jetcityimage

jetcityimage

Coca-Cola Consolidated, Inc. (NASDAQ:COKE) is the largest bottler of The Coca-Cola Company's (KO) products. In its most recent results, the company piggy-backed off of the strong growth that Coca-Cola experienced both during the quarter and for the full year. With modest volume growth, the company was also able to support pricing growth and improved efficiencies which led to higher margins at the company. In this article, I'll walk through the recent quarter and full-year results and provide commentary on the future outlook and valuation. To avoid confusion between Coca-Cola Consolidated and The Coca-Cola Company, I will henceforth in this article refer to the former as COKE and the latter as KO when discussing the two companies.

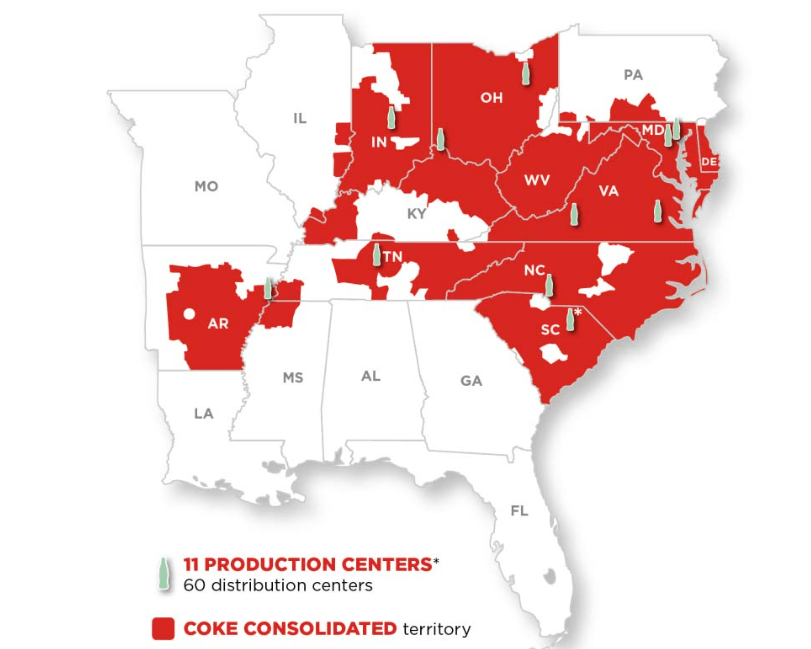

As the largest bottler for Coca-Cola products, COKE has a 120 year history that's almost as old as KO itself. With a dominant presence in the Southeast, Midwest, and Mid-Atlantic regions of the United States, the company has 60 distribution centers across 14 states and serve about 60 million consumers. The company manufacturers many Coca-Cola products including colas, bottled waters, iced teas, juices, and sports drinks.

Geographic Reach (Company Website)

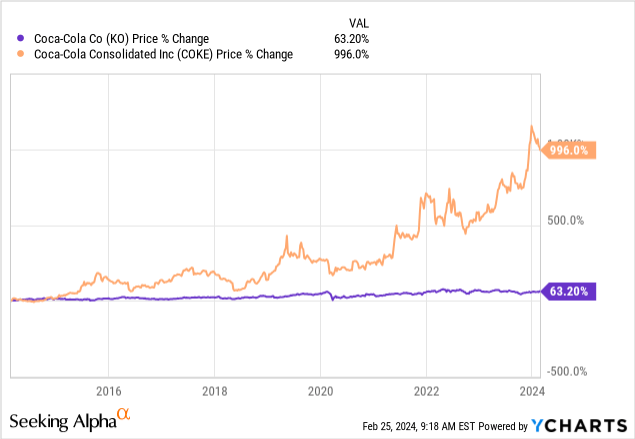

As the primary bottler for Coca-Cola products, I thought it would be interesting to compare COKE to KO. As shown by the graph below, COKE has significantly outperformed KO in terms of its share price performance. In the last ten years, shares of COKE have gone up almost 11-fold while KO's shares are up just 63.2%. That said, keep in mind that KO distributes a significantly higher portion of its free cash flow compared to COKE as a dividend, with shares of KO yielding 3.2% and shares of COKE yielding 1.9%. Nonetheless, even when accounting for dividends over the period, COKE has totally outperformed, returning a compounded annual growth rate of 27.1%.

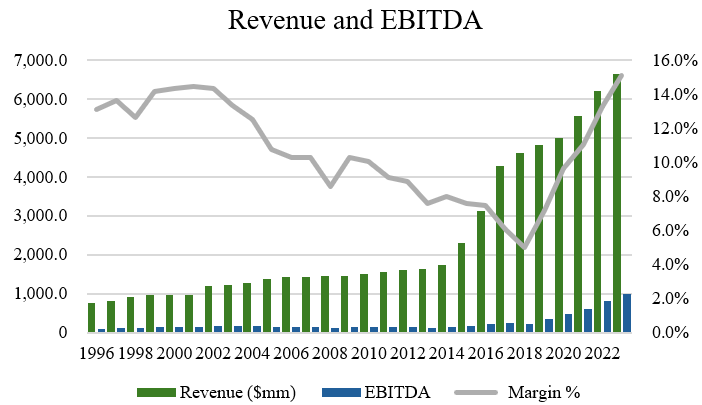

Over the years, Coca-Cola Consolidated has put up impressive results on both the top and bottom line. In the last two decades, revenue and EBITDA have compounded at CAGRs of 8.9% and 9.5%, respectively. Over the last ten years, revenues and EBITDA have compounded at CAGRs of 15.0% and 23.2%, respectively (source: S&P Capital IQ). With the EBITDA growth rate exceeding the revenue growth rate, this demonstrates that margins have expanded steadily over time. Moreover, with the 10-year period figures higher than their respective 20-year figures, this illustrates that the company's growth rate has accelerated.

Author, based on data from S&P Capital IQ

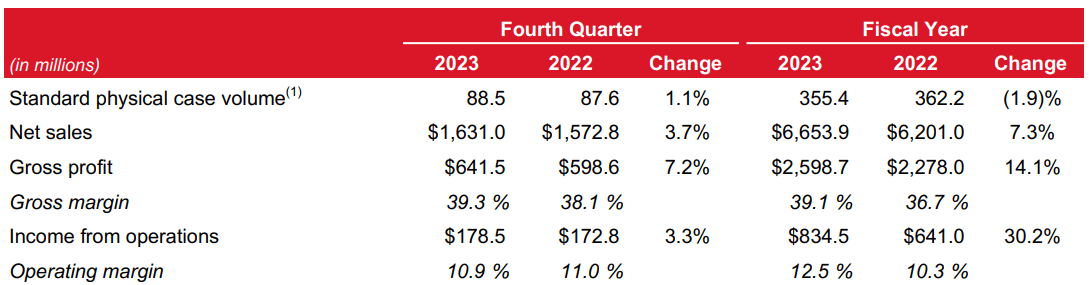

When looking at the recent Q4 results announced on February 22 for COKE, the company saw quarterly sales rise 3.7% year over year. This was driven by modest growth in volumes, where physical case volumes rose 1.1%. Making up the difference between the two figures was pricing increases. On a full-year basis, sales were up 7.3% despite a 1.9% decline in volumes.

Company Filings

Breaking the results down by category shows that much of the results are being driven by the sparkling and still categories, which experienced a 10.5% and 6.4%, respectively for the full-year. Increased demand from retail stores during holiday periods as well as brand uptake amongst Monster, smartwater, vitaminwater and Gold Peak products contributed to this growth.

As a benchmark, comparing COKE's results to KO, the latter had higher revenue growth of 12% for the quarter, with 140 basis points of gross margin expansion for the quarter. In the case of COKE, gross margins expanded 120 basis points which led to a 7.2% increase in gross profit for the year. One of the reasons for KO's higher revenue growth rate is due to its international exposure.

Unlike COKE which operates in select regions of the United States, KO has a growing international presence. During the quarter, KO saw strong growth in Australia, India, Latin America, and Japan. While U.S. growth is comparable to COKE, it's noteworthy to mention that COKE only has bottling rights in the regions it currently operates in and so it can't be expected that COKE will pick up market share gains or growth in international markets.

While COKE doesn't provide guidance or forecasts on the company's future (there are no analyst calls), KO's quarterly conference call did provide some indications on how we might expect COKE to fare.

For example, on the conference call, management noted that they continue to make progress refranchising company owned bottling operations, meaning that are essentially selling their bottling operations to other third-party companies. This has been a trend by most beverage companies in recent years to partner with bottling manufacturers rather than bottling themselves. Even though COKE is the largest bottler of KO's products, there are still around 200 similar companies around the world doing essentially the same thing.

The reason for this is to essentially run a tight ship, keeping margins high and operating an asset light model. So contracting to bottling manufacturers is a win-win as the bottlers have a steady stream of cash flows with a predictable business model and companies like KO and Pepsi (PEP) can focus on building asset-light businesses with a focus on capital efficiency, building out new product innovations, and focus their cash flows elsewhere.

As for my outlook on the company's future, COKE seems to be in a good position going forward to benefit off of the U.S. consumer. In the last seven years, the revenue growth rate of the U.S. has actually been slightly higher than the rest of KO's international exposure. While Latin America has been growing faster, KO has been able to grow sales faster through pricing increases compared to volume increases.

Author, based on data from S&P Capital IQ

Right now, the health of the U.S. consumer looks to be strong. And if you have the belief that I do that things are likely to improve from here, then the near-term outlook for both COKE and KO look very solid. KO expects that next year should bring about mid-single-digit sales growth as a whole for the company and I like the company's positioning relative to Pepsi. With the 2% beverage volume expansion for KO, Pepsi actually saw a 1% contraction so much of the advertising and marketing KO has been investing in has been working. The nice thing about investing in COKE vs KO is that one can benefit off of the health of the U.S. consumer (relative to a weaker international consumer) and also not have to worry about the heavy marketing and advertising costs that KO is left with the burden with. An investment in COKE over KO also has the added benefit of not having any foreign currency exposure, compared to KO which two-thirds of its revenue being generated internationally.

Finally, on the balance sheet front, COKE has a very conservative balance sheet with $599.1 million of long-term debt (most of which is made up of senior bonds at 3.8%), up slightly from last year. Its credit ratings are BBB rated from both Moody's and S&P suggesting a stable outlook and investment grade rating. Of note is that a substantial portion of long-term debt is coming due in the next 3 years, so it's likely that the company may need to refinance at higher rates. That said, the debt load is fairly small and is manageable at 0.6x EBITDA.

Company Filings

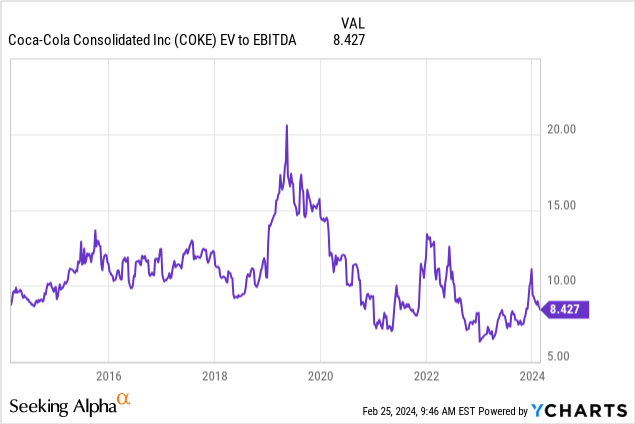

At present, there are no analysts covering COKE, despite its market-capitalization close to $7.8 billion and the huge analyst following of KO. When analyzing the historical valuation of COKE, the company trades for about 8.4x EV/EBTIDA on a TTM basis, which is close to the lower-end of its historical valuation range. On a P/E basis, the company trades for about 19.1x earnings.

Comparing KO to COKE, it would seem that despite its higher growth rate, the market has given KO a premium valuation over COKE. KO trades for 17.9x EBITDA and 24.8x earnings.

One reason I suspect that KO trades at a higher valuation is that KO may decide that it may want to do its own bottling in house and no longer use COKE. I view this as unlikely, given that KO has nearly a 30% economic interest in COKE. More likely than bringing things in house is that KO acquires the remaining interests of COKE which would likely be done at a premium to the prevailing market price.

While I don't foresee a buyout or acquisition by KO anytime soon, I also don't foresee much risk to KO that I wouldn't see for COKE. The health of the U.S. consumer, competition from competitor products like Pepsi, and higher raw material prices are all things to watch.

In summary, COKE reported some great results and I see no reason why that shouldn't continue. With a valuation close to the historical lows of its valuation range, shares provide a compelling company to buy a quality business at a fair price. At 8.4x EV/EBITDA and 19.1x earnings, the valuation seems like a reasonable price. As such, I'd recommend a buy rating on the company's shares.