Fertnig

Fertnig

My recommendation for Cricut Inc. (NASDAQ:CRCT) is a sell rating as I expect FY24 to continue seeing poor performance, which will cause the valuation to rerate back to 18x forward earnings. Note that I previously rated a hold rating for CRCT as the business continued to see very strong headwinds that made it impossible to model the stock's near-term performance.

The situation with CRCT appears to be a lot worse than I expected. In the 4Q23 quarter, CRCT reported revenue of $232 million, which was below consensus expectations by ~7% and was an 18% decline vs. 4Q22. Although the gross margin came in stronger than expected, reporting $41.96 million vs. the consensus expectation of $34.5 million, operating expenses went up by 19% to $80.5 million, resulting in a disappointing EPS performance of $0.05 vs. the consensus expectation of $0.058. Most importantly, the headwinds that were pressuring the business continue to persist, and hence, I am downgrading my rating to a sell.

On headwinds, there were no signs of a turnaround at all. CRCT continues to see lower user engagement, where the percentage of engaged users in the trailing 90 days reached a 4Q low of 44%. Relative to 4Q22, it is down a full 700 bps and is now near all-time lows. Although some bullish investors might say that this could be the bottom since it is near all-time lows, I think it is a delusion because the cause of the decline was, I believe, mostly the weak consumer spending environment and cautious retailer activity. Looking at how the inflation rate has trended in the past few months, I am not very confident that the Fed will be cutting rates in 2H24, which could cause consumers to spend more. If inflation trends up for the next few reports, my view is that the Feds are going to delay their plan to cut rates.

By the way, I am not the only one who has this negative viewpoint on consumer spending, as management themselves are guiding for 1Q24 revenue to decline on an annual basis, again, which would mark the 9th consecutive quarter of annual declines. The important part of the guide is that there is potential for revenue to see an annual decline on a full-year basis. Remember, they gave this guide just 16 days ago, so we can be pretty sure that 1Q24 revenue is going to see a decline as 4 weeks in 1Q24 (March) is unlikely to move the needle. While there was an uptick in consumer demand during Valentine's Day (largely due to promotion), I continue to expect the challenging demand trends from past quarters to persist in 2024 as there are no strong visible signs of a turnaround. I mean, even if the Fed does cut rates, the impact on consumer spending is not going to be immediate anyway, as consumers and retailers will stay cautious for a while; hence, I think FY24 is going to be another very weak year.

Lastly, what I thought was a key support for valuation and share price was the CRCT capital return policy to shareholders. Sadly, that is going away as well. The change in focus regarding capital allocation was the hint that got me to think about this. The new capital allocation priorities are first to make sure CRCT has adequate inventory to operate the business, followed by investing for growth, followed by M&A. There was no direct message to state that share buybacks and dividends would continue. In my opinion, in FY24, management is likely to focus on reinvestments in the business to position CRCT for growth, and there are unlikely to be any capital returns to shareholders. Note that over the past year, management returned $314 million to shareholders via share buybacks and dividends, and with the purchase of $10.8 million of shares in 1Q24, they have basically used up the remaining buyback authorization.

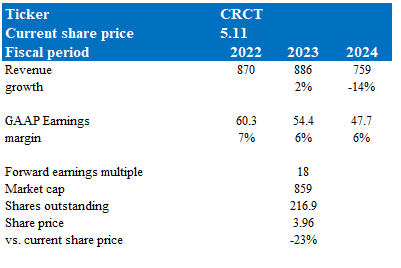

Author's valuation model

According to my model, CRCT is valued at $3.96, representing a 23% downside. Given the very poor performance since 4Q23, which has continued into 1Q24 and is expected to continue for the rest of the year, I have turned much more pessimistic about the business. Moreover, the reduced focus on capital returns to shareholders meant that there would be no support for the share price through CRCT share repurchases. From the way I see it, there is no apparent improvement in the business or outlook; as such, I don't see a reason for valuation to trade up to the current 21x forward earnings. My sense is that there is a portion of the market that is bullish because of a potential rate cut in 2H24 that will spur on demand, and as I have stated above, the impact is unlikely to be immediate. My view is that as CRCT continues to show poor performance, the valuation multiple will gradually trend back down to 18x, which is the low end of the CRCT trading range and where the stock traded just a few weeks ago.

If, contrary to what I expect, the board actually launches a strong share repurchase program, it could lead to a strong share price reaction in the near term. Also, if the Fed turns more bullish on the economy, cutting rates by more than expected, the consumer demand environment might turn positive faster than expected, which could drive up demand for CRCT.

Summarizing this post, the recommendation for CRCT is a sell as the business continues to see persistent headwinds, which led to a poor FY24 guidance. All operating metrics continue to point to a weak business performance: Revenue missed expectations by 7% in 4Q23, marking an 18% decline vs 4Q22; user engagement remains near all-time lows, indicating weak consumer spending; and management noted a potential revenue decline for FY24. The lack of capital return to support the stock price is also a negative point to me as CRCT is prioritizing reinvestment over shareholder returns. In my opinion, weak performance ahead will lead to multiple contraction back to 18x forward earnings.