Luis Alvarez/DigitalVision via Getty Images

Luis Alvarez/DigitalVision via Getty Images

Torrid Holdings Inc. (NYSE:CURV) is a small-cap DTC (direct-to-consumer) retailer that has something of a niche positioning. Essentially, CURV provides a range of apparel, intimates, and accessories for 25-40 year old North American women, with plus-size fitting. Contrary to initial impressions, this is not a small market (at least the segments covering apparel and intimates), believed to be sized at around $85bn. However, it is rather fragmented, as CURV, with roughly $1.16bn in trailing sales (and around 4m active customers), is believed to be the category leader with a share of just 1.3%.

Torrid’s management believes they are well positioned to build clout here, as this is a market that has traditionally been neglected by the well-established players in the broader industry; for context, less than 2% of apparel stores are dedicated to plus-size women.

CURV wants to be seen as an entity providing dedicated focus to this segment, and rather than producing non-plus-size apparel that can be adjusted, they make sure they stay true to their target market, as every single piece of clothing they produce, is fitted on a real woman. They also have an in-house concept whereby store teams are required to personally try on their products to validate the fit. CURV is also not particularly hung-up about focusing on sales via just one channel, and they are flexible about both e-commerce and in-stores.

One would think that all these practices may help generate a sense of customer stickiness and loyalty, and this can perhaps be gleaned from the strength of the company’s loyalty program. Torrid essentially runs a three-tier loyalty program, consisting of insider members who spend up to $499 p.a., Torrid Loyalists who spend between $500-$1000 p.a., and Torrid VIPs who spend over $1000 p.a. Note that over 95% of the company’s sales comes from clients who are part of the loyalty program.

Whilst we can appreciate the intent of CURV to cater to a neglected, niche market, we are not sufficiently convinced this is a business worth getting behind.

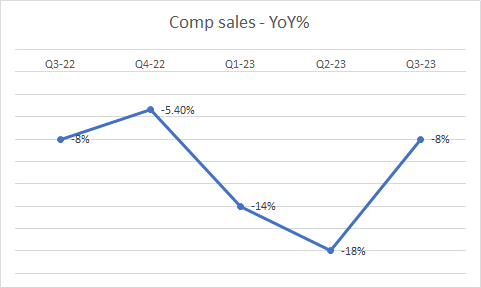

Firstly, consider that this is a business that has been losing ground for multiple quarters now, and that trend isn’t likely to change any time soon; over the last 5 quarters, one has seen consistent negative comp sales growth on a YoY basis.

Quarterly press release

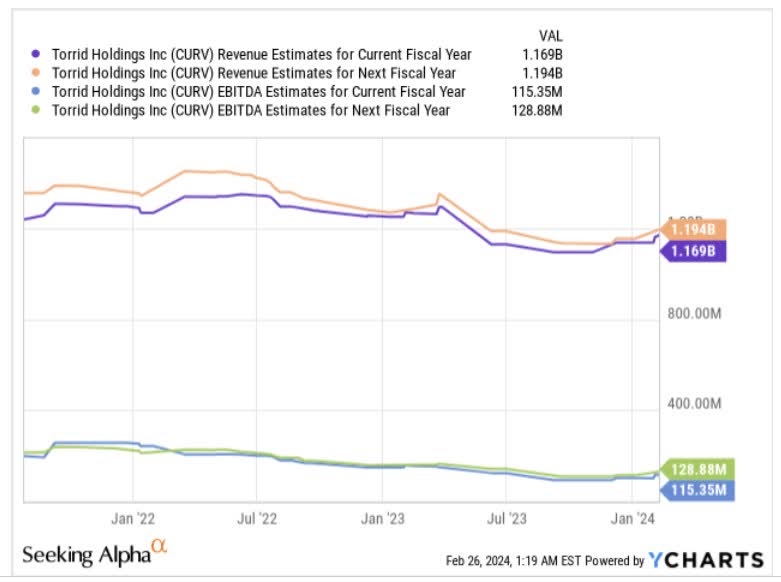

Despite having the benefit of a weak base effect (last year’s Q4 reported revenue had dropped by -8% YoY), it looks like the Q4 results (Torrid Holdings Inc. follows a Jan ending fiscal) will likely see yet another decline with reported revenue poised to come in -16% lower. In fact, it’s worth noting that consensus estimates don’t expect CURV to cross the sales rate it delivered in the FY ending Jan 2022 (almost $1.3bn) until FY27!

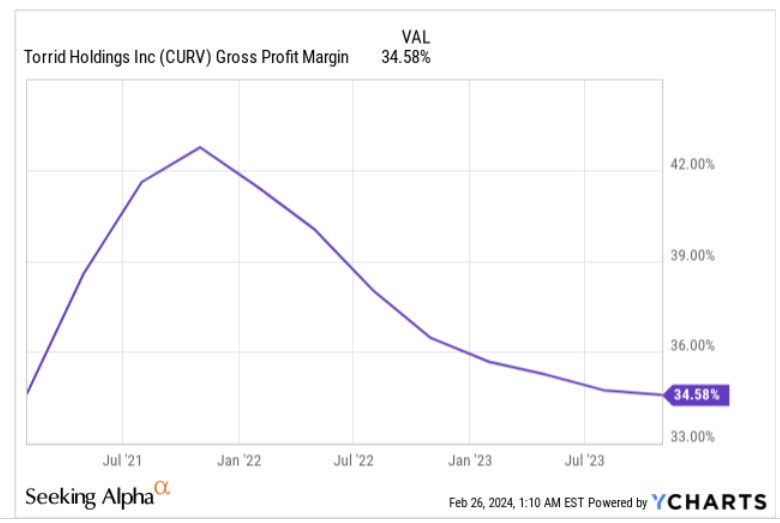

Note also how CURV's gross margins (on a trailing twelve-month basis) have contracted by almost 1000 bps over the last couple of years.

YCharts

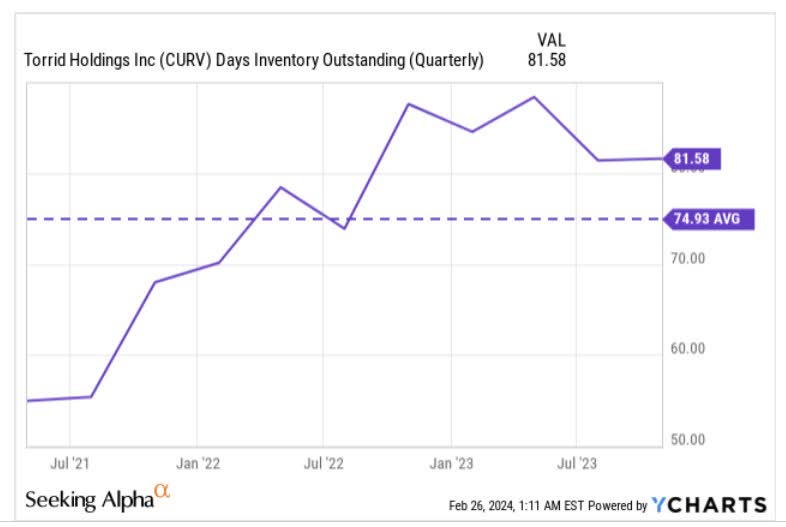

It remains to be seen how CURV fared during the holiday season, but do consider that its inventory levels are already well quite above the norm (approximately 75 days), and if sales weren’t resolute enough, this will likely result in further gross margin pressure as they seek to unload excess inventory post the holiday season. Already it’s worth highlighting that retail sales in Jan across the broader industry have been quite weak, coming in-0.8% lower, as against an expectation of a -0.1% drop.

YCharts

Low store occupancy and volume too has been driving gross margin pressure, as is subdued credit card-related revenue (which you would expect, given the financing environment).

Then, on the OPEX base, management is likely to press the pedal with digital marketing spend, and that also means that EBITDA improvements may not be meaningful enough. If one looks at implied consensus estimates on the EBITDA margin front for next year, don’t get carried away by the implied 10.8% margin that is expected, as it will still be a good 100bps lower than what was seen in FY22.

YCharts

The other challenge to note is that CURV’s balance sheet isn’t in the best state. Torrid’s current cash balance is just a miserly $15.6m, roughly only a fifth of what was seen in Jan 2021 ($123m). Note that traditionally this is a firm that has generated around $20m of FCF per quarter, but since late 2021, FCF generation has largely been negative.

When you can’t generate ample internally generated cash, you’re then forced to rely on external financing, and here, we feel quite uncomfortable with the level of debt that the business is carrying (the company currently has over a half a billion worth of debt on its balance sheet, which more than exceeds its asset base, with an implied net debt to EBITDA of nearly 3x).

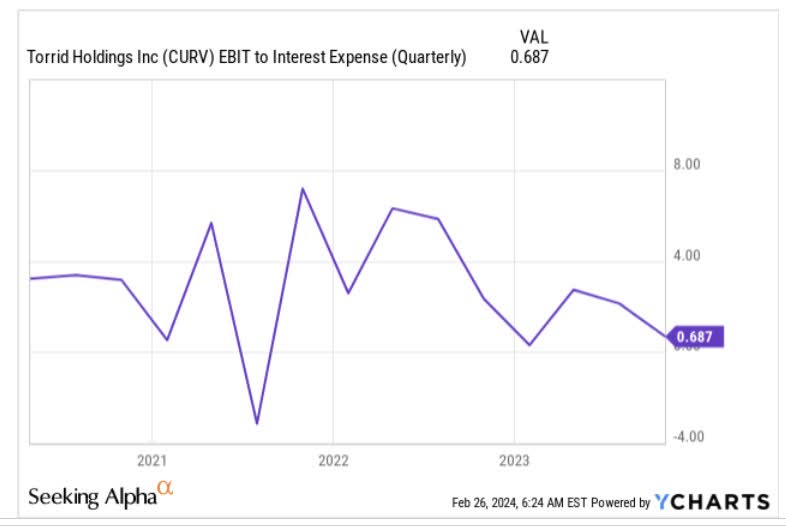

What’s also troubling is that recently, there have been quite a few quarters where CURV hasn’t generated ample EBIT to even cover the interest bill associated with that debt. Since it’s already highly financially geared, we’ve now seen the company resort to a$600m mixed-shelf offering, which will likely bring fresh dilution risks to shareholders down the line.

YCharts

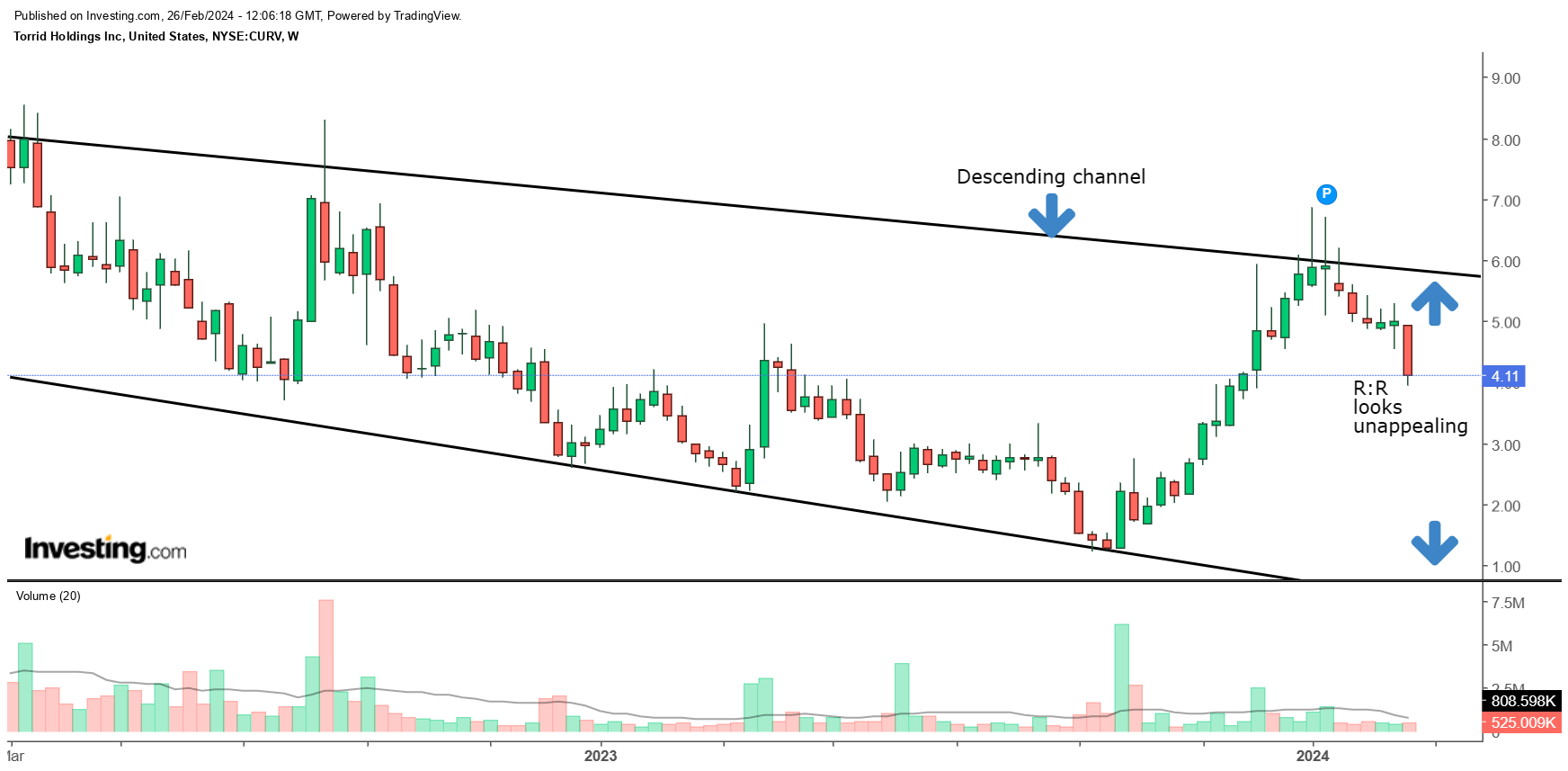

Finally, if we look at CURV’s weekly chart, it’s difficult to be too gung-ho about a long position now. Note that since March 2022, Torrid’s stock has been losing ground via the shape of a descending channel (marked by the two black lines). As things stand, the price is a lot closer to the upper boundary, of the channel, implying unfavorable reward to risk.

Investing