Chip Somodevilla/Getty Images News

Chip Somodevilla/Getty Images News

The S&P 500's (SP500) relentless breakout started after the index bottomed on October 27, 2023. Fed pundits interpreted Fed Chair Powell's rate pause at the time as a sign the central bank would cut interest rates. In January, the Fed indicated that although inflation persisted, it would not cut rates. January's hot inflation alert failed to incite stock market selling, either.

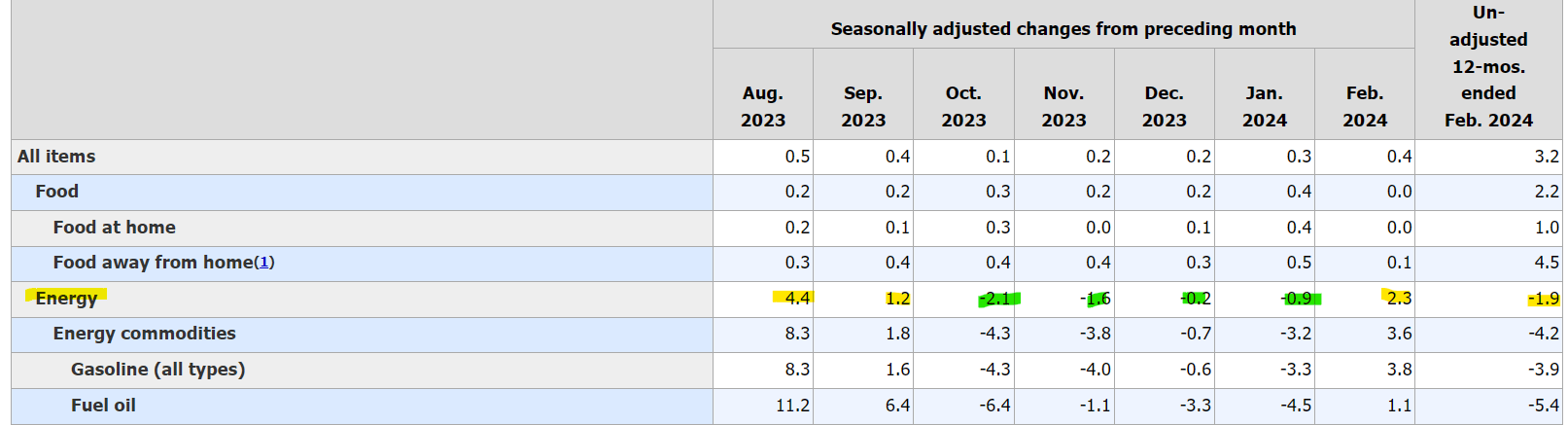

Nearly six months later, markets remained calm despite more of the same inflation rates in February. The Consumer Price Index for the all items index increased by 3.2% before seasonal adjustments. At face value, when inflation is 1.2% above the Fed's 2.0% target, should it not raise interest rates by 25 bps?

Unless the Fed anticipates the Bureau of Labor Statistics to report a sharp increase in inflation rates next month, the Fed is unlikely to hike rates after this week's meeting. It removed the rate hike option months ago. In the last FOMC statement from two months ago, the Federal Reserve said "the Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent."

The FOMC removed the sentence of the Committee anticipating "that some additional policy firming may be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time."

One line item that threatens the market is energy prices. West Texas Intermediate crude prices recently strengthened. Before that, the CPI reports benefited from weak energy prices.

In February, the energy index rose 2.3% over the month. Over the year, it decreased by 1.9%.

bls

As Spring approaches and the travel season returns, the energy sector requires increased output to avoid prices from rising from here.

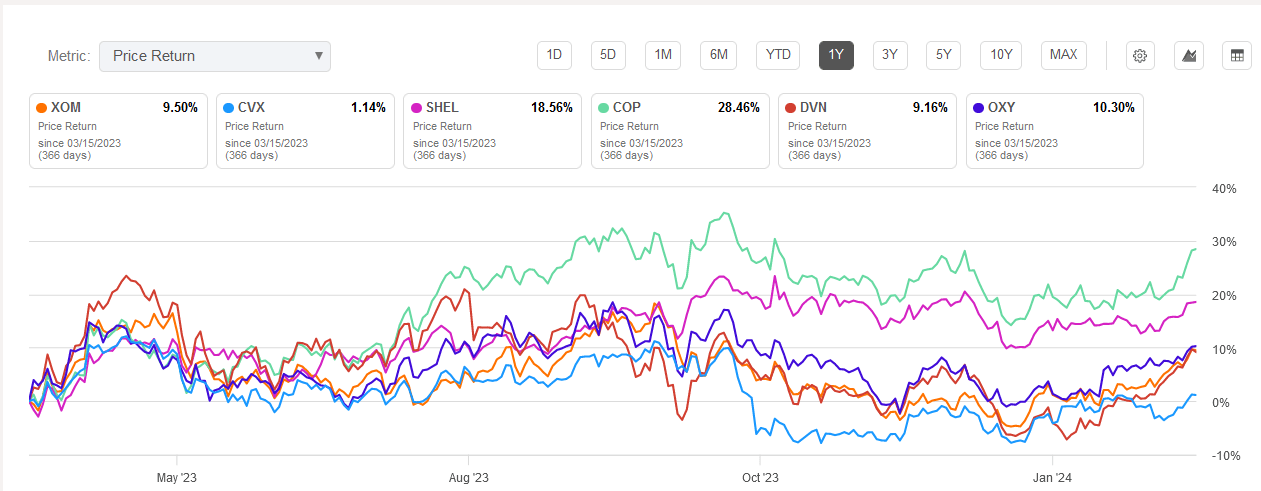

Investors may run a comparison of energy stocks to consider buying. In the last year, ConocoPhillips (COP) performed the best, followed by Shell plc (SHEL). Occidental Petroleum (OXY), which has a short float of 5.9%, is up by 10%. Exxon Mobil (XOM) and Devon Energy (DVN) trail OXY stock.

Seeking Alpha

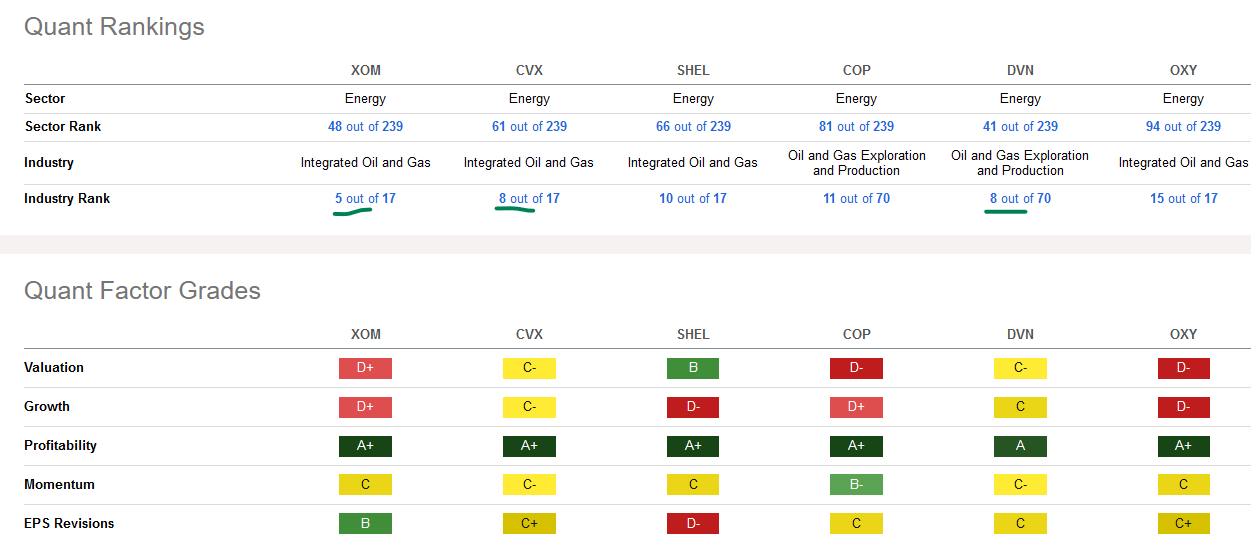

Chevron (CVX) is the worst performer, up by only 1.14% in the last year. In addition to the quant factor grades, the industry rank would help readers choose which energy stocks to buy.

Seeking Alpha

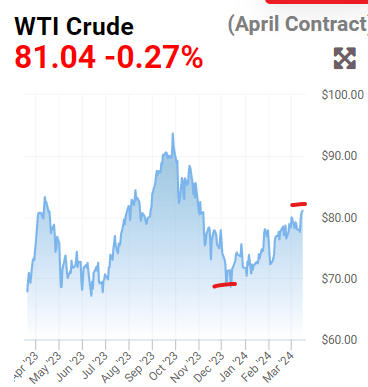

Oil prices crossed above $80 for the first time since last November 2023. Markets, led by tech firms selling artificial intelligence tools, traded higher along with WTI crude prices.

oil price

Risks are mounting that higher input costs would hurt high-flying AI stocks. Watch Super Micro Computer (SMCI) and Nvidia (NVDA) as the proverbial canary in the coal mine. If their stock price weakens, it would undermine the AI stock rally. Markets may flip and buy energy stocks in their place.

Instead of dismissing them as an AI bubble, readers are encouraged to monitor AI stock valuations against their upcoming new products and their revenue potential. For example, Nvidia's CEO will host GTC 2024 from March 17-21, 2024.

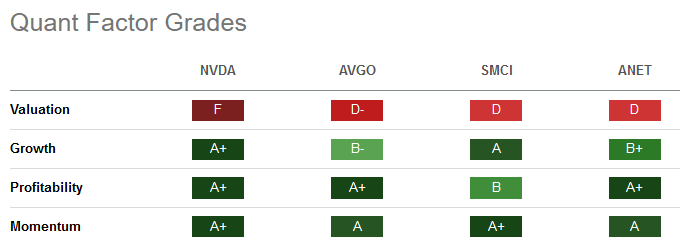

Nvidia and Broadcom (AVGO) have a quant rating of "Hold."

Seeking Alpha

Super Computer and Arista (ANET) have a "Strong Buy" rating.

All AI stocks mentioned score an A or higher on momentum:

Seeking Alpha

A rate hike this week is remote. Besides, the Fed has little control over energy prices. Conversely, it should have more influence on the housing market. Its interest rate policy has an impact on mortgage rates.

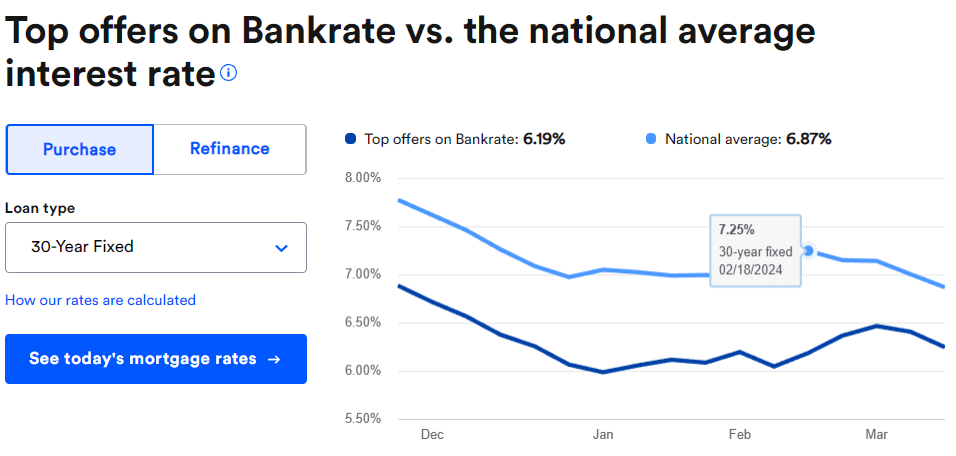

According to Bankrate, mortgage rates started climbing up until Feb. 18, 2024. The national average rate pulled back to close at 6.87% as of March 16, 2024.

bankrate

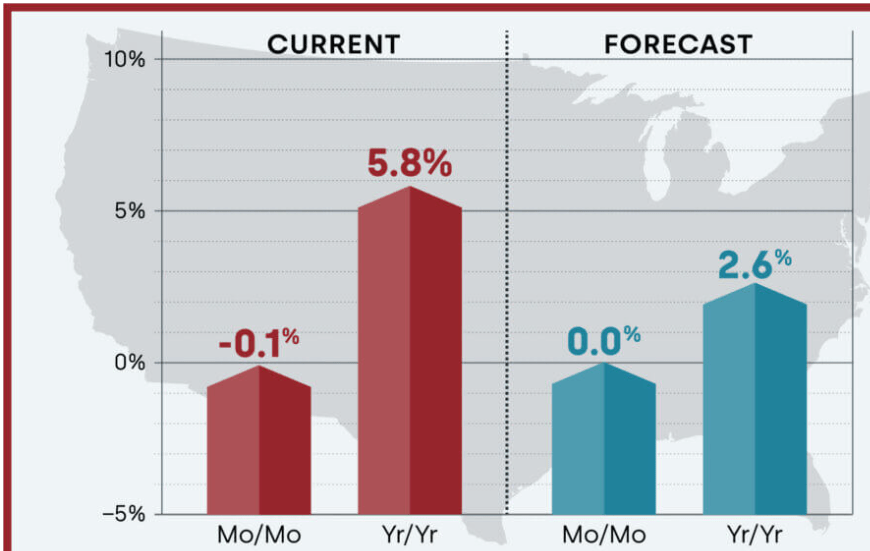

CoreLogic forecasts home prices unchanged from Jan. 2024 to Feb. 2024. It will increase by 2.6% Y/Y from Jan. 2024 to Jan. 2025.

CoreLogic

In its willingness to wait for its monetary policy to work into the economy, the Fed will look for the balance between supply and demand. In the Fed minutes, participants credited the recent expansion in economic activity to the increase in supply. Although the pace of job hiring slowed compared to last year, non-farm payrolls are still strong.

Readers should scrutinize the Fed's claim of a strong job market. In February's job report, the BLS revised December's nonfarm payroll employment report. The 333,000 figure falls to 290,000. In January, the NFP revised the report down by 124,000. The figure falls from 353,000 to 229,000.

The two revisions resulted in the December and January combined employment being 167,000 less than the officially reported figures.

In the February report, readers skeptical about its strength may look at the government employment figure. It increased by 52,000. This is consistent with the prior 12-month average growth of 53,000. Education accounted for 26,000 jobs while the federal government added 9,000 jobs.

Circling back to the Fed minutes, the Committee expects a demand-supply equilibrium in product and labor markets. The economy owes a better balance to the policy restraint in place. The Central Bank may achieve the hard-to-achieve soft landing, which meets the Fed's employment and inflation goals.

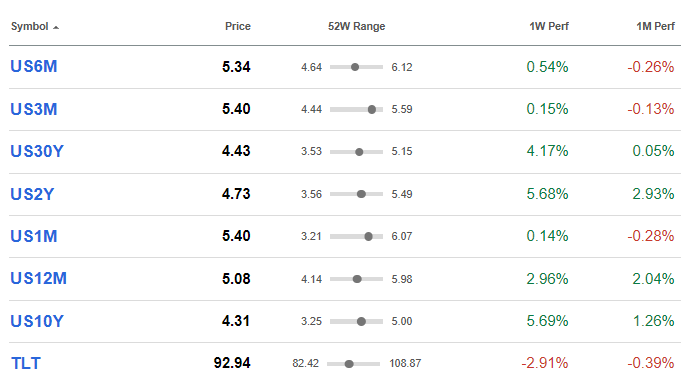

The hot job and February inflation report issued this month suggests an interest rate cut of 25 bps is highly unlikely. In the last week, the bond market priced in its low likelihood. The 2-year Treasury Bond (US2Y) and the 10-year (US10Y) staged the most pronounced yield increase. In the last week, their yields rose by 5.68% and 5.69%, respectively.

Seeking Alpha

Past readers who commented on buying the 20+ Year Treasury Bond (TLT) aggressively last year are underwater. Until the Fed has firm economic data indicating a drop in inflation, higher rates for longer would send TLT stock lower from here.

The small-cap ETF, iShares Russell 2000 (IWM) is a good leading indicator for stocks. It traded in a narrow range at between $202 - $205. It will not break out as small business owners pass higher input costs to their customers.

Last Thursday, March 14, the BLS posted the Producer Price Index rose by 0.6% in February. It increased by 1.6% in the last year. This is the biggest increase since rising by 1.8% in Sept. 2023. Recall that stock markets started their rally a month later. The latest PPI report suggests that inflation will persist in the months ahead. Most notably, the index for final demand energy increased by 4.4%.

Investors should hedge inflationary risks by holding energy stocks. In addition, the Fed will keep interest rates at the same level. This reaffirms the attractiveness of short-term Treasury bonds, including the iShares 0-3 Month (SGOV).

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.