Tony Anderson

Tony Anderson

The Direxion Daily Homebuilders & Supplies Bull 3X Shares ETF (NYSEARCA:NAIL) is a leveraged exchange-traded fund, or ETF, that covers an index containing some of the major U.S. homebuilders. We think that while news has been good for the homebuilding sector, particularly on rates, good news won't become better news anytime soon, so a leveraged ETF is a little out of the question for now as far as we're concerned. First, a critical note on the general issues of leveraged ETFs.

Because leveraged ETFs reset daily after mimicking changes in the index that day by a 3x factor in the case of NAIL, there is the problem of value erosion. While a 1% rebound after a 2% drop isn't so bad for the underlying index, having a 6% drop and a 3% rebound is more of a problem.

There is a reason why Warren Buffett's #1 rule is, don't lose money. If you lose money, you have less to recover with, meaning for every drop you need a bigger percentage recovery to bring you back to square 1. If an asset drops 33%, you need an almost 50% recovery to recover. If an asset drops 50%, you need 100% recovery to breakeven. Even if the next day is a bigger rebound than what you lost the previous day, with leveraged ETFs it is still less helpful even if the recovery gets doubled because more money was lost the prior day.

If you don't fully understand these risks, do not proceed with a leveraged ETF. They are best used over short durations because of value erosion. They are highly speculative burst instruments.

Links for reference on these risks:

There are also some advantages. Leveraged ETFs typically carry expense ratios that are below borrowing costs for doing margin trading. Also, some investors, particularly those that may be restricted from doing direct margin trading or shorting, can make use of leveraged ETFs regardless of those restrictions. However, value erosion is a major issue, and makes leveraged ETFs mainly useful over short horizons to speculate on key events.

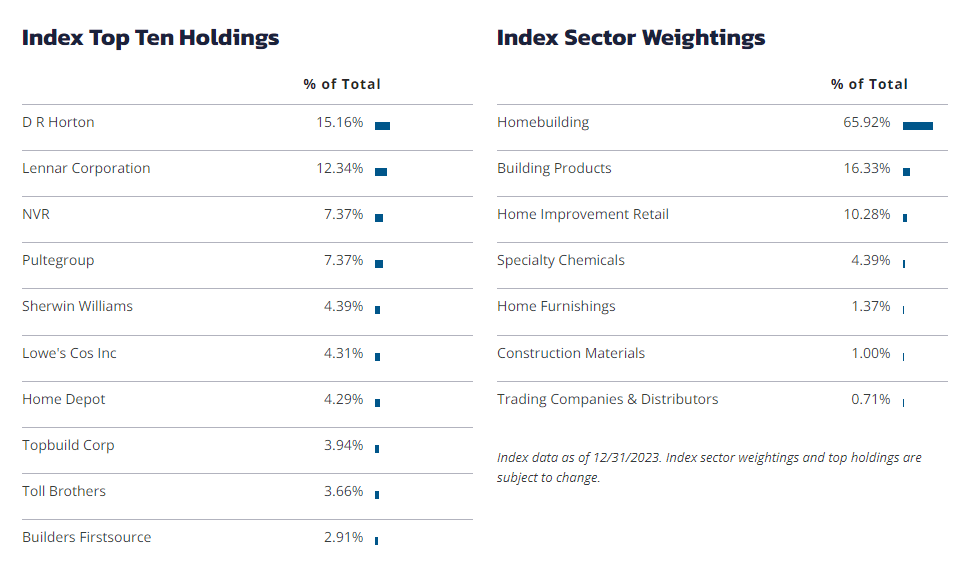

Moving onto NAIL's specific features, it follows an index with the following underlying weightings. It tracks this index with 3x daily resetting leverage at the same expense ratio as other Direxion ETFs, 0.98%. In principle, you are getting decent value with that since even 2x Direxion ETFs will have the same expense ratio.

Index (Direxion.com)

Certain things have gone well for the homebuilding business in recent months. The optimism around the rate situation in the U.S. towards the end of the year did a lot to start bringing down new mortgage rates, which has apparently increased interest in homebuilder inventory as of late. Optimism has reached global peaks, albeit remaining substantially below pre-pandemic levels still.

In terms of the performance of some of the larger allocations within NAIL, revenue trends haven't been that bad leading up to the end of the year, and the inventory of houses has been pretty stable - so no concerning and irrational bulges. Actually, revenue performance has been positive growth. Importantly, operating profits have actually held up as well, as some key costs, namely related to building products, have now been seeing limited inflation and deflation in some cases, and homebuilders do have quite a lot of bargaining power with vendors, all visible with companies like Carlisle Companies Incorporated (CSL) who've been winning on volumes only now, in great contrast to the situation a year ago.

Where we've been seeing interest rate-related delays in projects, including residential projects, we think that increased optimism and some proposed end to the rate cycle have made the segment a decent place to be. In building products, up the value chain, we've also been seeing very clear evidence that destocking trends related to delays downstream have now come to an end, and volumes have been picking up in a mild winter. Further downstream in home improvement activity, homeowners are reticent to do any more discretionary spending, having gotten a lot of it out of their system during COVID-19. Underlying demand is not improving in home improvement, it seems, and there's no expectation of that, either.

While performance has been good for the companies, and it shouldn't deteriorate too much further in the main sector weightings for the Direxion Daily Homebuilders & Supplies Bull 3X Shares ETF, it is unlikely that there will be further catalysts of good news to drive the bull ETF higher. Inflation is appearing sticky at current levels and has every reason to be given surveyed expectations. Optimism by markets also undermines the effectiveness of Fed policy in tightening conditions.

NAIL is a speculative instrument, and with markets having demonstrated a persistent bias towards optimism around a soft landing and the imminence of disinflation, totally ignoring basic economic data like rate expectations and wage growth trends, we have absolutely no expectation that rates will show a meaningful downward inclination over any horizon for which this ETF is suited, meaning over the next month or maximum two months.

As expectations for rate decreases may continue to falter, which has some effect on the rates in mortgages, which should need to decline for sentiment in the underlying NAIL index to improve, we don't think catalysts are imminent. Best to avoid NAIL, given its 3x sensitivity and the weak catalyst environment.