Sophonnawit Inkaew

Sophonnawit Inkaew

We previously covered Crocs, Inc. (NASDAQ:CROX) in December 2023, discussing why the stock's recovery from the October 2023 bottom was likely to be unsustainable. This was attributed to the decelerating growth of its core brand and HeyDude's disappointing performance, worsened by the slowing sales in the North American region.

With it no longer offering a compelling growth story and no dividends, we had believed that the stock might at best trade sideways, until the management was able to generate convincing growth in sales.

In this article, we shall discuss why we are reversing our previous Hold rating to a Buy, as the CROX management offers a promising guidance for HeyDude sales recovery in H2'24, with the robust cash flow also well deployed towards deleveraging and share count retirement.

Combined with its discounted valuations, we may see the stock potentially double over the next few years, assuming a rerating in its FWD P/E nearer to its historical means and sector medians.

For now, CROX has reported top/ bottom line beats in the FQ4'23 earnings call, with revenues of $960.10M (-8.1% QoQ/ +1.6% YoY) and adj EPS of $2.58 (-20.6% QoQ/ -2.6% YoY), with FY2023 numbers of $3.96B (+11.5% YoY) and $12.03 (+10.1% YoY), respectively.

Much of the YoY tailwinds are attributed to the excellent demand for its core brand, Crocs, with revenues of $732.45M (-8.3% QoQ/ +9.9% YoY) in FQ4'23 and $3.01B (+13.5% YoY) in FY2023.

This well balances HeyDude's underwhelming sales of $227.64M (-7.8% QoQ/ -18.4% YoY) in FQ4'23 and $949.39M (+5.9% YoY) in FY2023.

This is mostly attributed to the weaker wholesale sales as the market digests the oversold inventory in 2022, which has resulted in the lowered FY2023 HeyDude sales guidance in the FQ2'23 earnings call.

Despite so, CROX's balance sheet continues to improve, with the management consistently deleveraging to long-term debts of $1.64B (-14.1% QoQ/ -28.3% YoY), triggering a lower debt-to-EBITDA ratio of 1.69x by the latest quarter.

This is compared to 1.98x in FQ3'23 and 2.93x in FQ4'22, while nearing the 1.34x reported in FY2019.

While the stock does not pay a dividend, shareholder returns have also been excellent, with the management retiring 1.52M shares/ the equivalent 2.4% of its float over the last twelve months, and 8.86M/ 12.6% since FY2019.

Therefore, while we are still uncertain about HeyDude's synergy potential, we believe that CROX has executed competently, in both managing the "inbound receipts that were ordered pre acquisition" and the challenging "price matching with the gray market goods."

This is especially since we have observed sustained improvement in its sell-through rate with moderating HeyDude inventory levels of $104M (-6.3% QoQ/ -38.4% YoY) and stable Average Selling Prices of $30.65 (+3.2% QoQ/ inline YoY) by the latest quarter.

At the same time, the CROX management has offered a promising forward commentary, in which the HeyDude inventory correction is likely to be completed by H1'24, with FY2024 sales to be "flat to slightly up" on a YoY basis.

With the worst of the HeyDude headwinds behind us, we can also understand why the management has offered a relatively promising FY2024 adj overall EPS guidance of $12.27 at the midpoint (+1.9% YoY), compared to the consensus estimates of $11.95 (-0.6% YoY).

Combined with the growing demand for CROX's products internationally with revenues of $1.38B (+24.3% YoY) well balancing the decelerating domestic sales at $2.57B (+5.7% YoY) in FY2023, compared to FY2022 levels of +38.7% and +62% YoY, respectively, we believe that its prospects remain bright ahead.

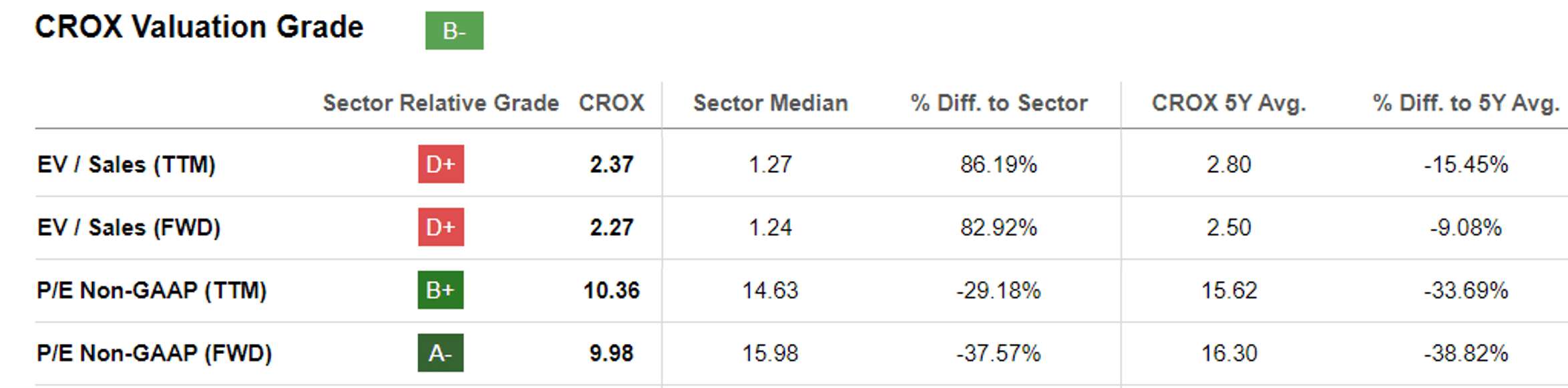

CROX Valuations

Seeking Alpha

As a result of these promising developments, we believe that the pessimism embedded in CROX's stock valuations may have been overly done, attributed to the discounted FWD EV/ Sales of 2.27x and FWD P/E of 9.98x.

This is compared to the pre-pandemic mean of 1.74x/ 20.64x and the sector median of 1.24x/ 15.98x, respectively.

Even when compared to its Consumer Discretionary stock peers, such as V.F. Corporation (VFC) at 1.19x/ 14.61x, Nike (NKE) at 2.95x/ 27.64x, and On Holding AG (ONON) at 5.43x/ 60.04x, it is apparent that CROX is undervalued here, with its prospects likely to be brighter as the HeyDude headwind lifts.

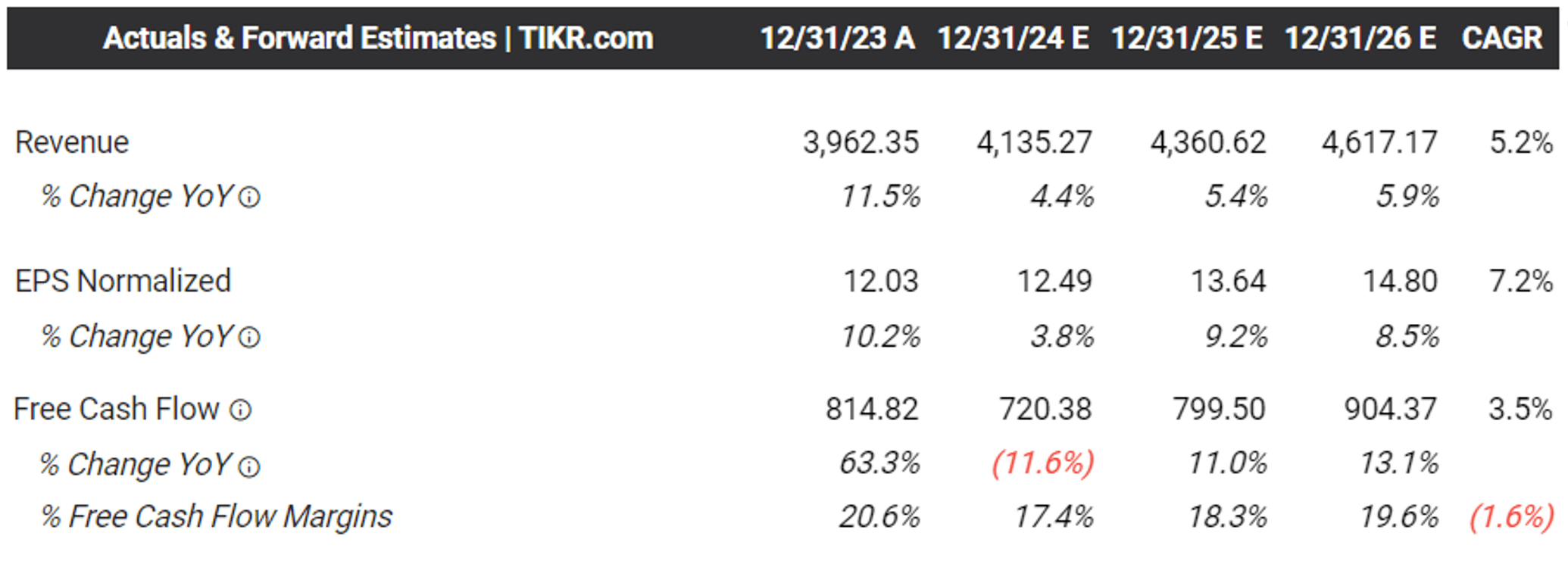

The Consensus Forward Estimates

Tikr Terminal

The same upgrade has also been observed in the consensus forward estimates, with CROX expected to generate an improved bottom line expansion at a CAGR of +7.2% through FY2026.

This is compared to the previous estimates of +4.28%, though drastically decelerated from the historical growth rate +105% between FY2017 and FY2023.

If anything, CROX's projected bottom line expansion may not pale in comparison to VFC's at -4.8%, though rightfully behind NKE's at +14.5% and ONON's at +37.4% over the same time period, implying that we may see an upward rerating in CROX's valuation close to VFC's ahead.

In addition, readers may want to note that CROX's Free Cash Flow generation is expected to remain exemplary over the next few years, allowing the management to consistently pay down debt to its leverage target of between 1x and 1.5x, with $875M still remaining on its share repurchase authorization.

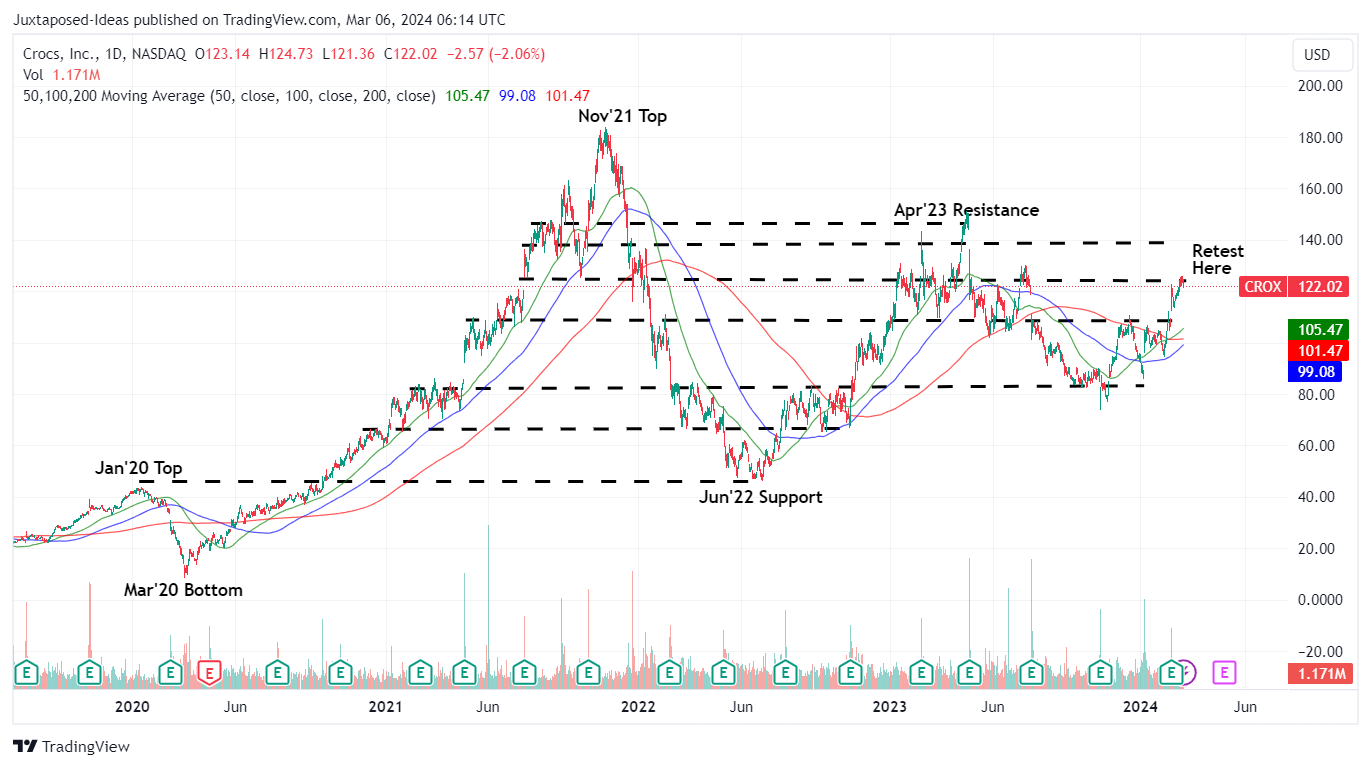

CROX 4Y Stock Price

Trading View

As a result of the excellent shareholder returns, healthier balance sheet, and promising forward guidance, we can understand why CROX has rapidly broken out of its 50/ 100/ 200 day moving averages, while retesting its previous resistance levels of $120s.

Based on the FY2023 adj EPS of $12.03 and the discounted FWD P/E valuations of 9.98x, the stock appears to be trading near our fair value estimates of $120.00.

We may also see CROX offer a nearly doubled upside potential to our long-term price target of $236.80, based on the consensus FY2026 adj EPS estimates of $14.80 and a speculative re-rating in its FWD P/E nearer to its 5Y average of 16x and the sector median of 15.98x.

As a result of the attractive risk/ reward ratio at current levels, we are carefully re-rating the CROX stock as a Buy here, though with no specific entry point since it depends on individual investors' dollar cost averages, and investing trajectory since its reversal may take a while.