PM Images

PM Images

Dear readers,

Today I want to cover a self-storage REIT CubeSmart (NYSE:CUBE). I last wrote about the company in March 2023 using their Q4 2022 results and issued a hold rating because I thought it was overvalued based on a relative multiple, which was almost the same as the historical average, and an implied cap rate of only 5.4%. Today I will assess the latest Q4 2023 results and see how the company has been performing.

The price has dropped by about 3% since my last article, which supports my argument that the boom we saw for self-storage is over and CUBE will be stagnant or underperform going forward. While the company has tried to diversify its portfolio and add properties in the suburbs, I am not sure that this will be enough to make a significant difference for them.

The self-storage industry has seen great growth in the past, however, during the years of the pandemic, many people were moving away from cities and to the suburbs, which eliminated the need for self-storage as people moved into bigger spaces (generally out of apartments and into houses). This is, of course, not beneficial for the industry. Even now that the pandemic is over, people seem to be staying in the suburbs a lot, so the industry's growth is nowhere to be seen. CUBE is no different from the rest of the industry, and its price has not changed much compared to March of last year. This is not too surprising also because the product offered is pretty homogeneous, so all the self-storage REITs have been competing for customers.

Now for CUBE itself, they have 1406 properties and are the third largest self-storage REIT. They have the most units in New York City, and are now expanding to 40 metropolitan statistical areas (MSAs) in the United States, in which 90% of stores are owned by CubeSmart. They expanded their units from cities into suburbs to ensure stable attractive demand trends for the long term. Regarding acquisitions, since CUBE started expanding in different MSAs across the United States, and therefore started building its portfolio on reliable and strong demographics, the local community now ensures solid and steady demand in its submarkets. Moreover, since 2018, CUBE has closed $3.1 billion of acquisitions on its own, in combination with $1.6 billion of acquisitions managed by a third party.

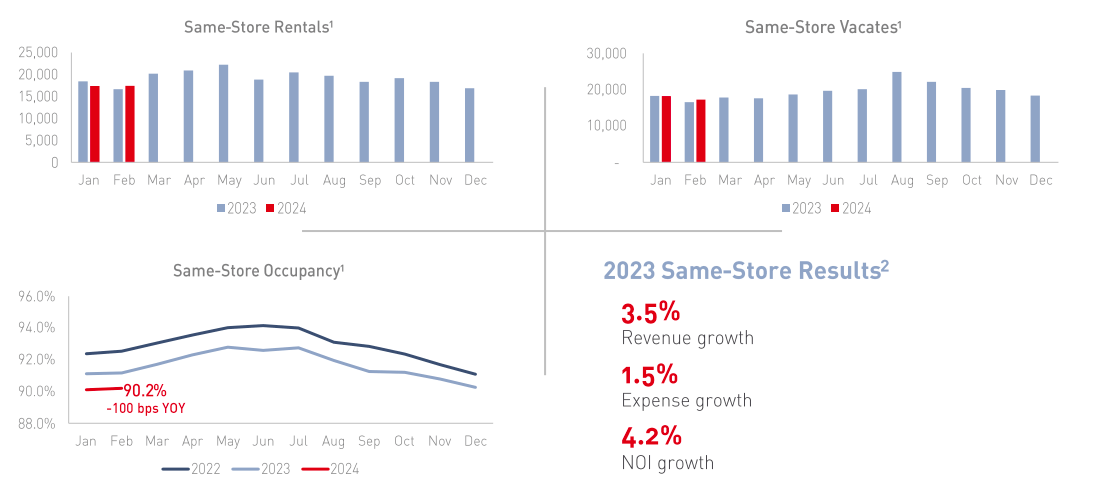

As for financials, CUBE had an average occupancy of 90.3% after the fourth quarter, compared to 90.8% in Q3. This is not too big of a drop but still not a very high occupancy's overall. In the fourth quarter, same-store NOI increased by 1.2% year-over-year, driven by 0.4% revenue growth and a 1.8% decrease in operating expenses.

CUBE

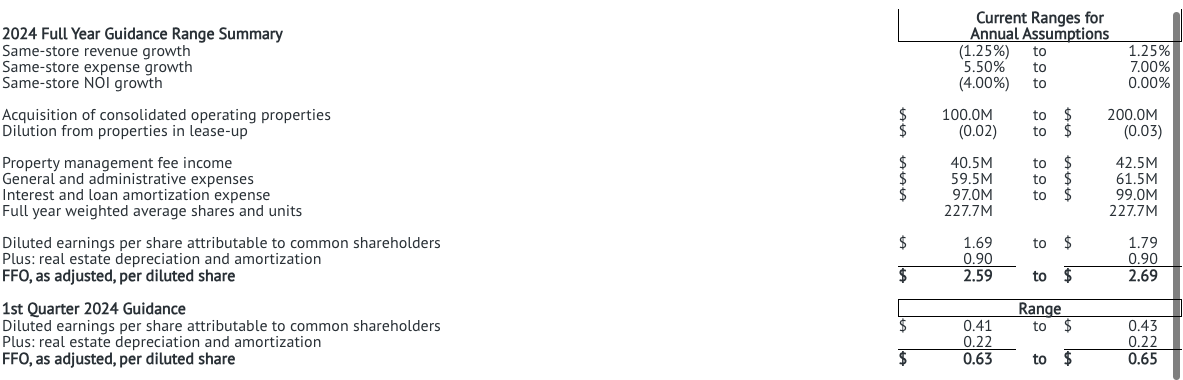

Full-year 2024 guidance calls for the same-store revenue growth to remain relatively stable at 1.25%. On the contrary, same-store expense growth is predicted to rise between 5.5% and 7%, mostly because of sharp increase in insurance costs. Same-store NOI growth is approximated to be in the range from 0% to 4%. As for the first quarter of 2024, earnings per share are expected to be between $0.41 and $0.43, and FFO per diluted share for the first quarter of 2024 is estimated at $0.63 to $0.65. FFO per share for the fourth quarter of 2023 was $2.68 and is now estimated to be between $2.59 and $2.69 in 2024. So, in short, next year is not looking really bright for CUBE in terms of FFO growth.

CUBE

CUBE's balance sheet is BBB-rated, so it is relatively stable and safe. The weighted average interest rate is 3% which is on the lower side. The debt totals $2.97 million, and they have the following maturities: in 2024 only $30 million matures, then in 2025 $300 million, and later in 2026 $335 million needs to be paid. The maturities are pretty well spread out over the years; however, CUBE does not have much cash and only has $18 million available under their credit line, so they are going to have to find funds to pay off their debt elsewhere. But they have time to deal with this since they have low maturities in 2024. I also like that their interest rate is not too high, so it is not going to be that much of a burden, at least for now.

CUBE presentation

The company has declared a dividend of $0.51 per share for 2024, which is an increase of 4.1% compared to the previously declared dividend for 2023 of $0.49 per share. CUBE has a history of increasing their dividends, so it is possible they will continue to do so unless they encounter some major problems. The dividend yield is 4.6% and the payout ratio is 75.8%.

Recently, CUBE has changed its strategy and has been trying to target customers in the suburban areas, which is a good strategy considering a lot of people have moved to the Sunbelt and live in bigger houses, further from city centers. However, I don't think it will be enough to make a significant difference in the stock price since there is not as much demand compared to urban areas because people have bigger houses with more storage at home, eliminating the need for storage elsewhere.

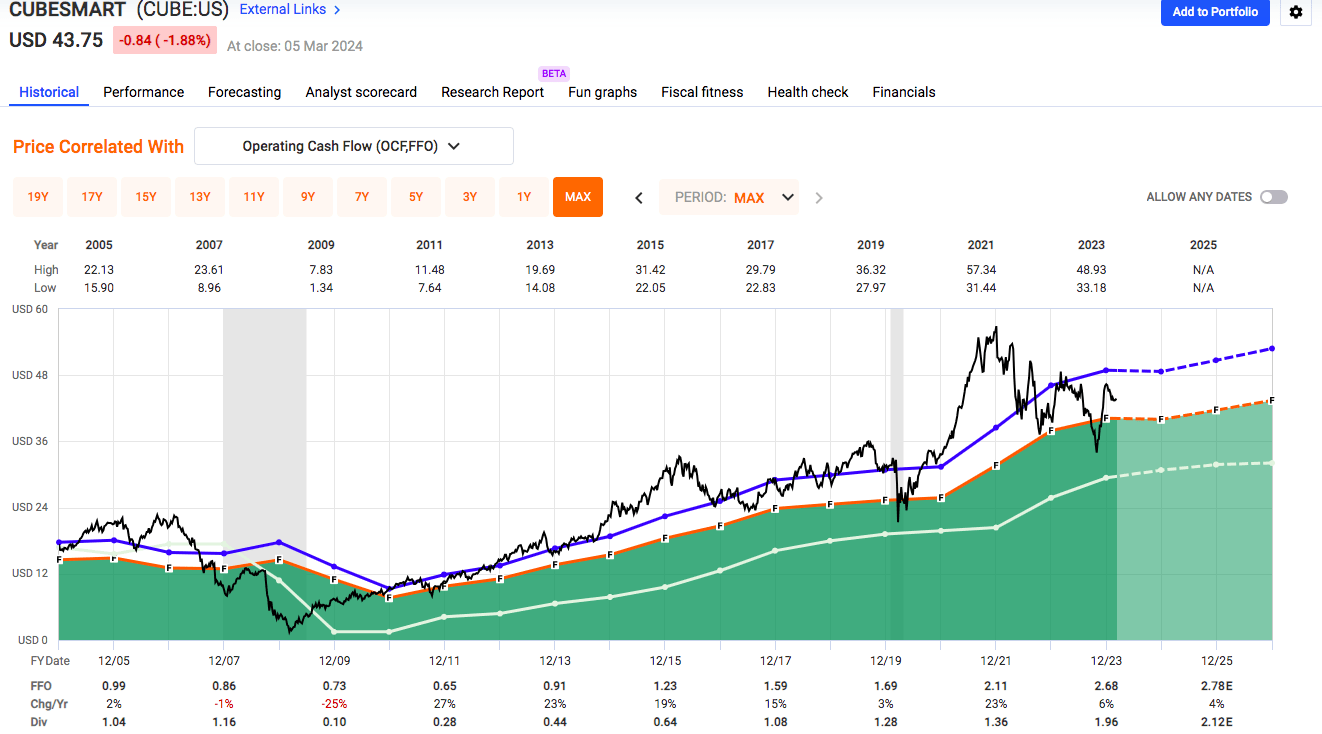

For this reason, demand for self-storage has not increased, but it's rather the same over the years. CubeSmart's P/FFO stands at 16.34x, with a historical average of 18.25x. Compared to their competitors, such as Public Storage (PSA), whose P/FFO is 16.55x, or Extra Space Storage (EXR) with P/FFO of 18.27x. Since they sell similar products, I don't think that neither company deserves a discount or a premium because of the product itself. In terms of growth, CUBE has been sort of in the middle compared to peers and dropped by 4% in the last year as opposed to PSA's 2.5% decrease and EXR's 8% decline. Their BBB balance sheet is rated the worst (PSA is A rated and EXR is BBB+) so when considering that I would even expect CUBE to have a small discount towards PSA. It is also the smallest out of the three in terms of their market cap, which is another reason why I would expect a small discount, which is not the case, at least not for EXR and PSA.

Also, considering that the market is pretty stagnant at the moment, I think the P/FFO it is too high as it is not too far off from the historical average. Moreover, a 4.6% yield is not high enough, in my opinion, therefore I wouldn't invest for the dividend only. In addition, FFO is supposed to remain the same or even decrease in the next year, so I don't see a lot of growth for the company in the near future. Overall, I think that the best days are over for self-storage and that the company will remain stagnant for now, which is why I rate the stock a HOLD at this time.

FastGraphs