metamorworks

metamorworks

Cerence (NASDAQ:CRNC) is a leading company in the field of automotive AI assistants. They develop technology that allows drivers to use their voice to control various aspects of their car, such as the navigation system, entertainment system, and climate settings. Their technology is used by many major car manufacturers around the world.

Upon its spin-off from Nuance in 2019, share performance has been lackluster. It reached an all-time high of $133 in 2021, a significant return from its spin-off price of $17 in 2019. However, the share price gradually trended down from the high thirties to the high teens for most of 2022. CRNC mostly saw sideways price action for most of 2023. It reached a 2023 high of $35, but has continued to decline into 2024. The stock currently trades at $14.8, down 22% YTD.

I initiate my coverage with a buy rating. My 1-year price target of $17.86 presents an over 20% upside from $14.82 today. At the current level, the stock appears undervalued.

YCharts

Fundamentals are not ideal, though there have been improvements as of Q1 2024, the latest quarter ending in December 2023. Revenue has seen considerable declines over the past two years. Having finished 2021 with a revenue of over $384 million, CRNC finished FY 2023 with a revenue of merely $294 million. In my view, it is a relatively dire outlook for a company that used to see over 10% annual growth just a few years ago.

The impact of declining revenue on cash from operations / OCF has been quite pronounced. CRNC generated over $74 million OCF just two years ago. Yet, OCF turned negative just the year after. OCF rebounded to $7.5 million in FY 2023, though in Q1 2024, CRNC ended up seeing a quarterly OCF loss of -$2.8 million.

CRNC has maintained an improving outlook of GAAP profitability, though given the past volatility, it could remain a challenge for CRNC going forward, in my opinion. In Q1 2024, CRNC saw a quarterly net profit margin of 17%, a relatively decent bottom-line performance. Furthermore, the net loss margin was over -19% last FY, an improvement from the prior year in FY 2022. I estimated FY 2022's net loss margin to be over -29% after adjusting for goodwill impairment of $213 million.

YCharts

Overall, the balance sheet looks decent. Debt-to-equity/DE ratio has seen a slight uptick over the past five years, though still below 0.4x, a reasonable level, in my opinion. The main reason has been the slight increase in long-term debt/LT debt. LT debt was over $277 million in Q1 2024, up 3% from 2020. CRNC has relied mostly on OCF and debt issuance to maintain its liquidity position. At $108.5 million today, the cash level has been relatively steady, considering the choppy growth performance as of late.

For FY 2024, CRNC has guided to a full-year revenue of $355-375 million, implying a revenue growth of over 20-27%.

company presentation

At that rate, it means that CRNC will be seeing stronger annual top-line growth than it did in the past five years. Based on the management's comment in the Q1 2024 earnings call, I believe there are a few catalysts that could help CRNC deliver an acceleration at that scale.

One key driver is the strong adoption of their innovative solutions. CRNC's new offering, Chat Pro, powered by Generative AI and LLM, is generating substantial interest from both existing and new players in the automotive industry:

So, good morning again. Yes, it was really amazing feedback from all OEMs from North America and big OEMs, European OEMs, OEMs in Korea, Japan, and China. I think that's clearly a game-changer with Chat Pro, but we are also going beyond Chat Pro.

Source: Q1 earnings call

company presentation

In my opinion, this widespread appeal indicates a strong likelihood of increased product adoption, which could translate into substantial revenue growth for CRNC in 2024 and beyond.

CRNC's strategic collaborations with leading technology giants like NVIDIA and Microsoft further strengthen its product outlook. These partnerships provide the company with access to cutting-edge technology and resources, allowing them to further differentiate themselves from the competition. By leveraging these advancements, CRNC can develop even more innovative and powerful solutions, solidifying its position as a leader in the automotive AI space.

KPI outlook (company presentation)

In my view, a key part of CRNC's success rate in closing the deals, aside from the product's strength, would be industry reputation. So far, I believe CRNC appears to have a strong position in that regard. CRNC currently boasts a dominant market share of 54% in the global auto software industry.

10Q

Furthermore, I believe the strong KPI outlook in Q1 could also serve as a leading indicator for revenue growth in the high-margin Connected Services/CS business. CS has both subscription and usage-based revenue models. Usage is driven by Monthly Active Users / MAU, which saw a 30% YoY increase in Q1. Meanwhile, the strong pipeline in Q1 should present an opportunity for future subscription revenue growth:

We expect a ramp in new connected services in FY '24 as several key programs that have been delayed by customers go into production. We continue to see a solid pipeline of opportunities for connected services, even as some expiring programs of old technology restrain the near-term growth.

Source: Q1 earnings call.

In my opinion, risk remains moderate. I would advise investors interested in CRNC to monitor the sales cycle and macro outlook, two potential key risks to my thesis.

Though the 200 demos and meetings during CES were encouraging, in the end, everything comes down to sales execution. I believe securing contracts with OEMs can still be a lengthy process. It involves complex negotiations and lengthy testing phases, potentially leading to extended sales cycles. This can create uncertainty regarding the timing and potential value of new contracts, impacting top-line estimates.

Due to the cyclicality, the ongoing economic headwinds today, such as elevated inflation and supply chain issues could negatively impact the automotive industry and consumer spending, indirectly affecting demand for CRNC's offerings:

Economic headwinds, a lack of charging infrastructure, and a confusing web of federal policies and regulations also threaten to slow new car sales and electric vehicle adoption. As demand softens, automakers are curbing their production plans despite an initial EV manufacturing rush.

Source: AutomotiveDive

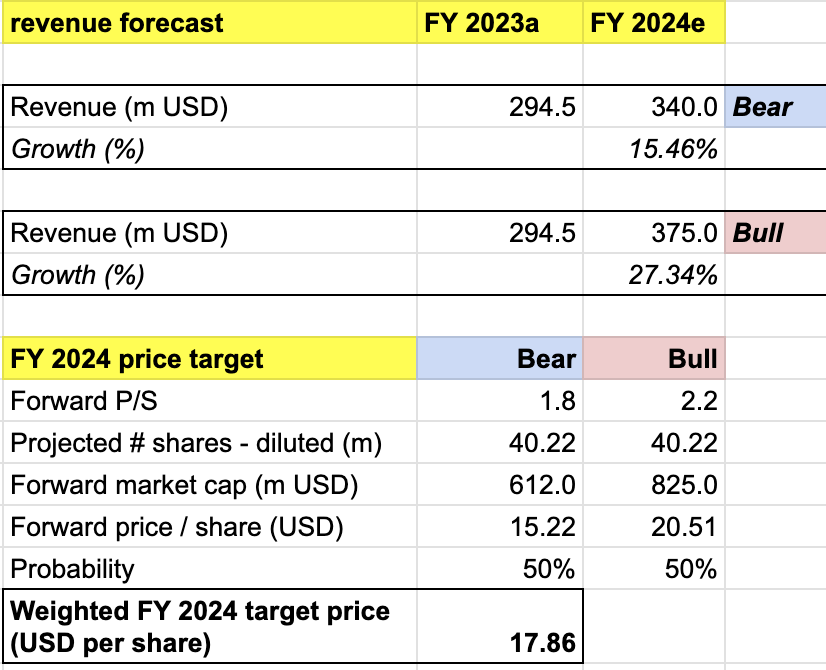

My target price for CRNC is driven by the following assumptions for the bull vs. bear scenarios of the FY 2024 projection:

Bull scenario (50% probability) assumptions - CRNC to achieve FY 2024 revenue of $375 million, a 27% growth, at the high end of the company's guidance. I assign CRNC a forward P/S of 2.2x, implying a share appreciation to $20.5, retesting its YTD high.

Bear scenario (50% probability) assumptions - CRNC to deliver FY 2024 revenue of $340 million, a 15% growth, missing the company's low end guidance by $15 million. I expect P/S to remain at 1.8x, at the current level, implying a sideways price action.

price target (own analysis)

Consolidating all the information above into my model, I arrived at an FY 2024 weighted target price of $17.86 per share, presenting a potential upside of over 20% from the current level. I give the stock a buy rating.

While potential risks exist, Cerence's foundation, strategic initiatives, and promising catalysts still suggest a decent outlook. Given their potential and current undervaluation, I initiate coverage with a buy rating and a 1-year price target of $17.86, representing an over 20% upside. Investors should watch closely as Cerence executes on its vision and capitalizes on these opportunities.