bjdlzx

bjdlzx

Crescent Energy (NYSE:CRGY) beat a lot of consensus forecasts with the current earnings report. At first, the market was pointing to things like hedging gains and other things that are not really valued. But coming right behind that is some solid operational gains mentioned in the conference call. The only thing the operational gains need is enough new wells for those effects to become material to the quarterly reporting. Since the unconventional business has a sharp first year decline rate, that materiality should climb rather quickly to become apparent to shareholders.

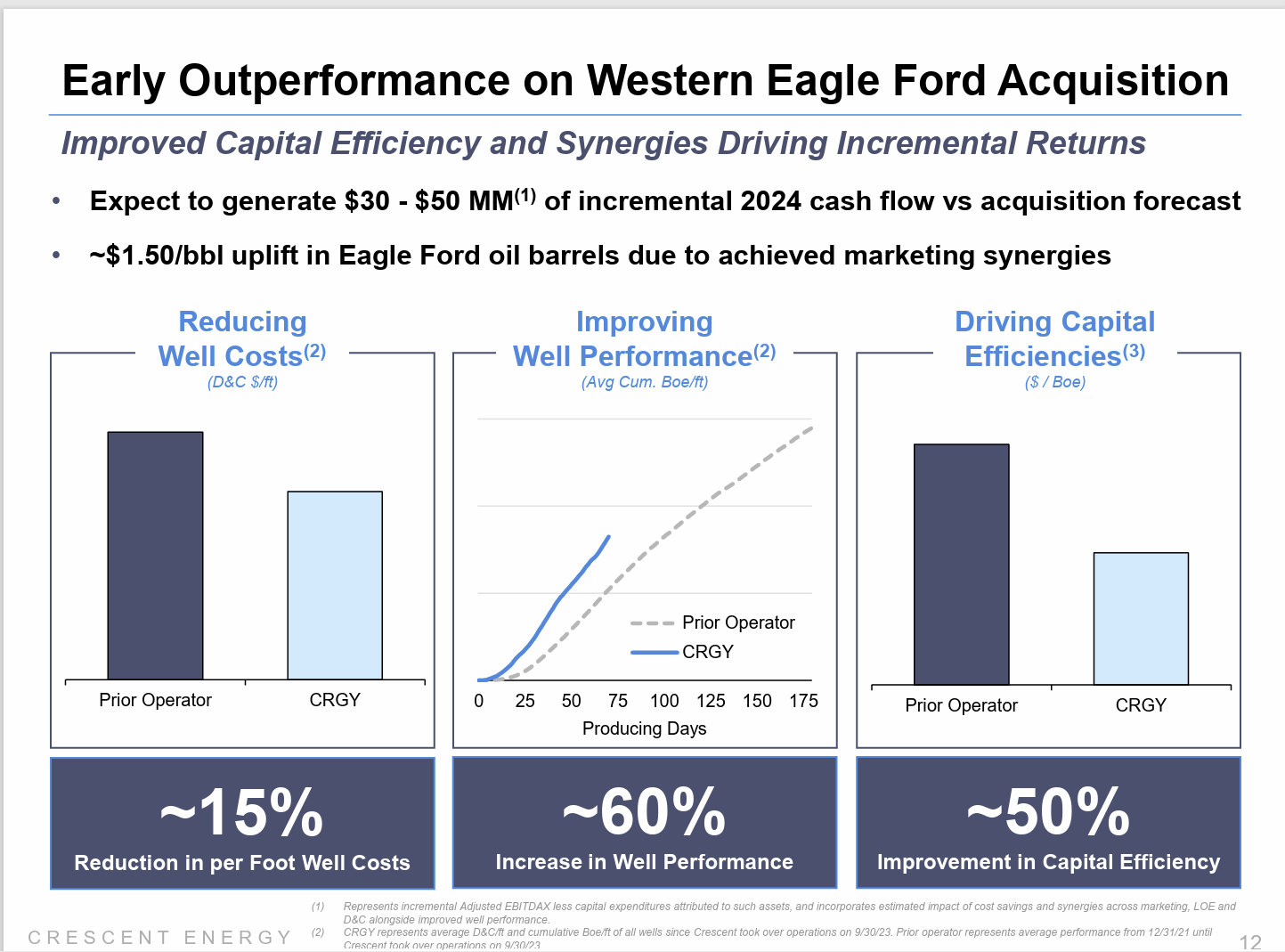

Management acquired some Eagle Ford properties in the 2023 fiscal year. That transformed a previously non-operated situation in a material core operated play, according to the CEO in the conference call. Mr. Market would, of course, demand to see reported improvements that justify something like that.

"In fact, our team is generating significantly better performance from all wells brought online since we took over operations in September. While still early in our efforts, we are seeing a 60% increase in well performance to-date with 15% lower costs across the program, which represents a massive shift in capital efficiency on the assets."

This quote from David Rockecharlie, CEO and Board Member, begins to be specific about the improvements made now that the company operates a significant amount of the Eagle Ford properties.

The question I always get is "why is this not in the quarterly report numbers?". The answer is that the improvements are probably not materially significant just yet. But progress like what is mentioned above should drive down the average costs that make the financial reports over time.

Crescent Energy Eagle Ford Operational And Cost Improvement Summaries (Crescent Energy Earnings Conference Call Slides Fourth Quarter 2024)

Sure enough, when the conference call slides are reviewed, management states that there should be a material addition to free cash flow as shown above in the current fiscal year.

That incremental performance can be a challenge for investors to observe with varying commodity prices and hedging. But over time, the profitability should outperform as something like this becomes very material to the company's overall reporting.

The Eagle Ford is a core area. Therefore, lower costs (to hopefully something approaching lowest costs) should become apparent. Every saving is important in that it increases company profitability (and cash flow when commodity prices are weak). But not all savings will be apparent from the quarterly reports or even the management presentations.

An aside would be that the market generally discounts any productive area where management does not control the operations. The situation here switched to management control in addition to acquisitions. Therefore, Mr. Market will likely be reviewing the track record on the way to a revaluation. This takes time, but it does appear that management is off to a good start.

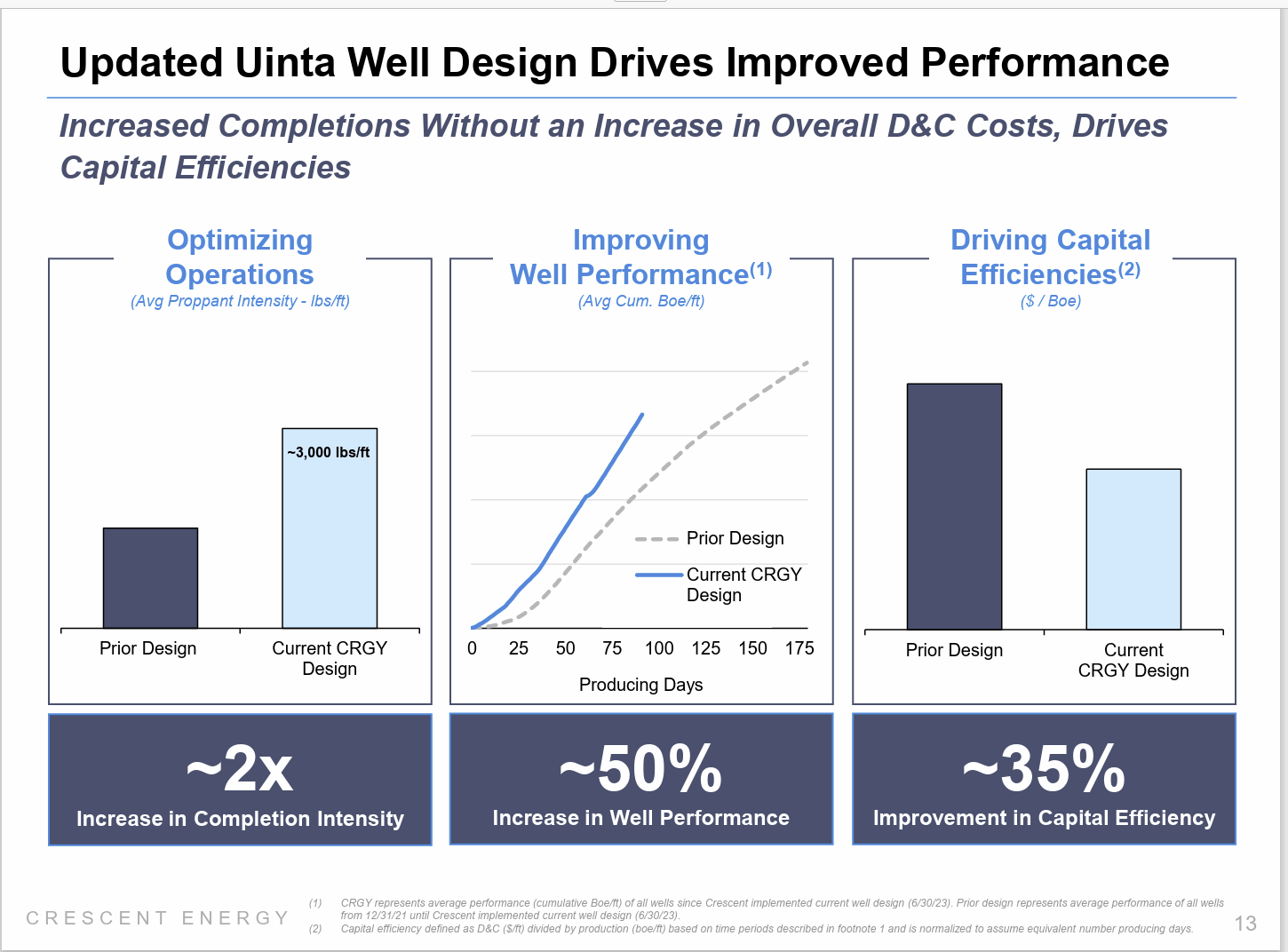

The Uinta appears to be successfully making that transition to a free cash flow generator from what I remember in the "good old days". This is true of a lot of basins. One of the market's big complaints was companies showing profits, but the sharp decline rates meant that all the cash was used (at the time) for replacing the production decline plus growth. The Uinta was a star performer that way in the good old days. But now that basin appears to becoming far more profitable.

Crescent Energy Uinta Operational Improvements And Cost Declines (Crescent Energy Corporate Earnings Presentation Fourth Quarter 2023)

Like the Eagle Ford, this cost progress should eventually lead to declining operational costs as more wells come online. Continuing technology advances should lead to more improvements over time.

The only question is if the cost improvements will exceed inflation enough for investors to see in the quarterly reports, or if it will keep cost increases below the rate of inflation.

Either way, the company's competitive position should improve over time. That should lead to a profitability increase and a better market valuation for the stock. Timing about something like this is always uncertain. So, patience is needed.

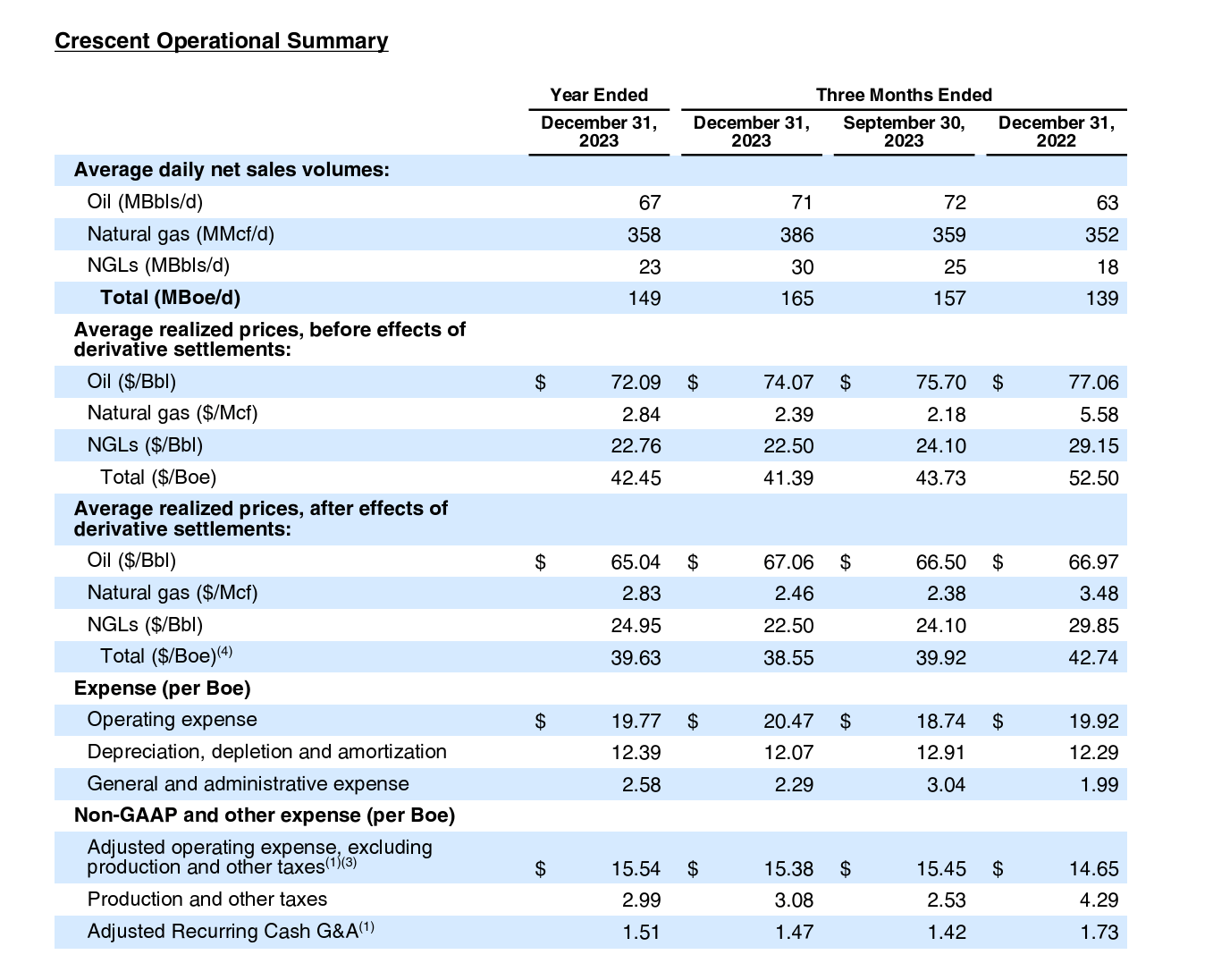

This management has been purchasing properties from "unnatural owners" as in probably distressed buyers. Therefore, high operating costs are very likely with the acquired properties. But depreciation could be below average due to the distressed cost of the properties.

Crescent Energy Fourth Quarter 2023, Earnings Summary (Crescent Energy Earnings Press Release Fourth Quarter 2023)

Depreciation and amortization is running on the low side as shown above. This is despite the fact that this company has purchased older production for the lower decline rate and cash flow. The company is not breaking out costs by area. But that overall figure confirms there are a few bargains in the company portfolio.

On the other hand, operating expense is on the high side. But if the buyer obtains a good enough purchase price, then high operating costs are acceptable. Naturally, management will be doing just what was reviewed above to bring down cost breakeven points in preparation for the next cyclical downturn. The point is that there is a good chance that overall costs are reasonable enough if the acquired properties initially have high operating costs. Basically, management goes for a good deal and then improves that deal through better operating practices and technology improvements or advances.

The other thing to note is that analysts appear to have underestimated the effect of the hedging program. When we get to the income statement, there is likely a large commodity hedging loss in fiscal year 2022 to account for the fact that commodity prices held steady. The hedging program is doing its job of minimizing earnings volatility. This is at least partially why there was an earnings beat compared to analysts' consensus.

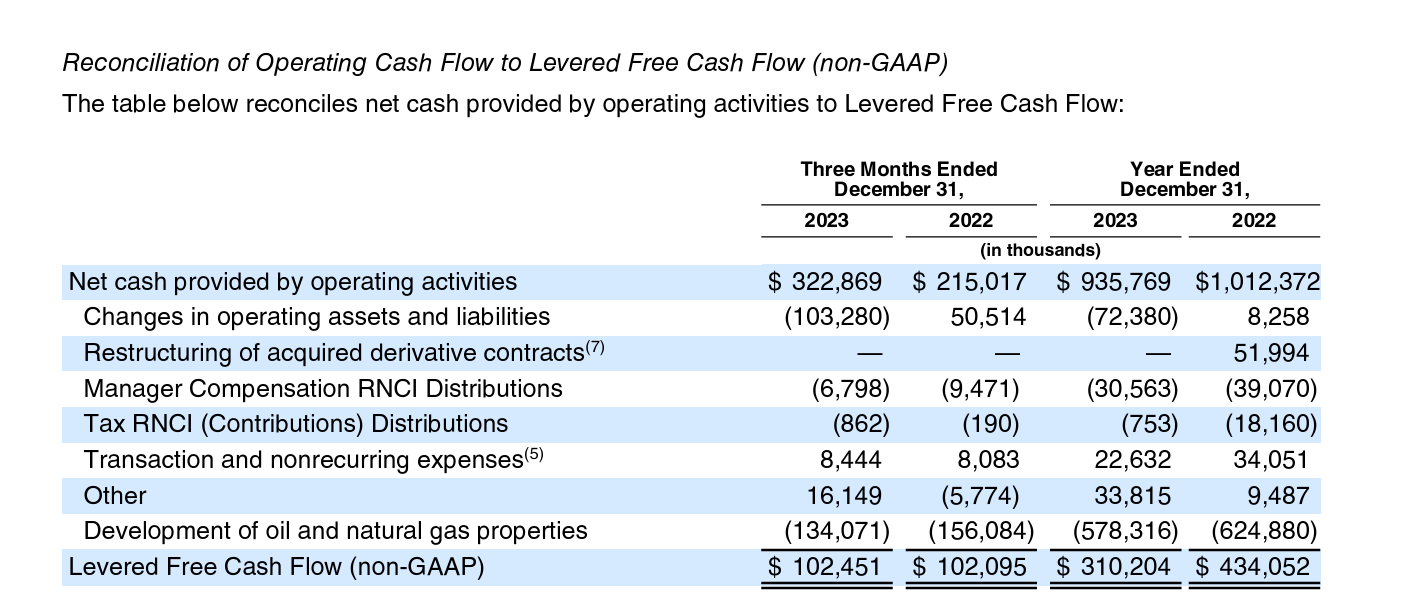

The main entities behind this company are known to be cash flow centered.

Crescent Energy Summary Of Free Cash Flow Calculation (Crescent Energy Earnings Press Release Fourth Quarter 2023)

The first thing to note is that the declining prices meant that less working capital was needed. Therefore, the current fiscal year received a boost (despite the acquisitions) from declining oil and gas prices compared to fiscal year 2022.

Even taking that into account, the hedging program helped the cash flow and free cash flow hold up rather well. The latest acquisitions should make a few quarterly comparisons "a slam dunk" on the positive side in the current fiscal year.

A solid, profit oriented, growth program based upon finding bargains helps to offset the volatility of oil and gas when a hedging program is used. The outperformance shown above is an example of what can happen. It is just one more strategy to help "smooth" the growth so investors and the market can tell what is going on (and the benefits of that growth). There is never a guarantee though that it will always work.

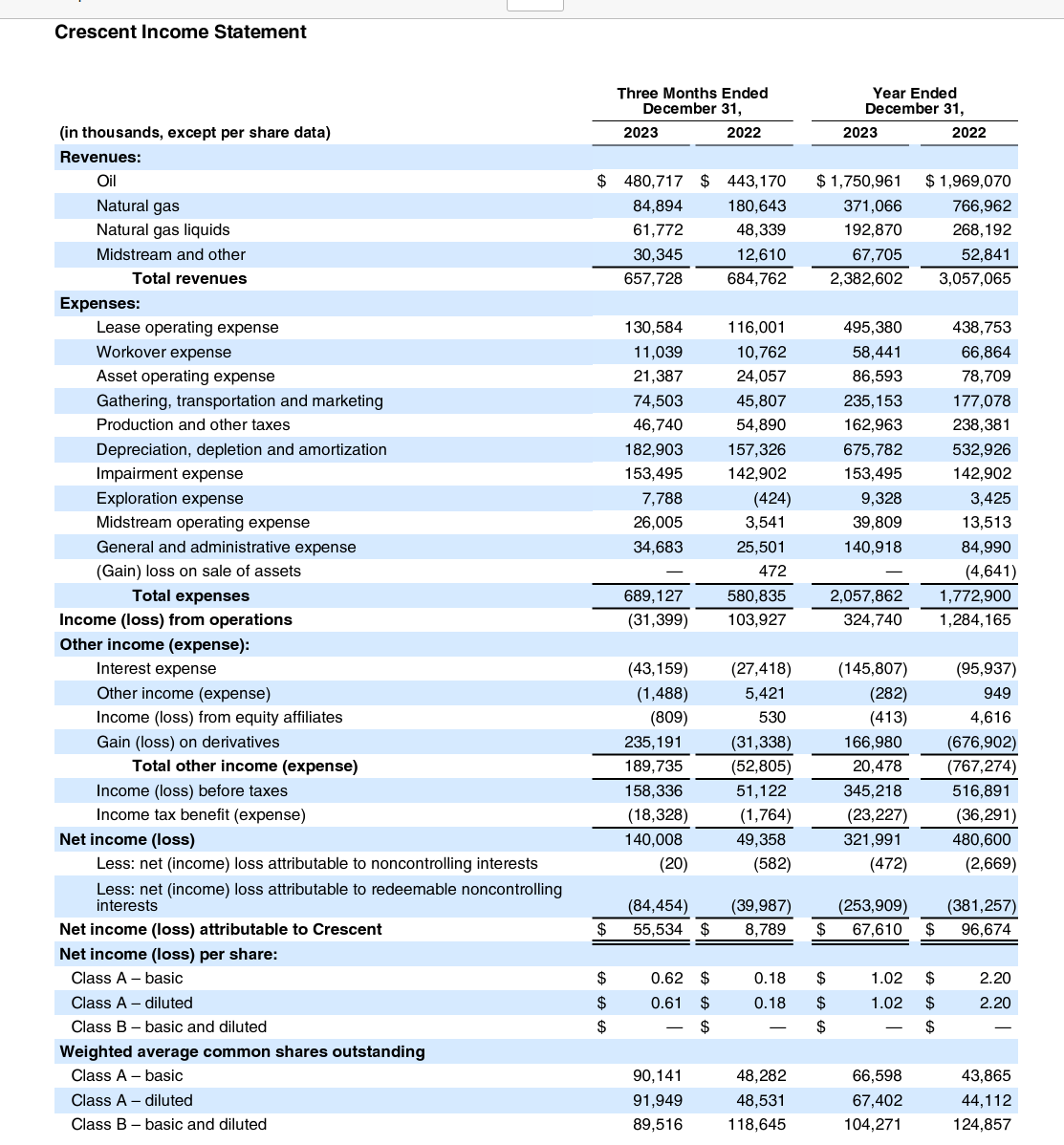

The income statement has a few nonrecurring items that can distract from the operational progress underway.

Crescent Energy Income Statement Fourth Quarter 2023 (Crescent Energy Fourth Quarter 2023 Earnings Press Release)

What seems to have made the earnings difference is the gain this fiscal year on hedging derivatives (which is non-cash) that exceeds the impairment charge (which is also non-cash). It is for this reason that I follow the cash flow statement a whole lot more because for me "cash is king".

The operational income really does not show the benefits of the cost reduction moves (and that should have been expected). It actually corresponds closely to the per barrel amounts (and their effects on income) shown before. That can be a problem for the market because the market wants financial results "yesterday" and not from things like hedging and impairment.

Cash flow is likely in for a big jump, not only because of the cost savings and operational improvements, but also because the Eagle Ford properties are in a low-cost area and those acquisitions significantly enlarged the company's production.

Generally, lenders allow a pre-acquisition summary of results to be part of the EBITDA calculation. Any improvements will enlarge EBITDA at any commodity price level to lower the debt ratio before any debt paybacks or production growth is considered.

The main reason for the earnings beat at the current time has a lot to do with non-repeating events in the eyes of Mr. Market. But this management has programs underway to make that improvement a repeating event from better operating results.

This idea remains a strong buy, as rarely do investors get to publicly invest alongside KKR and John Goff. The public float has increased considerably in the current fiscal year. Therefore, periodic conversions to public shares should have far less effect on the stock price than in the past. Management has also instituted a share repurchase policy that will work against the effects of additional stock becoming publicly traded shares.

The financial strength remains well within acceptable. There is a goal to achieve investor grade. That will also help the stock price long-term. This idea is not a traditional upstream idea. But growth through acquisition is becoming very acceptable to the market right now. I like management's chances of having considerable success at raising the stock price over time.