lovenimo/iStock via Getty Images

lovenimo/iStock via Getty Images

CrowdStrike Holdings (NASDAQ:CRWD) is one of the most significant investments in AI-led cybersecurity at the time of this writing, and it should be a large beneficiary of high market growth over the next decade. However, investors may want to consider the inhibition in price growth that could result from the premium valuation. Nonetheless, while I consider the stock overvalued at this time, I believe the long-term growth does outweigh this.

CrowdStrike leverages AI to provide a comprehensive suite of cybersecurity solutions. Its Falcon platform unifies cybersecurity operations, including endpoint security, threat intelligence, and cyber attack responses, into a cloud-delivered service.

The business model is subscription-based, and it emphasizes recurring revenue. It has the capability to tailor its solutions to the specific needs of industries, and it has clients ranging from finance, healthcare, retail, and government entities.

Recently, the company has made several key strategic moves, including acquiring Flow Security to expand in cloud security leadership, partnering with Dell Technologies (DELL) for managed detection and response, and introducing CrowdStrike SEC Readiness Offering to aid companies with new SEC breach disclosure rules. Additionally, its Charlotte AI is now available for general use, which is a generative AI technology used to enhance the firm's ability to stop breaches through threat analysis and real-time response.

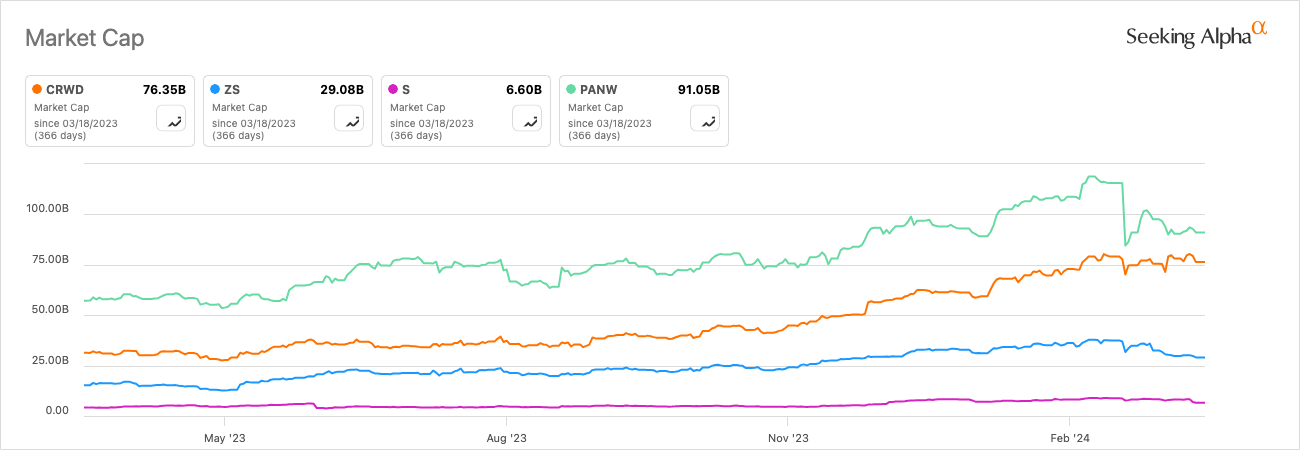

Key competitors in the market include Zscaler (ZS), SentinelOne (S), and Palo Alto Networks (PANW):

Author, Using Seeking Alpha

The key operational threats from these companies relate to the advancements in cloud security, AI-led threat detection, and platform utility. Zscaler competes significantly on cloud workload protection, SentinelOne on AI-led endpoint protection, competing with the Falcon platform, and Palo Alto Networks is a diversified competitor, including through network, cloud, and endpoint security.

The cybersecurity market is becoming evermore crucial to manage effectively with the advent of AI. I believe organizations are going to face significant breaches if not properly prepared, and CrowdStrike and its peers offer a need rather than a desire for most enterprises. Generative AI has the potential to revolutionize the cybersecurity industry, increasing security operation efficiencies, but AI also introduces new challenges, such as prompt injection attacks, API attacks, and inadvertent data leaks or exfiltration.

Additionally, the expansion of edge computing is bringing these technologies closer to the source of data, which is a great benefit to many industries looking for more comprehensive digitalization of data assets. However, there are, unfortunately, security risks that come along with this as the attack surface widens as a result. Therefore, the advance of computing power seems to directly correlate with the need for more advanced cybersecurity measures, and my opinion of the matter is that the market will experience exponential growth as a result of higher demand for digital products and services but greater reports of security issues. Advanced quantum computing is eventually going to be able to break conventional encryption algorithms, and so new standards are being set for quantum-resistant algorithms. The standard and the bar of effective data and cybersecurity is becoming higher every year, and investors will not need to look too deeply to understand the massive value I attach to firms like CrowdStrike as a result.

There are several market CAGR forecasts that are delivered from a range of research publications, which I have condensed here:

I believe these CAGRs are conservative, and my own estimate is at the upper end, toward 15%, although I believe this could be outperformed as AI gets more significantly accessed by criminal enterprises, driving higher demand for costlier security processes.

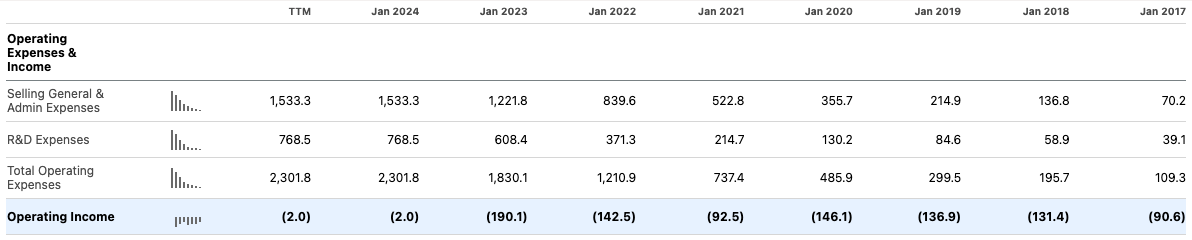

At this time, CrowdStrike has an operating loss, although it is very minimal when compared to previous reports, standing at just -$2 million for the last 12 months. In January 2023, it reported -$190.1 million in operating income.

Seeking Alpha

However, on the balance sheet, it has a high level of cash and equivalents, with $3,375.1 million reported over the last 12 months and $99.6 million in short-term investments. This significantly protects it, and as such, it has had only little total debt issued over the past few years, with a large issuance in 2021 of $739.6 million. However, it has been equity raising every single year for the past decade, and it has not repurchased common stock once over the period. While this may be of some concern to investors, we must remember this is a relatively new company, founded in 2011 with its IPO in just 2019. I believe that its high R&D expenses are wise to remain competitive, but overall, I do believe its financial position needs considerable strengthening before it can be deemed as a secure investment holding. Thankfully, the company's growth of 36.33% for YoY revenue and 47.13% for forward diluted EPS growth indicates strong future prospects as long as its capital structure is managed effectively.

At this time, the Chief Financial Officer of CrowdStrike is Burt Podbere, who was previously the CFO at OpenDNS, which was acquired by Cisco (CSCO). As a technology industry veteran, I believe he would do well to prioritize internal efficiency to drive down costs at a time when shareholders are undeniably looking for stable operating profit. Additionally, I believe the firm's long-term debt should be prioritized prior to any share buybacks, which, at this time, certainly seems to be the case. But with an equity-to-asset ratio of 0.35, both the balance sheet and the income statement need work, but its cash flow is exceptionally strong despite these weaknesses, with total cash flow from operations of $1,166.2 million over the past 12 months and a positive net change in cash since 2018, currently resting at $920.7 million.

Compared to the peers I have outlined above, here are the key metrics for consideration:

Of these peers, I find CRWD's metrics particularly appealing, as they show not only a positive net income margin but also a balance sheet and revenue growth rate which are significantly competitive. To my mind, an investment in CRWD provides somewhat more stability than in ZS or S, and while PNAW looks attractive, it has slightly slower growth.

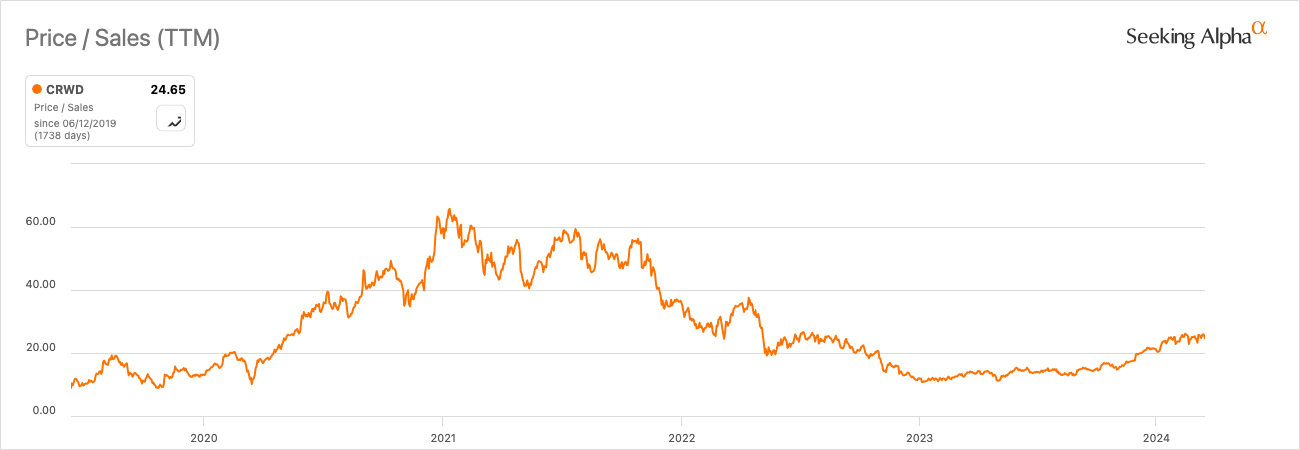

CrowdStrike currently sells at a TTM price-to-sales ratio of 24.65, but its average over the past five years is a price-to-sales ratio of 29.11. First of all, let us compare what is normal for the set of peers I have identified:

The average of ZS, S, and PANW in terms of current TTM price-to-sales ratios is 12.39. The average of ZS, S, and PANW in terms of five-year average TTM price-to-sales ratio is 19.34.

Considering this, CRWD has traded at a premium of 50.5% in terms of five-year averages over its peers on average in price-to-sales. At this time, it is trading at a 98.95% premium in price-to-sales to its peers on average. Whether CRWD's price is justified is difficult to ascertain, but we can see that the trend is downward for its price-to-sales ratio over the past three years, after significantly high investor sentiment for a period around the time of the global pandemic:

Seeking Alpha

From my analysis, a fair price-to-sales ratio for CRWD, and one that I believe the stock may be able to maintain over the long term, is 20. That indicates a premium on the stock at this time of approximately 23.25%. While this is of considerable risk for investors, the overvaluation does not mean that the stock is a bad investment; quite the contrary, I consider CRWD a Buy. However, it must be noted that some periods of lesser returns are likely due to overvaluation inhibitions in what otherwise seems to be a high-growth investment over the next 10 years.

One of the key risks and something that may deter investors is the high level of stock-based compensation. So, while there is no issuance of common stock at this time on the cash flow statement, the income statement is significantly weakened through said SBC. I believe this is good for the internal drive of the firm but bad for shorter-term shareholder interests, as it significantly dilutes present shareholder value. As of the last 12 months, CRWD's SBC has a total of $631.5 million.

This may be my favorite AI cybersecurity investment on the market at this time, and although the price is high for the stock, I believe it offers exposure to incredibly crucial operations that will be highly benefited from growing trends in technology at the moment, including heightened capabilities of technology malpractice which will need to be protected against. There is room for improvement as the firm develops in terms of its income statement and balance sheet, but with well-managed cash flow and what looks to me as prudent financial management, I am rating the stock a Buy.