Alistair Berg/DigitalVision via Getty Images

Alistair Berg/DigitalVision via Getty Images

This article was coproduced with Leo Nelissen.

As some of my longer-term followers may know, I have a background in supply chains. My Master's degree had a focus on purchasing and supply chain management, which has guided me very well in my investing journey.

I believe that buying companies that are critical in major supply chains is one of the best methods to build long-term wealth.

Personally, I'm invested in oil drillers, midstream companies, healthcare suppliers, railroads, agricultural companies, financial service providers, and many others that are key in the markets they serve.

Essentially, I try to buy companies that are so important that if they were to vanish overnight, it would be a catastrophe.

Having said that, one of the most important supply chains is the food supply chain. After all, we all have to eat!

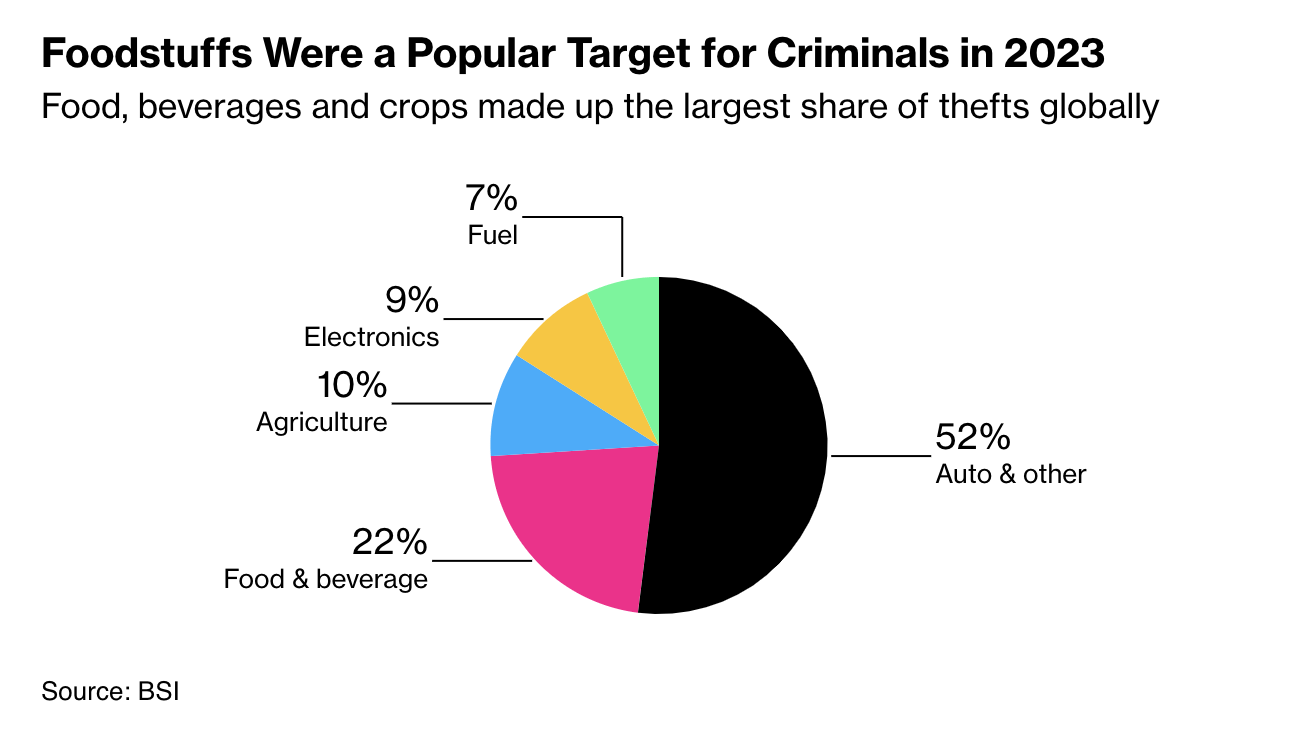

What's interesting is that this supply chain is increasingly targeted by thieves, likely due to elevated food inflation after the pandemic.

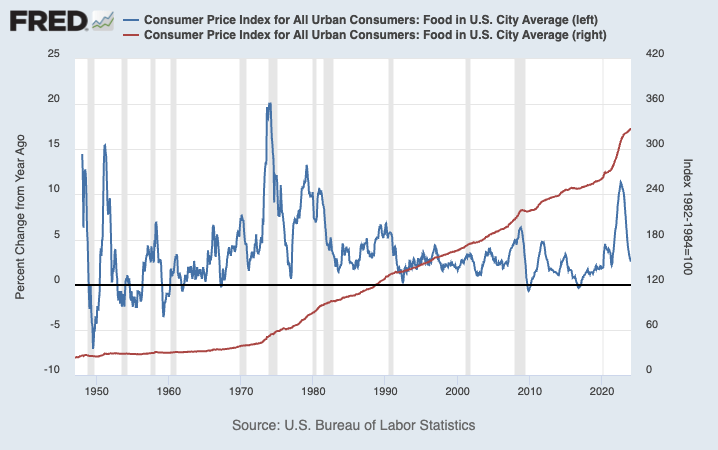

The chart below shows the Consumer Price Index for food in the United States. As we can see, after 2020, we witnessed the biggest increase since the 1970s.

Federal Reserve Bank of St. Louis

Hence, last month, Bloomberg reported that food theft is becoming an increasingly serious issue, noting that the theft of foods and beverages now accounts for more than a fifth of all incidents.

In 2021, the share of food and beverages in thefts was just 14%.

Combining agriculture and food, we see that this entire segment accounts for roughly a third of global theft.

Bloomberg

Based on this context, I looked into the food supply chain and found three companies that I like as long-term investments.

These companies are Canadian Pacific Kansas City (CP), also known as CPKC, cold storage giant Americold (COLD), and food producer Conagra Brands (CAG).

Leo Nelissen

Officially, CPKC has business ties with COLD, and COLD has ties with CAG. I did not find a direct relationship between CAG and CPKC, although I have enough findings to make the case that it is highly likely that a not insignificant part of CAG products is shipped by CPKC.

Either way, the main focus here is on making money in different stages of one of the most important supply chains in the world: food.

So, let's start with stock number one: the producer.

Conagra Brands is one of the cheapest consumer defensive stocks on my radar. After all, it is a victim of the post-pandemic inflation surge, as consumers have cut back on certain food items or switched to generic alternatives.

On a side note, this perfectly shows that even defensive consumer stocks are not always immune to challenging economic times!

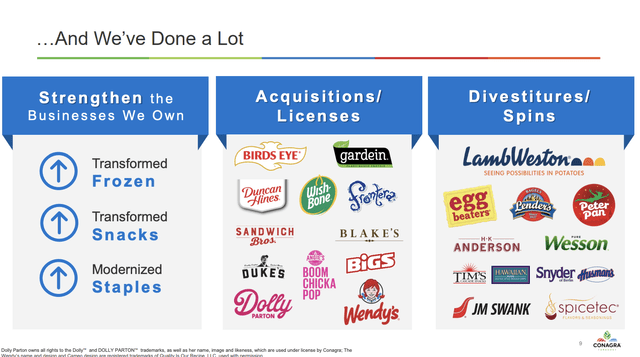

Conagra is a giant. It is currently the largest producer of frozen food in the United States. 80% of its products are either market leaders or number two in the segments they serve. This is the result of a major transformation in recent years, which came with both new M&A and divestitures.

Conagra Brands

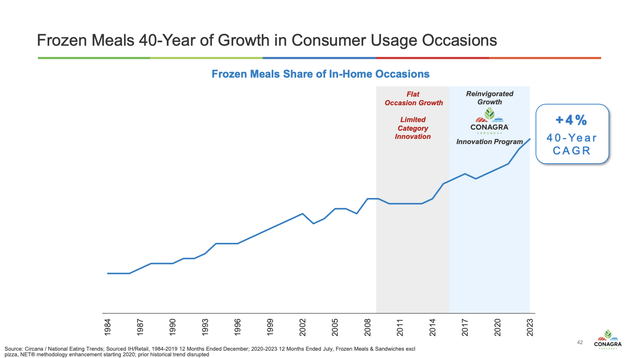

The company's "Innovation Program" has allowed it to return to market share growth, which has supported the company for many decades, with a brief period of stagnation after the Great Financial Crisis.

Conagra Brands

Unfortunately, recent economic challenges have put tremendous pressure on consumers, as we briefly discussed in the first part of this article.

In 2Q24, for example, the company reported an organic net sales decline of 3.4%. Roughly 2.9 points of this were caused by lower volumes. Even price/mix was a headwind.

"At a macro level, the industry-wide shift in U.S. consumer behavior that we discussed on last quarter's call persisted into the second quarter. These behavior shifts continued to pressure the volume and mix. However, while the consumer is still deploying some value-seeking tactics when they shop, we are seeing clear progress when it comes to volume recovery". - CAG 2Q24 Earnings Call

The good news, on top of that the company is seeing a potential recovery in volumes, is that free cash flow growth and debt reduction are on track.

In the first half of 2024, the company generated more than $640 million in free cash flow, more than 6x what it generated in the prior year period. It also lowered net debt to 3.6x EBITDA. It has an investment-grade balance sheet with a BBB- rating.

Even better, it has a dividend yield of 5%, which comes with a 54% 2024E payout ratio.

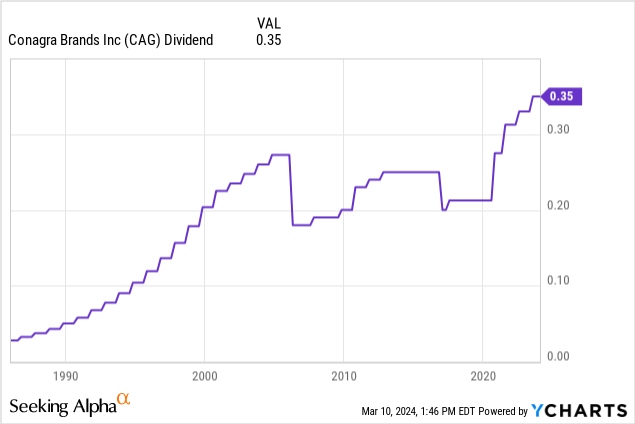

The five-year dividend CAGR is 10.1%, which is very high for a company with a well-protected high-yield dividend.

Please note that the company has not cut its dividend. The declines in the chart below display spinoffs.

Seeking Alpha

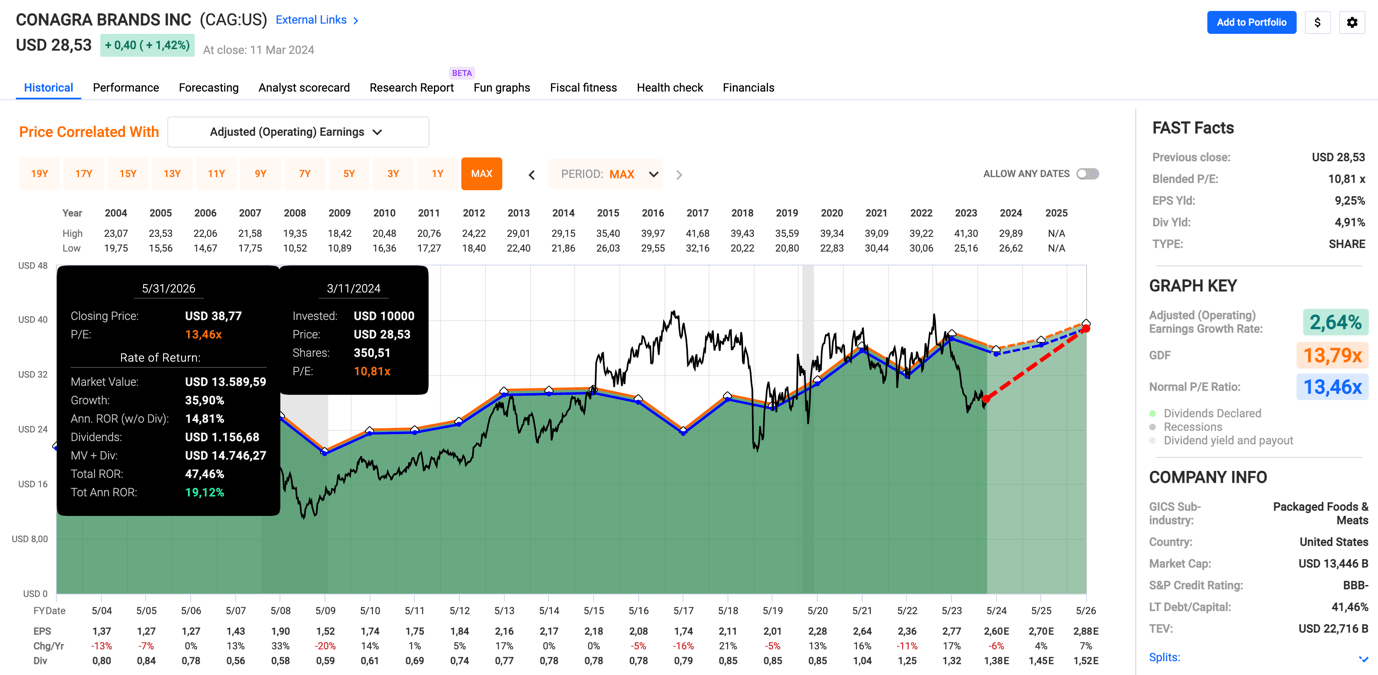

Moreover, while 2024 is expected to remain a challenging year with organic net sales contraction of up to 2% (according to company guidance), analysts are upbeat about the company's future, which makes for an attractive valuation.

The company currently trades at a blended P/E ratio of 10.8x. This is below its long-term normalized multiple of 13.5x. While analysts expect this year's EPS to decline by 6%, they foresee 4% growth in 2025 and 7% growth in 2026.

FAST Graphs

While a recovery may take time (especially if inflation remains sticky), I believe the stock has room to run to $39, which is roughly 37% above the current price.

Given the company's attractive valuation, elevated yield, and solid business, I consider this to be a fantastic recovery play in the food supply chain.

Conagra shines in the frozen foods segment. In order to operate in that segment, cold storage is needed.

That's where Americold comes in.

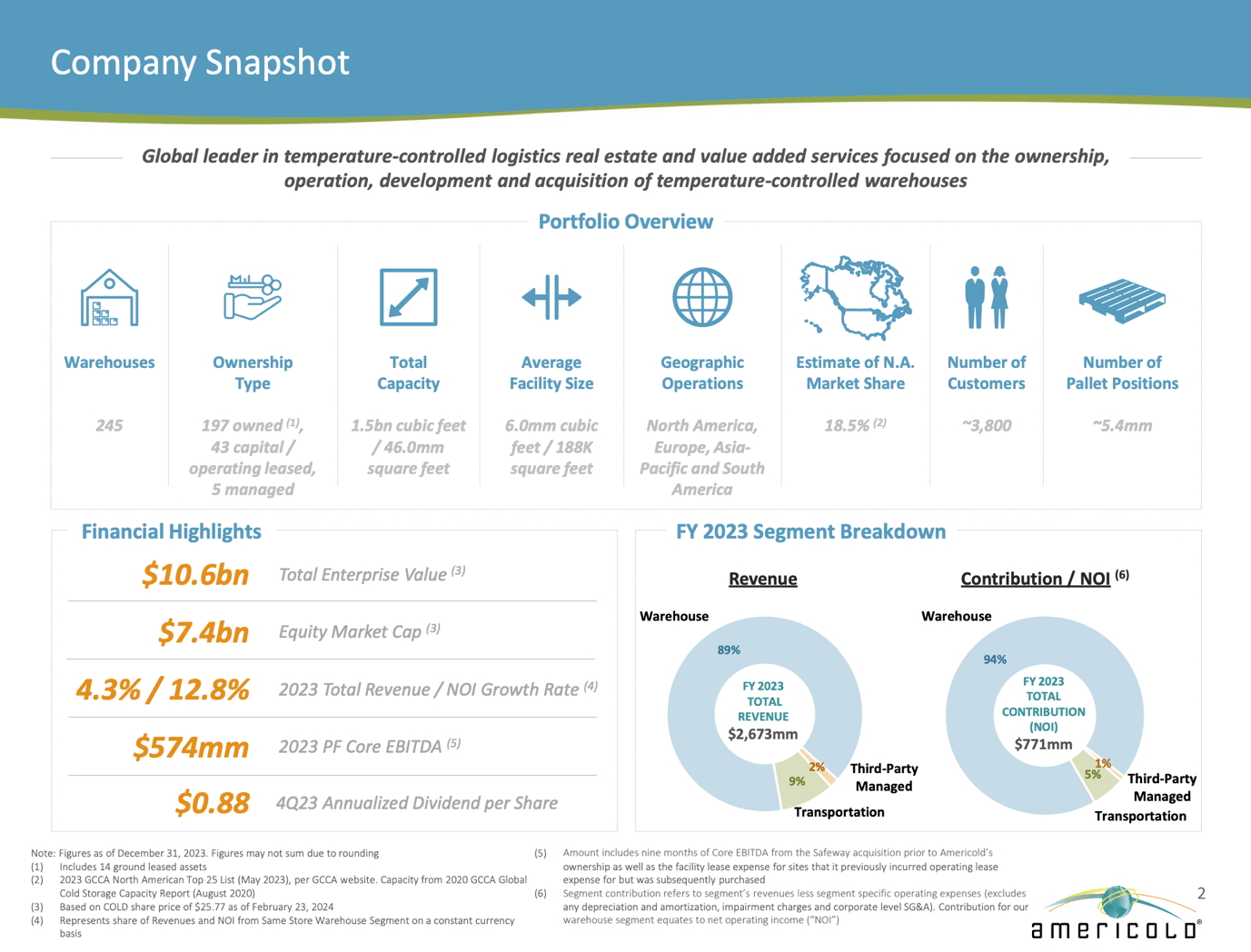

Americold is the global leader in temperature-controlled logistics real estate, operating 245 warehouses with an 18.5% market share in North America.

Americold

While neither Americold nor Conagra mentions each other in their 10-K forms, we can assume the two have been working together for a long time (not that it matters for this article, but still), as they have been involved in a lawsuit due to a warehouse fire.

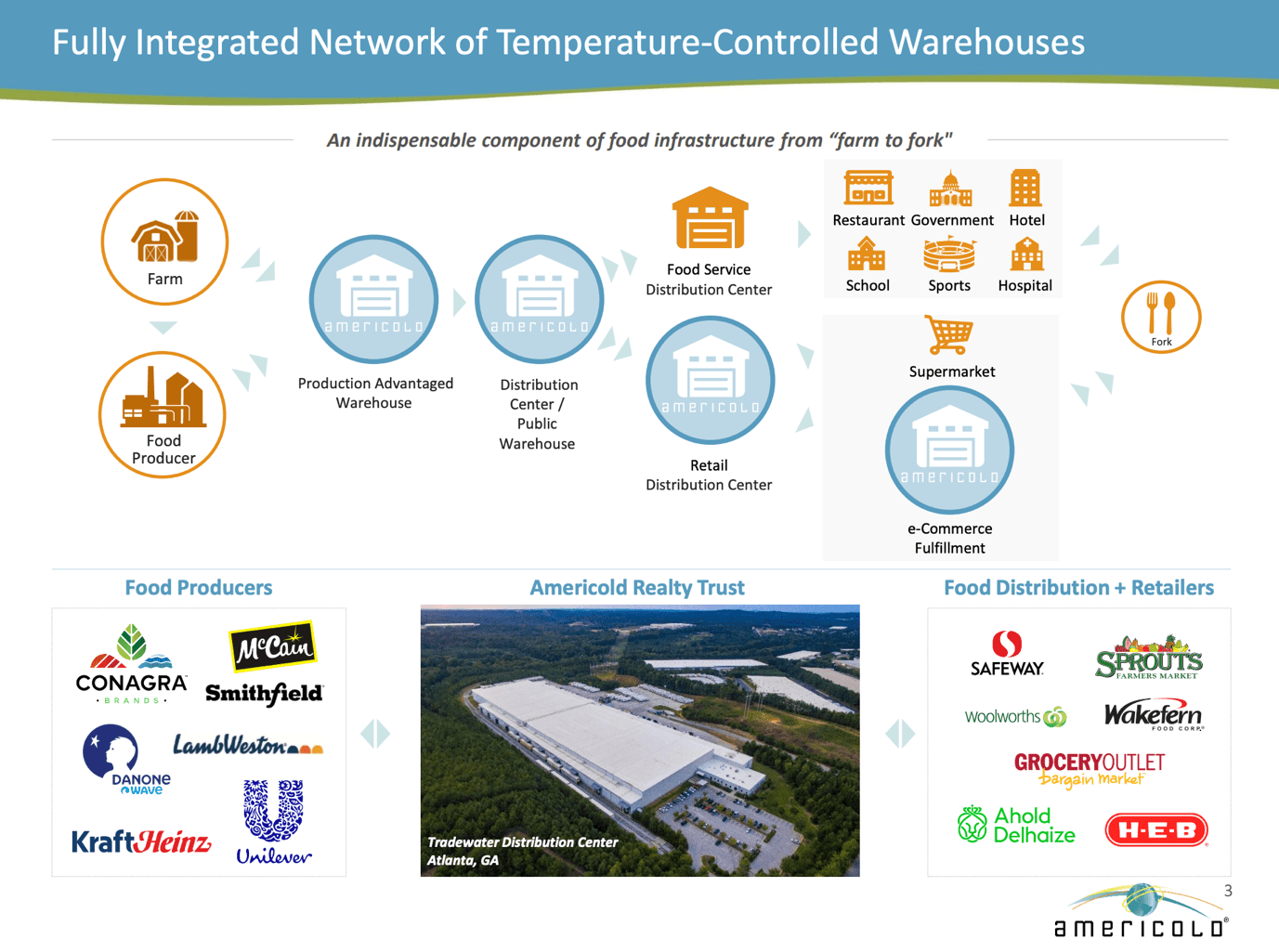

With that said, while Conagra isn't mentioned in Americold's 10-K, it is mentioned in its investor presentation as one of the major food producers it serves. The company also works with other giants, including meat processors, diversified producers, and distributors like Safeway.

Americold

In other words, as we discussed in the first part of this article, the company is a major player in the global food supply chain.

After all, 27 of its warehouses are in Europe, 19 are located in APAC nations, and two are in South America.

This business model comes with stability. Everybody needs to eat, regardless of GDP growth.

While higher economic growth is favorable for consumption, it's a highly anti-cyclical business model that comes with safety, as its average top-25 customer has been with the company for roughly 37 years!

No less than 15 of these customers have an investment-grade balance sheet. 100% of its facilities are occupied. Because cold storage assets are so expensive, the company does not build facilities without having long-term commitments from tenants. This also lowers risks.

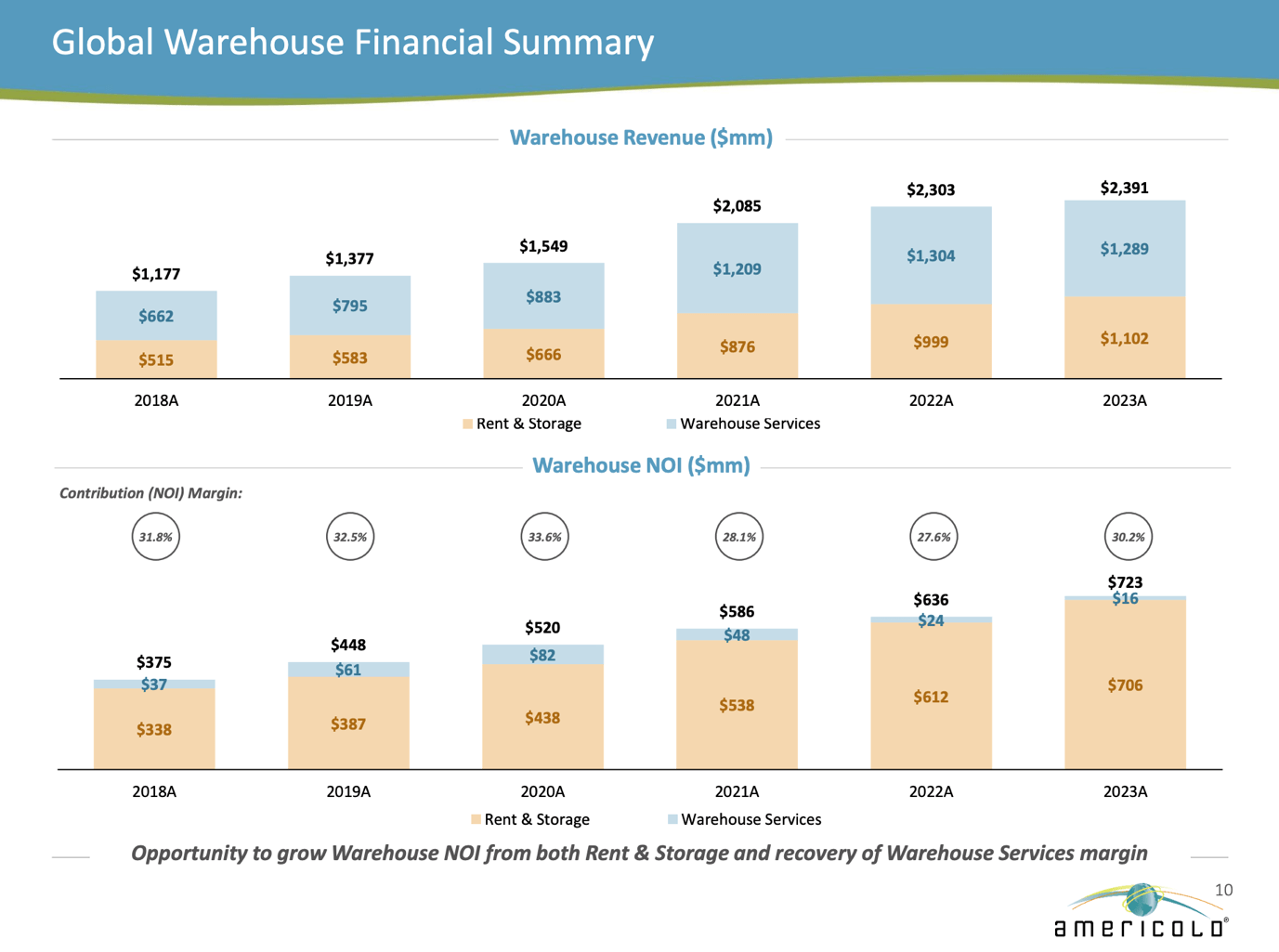

It also comes with growth. As we can see below, the company has grown its warehouse revenue from $1.2 billion in 2018 to $2.4 billion in 2023. Roughly half of this comes from warehouse services.

Net operating income has risen from $375 million to $723 million during this period.

Americold

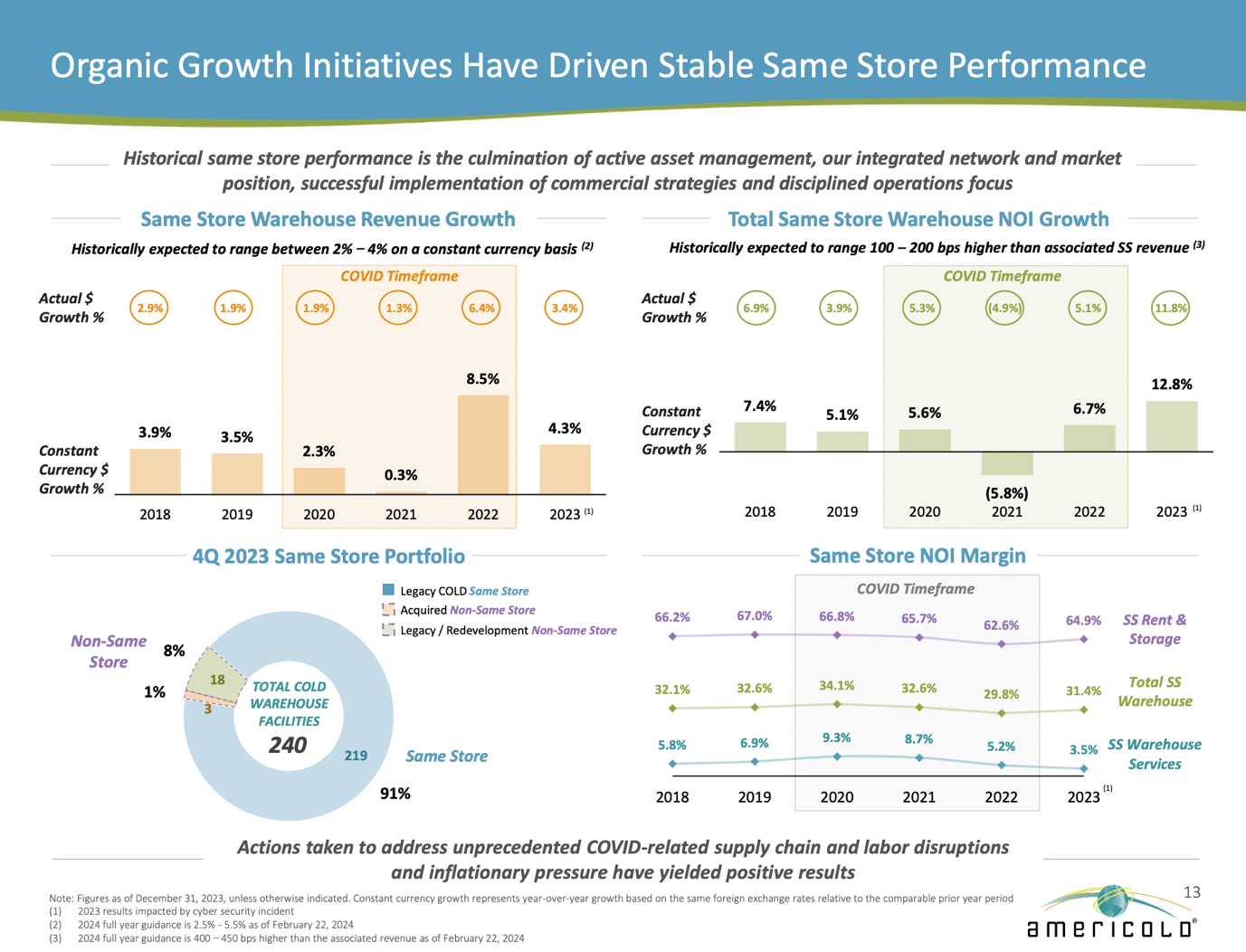

In terms of same-store growth, 2023 was the company's best year since it went public, with 12.8% constant-currency same-store warehouse NOI growth.

Americold

It also has a great balance sheet, with zero maturing debt in 2024 and 2025, $800 million in liquidity, 92% unsecured debt, 88% fixed-rate debt, and an investment-grade credit rating of BBB from Fitch.

The company also pays a dividend. Currently, it pays $0.22 per share per quarter, which translates to a yield of 3.3%. This dividend has a 2024E AFFO payout ratio.

Unfortunately, the company has not hiked its dividend since 2021.

The good news is that I expect dividend growth to pick up in the future. Not only is the dividend protected by a low payout ratio, but it is also expected to benefit from consistently elevated AFFO growth.

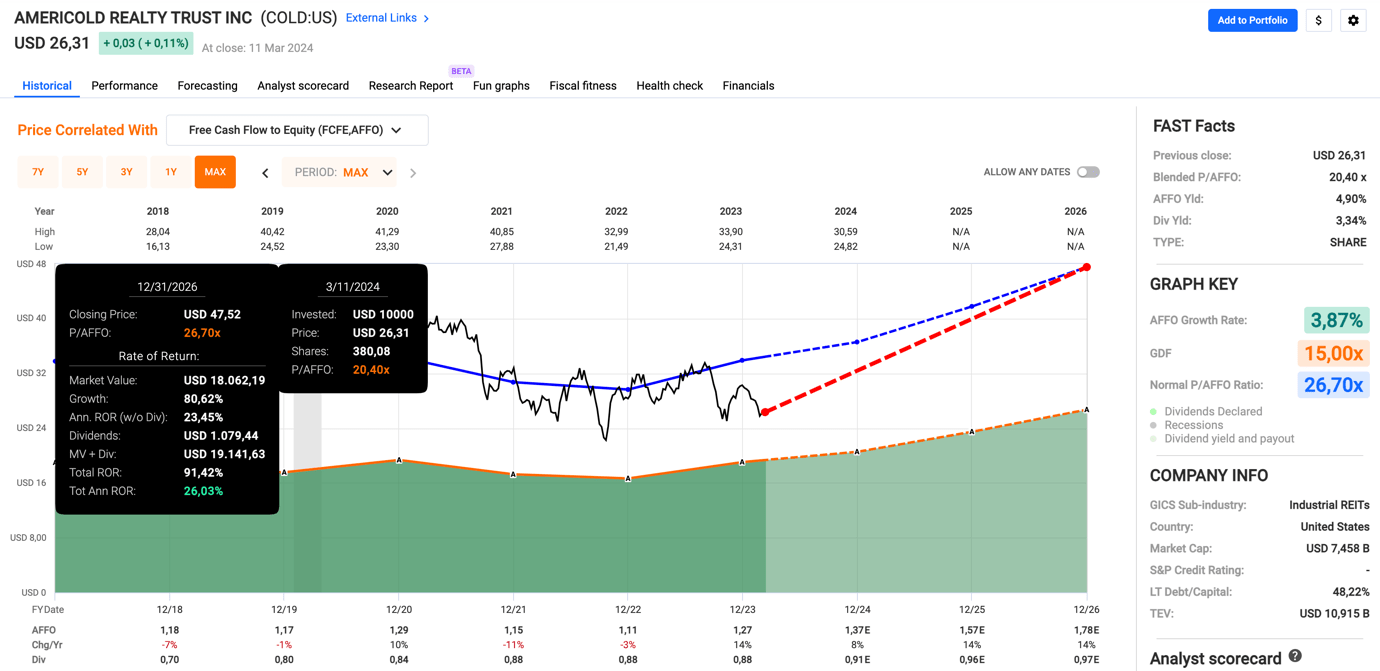

COLD currently trades at a blended P/AFFO ratio of 20.4x, which is below its long-term normalized ratio of 26.7x.

FAST Graphs

This year, AFFO growth is expected to be 8%, potentially followed by 14% growth in both 2025 and 2026!

Hence, COLD has a path to a stock price of $48, which is more than 80% above its current price.

Although it will likely take time until so much value is unlocked, the valuation is attractive, and I really like this wide-moat business model in one of the world's most important supply chains.

In the first part of this article, I mentioned CPKC, the railroad that connects sellers to buyers.

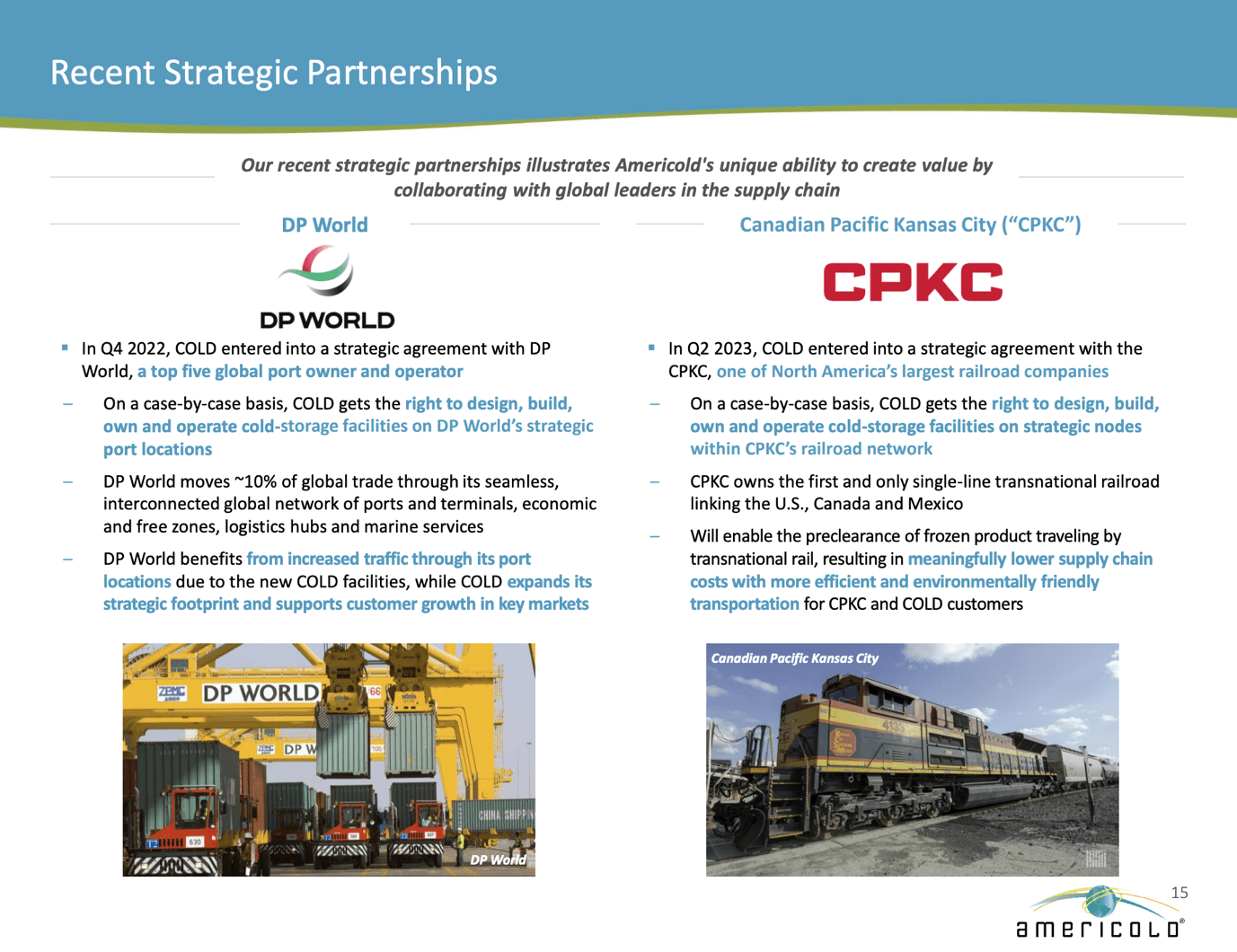

As we can see below, a big part of COLD's success is partnering with companies that allow its warehouses to thrive.

That's where CPKC comes in.

The company entered into a strategic agreement with COLD. COLD has the right to design, build, own, and operate its facilities on strategic nodes of CPKC's network.

Americold

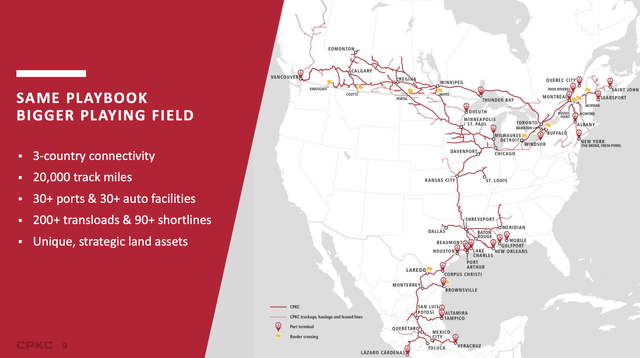

This is a huge deal, as CPKC is the FIRST railroad that connects all North American nations through its own network.

See, CPKC connects Canada, the United States, and Mexico through a network that spans 20,000 miles. This network connects more than 30 ports and 30 auto facilities.

Canadian Pacific Kansas City

Food transportation is just a small part of its operations.

It also transports bulk, merchandise, and intermodel. This includes a lot of Canadian and American grains, coal, fertilizers, and energy commodities.

Canadian Pacific Kansas City

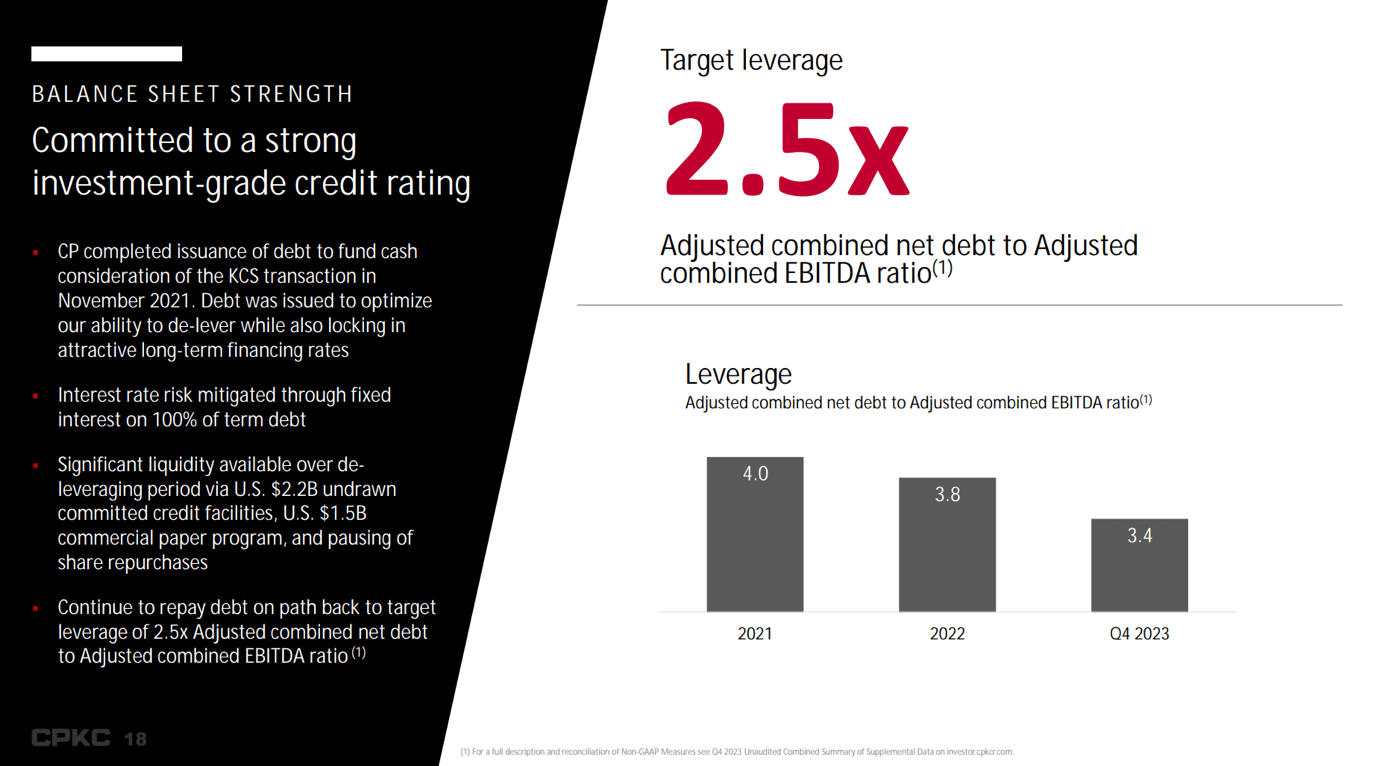

As some readers may know, CPKC is the result of a merger between Canadian Pacific and Kansas City Southern. This deal resulted in a 4.0x leverage ratio in 2021, which halted all buybacks and froze dividend growth.

Hence, the company yields less than 1% while I am writing this.

However, there is good news. The company is on pace to reach its leverage ratio potentially in 2024 or early 2025, which unlocks new dividend growth and buybacks.

Canadian Pacific Kansas City

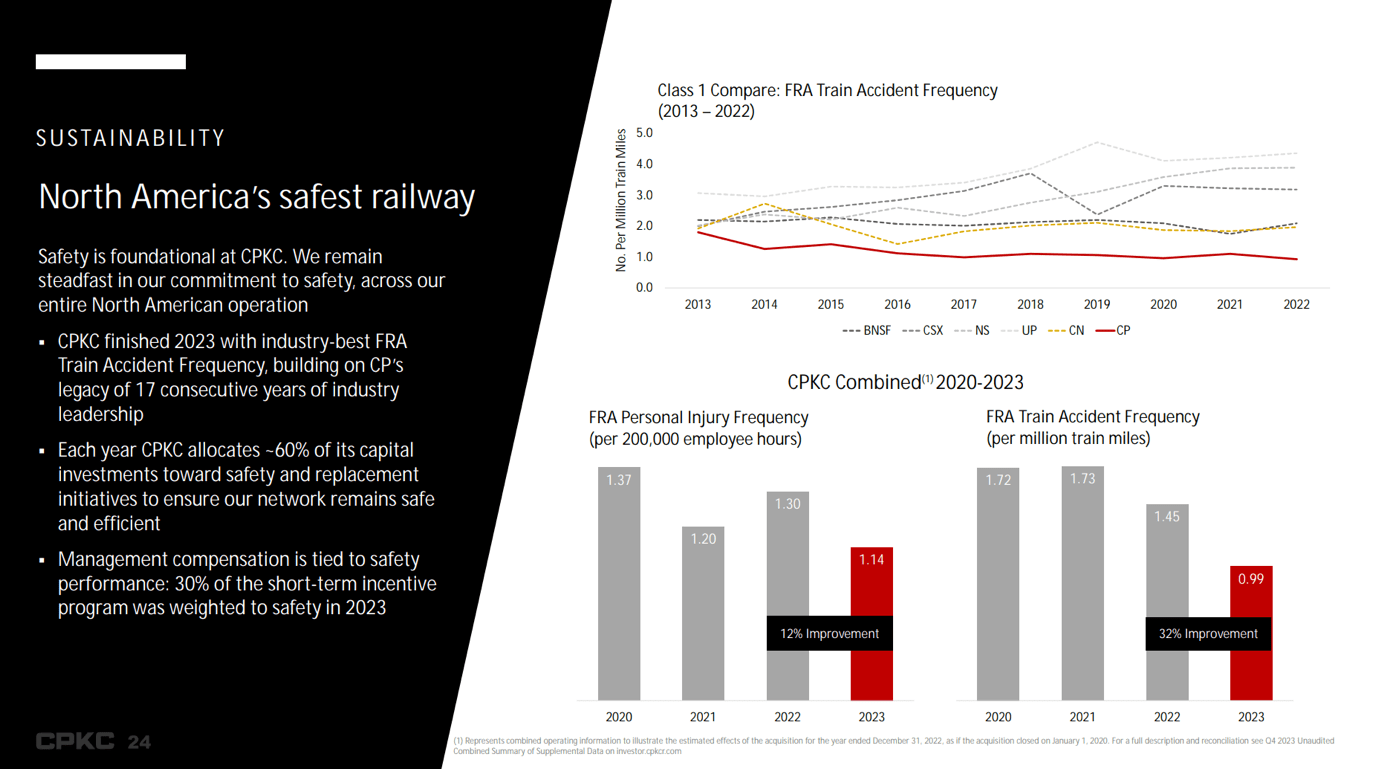

Adding to that, in light of train accidents like the one in East Palestine, Ohio, it needs to be said that CPKC is the safest Class I railroad in North America. It has the best accident rates for both its trains and employees.

In fact, it is also one of the most efficient railroads without sacrificing safety. As a shareholder, this is very important to me.

Canadian Pacific Kansas City

While CPKC is not "cheap," it benefits from massive merger synergies, as it is currently building a North American network that enjoys secular tailwinds like economic re-shoring, increasing agriculture and energy exposure, and strategic deals like the one with COLD.

As a result, the company expects to grow its revenues by high-single-digits every year, potentially leading to double-digit annual EPS growth.

This bodes well for its valuation, which does not appear to be cheap.

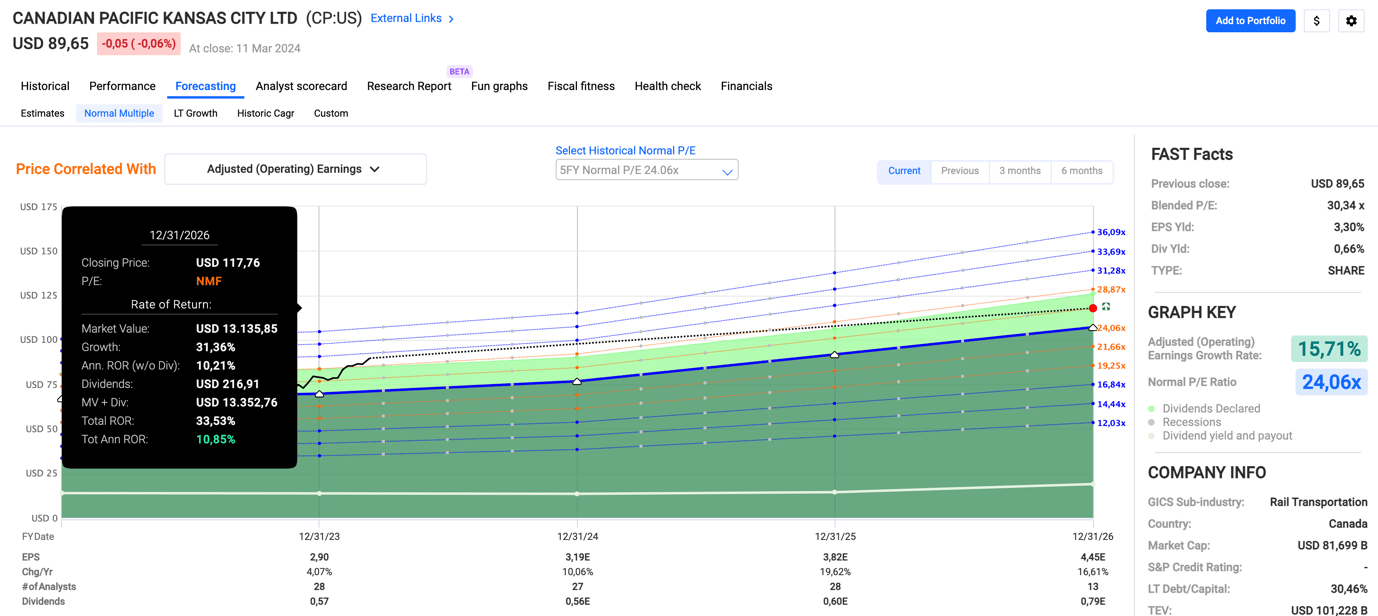

CP currently trades at a blended P/E ratio of 30.3x. While that may seem like a lot, the company is expected to grow its EPS by 10% this year, potentially followed by 20% next year and 17% growth in 2026.

FAST Graphs

This paves the way for >10% annual returns.

While economic headwinds could keep these returns subdued, I am looking to expand my investment in any corrections.

All things considered, I believe the three supply chain plays in this article all bring unique characteristics to the table.

On a long-term basis, I expect all of these investments to beat the S&P 500.

Author's note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: written and distributed only to assist in research while providing a forum for second-level thinking.