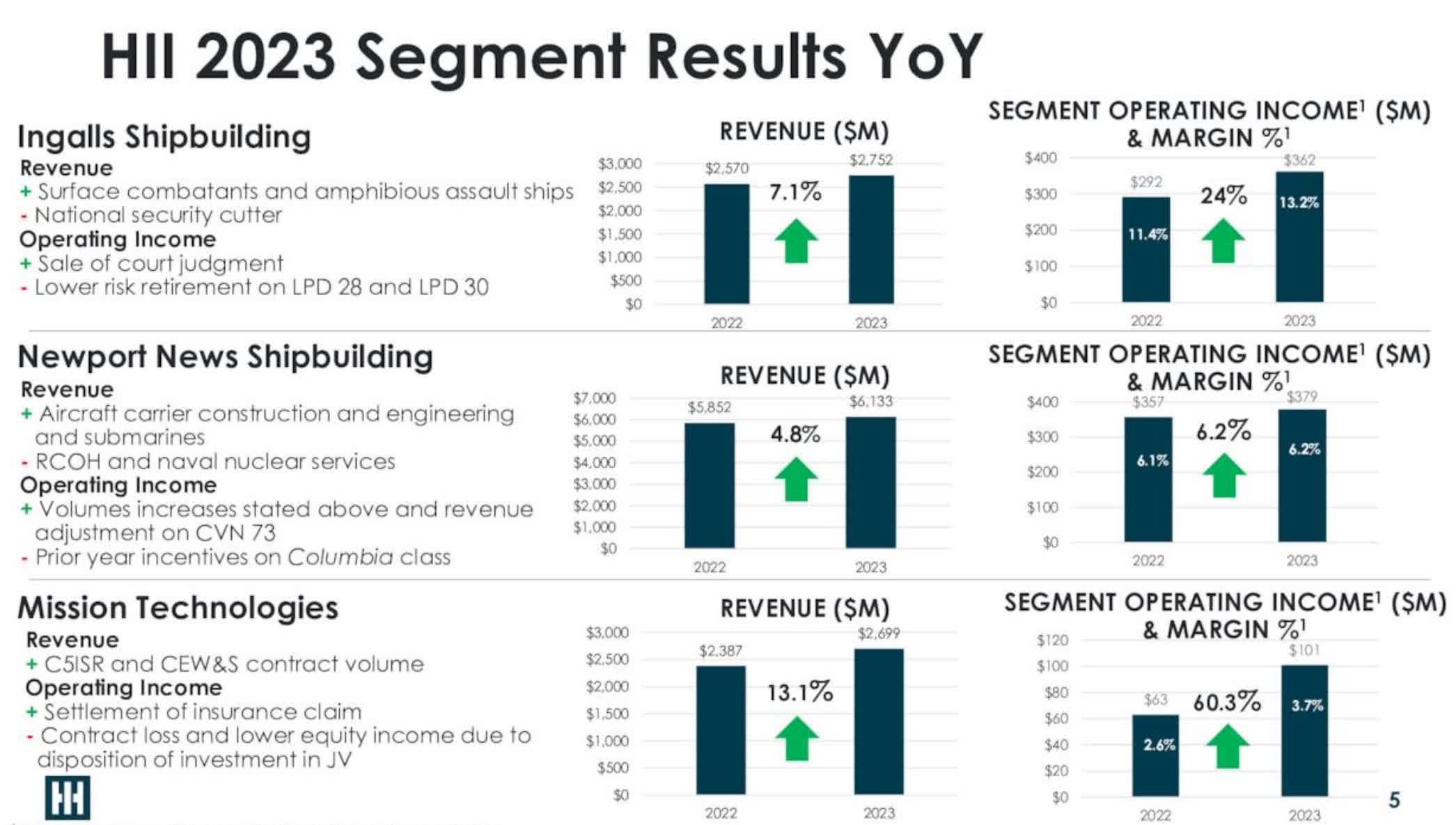

Aside from 2020, 2023 was a strong year for the shipbuilder as they brought in record revenue. Furthermore, they managed to grow their earnings year-over-year by double-digits. All three segments performed well during the year with mission technologies up double-digits at 13.1%. With the recent artificial intelligence boom, it is no surprise the division outperformed.

The other two also performed well, up 7.1% and 4.8% respectively. Operating margins were also up for the year at nearly 7%. So, all in all the company performed exceptionally. While the macro environment has plagued several high-quality businesses because of higher interest rates, HII seems to have been the exception.

HII investor presentation

To be fair, however, the shipbuilder has been kept busy by the government with new ships rolling out lately. The company launched and delivered four ships during the year while being awarded contracts to build 8 additional ones.

And they are expected to deliver several more in 2024 and 2025. They were recently awarded a $1.17 billion contract with the U.S. Navy last month as well. So, for the next few years, the company will seemingly be busy. Additionally, with the president seeking billions more for defense amid global conflicts, I think it's safe to say HII will be needed for the foreseeable future.

To close out the year revenues totaled $11.5 billion, a record for the company. This grew more than 7% from $10.7 billion in 2022. Earnings also grew impressively by double-digits to $17.07 from $14.44 from the year prior. Again, this was driven by strong growth in all three segments.

The best-performing segment, Mission Technologies, growth was driven by a $49.5 million settlement of representations and warranties insurance claim in relation to the acquisition of Hydroid. In my opinion, this was a strong year for the company, and a testament to their management and fundamentals to perform well in tough economic times.

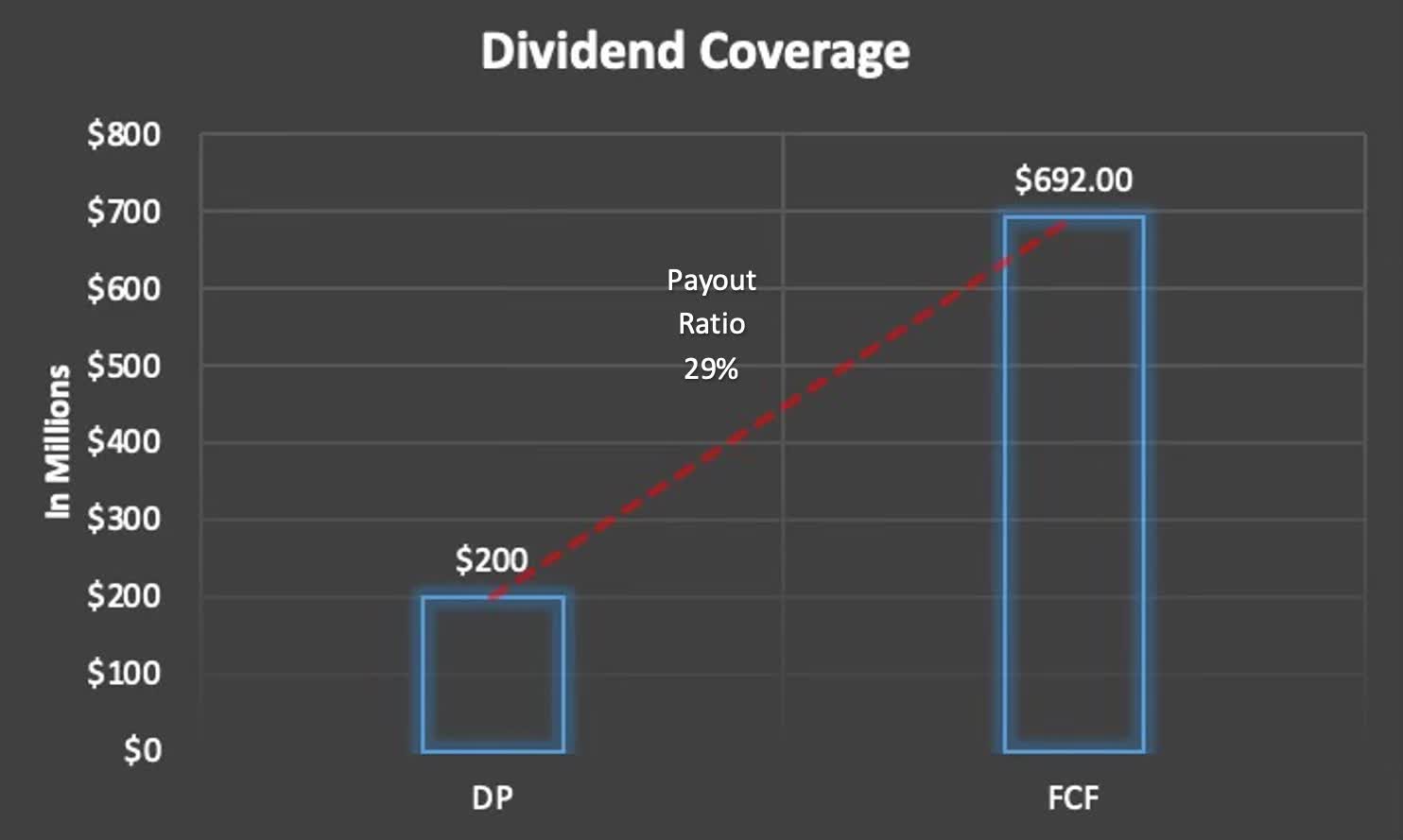

For the year, HII brought in $692 million in free cash flow, representing a growth rate of nearly 41% from 2022. Furthermore, I expect the company to continue growing the dividend at a respectable rate. Since paying a dividend in 2012, they've managed to grow this from $0.10 to the current $1.30. That's a growth rate of nearly 1200%!

This is in comparison to peer, Curtiss-Wright's (CW) growth rate of 150% over the same period. And their strong growth in cash flows was due to the growth in cash from operations which grew nearly 27% year-over-year. Furthermore, the company has been returning ample cash to its shareholders not only in the form of dividend growth but buybacks as well.

In 2023, HII bought back 377,000 worth of shares and has been steadily decreasing their share count over the years. And with the recent announcement and increase to $3.6 billion for their buyback program, I expect this will continue, driving earnings and cash flow growth for the foreseeable future.

With an annualized dividend of $5.02 and roughly 40 million shares outstanding, the company only needs $200 million in free cash flow to cover its dividend. Using their cash flow of $692 million, this gives HII a very low payout ratio of 29%!

This gives the company financial flexibility to reinvest back into the business to grow organically, or reward its shareholders with further dividend increases and buybacks. It also gives them ample cash if business is slow or the economy experiences a sudden downturn or they face financial hardship.

Author creation

Looking forward HII is projecting its cash flow to be $3.6 billion in the next 5 years. For 2024, free cash flow to be in the range of $600 million to $700 million. CAPEX is expected to be 1.5% of revenues and expected to increase because of shipbuilding capacity.

Using data from Seeking Alpha, earnings are expected to grow double-digits from 2025 forward while revenue is expected to grow low-single digits over the same period. Cash from operations is expected to grow at a healthy rate to $1.36 billion from $970 million over a 3-year period while free cash flow is expected to grow from $692 million to $759 million at the end of 2026.

Given the stock's outperformance in 2023 and 2024, you can see why the share price has climbed over the past year and now trades closer to its 52-week high. HII is up roughly 37% and has a current P/E of nearly 17x. And although this is still below the sector median's 19.6x, HII trades above its 5-year average P/E of roughly 14x.

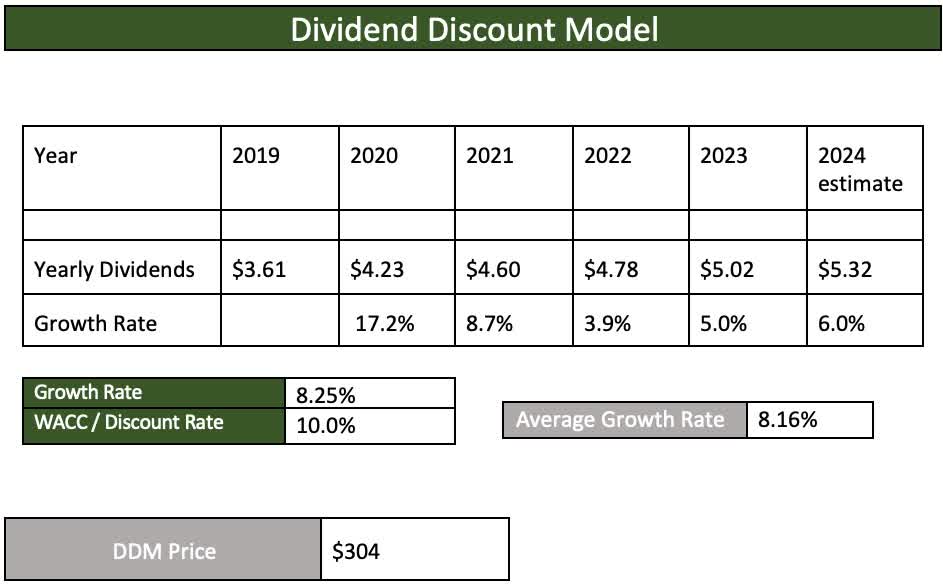

However, using the dividend discount model, the stock still offers investors some upside to my price target of $304 a share. Seeing as HII is a high growth stock and earnings are expected to grow at 10.5% for the next 5 years, I decided to use a ROR of 10%, slightly higher than the 7% - 10% average for the S&P.

Author creation DDM

Furthermore, the stock outperformed the S&P in both price and total returns over the past 3 years so a 15% is not so far-fetched. Although past performance doesn't predict future performance, and the stock may underperform going forward.

This is higher than Wall Street's $277, and more than 4% downside from the current price of roughly $290 where it currently trades at the time of writing. For those wanting a margin of safety, I agree with Wall Street's hold rating, but seeing the company's outperformance, I can see the stock moving higher from here.

HII has been firing on all cylinders during the current macro environment and building ships for the U.S. government seems all but secure. But nevertheless, the company still faces risks. In my opinion, the big risk here is them executing on their contracts. If the company falls behind because of higher costs of goods due to higher interest rates, or any reason for that matter, they may lose out on future contracts. And this will likely impact their financials going forward, which in turn could affect the dividend.

I can tell you from experience the military is big on timely execution and has no problem awarding competitors with contracts to stay on schedule. HII lost the frigate contract to peer Fincantieri Marinette Marine to produce the newer class Frigate for the U.S. Navy. And any shortfalls or delays in production can affect the company going forward. Additionally, working with the U.S. government, they are also susceptible to many types of geopolitical issues that can have a negative impact going forward.

Huntington Ingalls performed exceptionally well during tough economic times, which is a testament to the company's management team and quality business. Additionally, their fundamentals and outlook are strong with a strong line of future products in development. This will likely impact their financials positively and management expects free cash flow to be $3.6 billion in the next 5 years, strong growth from current numbers.

Furthermore, the company's dividend growth remains well-covered with a safe payout ratio of only 29%, further signaling healthy dividend growth and buybacks going forward. Although the share price is up 37% in the past year, I still think the stock offers investors some upside from here, therefore warranting a buy rating.