Matthias Hangst

Matthias Hangst

CureVac (NASDAQ:CVAC) had a rough end to 2023 after a German court invalidated one of their key mRNA technology patents, when they were quite optimistic on the earnings call prior to the decision that their patents would be upheld. Looking back, it’s the most recent in a string of less-than-encouraging developments for the company at a time when a pioneer in the mRNA therapeutic space should be flying high. It’s really looking like a case where the people behind the company are brilliant scientists but poor businesspeople, the unfortunate reality for a lot of biotech startups. As it stands, CureVac is stuck in neutral, and it doesn’t seem like they have anything extraordinary cooking in order to jump start their portfolio over the other big names in the mRNA space.

The patent that was invalidated in December is related to an invention CureVac claimed in 2002 pertaining to “G/C enrichment” of mRNA to increase its stability specifically when the sequence encodes some viral protein. The result of this invention is that the resulting mRNA polymer is “more stable” while still encoding the same protein sequence, which makes it more useful in a clinical application as something like an antigen-encoding vaccine. To a domain expert like Derek, it’s tough to look back and think this constitutes a genuine “invention” when:

The redundant nature of the genetic code, needed to engineer sequences of nucleic acids without altering protein sequence, is a fundamental biology concept and has been since the 70s

Codon bias, the tendency of organisms to favor particular triplets within redundant sets of “synonymous” codons for the same amino acid and its effect on protein translation, has been known since the 90s

Things like G/C content difference between genomes and its effect on nucleic acid and genetic stability have been heavily researched from the 70s through the 90s

RNA’s ability to fold into complex structural motifs, the role of RNA secondary structure in its biological function, and the role of intra-polymeric base pairing in nucleic acid folding, has been studied and modeled since at least the 90s (see this book chapter co-authored by one of the domain experts of nucleic acid structure prediction, published in 1999)

Technologies like polymerase chain reaction (PCR), a Nobel-prize-winning, field-transforming invention from the 80s, depend heavily on engineered sequences of nucleic acids, with G/C content as a key consideration.

Granted, the technology allowing for engineering and synthesis of sequences of nucleic acids took great strides throughout the 90s and early 00s, and engineering of mRNA molecules (versus DNA, as primers for performing PCR or other forms of genetic engineering) was probably not on anyone’s radar in 2002, but from an academic perspective, it really feels like all the pieces were already there and the patent invalidation seems justified.

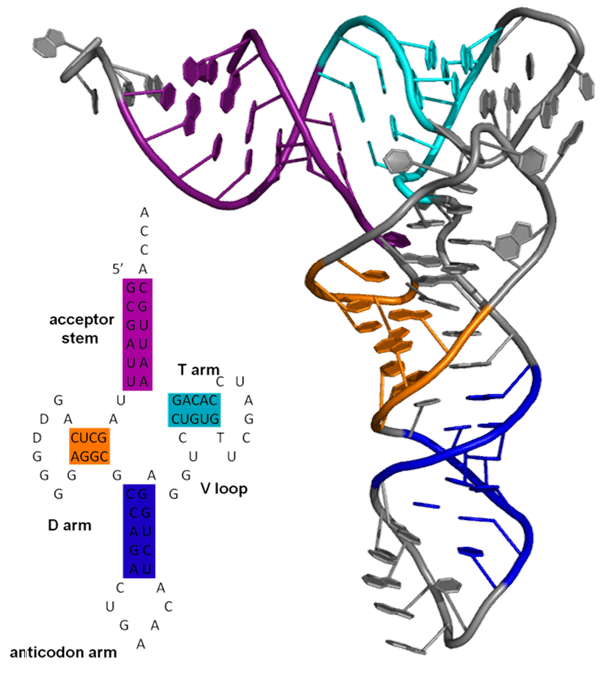

Transfer RNA (tRNA), a class of natural RNA molecules with complex three-dimensional structure, mediated by intra-molecular base pairs dictated by sequence, that is crucial to their function. (Wikipedia)

The other key technology patent CureVac holds, concerning what they call the “split poly-A tail invention”, feels more justifiable for patent purposes. Derek had to spend some time reviewing the patent body to understand what they mean when they say “split”, but more plainly, the patent describes including multiple features in a given mRNA molecule downstream from the coding region, most often two poly-A tails in series separated by a spacer sequence, as opposed to the single poly-A tail element usually seen in natural eukaryotic (non-bacterial) mRNA molecules. It isn’t immediately clear that this kind of sequence modification would result in an mRNA molecule with increased stability, half-life, protein yield, etc. versus the starting sequence, so from that perspective the patent feels safe.

Playing devil’s advocate, though, one could hypothesize that any observed additional stability is solely because the downstream segment of the mRNA is “just longer than normal”, a fact known and cited by the patent as increasing mRNA half-life when applied to natural poly-A tails; and the composition of that sequence doesn’t matter as much as long as it ends with a poly-A tail. We suspect that the patent authors take the results of that cited paper as the “base case” that the modified mRNA has increased expression over natural mRNA, and thus they do not include any unmodified sequences in their patent examples.

Given the combinatorial explosion of sequence elements one could attach to the end of a coding sequence and the costs required to perform these assays, it’s understandable they would focus their efforts on variations of the work from the cited article and patent the result that offered the biggest observed increase in protein expression. We don’t think this is a strong enough counterpoint in and of itself to invalidate the patent, but it’s really hard to say based solely on the data presented in the patent.

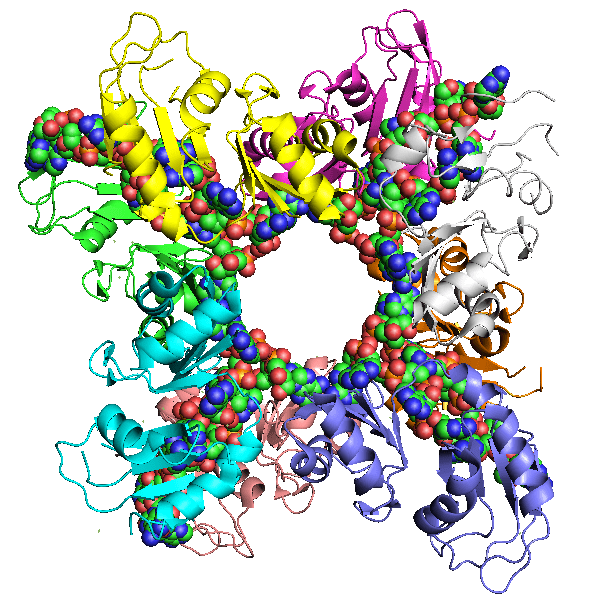

Poly-A RNA in complex with a binding protein, key to its function (Wikipedia)

With the science lecture out of the way, let’s talk a bit more about the business implications of this patent kerfuffle. If CureVac doesn’t have the patent protection on the mRNA engineering tech, that brings them right back in line with the other big mRNA pharmaceutical makers, namely BioNTech (BNTX) and Moderna (MRNA). Mentioning those two names, it’s impossible not to look back to the COVID pandemic and wonder: if CureVac was as pioneering as they claim to be with mRNA-based vaccine technology, why weren’t they able to productionize and monetize their technology in the same way as those other companies? Given the sensitivity of their stock to the patent litigation, it stands to reason that licensing the IP was meant to be the primary revenue stream as opposed to developing drugs, perhaps a model more suited to academic types. Now that model is in jeopardy, leaving CureVac the proverbial “day late, dollar short” in the clinic.

What’s more, this wake-up call comes at a time when the macro for COVID vaccine makers is souring, as exemplified by the big pharma partners in the space, Pfizer (PFE) and Roche (OTCQX:RHHBY). So even if CureVac is able to bring another mRNA-based COVID vaccine to market, it may not be the windfall they were hoping for to catapult them to the next level. The rest of their pipeline is a smattering of other projects, including:

Influenza vaccines

Malaria and rotavirus vaccines

Cancer immunotherapy, akin to Moderna’s individualized neoantigen therapy (there’s no evidence of an IP dispute brewing here yet, perhaps too early to call?)

Other RNA-based molecular therapies, such as a more efficient Cas9 “gene editing” platform

Given much of this work is funded by either federal agencies (the German government) or non-profits (such as the Gates Foundation for the malaria and rota vaccines), they explicitly mention in their annual report’s risks that the terms of the agreements may require them to either make their materials available freely/cheaply for certain populations, or to take a haircut on the sales of these therapies to make them widely available in the most vulnerable parts of the world. While that’s noble, it again smacks of being a bit too high-minded in what has quickly become a very profit-focused part of the biotech market.

It’s definitely rough goings from a macro standpoint, but there are reasons to be optimistic that the company isn’t going to collapse in the near-term. There are some hypothetical endgames out there that are worth hashing out, given there’s a potential weed whacker coming for the patent thicket.

CureVac’s influenza and COVID vaccines are part of a joint effort with GSK (GSK), which tracks with the collaborations of other mRNA pure plays, namely BioNTech and Pfizer. It’s a pretty sweet deal for a company at this stage: they get upfront cash to keep the lights on and fund clinical trials, and the big pharma company gets to claim “innovation” while both reap proportionately healthy revenues from the big pharma’s scope and marketing power. An out-and-out acquisition could very well be in order if the technology is truly that impressive and GSK wants to stay that one step ahead of Pfizer et al. CureVac stated on their most recent earnings call that they have a cash runway until mid-2025, so the idea of a buyout here is purely intellectual speculation for the time being.

CureVac brags about their production ability almost as much as they do about their basic science, which could very well be a good pivot for them if the mRNA engineering patents really do get invalidated. They highlight a scaled-down production setup called The RNA Printer, which they claim can be deployed in hospitals to allow point-of-care production of RNA therapeutics for patients. Cancer treatments and gene editing therapies like Cas9 feel like pretty good candidates for this kind of application.

If they really understand the ins and outs of nucleic acid production, formulation and such, that would make them fantastic engineering partners, planning out custom and semi-custom RNA production deployments for new builds: hospitals, research facilities, universities, etc. Most cheap outsourceable oligonucleotide work only deals with DNA, since RNA is a less stable molecule; having an on-site production facility eliminates that variable from the equation and would be massively beneficial to basic science doing research on RNA.

If the vaccine work fizzles out or doesn’t produce revenue like they or their partners would want, this technology could very well be a second wind that plays better to their strengths as technologists and researchers versus productization and commercialization.

In reviewing CureVac’s financials, there is a glaring standout that we were surprised to see unmentioned by other analysts or even the news: in the annual report dated April 25, 2023, page F-3, CureVac’s auditor expressed an adverse opinion on the company’s internal control over financial reporting. The specific material weakness was identified as “an IT system’s functionalities having not been configured to support segregation of duties in the recording of manual journal entries as well as in the authorization of purchase orders.” This particular weakness had been identified the previous year, but they were unable to complete their remediation plan during the year. Digging deeper, there have been disclosed material weaknesses in internal control since the company went public:

In the annual filing for 2020, they listed both “a lack of sufficient accounting and supervisory personnel who have the appropriate level of technical accounting experience and training” and “a lack of established accounting processes and procedures for new complex transactions and consistent application of existing accounting processes and procedures” as material weaknesses

In the 2021 filing, along with the IT-based weakness, they mention “business controls which were not adequately designed and operating effectively as a result of gaps in the identification of risks, precision of review controls and documentation to evidence control performance” as another weakness

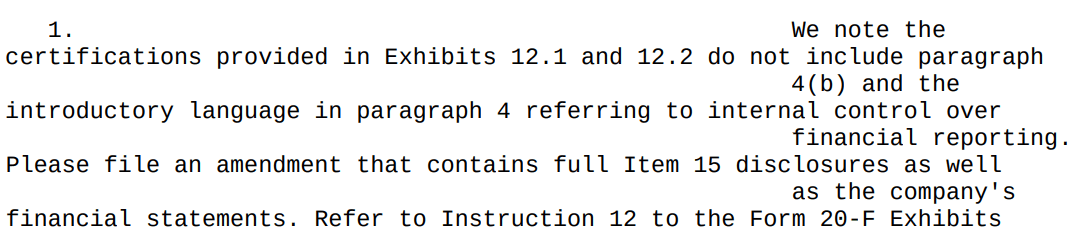

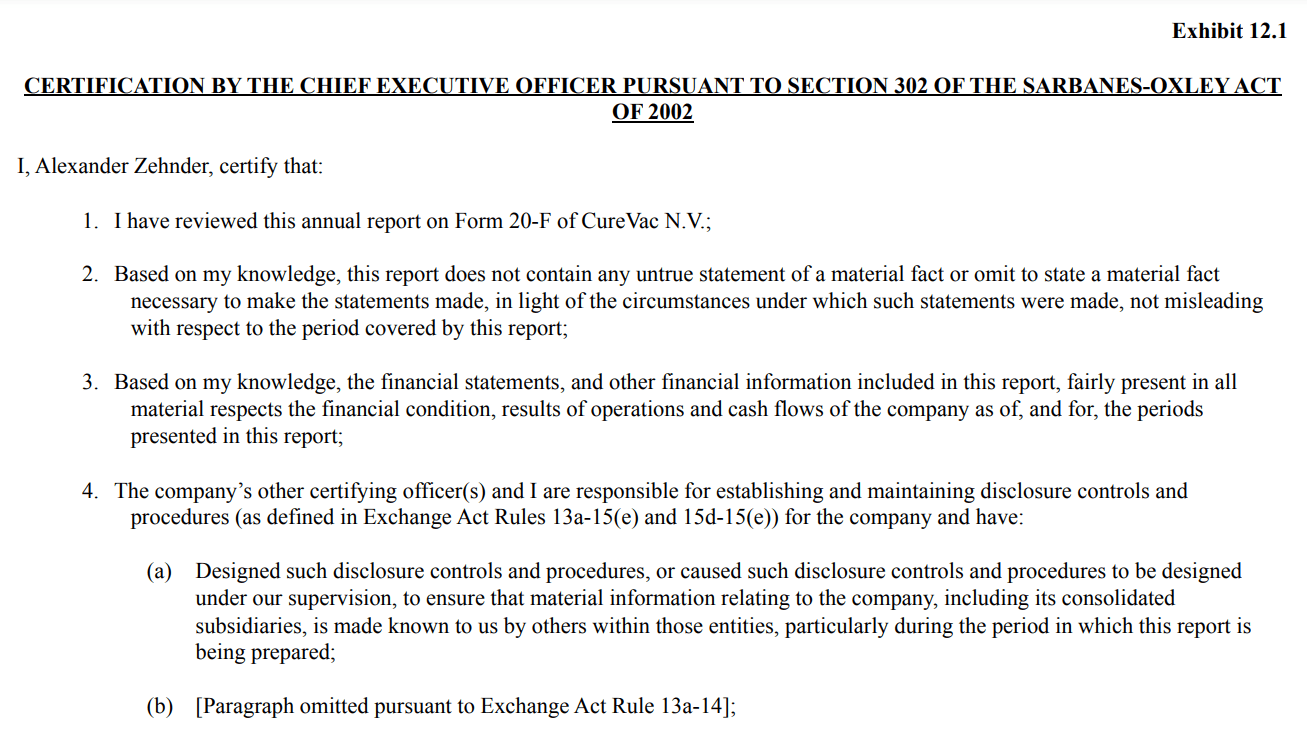

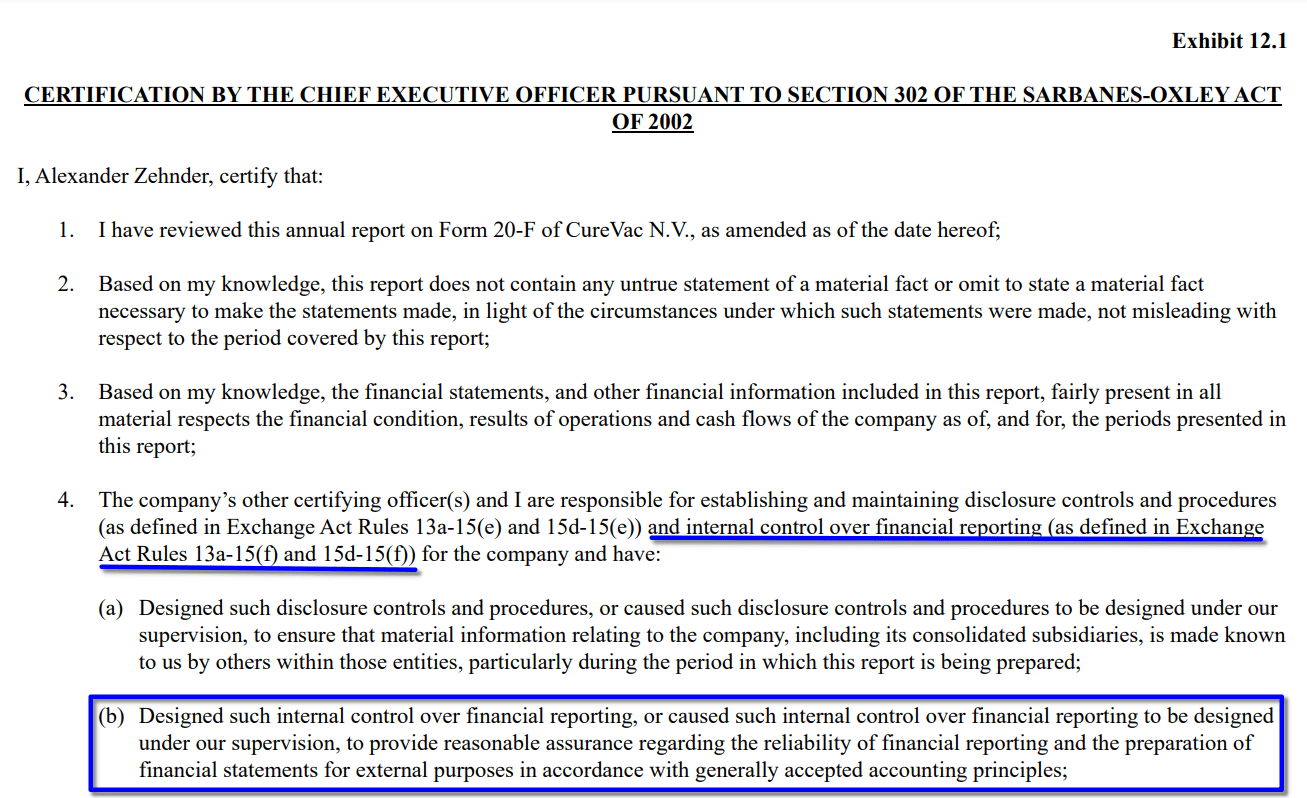

The SEC had to send a notice to CureVac asking them to revise their 2022 annual filing because it was missing key paragraphs in the CEO and CFO’s Sarbanes-Oxley certifications concerning their roles in having internal controls established at the company:

Excerpt from SEC notice to CureVac dated Sep. 26, 2023. Exhibits 12.1 and 12.2 refer to certifications pursuant to Section 302 of the Sarbanes-Oxley Act (CureVac IR) Excerpt of Exhibit 12.1 from the original 20-F filing, showing the CEO's certification pursuant to Section 302 of the Sarbanes-Oxley Act (CureVac IR) Excerpt of the amended Exhibit 12.1 filed October 12, 2023. Sections added in response to the SEC notice are highlighted in blue. (CureVac IR)

These material weaknesses are not difficult to address by any means. Betsy has a lot of experience with internal control from her time in accounting departments with companies much smaller than CureVac trying to go public. Internal control is something your auditors, IPO advisors and the like should actively help you build and solidify; they would only leave you with adverse opinions and material weakness disclosures if they had literally no other option. A trustworthy internal control system is a hard prerequisite for us to consider a company investment-grade.

Analyzing another clinical-stage company in Corvus Pharmaceuticals (CRVS) gave us a good head start on this article in terms of reviewing patents and projecting value at the pre-revenue stage. CureVac, however, is just different enough to make it tough.

Looking at the landscape, the most comparable name in our sphere we can see for their business model is Roche (RHHBY), whose diagnostics and pharmaceutical businesses are distinct enough revenue streams to operate independently but managed well enough to produce synergistic effects for the company. CureVac’s pharma business and their RNA printer business, from what we can tell, are distinct enough that either could survive in isolation, but if the two can succeed together, they would provide substantial ROI (the ifs here are quite long, though, as we have already established).

On the drug making side, we have two very clear pure-play examples in Moderna and BioNTech. BioNTech is probably a fairer comparison, given the tight partnership with Pfizer and the German domicile. BioNTech’s price went on a wild ride thanks to the COVID vaccine bolus, but has returned to a steady “up and to the right” trend.

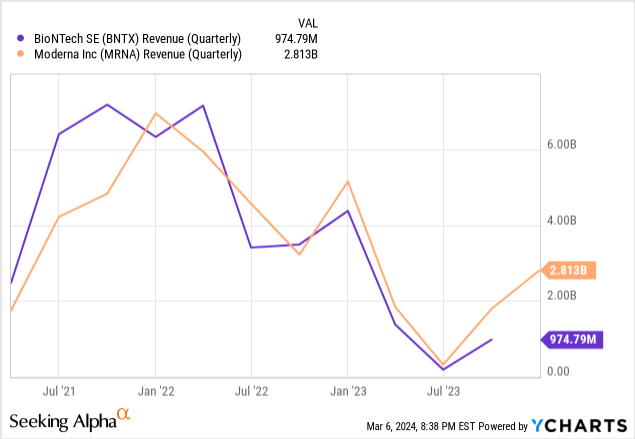

We use Price-to-Sales ratios in a multiple comparison, since CureVac has no net income and thus no meaningful bottom-line metrics. BioNTech has a forward EV/Sales ratio of 2.37 and a forward Price/Sales ratio of 6.02, versus 4.60 and 10.99 respectively for CureVac. Looking at the most recent quarterly revenues for BioNTech and Moderna, the party has really ended for mRNA vaccine makers:

Given the roughly two-to-one market shares, we estimate that in the best case, CureVac’s pharma portfolio will match BioNTech, giving them about 25% of the market share. The mRNA vaccine market is projected to grow at about 9.6% annually, reaching $27.7B by 2032. With 25% market share, that translates to about $7B for CureVac in 2032. With an EV/Sales ratio of 2.37, that gives us a future value of $16.4B for the pharma division. As for the likelihood of this outcome, with their most advanced drugs only in Phase 2, the focus on IP over product, and a headwind for being late to the market, we weight it at 10%.

The RNA printer business feels much more promising, given the lack of big-name effort in this space and the potential of tailored mRNA solutions in point-of-care settings. Its novelty also makes it a lot harder to value since there’s no good “pure play” reference points. Turning back to Roche as our reference, their diagnostics-to-pharma revenue split is about three-to-one, but given our sour view on the pharma side of CureVac, we project the future revenue split for these two arms as one-to-one or even two-to-one in favor of the RNA printer business. Splitting the difference based on our future value estimate for the pharma business, we project this business could be worth $25B. We put the success likelihood here at 20%, given:

Producing biotech equipment is more cap-intensive than producing pharmaceuticals

The RNA Printer business is newer, and the market for it is harder to assess (is it a hammer looking for a nail?)

They still have to execute and find care centers with space and patience to deploy these machines, which takes time.

Altogether, that gives the company a combined future revenue estimate of around $6-7B. Their cost of equity by CAPM has been hovering around 11.5% using 36-month betas and a 6% equity risk premium, and there’s no net debt to speak of considering their almost $500M in cash on hand. Discounting to the present gives us a rough valuation of $2.5B, which is about 3.25x their current market cap, a weighted-average price of $11.29/sh, in the lower quartiles of the analysts’ estimates.

Our valuation also takes as a base case that there is no benefit from their patents. If the split poly-A tail patent is upheld, that could increase their value in a buyout. There is still the matter of if this patent was infringed upon to decide, so there’s too much uncertainty around the value-add for us to consider it in the analysis.

Despite the allure of the outsized return, we cannot recommend CureVac. Two of the most important pieces necessary for a good investment – good business model and good culture – are not in place, as far as we can see. The IP protection the company thought they perhaps could rely upon for a stream of royalties is in jeopardy, and we don’t see it adding material value in the near future. That has left them exposed on the pharmaceutical development side, and although we think the RNA Printer is a promising idea, landing it with clients is still a large order without a Big Pharma partner to help defray costs. Meanwhile, the company has never issued financial statements to the U.S. Securities and Exchange Commission without some kind of “material weakness” disclosed about their internal controls.

For us to even begin to consider recommendation, we would need to see a substantial change in management’s approach to their internal control, possibly up to and including replacement of key individuals. The fact that the CEO just recently took over in April 2023 is hopefully a sign that they’re on pace for remediation, but their CFO has been in the role since 2016, well before they went public. With that wild card still in the air, we can’t recommend them, regardless of any potential upside. This analysis is a stark reminder to us that the skills which make you a successful scientist, academic and researcher do not necessarily correlate with skills which make you a successful entrepreneur, businessperson or company executive.