Kriangsak Koopattanakij

Kriangsak Koopattanakij

Market leadership, and more specifically growth equity leadership, has resided with the Magnificent Seven for the last year. The performance of these mega caps has led to historic levels of market concentration, obscuring a multitude of compelling businesses across the rest of the U.S. market. We recently spoke with Portfolio Manager Aram Green, who manages multi cap as well as dedicated small and mid cap growth strategies, about where he is finding attractive opportunities today.

Q: Being an early investor in disruptive technologies has been a hallmark of your approach as a growth manager. Given the attention paid to generative AI, what innovation themes are you excited about today?

Aram Green: 2023 was all about artificial intelligence. We believe every great company is becoming an AI company, similar to how a decade ago every company started embracing software and cloud computing to power their business. Today every company of size is investigating and investing in AI and that is creating new revenue drivers for the enablers of this ecosystem.

Our investments within AI have been primarily in infrastructure and software. The big infrastructure spend to develop data centers and compute power benefited portfolio companies like Nvidia (NVDA), Marvell (MRVL), nVent Electric (NVT) and Vertiv (VRT). We increased the size of those positions when generative AI started to take off but have started to de-emphasize AI infrastructure in favor of software companies building applications.

While we expect spending on infrastructure to continue, the rate of growth will moderate. Infrastructure is a one-time purchase as we transition from CPU-based computing to GPU-based servers. Software, on the other hand, is an annuity stream, as these businesses generally collect revenues under subscription-based agreements with very high renewal rates. These software companies are building applications and using data and analytics with AI to drive new, recurring and highly profitable revenue streams. We have been leaning into those companies, whether they be on the application side like ServiceNow (NOW), GitLab (GTLB) or HubSpot (HUBS), or on the information security side protecting that data, such as CrowdStrike (CRWD)or Varonis (VRNS).

In addition, we own companies like an Airbnb (ABNB) and Accenture (ACN), who have been early adopters of AI into the fabric of their companies, which should allow them to deliver more competitive offerings to their customers and drive efficiency through their cost structure. Over the long term, this should produce larger companies, with wider moats and scale, generating higher levels of cash.

Q: Up-and-coming health care companies are also a meaningful part of your portfolios. Where are you currently positioned in the sector?

Aram Green: Within health care we are finding opportunity in drug and therapy development. Our preference is to invest in the services and technology providers empowering drug discovery and commercialization, rather than take binary risk in early-stage biotechnology, compound-based companies. We are gaining this exposure through contract research organization ICON (ICLR), clinical and lab services provider Charles River Laboratories (CRL) as well as Doximity (DOCS), a cloud-based collaboration platform for medical professionals.

We have also found enablers that facilitate care and services to patients such as HealthEquity (HQY), a provider of health savings and similar services to manage medical costs, and Surgery Partners (SGRY), whose outpatient surgery centers offer a lower-cost setting for outpatient care that provides a better experience for patients and doctors.

Q: Beyond these higher-growth companies, where else in the market are you finding ideas?

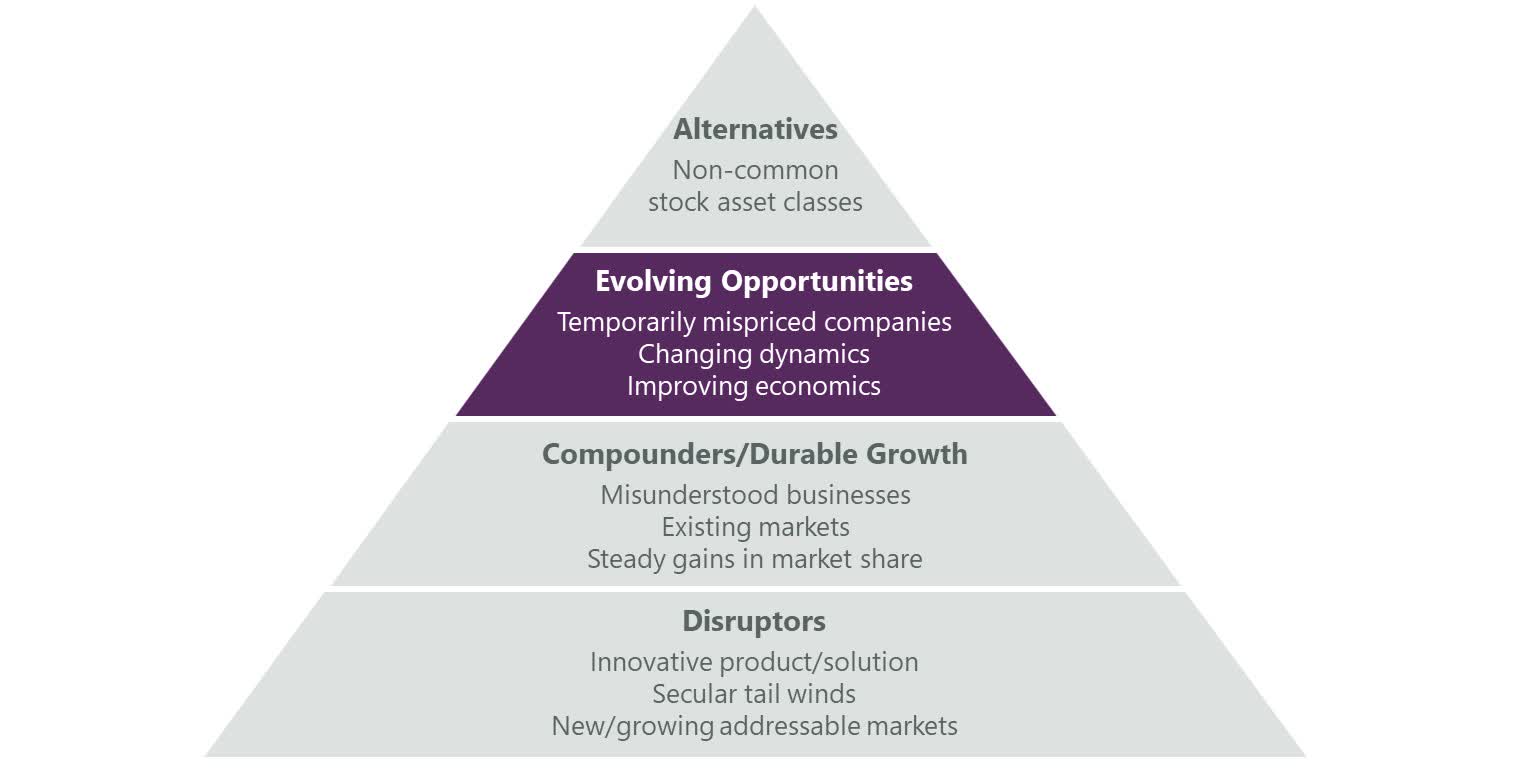

Aram Green: Companies we call "evolving opportunities" reflect more of the contrarian side of our active approach. These investments tend to be good companies that have run into difficulty for a range of reasons, including failed acquisitions, poor capital decisions and/or increased debt burden. We conduct our analysis, de-risking the stock to ensure the problems have peaked, and outlining positive catalysts that are expected to increase the key performance indicators of the business, whether it is revenue growth, profitability, free cash flow or higher-returning capital deployment, usually in the form of share repurchase and debt reduction.

Exhibit 1: Evolving Opportunities Tap Overlooked Catalysts

Pyramid of Growth Companies (ClearBridge Investments)

With the starting point for this type of investment being a compressed valuation, we view these evolving opportunities as coiled springs: as each one of their company-specific catalysts unfolds, that should lead to better reported results and merit a higher multiple from investors. We can drive performance with little downside risk in this area of the portfolio, given valuations are so washed out at the time of purchase.

We are disciplined in managing our evolving opportunity exposure. The best outcome is for a business to evolve into a durable compounder that can be held longer term. A good example is Performance Food Group (PFGC), which distributes food to corporate cafeterias, movie theaters and restaurants. The company made an acquisition right before COVID but due to restaurants closures, fundamentals were temporarily depressed and the multiple compressed with it. By engaging with management, we realized they were leaning into hiring salespeople and taking market share, winning new customers ahead of the rebound in food service.

When our thesis for owning an evolving opportunity plays out and we see limited upside ahead, we take our profits and move on to the next opportunity. This was the case with American Eagle Outfitters (AEO), which saw a rerating from a successful transition to e-commerce and new apparel lines. In cases where our thesis does not play out or the cost of waiting for catalysts to take hold is too great, we will quickly exit the position as we did when new management at Kering could not reinvigorate its flagship Gucci brand.

Q: Tighter financial conditions and higher costs of capital have caused investors to hunker down and crowd into mega caps for safety. How does a stable-to-easing interest rate environment support smaller stocks?

Aram Green: We should see greater conviction in corporate spending as the rate environment stabilizes. When management teams have clarity with respect to their cost of capital they are able to invest in new capital programs, increase product development and hire additional resources needed to fuel growth. During the current earnings season, for the first time in almost two years, we are starting to see the spending spigot open up again. Companies are re-activating growth initiatives put on hold when the macro environment was more uncertain and they were not sure what the cost of capital would be for those projects.

Furthermore, that stability is spurring confidence in the probability of a soft-landing scenario in the broader economy. These altering dynamics are positive for risk assets, and we have started inching into smaller cap stocks and those companies that have the ability to put more capital into their business to grow at faster rates.

Q: Any other tailwinds from a more predictable macro backdrop?

Aram Green: Another area that we're paying attention to is the return of M&A. When interest rates are volatile, management teams and company boards can't be certain about their borrowing costs to go out and make acquisitions. With steadier interest rates, executives can plug those financing costs into their models to determine whether a deal will be economically sound.

This year we have seen M&A activity in biotech as well as sizable consolidation deals within the energy space. We think that is going to continue and that increased activity will be at higher valuations than we have seen the last few years. A stable rate environment gives buyers higher conviction in the multiples paid for assets. This is especially true for growth stocks where a lot of the value is in the future and needs to be discounted back to present value.

Q: What about the new issue market: how are current conditions becoming more conducive for IPOs?

Aram Green: With the Fed persistently on their front foot in rapidly raising interest rates to cool inflation, IPO activity seized up in 2022 and continued through the first half of 2023. That led to a wide spread between what management teams thought their company was worth compared to the multiples investors were willing to pay. That delta as well as heightened economic uncertainty froze the market for new issues. We are now starting to see that thaw.

We had several companies go public in September and October, including Klaviyo (KVYO), one of the private investments we made several years ago. In addition, we have been very active in meeting with private companies on the path to go public. There is a tremendous amount of innovation out there, and we expect to see a number of those companies come to market as we move through the balance of the year. We are doing our homework now to be prepared for those actionable investment opportunities.

Aram Green is a Managing Director and Portfolio Manager at ClearBridge Investments.