Jacob Wackerhausen/iStock via Getty Images

Jacob Wackerhausen/iStock via Getty Images

Credo Technology (NASDAQ:CRDO) is a company providing high-speed connectivity solutions, such as integrated circuits / ICs, Active Electrical Cables / AECs, and Serializer and Deserializaer / SerDes Chiplets.

Share performance has been relatively strong since going public in 2022 at the price of $11 per share. Despite the demand shock from a major customer in 2023 that caused the stock to reach an all-time low of $8, CRDO has had a strong rebound since. Over the past year alone, return stands at 126%.

I initiate my coverage with a neutral rating. My 1-year price target of $24 presents a merely 4% upside from $23 today.

YCharts

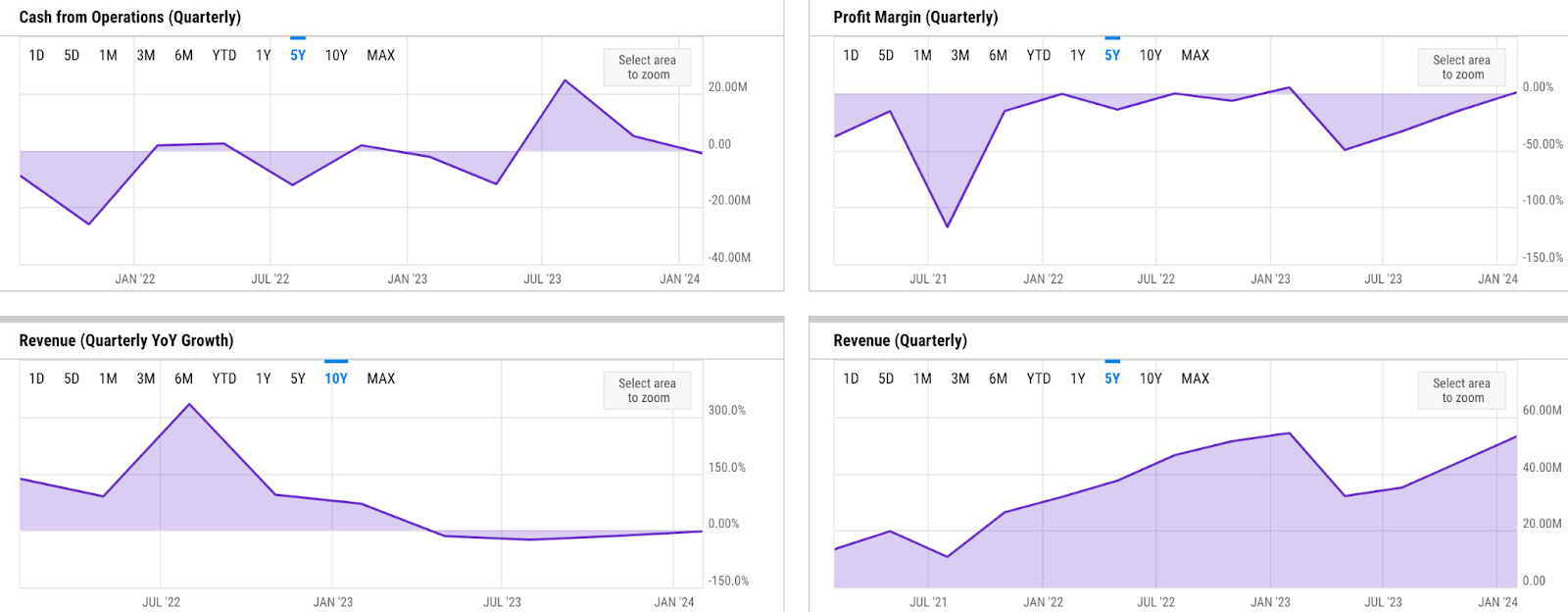

Fundamentals are mixed. Revenue growth has been choppy, with CRDO seeing quarterly revenue growth in recent times. In its latest quarter, Q3 2024, CRDO delivered a revenue of $53 million, a -2.2% YoY growth. GAAP net profitability has also gradually improved since reaching the -49.6% net loss margin in April 2023. Overall, CRDO did not really have a strong performance for most of 2023. It pretty much saw a double-digit net loss margin for almost every quarter, including in April.

Operating cash flow / OCF generation has been inconsistent. In Q3 2024, CRDO saw an OCF loss of -$1 million, despite having generated over $5 million of OCF the prior quarter.

YCharts

CRDO has maintained a relatively solid and steady liquidity position around $200 million - $240 million with no debt. In Q3, 2024, CRDO even raised an additional $174.6 million to bolster its liquidity. As a result, CRDO finished Q3 2024 with a liquidity of over $409 million, up by 70% from the prior quarter.

As a business that primarily provides high-speed connectivity solutions for data centers, I believe CRDO is benefitting from the secular growth opportunities in increasing AI adoptions. The opportunities are manifested in the increasing demand from the hyperscale data center developers ("hyperscalers") such as Microsoft, Amazon, or Google, to deliver high-performance computing / HPC capabilities to enable AI applications.

Based on the management's comment in the Q3 2024 earnings call, US hyperscalers play a key role in driving CRDO's business. So far, I believe CRDO has seen positive developments in advancing the collaborations with the five US hyperscaler customers, primarily within the AEC business. In my opinion, these positive developments provide better pipeline visibility for CRDO, which is an indicator of future revenue growth:

We expect U.S. hyperscalers to remain the majority portion of AEC demand in the foreseeable future. Many of these customers have distinct architectural requirements that demand innovation and tight collaboration between the engineering teams at Credo and the customer. We're engaged at different stages with the five U.S. hyperscalers as well as other global hyperscalers and Tier 2 data center operators.

Source: Q3 earnings call.

10Q

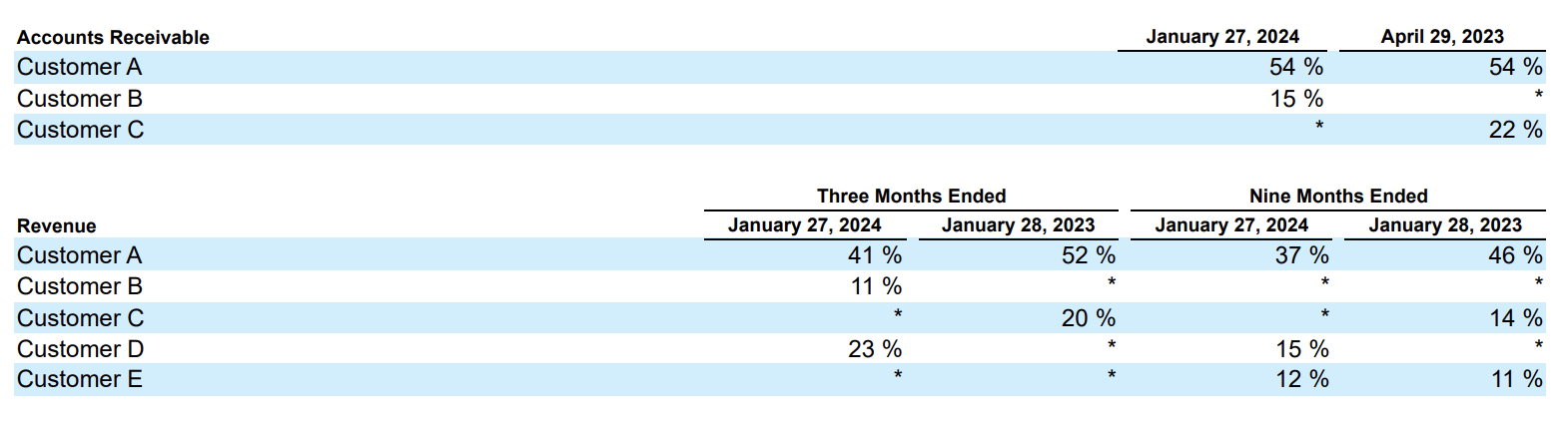

Stronger uptake of AEC solutions could also potentially drive meaningful growth in overall business, in my view. Though CRDO does not break down its revenue by product lines, AEC seems to make up a considerable share in Product sales revenue, the biggest revenue stream for CRDO. Product sales made up over 78% of revenue in the nine months ending January 2024, while the decline in AEC demand in the same period also resulted in 11.4% decline in Product sales, which demonstrates AEC's meaningful share in the revenue stream.

I believe CRDO is well-positioned to capture the opportunities, due to its leading reputation in AEC business. Following Microsoft, which is the first CRDO's hyperscaler customer implementing AEC solution, CRDO continues to attract more hyperscaler customers with its leading AEC solutions as of Q3:

But to give you color on what they were, the largest customer was our first AEC hyperscale customer that we've talked about. They came in at 28%, and that's followed by a lead chiplet customer, much of which was NRE driven at 23%. And then the final of the top three, which you'll be able to figure out who that is based on the warrant was our second AEC hyperscaler customer at 19%. So, two of the top three then would be AEC driven, the other being chiplet driven. So there's going to be variability in that as we go. Last quarter was a bit interesting and unique in that the top four customers all represented different - four different product lines.

Source: Q3 earnings call.

Moreover, given that CRDO is already working with hyperscalers outside the US and with lower-tier data centers as of Q3, I believe there is a future growth opportunity for CRDO beyond its core US hyperscalers customer segment.

CRDO's large revenue concentration within a small number of customers remains a major risk. For instance, as discussed earlier in the catalyst section, the lower AEC demand in January 2024, which resulted in 11% YoY decline in Product Sales revenue, actually came from just one large customer.

10Q

Though CRDO seems to have diversified its customer base a bit more as of January 2024, I believe it would take some time before CRDO could acquire more customers and reduce its concentration risk further due to the potentially long sales cycle.

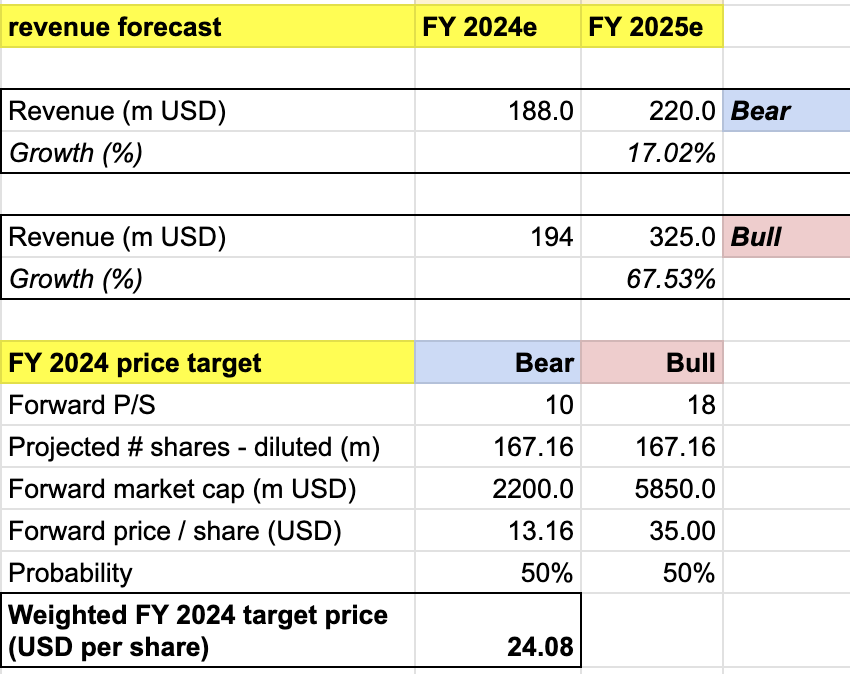

My target price for CRDO is driven by the following assumptions for the bull vs bear scenarios of the FY 2025 (FY ending in January 2025) projection:

Bull scenario (50% probability) assumptions - CRDO to achieve FY 2025 revenue of $325 million, a 67.5% growth, at the high end of the market's estimate. I assign CRDO a forward P/S of 18x, which implies a share appreciation to $35. In this scenario, I would expect CRDO to start realizing significant revenue from converting its hyperscalers-driven sales pipeline.

Bear scenario (50% probability) assumptions - CRDO to deliver FY 2025 revenue of $220 million, a 17% growth YoY. CRDO would miss the low-end range of the market's estimate, effectively resulting in a correction to $13. In this scenario, I would expect CRDO to see either a reduced demand from one of its major customers or a longer-than-expected sales cycle that would negatively impact FY 2025 revenue.

own analysis

Consolidating all the information above into my model, I arrived at an FY 2024 weighted target price of $24 per share, presenting a potential upside of merely a 4% from the current level. At this point, I would give the stock a neutral rating.

In my view, despite the attractive secular trends and promising progress in the discussions with the hyperscaler customers as of Q3, CRDO's revenue concentration still presents a major risk factor. This is the reason why I assign my price target model a 50-50 bull-bear probability. However, I conclude that CRDO could be an interesting long-term opportunity, and I would advise interested investors to monitor CRDO's progress in the next few quarters before dipping in.

CRDO is benefitting from the growing demand in HPC in the data center industry, mostly driven by the increase in broader AI adoptions. Its leading position in AEC solutions has put it in a good position to attract the most valuable potential customers in the data center industry, the "hyperscalers", which include the likes of Microsoft, Amazon, or Google. However, the high revenue concentration within a small number of large customers presents a major risk. As seen last year, a potential demand shock from any of its customers into the FY could pressure share performance considerably. My 1-year price target of $24 accounted for such risk. At a projected upside of merely 4%, it suggests that CRDO appears close to being fully valued. I rate the stock neutral.